Nope. It’s now up to $9 billion of shareholder money lost by Jamie Dimon on one freaking trade. ONE FREAKING DERIVATIVES TRADE!!!!

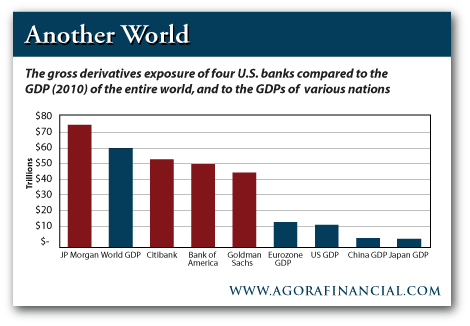

Dimon is the superstar of Wall Street. He is Obama’s best buddy. Once Corzine got caught fucking his shareholders and depositors, Dimon went to the head of the list for next Treasury Secretary. Based on his recent performance he would make a perfect Treasury Secretary. We lose $9 billion dollars every three days. It took him a few weeks. Now for the best part. Check out JP Morgan’s total derivatives exposure. It is $10 trillion more than WORLD GDP. It is more than 4 times the U.S. GDP. This is one freaking bank!!!!

These parasitic bankers are going to blow up the entire world and we sit idly by watching it happen and doing nothing to prosecute or rein in these criminals. How can the JP Morgan Board of Directors allow this shithead to destroy their company and the world economy. It’s because these Boards are nothing but cronies of the CEO who are part of the criminal conspiracy.

When these derivatives bets start going bad across the board (because all the Wall Street banks are lemmings and make the same exact trades) we will again be subject to the fear mongering politicians screaming that we must save the economic system before its too late and bail these fuckers out again. When will it stop?

Latest Press: JPMorgan Loss As Large As $9 Billion

Submitted by Tyler Durdenon 06/28/2012 07:38 -0400

We have long said that the maximum potential loss of the JPM CIO trade based on the blow out in IG9 10 year (and associated trades complex), which has about a $200 million DV01, is far beyond not only the $2 billion that Jamie Dimon estimated on May 10, but above our own estimate which was $5 billion on that same day. Today, the NYT “according to people who have been briefed on the situation” which translated means just more media propaganda because all the news on the topic in the past month has been leaks by axed parties, says that ‘Losses on JPMorgan Chase’s bungled trade could total as much as $9 billion, far exceeding earlier public estimates, according to people who have been briefed on the situation.” Also according to the NYT, and roundly refuting what the other leak had told Bloomberg and other media outlets, “The bank’s exit from its money-losing trade is happening faster than many expected. JPMorgan previously said it hoped to clear its position by early next year; now it is already out of more than half of the trade and may be completely free this year.” Obviously, this refutes media “reports” also based on “people familiar” or “conflicted sources” that JPM has unwound its trade, either by novating, or by transferring it over to helpful hedge funds. Bottom line: take everything with a grain of salt until Dimon himself gives an update in two weeks, as this could easily be an upper bound loss estimate starwman to set expectations very low, sending the stock soaring when the “final” announce loss comes in at ~$5 billion, courtesy of other well-known “masking” techniques such as loan loss reserve release and DVA benefits.

More:

As JPMorgan has moved rapidly to unwind the position — its most volatile assets in particular — internal models at the bank have recently projected losses of as much as $9 billion. In April, the bank generated an internal report that showed that the losses, assuming worst-case conditions, could reach $8 billion to $9 billion, according to a person who reviewed the report.

With much of the most volatile slice of the position sold, however, regulators are unsure how deep the reported losses will eventually be. Some expect that the red ink will not exceed $6 billion to $7 billion.

Nonetheless, the sharply higher loss totals will feed a debate over how strictly large financial institutions should be regulated and whether some of the behemoth banks are capitalizing on their status as too big to fail to make risky trades.

JPMorgan plans to disclose part of the total losses on the soured bet on July 13, when it reports second-quarter earnings. Despite the loss, the bank has said it will be solidly profitable for the quarter — no small achievement given that nervous markets and weak economies have sapped Wall Street’s main businesses. To put the size of the loss in perspective, JPMorgan logged a first-quarter profit of $5.4 billion.

More than profits are at stake. The growing fallout from the bank’s bad bet threatens to undercut the credibility of Mr. Dimon, who has been fighting major regulatory changes that could curtail the kind of risk-taking that led to the trading losses. The bank chief was considered a deft manager of risk after steering JPMorgan through the financial crisis in far better shape than its rivals.

“Essentially, JPMorgan has been operating a hedge fund with federal insured deposits within a bank,” said Mark Williams, a professor of finance at Boston University, who also served as a Federal Reserve bank examiner.

A spokesman for the bank declined to comment.

In other words: the world’s largest prop trading deks, with a $200 million DV01, as Zero Hedge readers have now known for just under two months.

Ive said about the same.There should be a site that keeps track of all these crooks and the things they did.

I wonder how many of Obamas buddys make out like bandits with the court ruling against personal freedom.

There was a post on Zero Hedge the other day estimating that, net net, a loss of $50 Billion might render JP Morgan insolvent. With a gross derivatives exposure of about $75 Trillion, a loss on the unwinding of the gross derivatives position of any more than 0.1% ($75 Billion) would certainly do the trick.

Net net. A powerful concept. Unlike mark-to-market, net net cannot be legislated away. Net net, you’re either solvent, or you’re not.

There are only about $800 Billion in cash dollars currently circulating the planet. There are a lot of potentially competing claims on those dollars — upwards of $700 Trillion in gross notional terms. How optimistic and unrealistic to think that it will all net out anywhere close to $0

Net net, the coming scramble for dollars (existing and yet to be printed) should be a sight to behold.

Another worthwhile source:

http://www.teribuhl.com/

and another JPMC story earlier:

fun fun fun for Jamie