The report from RealtyTrac last week proves beyond the shadow of a doubt the supposed housing market recovery is a complete and utter fraud. The corporate mainstream media did their usual spin job on the report by focusing on the fact foreclosure starts in 2013 were the lowest since 2007. Focusing on this meaningless fact (because the Too Big To Trust Wall Street Criminal Banks have delayed foreclosure starts as part of their conspiracy to keep prices rising) is supposed to convince the willfully ignorant masses the housing market is back to normal. It’s always the best time to buy!!!

The talking heads reading their teleprompter propaganda machines failed to mention that distressed sales (short sales & foreclosure sales) rose to a three year high of 16.2% of all U.S. residential sales, up from 14.5% in 2012. The economy has been supposedly advancing for over four years and sales of distressed homes are at 16.2% and rising. The bubble headed bimbos on CNBC don’t find it worthwhile to mention that prior to 2007 the normal percentage of distressed home sales was less than 3%. Yeah, we’re back to normal alright. We are five years into a supposed economic recovery and distressed home sales account for 1 out of 6 all home sales and is still 500% higher than normal.

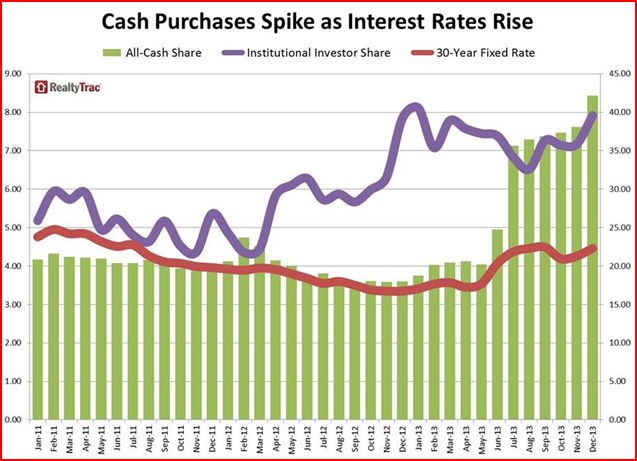

The distressed sales aren’t even close to the biggest distortion of this housing market. The RealtyTrac report reveals that all-cash purchases accounted for 42% of all U.S. residential sales in December, up from 38% in November, and up from 18% in December 2012. Does that sound like a trend of normalization? There were five states where all-cash transactions accounted for more than 50% of sales in December – Florida (62.5%), Wisconsin (59.8%), Alabama (55.7%), South Carolina (51.3%), and Georgia (51.3%). In the pre-crisis days before 2008, all-cash sales NEVER accounted for more than 10% of all home sales. NEVER. This is all being driven by hot Wall Street money, aided and abetted by Bernanke, Yellen and the rest of the Fed fiat heroine dealers.

