“I was not for this program, popularly known as QE3, to begin with. I doubted its efficacy and was convinced that the financial system already had sufficient liquidity to finance recovery without providing tinder for future inflation. But I lost that argument in the fall of 2012, and I am just happy that we will be rid of the program soon enough. “I am often asked why I do not support a more rapid deceleration of our purchases, given my agnosticism about their effectiveness and my concern that they might well be leading to froth in certain segments of the financial markets. The answer is an admission of reality: We juiced the trading and risk markets so extensively that they became somewhat addicted to our accommodation of their needs… you can’t go from Wild Turkey to cold turkey overnight.

So despite having argued against spiking the punchbowl to the degree we did, I have accepted that the prudent course of action and the best way to prevent the onset of market seizures and delirium tremens is to gradually reduce and eventually eliminate the flow of excess liquidity we have been supplying… one would be hard pressed to say that ending our asset purchases, which the depository institutions from which we buy them deposit back with us as excess reserves, would deny the economy needed liquidity. The focus of our discussions now is when and how to ‘normalize’ monetary policy.” – Fed Governor Richard Fisher

Talk about speaking the truth!!!

He admits that QE was designed to benefit Wall Street banks, hedge funds, HFT and the rest of the parasites on the ass of America. It was designed by the few for the few. It benefited Wall Street, not Main Street. The .01% saw their riches expand exponentially. The 1% benefited modestly as their 401k’s rebounded. The 99% got higher food and energy prices, along with declining real wages.

I know that John Hussman’s weekly letter is too deep in the weeds for many people, but I learn stuff every week that helps me understand the truth about our financial system and our manipulated, bubble markets. The Federal Reserve is primarily responsible for the two bubbles that have already burst since 2000. They are single-handedly responsible for the bubble that will burst in the near future. The Fed will have withdrawn the $85 billion per month punchbowl by October of this year. Hussman explains what happens next:

That sucking sound you hear is the Federal Reserve exiting from the most reckless policy experiment in its history. Unfortunately, that policy experiment has been the primary driver of speculation in recent years. One can’t rule out some stall in the tapering timeline, but even QEternity appears to have an expiration date. Despite present complacency, this transition is likely to be painful for the market, as one does not normalize valuations that are 100% above historical norms without pain – typically concentrated in a handful of steep but short-lived free-falls. That said, there was no evidence years ago that boosting the market to speculative highs would do much good for the economy (consumers spend from their view of “permanent income,” not from temporary fluctuations in volatile assets).

Make no mistake about it, valuations today are more extreme than they were in March 2000. Think about that for a few moments. Are you mentally and financially prepared for a third 50% plunge in the stock market in the last fourteen years? Well, are you punk?

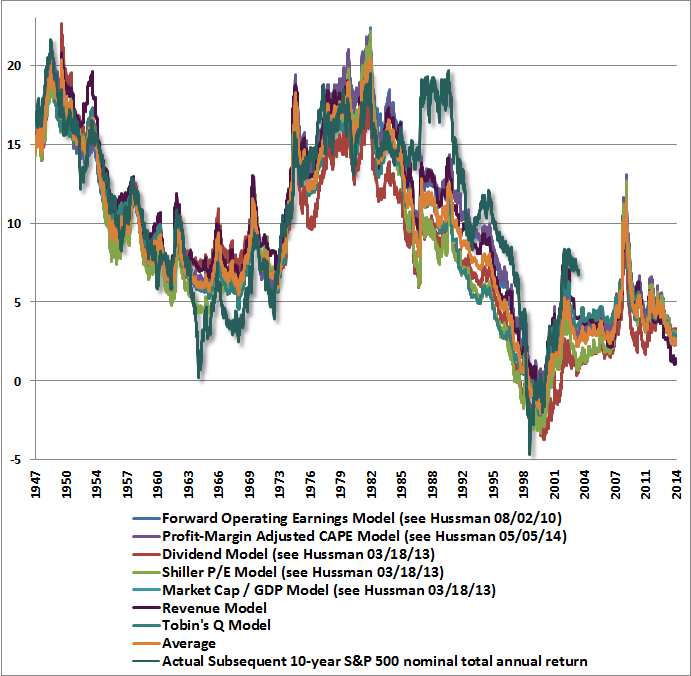

With advisory sentiment running at 56% bulls and fewer than 20% bears, with most historically reliable valuation metrics about twice their pre-bubble norms (and presently associated with negative expected S&P 500 nominal total returns on every horizon of 7 years and less), with capitalization-weighted indices near record highs but smaller stocks and speculative momentum stocks diverging badly, and with a Federal Reserve clearly intent on winding down the policy of quantitative easing that has brought these distortions about, we continue to view the present market environment as among the most dangerous instances in history.

