The Happy Story of Boomers Retiring on Their Generational Wealth Is Wrong

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

This happy story is wrong on multiple counts.

The conventional view of the Baby Boomers’ retirement is a happy story: since we’re living longer and remaining productive longer, Boomers will not be as much of a burden on Gen-X and Gen-Y as doom-and-gloomers assume.

Not only are Boomers staying productive longer, they will draw upon their vast generational wealth as they age, limiting the financial burden on younger generations.

This happy story is nicely summarized in this lengthy piece The Fear Factor: Long-held predictions of economic chaos as baby boomers grow old are based on formulas that are just plain wrong.

In this view, the only thing needed to prop up Social Security for the rest of the 21st century is a higher tax on high-income earners, in effect moving the limit on earned income exposed to Social Security taxes from about $114,000 to $217,000.

This happy story is wrong on multiple counts. Let’s start with the most egregious errors:

1. It ignores the End of Work and the decline of full-time jobs

2. It ignores the Elephants in the Room, Medicare and Medicaid

3. It ignores the inconvenient reality that there is nobody to buy the Boomers’ overpriced stocks, bonds and homes when they start to unload them

Put another way: the happy story ignores the changing nature of work and jobs, the unsustainable cost trajectory of Sickcare (a.k.a. healthcare) and the inability of Gen-X and Gen-Y to buy Boomer assets at bubble valuations. Take these factors into minimal consideration and the claim that 76 million people (out of 316 million) can retire with no negative repercussions falls completely apart.

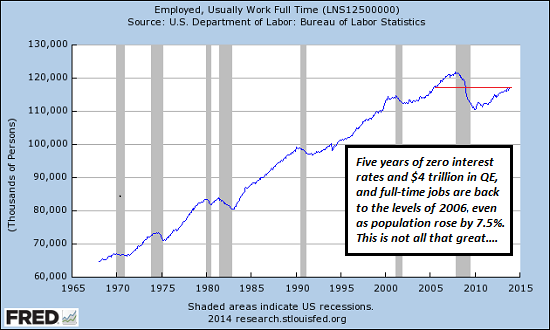

1. The end of work and changing nature of jobs: I have covered this for many years, most recently in a program with Gordon Long: The New Nature of Work: Jobs, Occupations & Careers (25 minutes, YouTube).

Insert end of work in the custom search box on this site and you’ll get 10 pages of articles published here on that topic. For example:

Global Reality: Surplus of Labor, Scarcity of Paid Work (May 7, 2012)

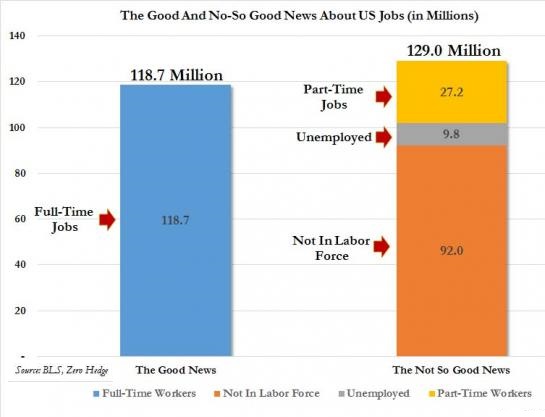

The reality is sobering: 57 million people draw Social Security benefits, tens of millions more draw Medicaid, Section 8 housing credits, etc., and full-time jobs number 118 million:

The Good And The Not- So-Good News About US Jobs In One Chart (Zero Hedge)

That’s a ratio of roughly two workers for every retiree and considerably less than that for workers to the total number of government dependents. As the Baby Boom retires en masse, if full-time jobs don’t rise as dramatically as the number of retirees, the system fails.

The happy story repeats the usual falsehood that Social Security has a Trust Fund it can draw down. This is a falsehood because the Trust Fund is fiction: when Social Security runs a deficit, the Treasury funds it by selling Treasury bonds, the same way it funds any other deficit spending. If the Treasury can’t sell bonds, the phantom nature of the Trust Fund will be revealed.