Source: Realty Trac

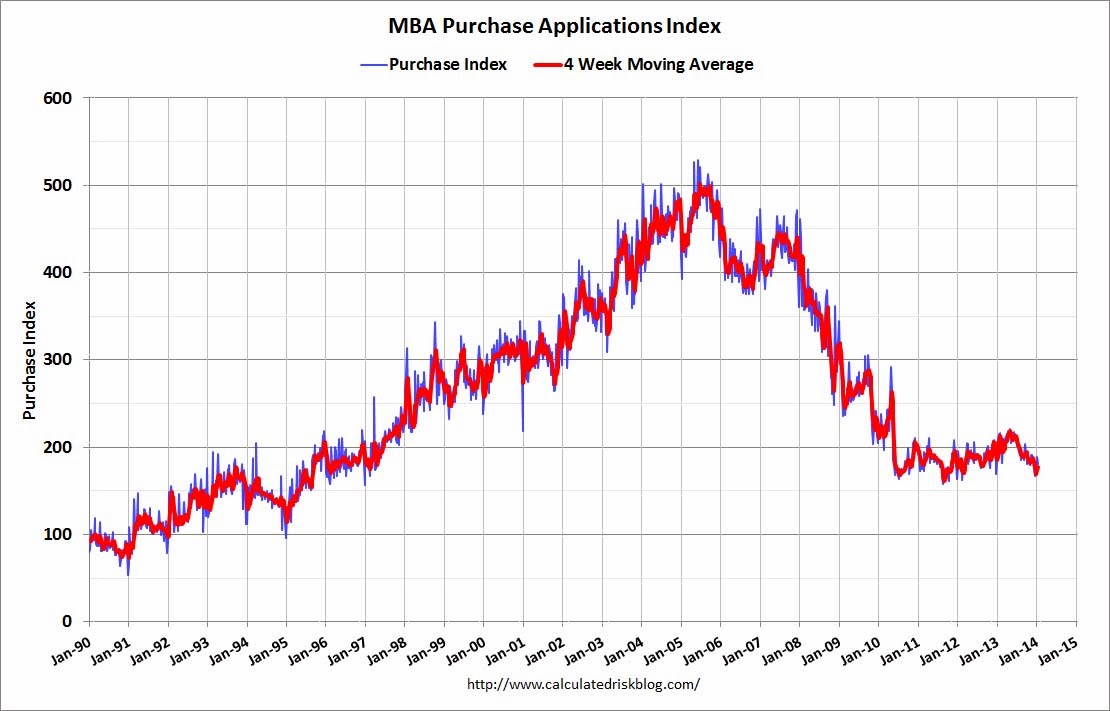

The fact that Wall Street is running this housing show is borne out by mortgage applications languishing at 1997 levels, down 65% from the 2005 highs. Real people in the real world need a mortgage to buy a house. If mortgage applications are near 16 year lows, how could home prices be ascending as if there is a frenzy of demand? Besides enriching the financial class, the contrived elevation of home prices and the QE induced mortgage rate increase has driven housing affordability into the ground. First time home buyers account for a record low percentage of 27%. In a normal non-manipulated market, first time home buyers account for 40% of home purchases.

Price increases that rival the peak insanity of 2005 have been manufactured by Wall Street shysters and the Federal Reserve commissars. Doctor Housing Bubble sums up the absurdity of this housing market quite well.

The all-cash segment of buyers has typically been a tiny portion of the overall sales pool. The fact that so many sales are occurring off the typical radar suggests that the Fed’s easy money eco-system has created a ravenous hunger with investors to buy up real estate. Why? The rentier class is chasing yields in every nook and cranny of the economy. This helps to explain why we have such a twisted system where home ownership is declining yet prices are soaring. What do we expect when nearly half of sales are going to investors? The all-cash locusts flood is still ravaging the housing market.

The Case-Shiller Index has shown price surges over the last two years that exceed the Fed induced bubble years of 2001 through 2006. Does that make sense, when new homes sales are at levels seen during recessions over the last 50 years, and down 70% from the 2005 highs? Even with this Fed/Wall Street induced levitation, existing home sales are at 1999 levels and down 30% from the 2005 highs. So how and why have national home prices skyrocketed by 14% in 2013 after a 9% rise in 2012? Why are the former bubble markets of Las Vegas, Los Angeles, San Diego, San Francisco and Phoenix seeing 17% to 27% one year price increases? How could the bankrupt paradise of Detroit see a 17.3% increase in prices in one year? In a normal free market where individuals buy houses from other individuals, this does not happen. Over the long term, home prices rise at the rate of inflation. According to the government drones at the BLS, inflation has risen by 3.6% over the last two years. Looks like we have a slight disconnect.

This entire contrived episode has been designed to lure dupes back into the market, artificially inflate the insolvent balance sheets of the Too Big To Trust banks, enrich the feudal overlords who have easy preferred access to the Federal Reserve easy money, and provide the propaganda peddling legacy media with a recovery storyline to flog to the willingly ignorant public. The masses desperately want a feel good story they can believe. The ruling class has a thorough understanding of Edward Bernays’ propaganda techniques.

“The conscious and intelligent manipulation of the organized habits and opinions of the masses is an important element in democratic society. Those who manipulate this unseen mechanism of society constitute an invisible government which is the true ruling power of our country. …We are governed, our minds are molded, our tastes formed, our ideas suggested, largely by men we have never heard of.”

Ben Bernanke increased his balance sheet by $3.2 trillion (450%) since 2008, and it had to go somewhere. We know it didn’t trickle down to the 99%. It was placed in the firm clutches of the .1% billionaire club. Bernanke sold his QE schemes as methods to benefit Main Street Americans, when his true purpose was to benefit Wall Street crooks. 30 year mortgage rates were 4.25% before QE2. 30 year mortgage rates were 3.5% before QE3. Today they stand at 4.5%. QE has not benefited average Americans. They are getting 0% on their savings, mortgage rates are higher, and their real household income has fallen and continues to fall.

But you’ll be happy to know banking profits are at all-time highs, Blackrock and the rest of the Wall Street Fed front running crowd have made a killing in the buy and rent ruse, and record bonuses are being doled out to the men who have wrecked our financial system in their gluttonous plundering of the once prosperous nation. Their felonious machinations have added zero value to society, while impoverishing a wide swath of America. Bernanke, Yellen and their owners have used their control of the currency, interest rates, and regulatory agencies to create the widest wealth disparity between the haves and have-nots in world history. Their depraved actions on behalf of the .1% will mean blood.

Just as Greenspan’s easy money policies of the early 2000’s created a housing bubble, inspiring low IQ wannabes to play flip that house, Bernanke’s mal-investment inducing QEternity has lured the get rich quick crowd back into the flipping business. The re-propagation of Flip that House shows on cable is like a rerun of the pre-bubble bursting frenzy in 2005. RealtyTrac’s recent report details the disturbing lemming like trend among greedy institutions and dullard brother-in-laws across the land.

