In case you were being distracted by the Obamacare TV commercials (paid for with your tax dollars) running every 10 minutes, Obamacare is an epic failure of monstrous proportions. The two articles below reveal the epic-ness of the failure. First we know that 4.2 million suckers have enrolled. But, for some reason Obama and his minions won’t reveal how many have actually made a premium payment. I wonder why? Nine states and DC have reported what percentage have actually paid. It seems that out of 1.3 million enrollees, only 80% have paid. You can be sure the Federal numbers will be worse. At most, 3.3 million of the 4.2 million have paid.

Now let’s go back to yesteryear when the Obama declared he would cover the 30 million uninsured Americans. According to Kaiser Family Foundation there are 28.6 million Obamacare eligible people in the country. Their goal was to enroll 7 million people, or less than 25% of those eligible. With two weeks to go, they are going to end up with less than 4 million paying Obamacare enrollees. That means that 86% of those eligible will not be in the plan. Even worse, it seems 65% of those who have enrolled already had insurance.

HealthMarkets, a insurance holding company based in Texas, conducted its own survey based on the 7,500-or-so people that the company enrolled in exchange-based plans. Based on their survey only 35% of enrollees were previously uninsured. 10% previously had employer-sponsored coverage, but were dropping into the exchanges either because the exchanges offered a better (i.e., taxpayer-subsidized) deal, or because their employer had stopped offering coverage. 15% previously had individually-purchased coverage, but their old plans had been rendered illegal by Obamacare and were canceled. The remaining 40% were people previously covered under the old individual market, a market that was substantially less expensive than the Obamacare exchanges.

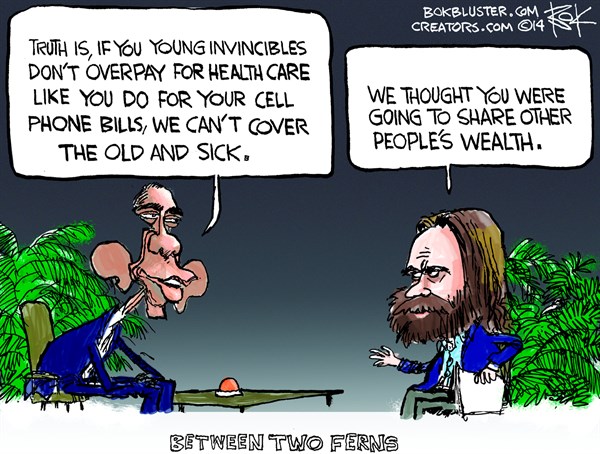

And the cherry on top is the fact that 2.8 million of the 7 million goal needed to be between 18 and 34 years old for the numbers to work for insurance companies. Only 1.1 million 18 to 34 year olds had enrolled as of March 1. This is an absolute disaster for Obama and explains the desperate commercials being aired non-stop targeting millennials. Without enough healthy young people in the plan, the costs will be far greater than the premiums collected. Therefore, insurance companies will make up for this profit shortfall by increasing premiums for the rest of us.

Thank Obama for your 10% to 20% premium increase next year. I’m still waiting on my $2,500 savings promised by Obama in 2009.

This is the fabulous result of government controlled, mandated, and run healthcare. And Obama has delayed all the bad shit until after the 2014 elections, so his Democrat minions (not one Republican voted for Obamacare) aren’t wiped out in a landslide. It’s funny how you don’t hear much about this from the captured MSM.

And I almost forgot about Obama’s promise that Obamacare wouldn’t add one dime to the deficit. He was right. The CBO says it will add $1 trillion to the national debt in the next 10 years. So it will add at least $3 trillion to the national debt. That Obama should have paid better attention in math class.

How many Obamacare enrollees have paid is revealed by some states

on March 14, 2014 at 5:52 PM

The Obama administration has released numbers on enrollment in the Affordable Care Act exchanges — but not how many of those people have actually paid.

That’s a key component, eyed especially hard by critics of the president’s health insurance reform.

CNBC is reporting today that nine states and the District of Columbia have reported those numbers, and they are “all over the map” — ranging from 92 percent of enrollees have paid in Connecticut to 54 percent in Maryland.