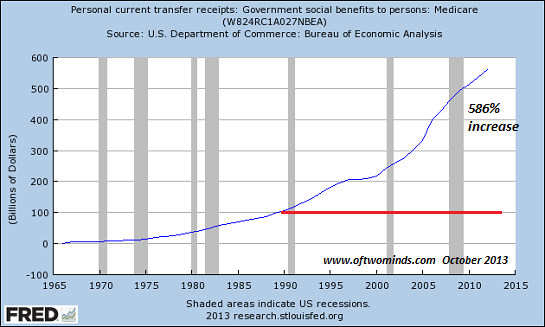

2. Everyone who looks at numbers rather than fictional claims knows the intractable problem is Medicare and Medicaid. In Sickcare, there are no real limits on cost, and so every attempt to impose cost discipline fails or triggers blowback.

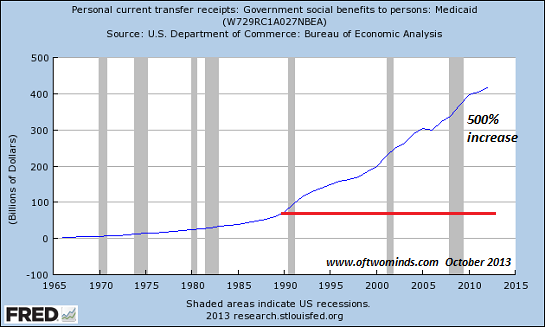

Here is Medicare’s twin for under-age-65 care for low-income households, Medicaid:

As I have observed for years, Obamacare and Medicare/Medicaid do not tackle the underlying problems of Sickcare costs in America. If you haven’t read these analyses, please have a look:

Why “Healthcare Reform” Is Not Reform, Part I (December 28, 2009)

Why “Healthcare Reform” Is Not Reform, Part II (December 29, 2009)

That Which is Unsustainable Will Go Away: Medicare (May 16, 2012)

Obamacare is a Catastrophe That Cannot Be Fixed (December 6, 2013)

3. As I explained in The Generational Short Part 2: Who Will Boomers Sell Their Stocks To?, the Boomers’ vast generational wealth will shrivel once they start selling assets en masse. The reality is neither Gen-X nor Gen-Y have the savings, income or desire to buy bubble-level assets from their elders.

This reality has been papered over for the past 5 years of super-low interest rates, which have enabled unqualified buyers to buy overpriced assets with modest income. Once the defaults start pouring in (and/or interest rates rise), the reality will become visible: you can’t cash in your wealth if there are no buyers.

There are numerous other fatal flaws with the happy story that 76 million Boomers can retire on full pensions and live off their home equity and stock portfolios. Here are a few of many:

4. Pension funds based on annual returns of 7.5% will be unable to fund the promised pensions when annual returns decline to negative 5%. As John Hussman has explained, every asset bubble in effect siphons off all the future return: when the bubble finally pops, average annual returns are subpar or negative for years.

5. The ultimate buyer of all Boomer assets is presumed to be the Federal Reserve.I explain why this isn’t going to happen in The Fed’s Hobson’s Choice: End QE and Zero-Interest Rates or Destabilize the Dollar and the Treasury Market (June 24, 2014).

6. It’s presumed the Federal government can borrow as many trillions of dollars as it needs to fund retirement and social benefits as far as the eye can see. Please see the article linked above to understand why limits on the Fed’s money printing and buying of governemnt bonds imposes limits on Federal borrowing.

To quote Jackson Browne: Don’t think it won’t happen just because it hasn’t happened yet.

7. Boomers are staying productive longer and keeping their jobs longer. The reasons for this are many, but one consequence is a dearth of opportunities for Gen-Y job seekers. As full-time employment stagnates or even declines, it’s a zero-sum game for the generations: every job a Boomer holds onto is one a Gen-Y applicant can’t get.

A 12-hour a week low-pay part-time job will not support a wage earner or fund a retiree.

8. A Boomer who bought his home for $50,000 decades ago can live very well on $75,000 a year; it’s a different story for Gen-Y. The Boomer has a low mortgage payment (presuming he didn’t extract all the equity in the go-go years) and low property taxes in states with Prop-13-type limits. The Boomer who hits 65 has relatively modest medical expenses as Medicare does all the heavy lifting.

Low housing and medical expenses leave Boomers with relatively ample discretionary income. The Gen-Y wage earner who takes the same $75,000 a year job is not so fortunate. The Gen-Y wage earner is offered the Boomer’s $50,000 home for $550,000, and crushing property taxes to go with the gargantuan mortgage.