- 156,862 single family home flips — where a home is purchased and subsequently sold again within six months — in 2013, up 16% from 2012 and up 114% from 2011.

- Homes flipped in 2013 accounted for 4.6% of all U.S. single family home sales during the year, up from 4.2% in 2012 and up from 2.6% in 2011

Source: Realty Trac

The easy profits just keep flowing when the Fed provides the easy money. What could possibly go wrong? Home prices never fall. A brilliant Ivy League economist said so in 2005. The easy profits have been reaped by the early players. Wall Street hedge funds don’t really want to be landlords. Flippers need to make a quick buck or their creditors pull the plug. Home prices peaked in mid-2013. They have begun to fall. The 35% increase in mortgage rates has removed the punchbowl from the party. Anyone who claims housing will improve in 2014 is either talking their book, owns a boatload of vacant rental properties, teaches at Princeton, or gets paid to peddle the Wall Street propaganda on CNBC.

Reality will reassert itself in 2014, with lemmings, flippers, and hedgies getting slaughtered as the housing market comes back to earth with a thud. The continued tapering by the Fed will remove the marginal dollars used by Wall Street to fund this housing Ponzi. The Wall Street lemmings all follow the same MBA created financial models. They will all attempt to exit the market simultaneously when their models all say sell. If the economy improves, interest rates will rise and kill the housing market. If the economy tanks, the stock market will plunge, creating fear and killing the housing market. Once it becomes clear that prices have begun to fall, the flippers will panic and start dumping, exacerbating the price declines. This scenario never grows old.

Real household income continues to fall and nearly 25% of all households with a mortgage are still underwater. Young people are saddled with $1 trillion of government peddled student loan debt and will not be buying homes in the foreseeable future. Dodd-Frank rules will result in fewer people qualifying for mortgages. Mortgage insurance is increasing. Obamacare premium increases are sucking the life out of potential middle class home buyers. Retailers have begun firing thousands. The financial class had a good run. They were able to re-inflate the bubble for two years, but the third year won’t be a charm. In a normal housing market 85% of home sales would be between individuals using a mortgage, 10% would be all cash transactions, less than 5% of sales would be distressed, and 40% would be first time buyers. In this warped market only 40% of home sales are between individuals using a mortgage, 42% are all cash transactions, 16% are distressed sales, 5% are flipped, and only 27% are first time buyers. The return to normalcy will be painful for shysters, gamblers, believers, paid off economists, Larry Yun, and CNBC bimbos.

[img [/img]

[/img]

That they were even able to reinflate in markets like Phoenix and Detroit just blows my mind. It truly demonstrates just how unpredictable all of it really is. Where things will go next is anyone’s guess. Any true measure of reality would demand that home prices crash and crash hard but, these clowns at the Fed have been able to juggle these knives a lot longer than I ever thought possible.

If one year of 1% interest rates under Greenspan gave us what was then the largest asset bubble in world history, imagine what 0% for 5 years (and counting) under Bernanke will do! It’s going to be horrific.

We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.”

Ben Bernanke – July 2005

“House prices have risen by nearly 25 percent over the past two years. Although speculative activity has increased in some areas, at a national level these price increases largely reflect strong economic fundamentals.”

Ben Bernanke – October 2005

“Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.”

Ben Bernanke – February 2006

“Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low.”

Ben Bernanke – February 2007

“The Federal Reserve is not currently forecasting a recession.”

Ben Bernanke – January 2008

“The continuing shortages of housing inventory are driving the price gains. There is no evidence of bubbles popping.”

David Lereah, NAR’s chief economist, August 2005

“We are really on track for a soft landing. There are no balloons popping.”

David Lereah, NAR’s chief economist, December 2005

“It appears we have established a bottom.”

David Lereah, NAR’s chief economist, January 2007

Housing is a can’t miss investment. Just ask the average American and their surging household income.

[img [/img]

[/img]

The future for housing is so bright, you gotta wear shades.

[img [/img]

[/img]

Well, not to put a positive slant on it mind you, God forbid that TEOTWAWKIT, gets delayed. But. it is not meaningless that foreclosure starts were at a seven year low. The fact that mortgage holders have held off dumping foreclosed properties on the market as well, is probably a better decision than flooding the markets and causing a total collapse.

I am no fan of the thieving, criminal, “Banksters” but, for the moment it ain’t as bad as it could have been. I swear sometimes it seems like people are trying to push the news to cause a Mad Max world, rather than highlight something good for a change.

Are purchases of high-end houses by the 1% skewing the higher-price per home numbers?

Hard to believe mid-range houses in places like Detroit and Vegas are trending higher…or are

the institutional buyers driving up the prices?

Institutional buyers and the Chinese are driving the prices higher.