Major market peaks, even those like 2000 and 2007 that were followed by 50% losses, have never felt dangerous at the time. That’s why they were associated with exuberant price extremes. Sure, investors had a sense that prices had advanced a great deal, but endless reasons could be found to justify the advance. Avoiding major losses required an intimate familiarity with market history, and enough discipline and patience to maintain what Galbraith called a “durable sense of doom” about observable conditions. The general rule is that you don’t observe the “catalyst” in advance, only the stack of dynamite.

Make no mistake, reliable valuation measures for the median stock are actually more extreme today than in 2000. On a capitalization-weighted basis, valuations are beyond every pre-bubble point in history except for a few months in 1929. In the bubble that ended in 2000, final valuations were higher owing to the extremes in large-capitalization technology stocks at that peak. Many observers seem to believe that valuations are of no concern unless they match that singular extreme. Good luck on that. The novelty, imagination, and extrapolation born of the late-1990’s internet and technology revolution is unlikely to be matched by an economy that can’t post growth beyond the threshold between expansion and recession despite the largest monetary intervention in history. The Fed is already retreating from that intervention, and for good reason, because while the Fed’s extraordinary actions are not actually linked to real economic outcomes, they encourage very risky speculative side-effects.

Meanwhile, an average, run-of-the-mill bear market would wipe out the entire advance in the S&P 500 Index since April 2010. Even on a total return basis, I doubt that any of the market’s gains from that point will actually be retained by investors by the completion of the present cycle. We currently estimate S&P 500 nominal total returns averaging about 2.4% annually over the coming decade.

Understand that nominal means before inflation. Therefore, you will be getting a big fat ZERO real return from the stock market over the next ten years. Considering the Fourth Turning has approximately fifteen years to go, this makes sense as we enter the war zone. I’m sure all seven of these valuation methods are wrong this time. Just ask a CNBC bimbo or Wall Street economist shyster.

Read John Hussman’s Weekly Letter

I’ve liked a lot of what Richard Fisher has had to say over the years. He’s the one who should head the Fed until it can be sent to the dust bin of history . I think that in the future he’ll be one of the few folks that will say ” I told you so ” . I can imagine what he says in the private meetings .

ZH has been running article after article showing the “smart money” is getting out of stocks, and retail investors aka “Muppets” have been piling into stocks lately. It doesn’t take a genius to figure out that the Fed is withdrawing the QE heroin, and the results aren’t going to be pretty. The only problem is, the Fed’s balance sheet is now over $4 trillion, so they won’t be much help when this bubble collapses like all the rest. Grandma Yellen is just as clueless as Bernanke after the 2007/2008 collapse, if not worse. All that matters in the banksters and billionairs make more billions. Their greed is never sated, and one can only hope they lose this wealth when the next bubble pops.

I don’t think the fourth turning has 15 more years to go. I think it started in the early 2000. While Howe’s theory would contradict 9/11 was any type of usher in of the fourth turning. I think it was due to the drastic change in mood of the country. Recently the article written by Monica Lewinsky was published. While I remember the impeachment and learn what the definition of “is” is, the mood of the country changed drastically from that “scandal”. One year the country was concerned about blow jobs in the oval office quickly followed by the 2000 election chaos, the dotcom bubble, and 9/11. I think we will see drastic changes before 2020.

QE = counterfeiting.

The Constitution says money should silver & gold coinage, things that cannot be created ad infinitum by a cabal of central bankers.

The US economy can’t make it to 2020. It’s already a walking zombie, now trying to kill off the remaining few non zombie countries like Russia & China.