The Gen-Y wage earner typically still has often-monumental student loan debt to pay off, and much higher healthcare expenses as companies offload rising Sickcare costs onto employees. Higher Social Security and Medicare taxes hit Gen-Y square in the financial solar plexus, while retiring Baby Boomers escape these taxes altogether unless they’re still working.

The point is an income that offers a Boomer a middle class lifestyle does not offer a corresponding discretionary income to Gen-Yers. The entire pyramid of well-funded retirement is based on a generational continuation of massive borrowing and discretionary spending.

If that doesn’t happen for structural reasons, the pyramid of well-funded retirement collapses under its own weight.

Fuck Boomers.

BES.

“BES”?

A. R. Wasem says:

“BES”?

Boomers Eat Shit.

My families got several well off boomers/prophets and a silent/artists or two that range from smug fucks to almost decent human beings. But not one of ’em thinks bad shit is in their futures. The ability to ignore reality has got to, given the assets they control, afford this train load of bullshit a certain amount of momentum. Their collectively ridiculous arrogance will only fuel the panic in T4T crisis – when the day comes that they can’t have it their way I’ll be laughing my fucking ass off like the guy on the plane who knew we didn’t have enough fuel when we took off.

“The fellow that can only see a week ahead is always the popular fellow, for he is looking with the crowd. But the one that can see years ahead, he has a telescope but he can’t make anybody believe that he has it.”

Will Rogers

Here’s what I see as far as the housing market:

I sell mostly bank-owned property. There are 3 types I deal with: Straight foreclosure, Deed in lieu of foreclosure, and reverse mortgage foreclosures. Guess which one is rising the fastest? Yep, reverse mortgage foreclosures! So, baby boomers suck all the equity out of their POS homes (and believe me, most of them are utter crap, nothing fixed, hovels) and this was in the last 4-5 years. So a home that is only worth 150K in today’s market has a reverse mortgage on it for 300K! The person dies or goes permanently into assisted living, triggering the mortgage to become payable immediately. FNMA reverse mortgages (largest sector) allow the heirs to “buy out” the mortgage and keep the house, or sell the house and pay off the note. I have yet to see one that is possible. They are either so damaged as to be unable to get financing or so far underwater you can’t buy them. So the bank takes them back in the foreclosure auction. Now, thanks to our wonderful Mr Frank and Mr Dodd, who wrote a nifty piece of legislation a few years back, FNMA is unable to take less than the appraised value. Ok, you ask, what’s wrong with that…well, appraisers come from a giant pool of appraisers and oftentimes are not from the area, and comp the house out too high or are unaware of hidden damage like failed septic or freeze damage. The appraisal price now becomes gospel and cannot be lowered for 180 DAYS. At which point it’s worth even less. Because these are FNMA properties we are on the hook for all the losses. I have no idea what these people are doing with the money they take out, but it’s certainly not maintaining the houses. I would assume some of them are using the money to go into long-term care, but speaking from personal experience one of these was used to build a daughter’s house right next door!

Also, I find that even if they don’t take out these mortgages, the condition of the homes are generally so dated, with old roofs, original windows and ancient heating systems that they are worth 20-50K less than the typical home in their respective neighborhoods.

Now, speaking from another perspective…buyers. Buyers are able to access pretty much the same info as any real estate agent. They may not know how to use it as effectively, but they can see that the housing “recovery” is pretty much a smoke and mirror show. LISTING prices are up, sure, but SALES are down, with an increase in market times. So…what does that mean? A few things…buyers are not really all the confident in their ability to hold onto their jobs. AND…the listing price increase is based on nothing real if the sales in the past 3-6 months don’t support it. AND if there are still short sales and foreclosures out there then these “gains” are not warranted.

I am seeing more and more appraisals fall apart because there simply are no sold properties to support the contract price on a home.

I also do a lot of “BPO” work for the banks. Broker Price Opinions. These entail driving by (or sometimes going inside) and taking a picture and filling out an opinion of value. While these are NOT appraisals, it does make me scratch my head, because I am seeing sold prices (3-6 months, considered recent in this market and pretty much everywhere else) that are SIGNIFICANTLY less than what is currently offered for sale. I mean 40K less. I don’t get it and I don’t see where it’s coming from. I constantly have to put in statements like “severe disconnect between pricing in current inventory and current sold properties”.