We can’t talk about what we are not supposed to talk about. How many of those subprime foreclosure’s are unsaleable at any price given the locations they’re in?

Given that, what would you do with who ever has the mortgages?

Have the bank set up a phoney subsidiary and rent them out to the government (section 8)?

Whatever happened to Mary Malone??

So many graphs to tell us how fucked we are. It’s all true.

However, there’s a much simpler way to prove we’re fucked. The FIRST thing any mortgage broker worth his salt is to determine “How much can this person afford? And it ain’t pretty. Looking at the nation as a whole you only need to look at two raw numbers and calculate a third.

Given that;

1)—- MEDIAN FAMILY INCOME = $51,404

2)—- MEDIAN HOME PRICE 2013 = $203,500

Therefore,

————– the median family can afford a home that costs $145,788.

Since,

————– $145,758 is less than $203,500

We can safely conclude that

. ———– THE AVERAGE FAMILY CANNOT AFFORD A MEDIAN PRICED HOME IN THE USA

Which means,

. ———– the next fucking housing bubble-burst is coming soon to a theater near you

.

.

Median home price stat —

YOU GUYS better put your god, money off to the side and take a look at whats really going on in america,YOUR about to see more then a crash,YOUR ABOUT to see nuclear war,PLANET WIDE,and it won’t be funny for the ones in cities or near them,OBOOZO is fixing to become dictator and chief,and when he tries,your going to see blood running in the streets everywhere in america,and ALL that housing you guys are worring about ,will be BURNED TO THE GROUND,guaranteed..YOU know when the poor have lost everything they LOSE IT,and that is exactly where america is at RIGHT NOW,one more trip wire and it will be on,HOPE you got a good place to hide,your about to need it……..

Arizona

I’ll bet you were a real blast at your Super Bowl party yesterday.

AMERICA HAS BECOME THE MOST “GODLESS ” nation on the planet,sick and depraved,attacking other nations,robbing anyone who can’t fight back,murdering millions of innoucent women and children,EVERYWHERE,how long do the decieved idiots in america think they can keep doing this,forever,NO you ain’t ,THEIR WIDE AWAKE,and really pissed off,AND NOW THEIR HERE in america ,just waiting for the word to attack,and they will,thanks to oboozo and his banker friends at the fed,they see the storm coming,and will do anything it takes to protect themselves,INCLUDING starting a war….THIS country has been divided up like a big fat pie,with every foreign nation having been given a extra big piece,namely china and russia,WAKEUP,….RED DAWN is on you………………..

Every mortgage has an acceleration (demand) clause. Do you understand why? It’s designed to be triggered when a homeowner might want to foreclose ….. and it then allows the bank (mortgagee) an attempt to recover the entire unpaid value of the mortgage (instead of just missed payments).

I am certainly no banker, but what benefit is there to the bank to accelerate payment? A homeowner in foreclosure almost certainly has few, if any, recoverable assets. I believe an active mortgage is an asset to the bank which provides an income stream. A dead mortgage is a liability, provides no income, and creates a whole lot of problems for the bank. Again, how does the bank benefit?

In other words, what the hell are you implying? (I can’t fuckin’ believe I responded to you.)

******************** matslinger POLLUTION Alert !!!! ********************

fuckme.

In other words, the middle class must become renters; Obama welcomes you all to the Federal Reserve Plantation where the elite that raise their cattle and pigs in the sky, own a controlling interest in our government and every big business, earn 500 times what the people actually doing the work earn, who try to fill your minds with crap from their Mass Media will now also be your landlord.

“In other words, the middle class must become renters; ” ——– robert h siddell jr

Yup.

Although I must quibble with “must become”. We already are, and have always been (in the modern ers) a nation of renters. Property Taxes = you never ever truly own your home. You pay rent to the government, and if you don’t, owning Title doesn’t mean jack shit … see ya!

Many good posts here and many very angry ones about our country as well – as they should be.

At the risk of derision by others, I will say again that venting solves nothing. I’ve been guilty of this myself.

Citizens have only two options –

1. Stand up for themselves by reforming government to make the changes necessary for most to have enough opportunity to prosper OR

2. Sit back, be quiet, complacent, subservient – and continue to be exploited and face increasing hardship and poverty – and a hopeless future.

The Admin always points out the truth because he knows the facts and does the research. He knows what propaganda is. However the bottom-line is that if citizens won’t completely reform government beginning by replacing republicans and democrats to help themselves, they have no right to complain about anything.

I assume most who visit this site are either independents or libertarians but perhaps I’m wrong. In any case, the system cannot be reformed from within. So as difficult (or perhaps impossible as some argue), as finding and electing independent political candidates is, this effort must be made. We must communicate with everyone we know to try to persuade others. Despite the odds, there is no other choice.

Just a stupid fantasy and not worth the effort?