Here’s a list of the states, the number of those who have selected a plan and the percentage of those who have paid as reported by CNBC:

Connecticut, 57,465, 92%

Minnesota, 33,722, 90%

California, 923,832, 85%

Rhode Island, 19,690, 83%

DC, 6,516, 75%

Nevada, 30,015, 70%

Vermont, 24,326, 59%

Washington, 191,081, 57%

Maryland, 38,070, 54%

CNBC quotes Dan Mendelson, CEO of the consulting company Avalere Health, who says the Obama administration is in an awkward position, because the paid enrollment rate is a fluid number, and one that could hurt the administration politically and “helps the Republicans.”

“It doesn’t help them to put out that number. It’s going to be lower than enrollment no matter what,” said Mendelson. “It doesn’t help them in any way to move the goalposts and make the field longer.”

Mendelson said that once open enrollment ends March 31, he expects between 5 percent and 10 percent will be unpaid.

Young ObamaCare Enrollees To Fall 50% Below Target

By JED GRAHAM, INVESTOR’S BUSINESS DAILY

Posted 03/13/2014 08:02 AM ET

Young adult enrollment in the ObamaCare exchanges will likely be only half of the first-year target at best, a bad sign for the health reform’s long-term health.

While sign-ups may pick up in the next few weeks, don’t expect a huge last-minute surge to make up the difference. The exchange plans’ high deductibles and loose individual mandate enforcement work against hopes that young, healthy Americans will meet the March 31 deadline.

Data through five months of the open-enrollment period show that slightly fewer than 10% of eligible 18- to 34-year-olds have signed up for coverage. Among young men, roughly 1 in 12 has signed up.

The Kaiser Family Foundation puts the ObamaCare-eligible population at 28.6 million, with 40%, or about 11.4 million, in the 18-to-34 age group.

Compared to the size of the potential market, the first-year target of 7 million enrollees, including about 2.8 million young adults, was relatively modest.

Yet it’s now clear that the initial target is well out of reach. The Avalere Health consultancy projected that sign-ups — paid and unpaid — will end March at around 5.4 million.

Through February, not quite 1.1 million young adults had selected an exchange plan. Among this group, the male-female breakdown was about 45% vs. 55%. That matters because women at child-rearing age are more likely to run up big medical bills.

In February, 268,000 18- to 34-year-olds signed up, so a decent upsurge in March could lift the total close to 1.4 million. But that’s before winnowing out the people who don’t pay.

Anecdotal reports from a handful of states and large insurers now point to a paid rate of about 85%, possibly lower.

While that could improve before the March 31 deadline, there’s reason to suspect that the paid percentage might lag among young adults, since they are showing more reticence about signing up in the first place.

Once the unpaid group is subtracted, it appears likely that young-adult enrollees will fall at least 50% below the first-year target The White House had initially set that target at 2.7 million. Differing only slightly, Kaiser Family Foundation researchers have said that 40% of enrollees should be 18- to 34-year-olds to match their representation in the eligible population.

The age mix is important because the exchanges charge younger people higher premiums relative to pre-ObamaCare individual market insurance, so that older people can be charged less without negating insurer profits.

If young adults make up just 25% of the ObamaCare exchange population, it would wipe out much, but not all, of the 3% to 4% profit margin insurers typically allow for in setting premiums, Kaiser Family Foundation experts figure.

Yet that calculation assumes the health status of those who do sign up is about average. In general, an insured pool comprising a smaller share of the eligible group raises concern that the covered group will be costlier than average.

Without a huge upsurge in young-adult participation in March, policymakers will have to wrestle with the question of what went wrong.

Technology hiccups are sure to get some of the blame. Some may point to the last-minute exceptions the Obama administration carved out for those who were previously insured in the individual market but received cancellation notices.

Another partial explanation may turn out to be that young adults bought off-exchange policies.

Yet the dearth of young-adult enrollees is also raising basic questions about the structure of health subsidies and the mandated benefit package.

“I believe (the uninsured) are not buying it because the premium — even net of the subsidies — is too much for plans that have deductibles that are too high,” wrote health care consultant Robert Laszewski.