I am seeing homes that need a lot of work overpriced by about 20-30K and sitting, sitting, sitting.

Once the fall/winter months are here that little scenario is going to implode.

Where’s Steph been? I’d give her a thumbs up, even with typos.

realestatepup, great post – another layer of the onion, from my vantage point is this. People aren’t moving – either with van lines or rental trucks, in any way/shape/form compared to prior years. I talk to others around the country, same thing. ALL of the ‘majors’ have lost and are losing so many drivers and O/O they simply have no capacity whatsoever. And its not just the highly discounted shit, many of the discounts are plummeting in hopes that a little more minnow on the hook might do the trick – nothing…… they just can’t get driver assignments, ’cause they’re not there. The boomers ain’t going anywhere, gen Y is broke and unemployed and can relocate with a suitcase, and the X’ers are just scrambling to maintain. This country is locking up before our very eyes, but people walk around with this fake/phony optimism like trained lemmings actually believing ‘positivity’ works.

REP, so what? It just means the boomers made out on the reverse mortgage. Who thought that was going to be a good idea?

Yeah, it’s another layer of the onion, but it hits back at the status quo, banks and federally guaranteed loans.

@Iska Waran

You know, I saw “fucking boomers” and I knew my name had to be in the comment thread somewhere. I clicked over and I was not disappointed.

Ah, yes. Boomers…Anyone still in denial? I know many offline who are volunteer crash dummies. They think they are getting a sweet deal driving a shiny new piece of shit GM car until it crashes the wall and their springs come loose. When it comes to Boomers still working. This must be a fallacy. Most are getting out of the job market through early retirement. I can’t blame them.

Also, my salad tossing dissenters would be joyful to know old Darden fucked up their sale of Red Lobster when they failed to let shareholders vote. That is going to be messy. I kept my old name tag as a relic when they go bankrupt. Can’t wait.

@Nonanonymous:

Yes, the boomers made out like bandits but once again stuck everyone else down the line with the tab. That’s the whole point of this…of course until SOME FREAKING GENERATION wakes the hell up and says “No, we are not going to finance any more stuff for anybody” this will just continue ad nauseum.

Those charts, and Medicare spending are mind boggling. The boomers think the free shit is going to last forever. They’re the most obese generation in the history of the world, making morbid obesity socially acceptable for the masses, killing 340k people a year. But boomers don’t care, because somebody else is paying for their 12 meds, their heart caths, their scooters, the sleep apnea machines, their bypass grafts, their oxygen, Hepatitis C treatments, their joint replacements after the blimps destroyed their joints and every other aspect of their health. They can’t suck that sweet Medicare cash fast enough.

Turns out, Obamacare is gutting Medicare. In a few years, it will be unrecognizable. Obama has thrown boomers under the bus, and they haven’t even figured it out yet. All the douchebag ex-hippie liberal fuck boomers that voted Obama into office twice are going to get what’s coming to them. Boomers discovered debt, and now we’re $59 trillion in public/private debt, on a collision course with collapse. They don’t care, they just get fatter and fatter, and will end up in an early grave, but it’ll be too late, they bankrupted this country already. Game over.

“Rates for Baby Boomers (45- to 64-year-olds) have reached 40 percent in two states (Alabama and Louisiana) and are 30 percent or higher in 41 states. By comparison, obesity rates for seniors (65+-year-olds) exceed 30 percent in only one state (Louisiana). Obesity rates for young adults (18- to 25-year-olds) are below 28 percent in every state.”

http://fasinfat.org/obesity-by-age/

Adult Obesity Rate by Age Group (2012)