The alternative is to remain complacent and quietly take whatever abuse ,corruption, and poverty the current political status quo hands out – which will likely mean a very bleak future for most citizens. I hope citizens have more self-respect than this.

“At the risk of derision by others, I will say again that venting solves nothing…” —— ss

You won’t be derided. TBP has some of the smartest people on the internet. Regarding prepping and changing things, as in any bell-shaped curve we have folks here who 1) just vent (few), at least do some things (most), 3) go all out (few). That’s my guess.

“I assume most who visit this site are either independents or libertarians …” —— ss

That’s correct.

@matslinger

I haven’t seen such clauses in most mortgages, well at least personal mortgages signed prior to 2007/2008.

My gut feeling was that low refi rates and the Ob ama programs like HARP, HAMP and the like were to cement title on debt/properties that were not put into contracts for years and years. Mary Malone would totally agree with that and outright said it a few times.

Such demand clauses are a huge part of the reasons that small American business has, and continues to, go dark. The freaking banksters are sucking up assets and firing employees from sea to shining sea. With both the gubment’s permissions, and orders. I followed the FDIC for a few years until the corruption and obviousness of the intentional demise of the small, independent businessman made it mentally risky to continue my knowledge acquisition.

As to why, what is the purpose, that is freaking easy.

The banksters, Section 8 renters, local property tax bureaucrats, US Congress, Ob ama administration, Wall Street, Ben Bernake, the European Union and the rich drug Lords, Chinese and Russians (and others) are amongst the reasons why they would do this.

Just wait until China calls their notes. My best guess is they will be satisfied with the trillions of dollars of mortgage debt bought/guaranteed by Benny and the Treasury.

Then these debts will be owed directly to China while we are taxed, fined and regulated to death by the local guys.

There won’t be an out for any of us if there are no new buyers. Wonder how many millennials will be hitting the lottery and magically become able to pay $1000 to college loans and $3000 for housing every month. Oh, that’s right, they’ll increase the flippin’ minimum wage!

This just keeps getting worse, deeper, more horror invoking.

I have the feeling that the American dream of home ownership hasn’t even yet begun to become the nightmare we will soon see and feel.

But, hell, once our assets are wiped out, our jobs gone, maybe we will be able to move back into our stolen homes and get Uncle Sam to pay for it.

The new American dream I guess.

“I haven’t seen such clauses in most mortgages, well at least personal mortgages signed prior to 2007/2008” —————- TeresaE

I have never NOT seen a mortgage without an acceleration clause.

“Acceleration clauses first began to appear in loan contracts in the 1970s. Due-on-sale clauses were prohibited in many states until 1982, when Congress lifted restrictions on them. Many homeowners had begun selling their homes through land contracts in the 1970s. Purchasing in this manner allowed buyers to avoid high interest rates on new home loans, which were common at the time. Typically, the seller’s title interest would be signed over to a buyer, who would also assume the old low-interest rate loan. Due-on-sale clauses effectively acted to prevent such sales.”

——– http://homeguides.sfgate.com/can-mortgage-accelerated-upon-transfer-title-7291.html

Regarding my post @11:33 ….. Average home affordability, $145,788. How I came up with that number.

Step 1: Determine monthly Debt-To-Income ratio. Basically, take gross monthly income and subtract out all monthly debts, leaving income available for the monthly mortgage payment.

Annual Income —– $51,404

Monthly income — $4,284

Subtract

——— 20% taxes (-$856)

——— Car payments, credit card bills ($426)

——— Property taxes, homeowners ins, HOA dues ($400)

Adjusted Monthly Income —– $2,600

STEP TWO: Make down payment and interest rate assumptions

——— Down Payment ———– $10,175

——— Interest Rate ————– 5%

——— Term ———————— 30 years

This calculates to a maximum monthly mortgage payment of $728, and a home of $145,788

I am trying to get signatures for the Harp 3.0 petition. Harp 3.0 would help thousands of underwater home owners refinance to todays lower rates. To date only a selected few have been helped, HARP 3.0 will help the millions of responsible HomeOwners that have a sub prime mortgage. The link provided would greatly help the responsible homeowners left out in the cold. https://petitions.whitehouse.gov/petition/help-underwater-homeowners-install-countup-clock-white-house-remind-policy-makers-failure-pass-harp/pjmvr9pc

First of all, the Fed does not print money. It cannot create new money, should it do so it would be instantly insolvent, there would be no lender(s) of last resort, there would be bank runs = Argentina (whose central bank is making unsecured loans).

Second of all, Wall Street needs higher real estate prices to balance its books going back to ’07. How to push prices? Banks lend to each other or to themselves, using funds to buy back houses by way of captive hedge funds and investment trusts.

Third, there is still secular demand for housing and low interest rates have enabled house purchases by individuals that would otherwise be out of the market. Yes, the Fed can affect interest rates, they also create moral hazard.