Avalere Health has put the average deductible at $2,567 for a silver plan and $4,545 for a bronze plan.

That is a whole lot different than RomneyCare, whose 2007 rollout in Massachusetts is cited as reason to expect a last-minute surge in demand.

Under RomneyCare, there initially were no deductibles for households earning up to 300% of the poverty level.

A political fight over temporarily suspending the individual-mandate tax penalty also might encourage some to remain uninsured, at least for now.

Health and Human Services Secretary Kathleen Sebelius told lawmakers Wednesday that the mandate penalty would not be delayed. But the Obama administration has quietly made it much easier to get an ObamaCare hardship exemption.

Your brain-teaser for the day: name one positive action from this administration over the last 5 years. I’m not talking about flowery words or bold promises. I mean real substantive policies that adhered to the Constitution and that resulted in meaningful improvements for the entire country.

Thanks for that excellent analysis admin. You forgot to mention almost 6 million people have had their insurance cancelled because of Obamacare, and another 6-8 million will get cancellation notices this year (many right before the elections).

Obamacare is a failure of biblical proportions. Fewer people, not more, will have health insurance. The sickest, fattest people that have destroyed their health are covered, and everyone else will be paying for their irresponsibility with double or tripling of their premiums, and quintupling of their deductibles, and that’s only the beginning.

What I’m seeing every single day in the office is people with brand new Medicaid coverage (free healthcare). Obama and his minions are padding their numbers by letting anyone that can fog a mirror into Medicaid. And people are dumping their private insurance they have to pay for and getting on Medicaid. Medicaid is billions of dollars behind here in the socialist state of Illinois, and I can only imagine how many hundreds of billions behind nationwide. This farce will continue for a few years until people realize how much having 15 million more people getting free healthcare is costing, then there will be outrage. By then, of course, Obama will be out of office, playing golf with his rich friends, and getting $300,000 per speech he gives to liberal progressives throughout the land (that is, of course, if he doesn’t become dictator and never leaves office). And, in the meantime, hospitals and doctors across the country will go bankrupt, close up shop, and leave town because Medicaid never paid them a dime.

[img]http://thepeoplescube.com/red/download/file.php?mode=view&id=29651&sid=846a93b0030ec00ab92672933023d5a3[/img]

Burn, baby, burn…

What is health insurance for? Given that emergency treatment is required without evidence of how the bill will be paid (under EMTALA), and given the existence of Medicaid (such as it is), health insurance is to protect a person’s net worth in the extremely unlikely event of a health calamity. As the libs would say, “without health insurance, everyone is just one health crisis away from financial ruin.” What financial ruin? Most people under age 35 have a negative net worth. Who cares if they have to file bankruptcy to wipe out their emergency room bill? Young people would have to be stupid to buy health insurance now. They may have been stupid enough to vote for Obama, but they’re not quite stupid enough to write a check for insurance they don’t need.

And you can keep your plan. I guarantee it!

Suckers.

As the previous idiot I chief said, Mission Accomplished.

Thanks Admin, just talking about all this last night with my liberal relatives, they don’t understand because they don’t want to understand.

So when the aca fails, what then? That’s what has me concerned, will the narcissistic sociopath president become so pissed he drops a bomb? Will he then lash out at personal retirement plans to pay for whatever is next?

Uncertain days ahead that’s for sure.

Rise Up,

I like that chick, here’s her argument on the Second Amendment.

WTF? Now I’m too afraid to try again………….

[img [/img]

[/img]

OUCH! Those dang unintended circumstances sure do hurt!!

Obamacare [/img]

[/img]

[img

[img [/img]

[/img]

Complexity and the impetus to shove thousands of small business guys over the edge.

The hits concerning this “law” just keep coming. More requirements for employers, more fines, more taxes, more paperwork, more, more, more.

THIS is why small biz is closing down and no longer employs 75% of the non-gubment employees.

Complexity, and its associated, mandated, corruption has killed this country.

O’care is yet the biggest nail in the coffin since the Patriot Act.

Bye-bye Republic, we sure didn’t manage to keep you long.