State 18-25 26-44 45-64 65+

B Alabama 24.4% 33.0% 40.0% 26.9%

A Alaska 10.2% 25.4% 32.4% 26.8%

D Arizona 18.4% 29.4% 28.9% 22.6%

C Arkansas 27.5% 38.8% 38.9% 25.9%

E California 13.7% 26.0% 31.0% 21.1%

F Colorado 11.1% 20.8% 24.6% 19.6%

G Connecticut 10.8% 28.5% 28.4% 26.5%

H Delaware 11.2% 27.7% 33.5% 26.0%

y District of Columbia 15.7% 19.1% 31.9% 19.1%

I Florida 14.6% 26.2% 30.7% 22.9%

J Georgia 16.1% 31.2% 34.6% 25.4%

K Hawaii 17.1% 29.1% 26.8% 14.1%

M Idaho 13.3% 26.7% 32.1% 26.9%

N Illinois 14.3% 28.6% 33.6% 27.7%

O Indiana 20.5% 32.0% 37.0% 29.3%

L Iowa 17.7% 31.4% 35.9% 29.6%

P Kansas 20.0% 32.1% 34.3% 26.2%

Q Kentucky 17.6% 33.5% 36.0% 29.2%

R Louisiana 19.0% 38.8% 40.0% 30.4%

U Maine 14.9% 30.7% 32.5% 25.9%

T Maryland 11.8% 27.9% 34.4% 26.2%

S Massachusetts 14.3% 22.2% 27.5% 22.6%

V Michigan 19.4% 34.2% 34.4% 29.6%

W Minnesota 15.0% 25.5% 30.0% 26.3%

Y Mississippi 23.6% 38.9% 38.5% 29.0%

X Missouri 15.5% 29.0% 36.9% 28.1%

Z Montana 15.4% 24.1% 29.1% 22.3%

c Nebraska 17.1% 28.8% 34.5% 26.8%

g Nevada 13.9% 27.2% 31.1% 25.1%

d New Hampshire 16.3% 27.9% 31.3% 26.5%

e New Jersey 13.3% 25.0% 27.3% 27.2%

f New Mexico 20.1% 31.3% 30.2% 20.4%

h New York 13.2% 23.0% 27.6% 25.7%

a North Carolina 20.5% 30.2% 34.7% 26.2%

b North Dakota 18.9% 31.1% 35.0% 27.3%

i Ohio 15.3% 32.2% 34.8% 28.8%

j Oklahoma 25.4% 34.0% 36.7% 26.8%

k Oregon 13.9% 29.7% 32.0% 25.4%

l Pennsylvania 19.1% 28.7% 33.2% 29.3%

m Rhode Island 14.2% 27.5% 30.2% 24.5%

n South Carolina 19.2% 34.7% 36.8% 27.2%

o South Dakota 16.2% 28.4% 32.9% 28.4%

p Tennessee 16.8% 33.0% 38.2% 26.3%

q Texas 14.4% 31.5% 34.9% 26.9%

r Utah 12.7% 23.5% 32.3% 25.6%

t Vermont 15.7% 22.9% 26.4% 25.5%

s Virginia 14.1% 26.5% 34.2% 26.8%

u Washington 15.4% 27.9% 31.3% 25.6%

w West Virginia 27.9% 35.5% 37.8% 28.7%

v Wisconsin 17.6% 28.9% 35.4% 29.5%

x Wyoming 15.4% 26.2% 29.4% 20.5%

I will sell you my house for one meeeeellllion dollars. Chelsea Clinton are you reading this? Easy helicopter distance to the Formula One track.

The garden does not convey.

What is mind boggling is Planck scale and these folks aren’t even close, but I’m sure they will alleviate that problem.

More whiny bullshit from the usual suspects. How many of you weak dicks are debt free? I am! How many of you own your homes? I do, two of em. How many of you cheap fuckers put your kids through college without one cent of debt? I did, two of em! I still work a full time job in a very technical and challenging field. Don’t talk to me about lazy dependent boomers. Laziness is a young person that still lives with mom and dad, fucks around on the computer all day and has never turned a productive wheel in his/her miserable life. Y’all can kiss my fat boomer ass!

ragman

You really should read Luke 12:20 …. even if you’re not the religious type. [/img]

[/img]

[img

The Boomers were really the first generation eating processed food almost exclusively. The body is an amazing thing and you can eat convenience for a long time, but it does catch up with you.

I believe a lot of the Boomers’ health problems could be turned around in 1-2 years with nutrient dense foods (fresh picked produce, pastured animal items cooked from scratch) but like the public in general, it’s easier to buy some pills from the billionaires to mask the symptoms because cooking from scratch and shopping for real food is just too time consuming. If you’re interested, check out westonaprice.org or ppnf.org (I think both offer the best nutritional advice since it’s based on looking at long term healthy native peoples.) Sure seems to work well for people at the food club.

TBP has contributed towards my wife’s ever expanding vocabulary.

Lately its been “fat fucking boomers.”

I’m so proud of her!

Wise words Stucky, wise words, John