The problem w/ real estate is that it isn’t just housing expense, it is the added cost of the needed car. Cars are bankrupting the housing sector along with other sectors (as well as entire countries).. People claiming the Fed prints money = Peak Oil denial.

“I am trying to get signatures for the Harp 3.0 petition.” —— Sean Omar

Good luck with that.

HARP, HAMP and the other alphabet save-the-homeowner type bills are NOT LAWS. They are GUIDELINES and participation by the bank is totally VOLUNTARY.

Which explains the truth of your statement —- “To date only a selected few have been helped”.

“First of all, the Fed does not print money.” ———— steve from virginia

Oh.

Then please explain the following statement made by Ben Bernanke.

“The U.S. government has a technology, called a printing press that allows it to produce as many U.S. dollars as it wishes at no cost.”

“Secondary Market Mortgages – those that the big GSEs (FNMA & FHLMC), FHA, VA & RD ‘guarantee’ do not have demand clauses.” ———– MortgageDiva

Oh.

Then what does this mean? (emphasis mine)

“17. Transfer of the Property or a Beneficial Interest in Borrower. IF ALL OR ANY PART OF THE PROPERTY OR ANY INTEREST IN IT IS SOLD OR TRANSFERRED (or if a beneficial interest in Borrower is sold or transferred and Borrower is not a natural person) without Lender’s prior written consent, Lender may, at its option, REQUIRE IMMEDIATE PAYMENT IN FULL OF ALL SUMS secured by this Security Instrument. However, this option shall not be exercised by Lender if exercise is prohibited by federal law as of the date of this Security Instrument. If Lender exercises this option, LENDER SHALL GIVE BORROWER NOTICE OF ACCELERATION. The notice shall provide a period of not less than 30 days from the date the notice is delivered or mailed within which Borrower must pay all sums secured by this Security Instrument. If Borrower fails to pay these sums prior to the expiration of this period, Lender may invoke any remedies permitted by this Security Instrument without further notice or demand on Borrower.”

—— from, ….. Paragraph 17 of the standard “Single Family FNMA/FHLMC UNIFORM INSTRUMENT Form 3005

There is a box on the TIL (Truth In Lending) that says; ““DEMAND FEATURE: This obligation has a demand feature”

I think the confusion arises from not understanding the TYPE of “demand” . If the demand box is checked, the type of demand will be stipulated later in the Mortgage Note, I think. There are three types of demand;

1) “Acceleration clause.” —- basically you violate a contractual obligation; missing payments (technically, even ONE), not insuring the property, or even keeping the property in disrepair …. Will give the lender the right to “call” (demand) immediate payment in full. A GSEs most DEFINITELY can have this clause.

2) “due on sale clause.” —- As the name implies payment in full is demanded when Title is transferred …. And there are SEVERAL ways this can occur, not just a “sale”. Pretty much every mortgage has this. It’s purpose is twofold; 1) to protect the lender against rising interest rates … so if interest rate have risen you can’t let the buyer “assume” your mortgage, and 2) protects the lender in the event the new owner not being able to afford the mortgage obligations.

3) A simple and straight “demand clause” —— basically the lender can demand repayment of the loan in full at any time for any reason. For example, if interest rate rise the lender may force the borrower to agree to a rate hike by threatening to call the loan. It is in this case that MortgageDiva is correct ….. a “simple demand” is NOT allowed by GSE backed mortgages.

Catherine Austin Fitts says it is mathematically impossible for the banks/mortgage lenders to have incurred the losses they did unless multiple mortgages were written on the same pieces of property.

If you know someone who’s facing foreclosure, tell them to find a lawyer who will insist on the original loan documents, as–theorectically–required by law.

Personally, I am hoping the stock market falls below 15,000 tomorrow. It took a couple years to inflate, how many weeks to bottom out. The lowest it got before the QE craze was in the 6,000 range. The financial elite have a long fall to embrace. Welcome to the bottom, bitches.

Thank goodness we paid the mortgage off in December. We had less than a year to go anyway, but when our credit union announced they were outsourcing mortgage management to a company /we had never heard of effective Jan. 1, we elected not to go thru the rigmarole

“We can ignore reality, but we cannot ignore the consequences of ignoring reality”

Ayn Rand

Newbie ‘steve from virginia’ says the Fed does not print money (technically true, but still bullshit.)

Newbie ‘MortgageDiva’ says GSEs don’t have demand clauses. False!

They got called out NICELY by me and asked for an explanation. They disappeared into the ether.

FUCKIT!! FROM NOW ON I’M ONLY ADDRESSING TBP REGULARS …. unless, of course, it’s to give a Newbie a world-class asskickin’ beatdown.

Stucky….would you send my HEMP petition….it’ll help folks smoke better reefer in the future . SSS already signed it .

@Stuck, due on sale clauses, you betcha.

What I was really talking about was a demand-for-any-reason clause which is what I believe the other poster was attempting to talk about.

I have not personally seen these in a mortgage and would have been really hesitant to sign such a document. In business loans and mortgages, it is more the rule though.

From what I have heard – but have absolutely no first hand knowledge as I haven’t read a new mortgage in 9 years – they have been inserted into the new (and refi) contracts.

As most Americans read below an eighth grade level, I have to believe that nobody would notice the difference. Well, nearly nobody.

These elitist freaks have us by the short-hairs. No way around it.

At least “the fed doesn’t print money” amused the hell out of me.

“What I was really talking about was a demand-for-any-reason” ——— TeresaE

Yes. I’ve never seen one either in any of the mortgages I’ve done.

I was talking about the “acceleration clause” which is pretty much on every mortgage. A lender would be nuts to not include it.

I’m glad we straightened that out.

“As most Americans read below an eighth grade level, I have to believe that nobody would notice the difference. ” ——— TeresaE

It’s worse than that. I have NEVER seen anyone actually read the mortgage documents. Ever. Of course there are a LOT of documents. I am feeling Benevolent and Kind today, so let me quickly and briefly let readers know the FOUR documents they MUST be fully aware of. Print this out.

Note: It is the closing agent’s obligation, by law, to go through these documents with you. But, on big “trick” these people do is to go through all the mundane bullshit first. They might spend an inordinate amount of time on the easy-to-explain documents. They save the really important stuff for the end. The reason is psychological. The first is that since they will be so ‘truthful and forthcoming’ with all the mundane shit, they know that you will come to believe they’ll be totally upfront later on. Secondly, more importantly, it’s to lower your Bullshit Detector, to wear you the fuck out, so that by the time you get to the really important stuff, you’re just signing shit like a robo-signer. Really.

The documents ………

TRUTH IN LENDING —- it has most the financial stuff; actual APR, total amount financed, total monthly payment, total of all payments. This is where dishonest brokers sweat their balls off; whatever bullshit they sold you? …. NOW is the time for you to check, double-check, and triple check/

FINAL Good Faith Estimate —- About a day or so before closing the broker will submit a FINAL GFE to the lender. (Sometimes it’s even just a few hours before closing.) Do NOT fall for their bullshit — “But I already gave you the GFE.”. Do what you can to get the FINAL GFE from your broker the DAY BEFORE your closing. The GFE has the loan origination fees, loan points, and all your other closing fees. Understand each and every one, and don’t be afraid to ask questions! This is your second opportunity to see the broker sweat his balls off (if they bullshitted you in the sales process.)

Mortgage Note (Primissory Note) — basically your IOU promising to repay the loan. However, it also includes the terms for repayment; interest rate, fixed or adjustable, late fees, loan amount, and term.

Mortgage (Deed of Trust) — basically provides information and security about the loan in the promissory note. The verbiage therein contains a lot of “granting” language … like a deed does … the primary purpose is to give the bank the right to take the property if you go into default. In other words, it is here where you will find the DEMAND details.

Oh … one last thing

I would strongly suggest that you tell the closing agent that you wish to review the above four documents FIRST.

Don’t believe any bullshit that they can’t do that … they’ll get to it soon enough … whatever.

Do you know who is really in control of the closing session? YOU!! Because you can walk the fuck away any time you want from the closing table. And they know it … and it often scares the shit out of them.

Printing it out Stucky, Thanks

Way back in 2004 I questioned all numbers from NAR/MBA.

I was a title schlep doing reo Sheriffs nod’s finding and flipping a real short sale artist wholesaler in the ghetto. Wall streeters today are just following my plan i started yrs ago. In fact one Portfoilio mgr asked me how is this going to end. Anyway, I put Yun under the table at a semi that year…told him im killing it in foreclosures and he said- “no thats coming to an end.”

Long story, but your reprinting what is REALITY!.

Then came Jim Cramer 2007 buybuy buy on BOA and Countrywide buyout…hell, at the same time I was shorting 30% of their local loan portfolio.. Jimmy says buy…repackaged crap my friends were selling at GS to Pension funds…frigging crooks on the Wall. About 40% of the Countrywide loans were in DEFAULT w NOD’s..BOA found that out a little too late.

Prices are up cuz I said in 2009 ” banks must limit supply of reo’s, let cities foreclose, get a bailout deal to recapitalize, lower mtg rates, offer modifications, delay pending NOD’s, limit and bid up rentables when available so prices have to go up.

Us Flippers and investors need to keep things moving. Today, were in bidding wars just like it was in 2006 and 2007.

I could go on and on and finish the book, but….either way it’s all going to burn(turn) down in the end but not yet! Not yet.

Heck, we ‘re all in denial.

@Stucky

Hey, thanks for the shout out.

I’ve been busy these days – doing volunteer work for a non-profit. We educate homeowners about the mortgage-backed security fraud and how it impacts their mortgages.

We hold about one workshop a month. Then, individual homeowners make an appointment to meet with me one on one, where I review the recorded documents (mortgage, Assignment of Mortgage, latest version of the Note.)

I dig into the details, flag the fraud and violations. Then, we hand the report back to the homeowner and refer them to a short list of attorneys.

We also use PR – in the form of a public shaming of the requisite “lender.”

So far, two of our homeowners have obtained substantial principal reductions, elimination of the arrears, 2% interest and shorter terms.

Really exciting.

And a number have gone live with their petitions – one homeowner obtained over 7,000 signatures. We marched into NYC, up Park Ave and delivered the petition to JPM Chase. Of course, we were tailed by the head of Metro Police. But he seemed like a rather pleasant guy – and agreed that the homeowner was getting the shaft and deserved relief.

I’m still coaching homeowners from TBP “Who’s Your Lender” but since the post went down, and the Snowden revealed the NSA spying, the number of emails has dropped considerably.

My laptop “updates” every night – sometimes turns on in the middle of the night – but I really don’t care.

Small price to pay for helping people who need it the most.

I feel very blessed to do this kind of work. The people I work with are really wonderful. And the homeowners are some of the nicest people I’ve ever known.

All in all, things are good. Thanks for asking!

Mary Malone

You’re welcome!!

“I’m still coaching homeowners from TBP “Who’s Your Lender” but since the post went down, and the Snowden revealed the NSA spying, the number of emails has dropped considerably.” —- MM

That was one of, if not THE, most helping-other-people posts ever. Maybe Admin can resurrect it, if you want?

You are a godsend to many people. That must be so rewarding. FWIW, I’m so proud of you!!

GREAT to hear from you, and that you are doing well!!

speaking of distorted…like ber’ rabbit pleaded, “please don’t throw me in the briar patch.”…and they did.http://www.zerohedge.com/contributed/2014-02-05/bitcoin-revolutionary-game-changer-or-trojan-horse

And Yves Smith argues that Bitcoin actually plays into the hands of the central bankers:

Many [Bitcoin enthusiasts] clearly relish the idea of launching a currency outside the control of central banks (plus this beats Cryptonomicon in geekery).

If you believe the hype, you’ve been had. As Izabella Kaminska of the Financial Times tells us, you all are really just doing free/underpaid R&D for central banks, since you are debugging and building legitimacy for one of their fond projects, making currencies digital and getting rid of cash altogether.

I had wondered about the complacency of Fed and SEC officials in Senate Banking Committee hearings on Bitcoin last year.

punch digital currency followed by the pound a RFID in my ass sign.

https://www.youtube.com/watch?v=eob532iEpqk

@Stucky

Thanks for the kind words.

I’d be glad to re-ignite the Who’s Your Lender post – but I think it has been disabled. We were up to over 2500 comments – so not sure how we can get it back up.

Admin has given us so much opportunity to get the word out. Really appreciative!

@Admin

Thanks so much for reposting ‘Who’s Your Lender’

You are a very nice man.

Mary

I don’t think it loads all the comments. It must time out because there are 2,800 comments.

Unfortunately, this article is fundamentally wrong. It is true that the Fed will “taper” for a while, but it will do so only long enough to temporarily implode some of the emerging market countries our government is a rival to (ie: Russia). Once the policy goal has been achieved (ie: bringing Ukraine into Europe), the tapering will cease and the printing to infinity will return with gusto. House prices will continue to be artificially supported, bond yields will continue to be ultra-low, bank deposits rates will return to zero (if they ever move off of zero) and stock prices, after having been temporarily compressed, will explode again.

If you think that the Fed is going to allow long term deflation, you are wrong. It is owned by the big banks, lock, stock and barrel. Yellen and all her predecessors have taken orders from them since 1914 and will continue to do so. The middle class will continue to be fleeced to the enrichment of the top 10%, and, as the law of diminishing returns kicks in, the percentage of the population that is benefitting from QE to infinity will continue to shrink, until finally, when the system implodes in a Zimbabwe-like event involving hyperinflation, the QE will be benefitting only the top .0001%.

The “taper caper” will continue until about September, assuming government foreign policy goals are met, and then, with the DJIA at around 11,000 or so, it is off to the QE to infinity game once more. Otherwise, the Dow will sink to 2-3,000, and too many TBTF banks will collapse. Too many banksters who are now quietly manipulating paper gold and accumulating physical gold, based on the hyperinflation scenario, would go bankrupt. You can be sure that the Mandarins of the Fed will not cross their masters.

Now I’ve read recently about getting a “land patent” that theoretically would shield you from having your house/land taken away if you don’t pay taxes or in case of eminent domain grab:

http://www.teamlaw.org/PatentHowTo.htm

Your thoughts?

I meant, if you don’t pay your property taxes.