The expansion of the BOJ asset purchase program was timed to start with the end of the Fed’s asset purchase program. I mean, come on. Could it have been any more obvious?

There is no big question that the Bank of Japan has been acting in concert with the Fed for the better part of this century at least. And politically, Japan is a client state of the US.

And readers know that I have a long standing observation that one of the great difficulties in recovering from the long period of Japanese economic stagnation since the collapse of their great real estate and stock market bubble has been the inability to clean up their interlocking financial system dominated by industrial combines called keiretsus and a closely associated political system run by a surprisingly well connected minority of insiders.

Beyond that I wondered why was Japan pursuing the purchase not only of domestic equities and non-sovereign paper, but foreign equities as well with their very large pension fund? Are these intended as ‘investments?’ Or are they a form of cross subsidies in support of a more global agenda?

It makes me wonder if the policy being pursued by the BOJ is not designed to help the people of Japan now, so much as to support the requests of the international banking concerns, more specifically the US Federal Reserve.

This made me wonder if Kuroda is pursuing the same type of trickle down stimulus in buying large amounts of financial paper by printing money, rather than engaging in policy actions to stimulate aggregate demand.

And there is that nasty consumption tax hike in April which tends to have a regressive effect on lower income households. A weak yen is good for the exporters and multinationals, but is hard on small businesses and consumers.

Although the Japanese GINI coefficient for economic equality is lower than that of the US, in terms of power Japan is a very top heavy, insider dominated society. Their incorporation of University pedigrees into the success ladder would make the Ivy League envious.

Here is a thoughtful discussion of Japanese quantitative easing from just a few weeks ago from Sober Look. As you can see, the consensus was running heavily against an expansion, making the surprise from BOJ the day after the Fed taper even more of a surprise.

“With wage growth remaining sluggish (particularly for non-union workers), rising import costs could undermine consumer demand – particularly in the face of higher consumption taxes. Given these headwinds, there may be sufficient political pressure to put the BoJ into a holding pattern.”

I am not sure of all the specifics of what is happening in Japan, but I am becoming increasingly persuaded that the Anglo-American financial cartel and some of its client states are engaging in an intensifying currency war with regard to the international dominance of the dollar.

This extends not only to the dollar as the primary benchmark for international valuations, but also to the more compelling power that such an instrument, in the hands of a single governmentally affiliated entity, provides to those who wield it to set international and domestic policies that go far beyond mere terms of trade.

So I think it is fair to ask for whom the Bank of Japan and their political leadership are making some of their policy decisions. And further, it is incredibly naïve not to ask the same questions about the Federal Reserve and the political leadership of the US.

Money power is political power, in every sense of the word.

Employment In Japan

It has been quite some time since I have been doing business in Japan, and I was curious to know if the culture of the ‘salary man’ had changed. What is the employment picture in Japan really like for the average person? What are things like behind the statistics put forward in the international press?

While unemployment in Japan is very low at 3.6% or so and the Labor Participation Rate is still fairly high, it looks like ‘underemployment’ might be something worth looking at given the slack in wage growth. Certainly Japan is experiencing deflation, but is that a ’cause’ or an effect as part of some other economic feedback loop?

What happened to the NAIRU non-accelerating inflation rate of unemployment theory? It is the theory put forward by Friedman and the monetarists that refers to a level of unemployment below which inflation must rise due to wage pressures. Personally I think the growth of monopolies, the globalization of markets, and the relative political weakness of labor has knocked another dodgy economic theory into a cocked hat.

Places like the old South might have had nearly full employment, but I don’t think slavery was adding seriously to wage pressures. Maybe not wages, but on the costs of transport, whips and chains. But this is just my opinion and I could be wrong.

Sometimes it is not always easy to find things because people tend to be very positive about their country, especially when speaking with others. And I dislike looking at OECD statistics and other compendiums because they tend to lose quite a bit with time lag and a lack of insight past government statistics which, and I know this is hard to believe, tend to paint a pretty picture.

But I did get this in from a long time friend in Japan.

“It is difficult for many young people who are part-time or temporary, particularly the men. It is hard for them to “attract” a mate. Many couples are both employed but when they have children there is pressure to find a nursery and often times the wife cannot return to her former job. This obviously complicates the demographic conundrum. Although I do not have figures, this sort of conversation comes up even on the TV.

This is from JIJI dot com. Sorry but Japanese.

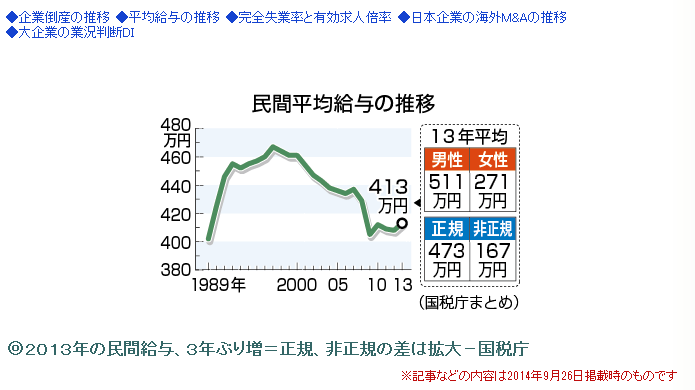

The chart shows average monthly salary after subtracting inflation for 2013 having dropped 0.5%.

According to the latest government statistics there are 33.1 million “full time employed” (seiki shain) and 20.4 million “part-time” (hi-seiki shain).

This means that the hi-seiki 非正規 or part-time/temporary account for 38% of the work force.

You can see the numbers I quote “3311” and “2042” in the second line of the page linked below.

Japanese Internal Affairs and Communication Ministry

Note: Hi-seiki refers to any type of employment other than full-benefit employee of a company. I have also seen figures that suggest 40% of those employed earn an average of less than 3 million yen (about $26,710 per year at current exchange rates).

Jesse’s Note:

There is an English tab on the site, but unfortunately the tab goes to a different site and does not ‘match up’ with the Japanese page.

Here is a google translation of the relevant line on the page.

Heisei “regular staff and employees” of the October time year 24 33,110,000 people, “non-regular staff and employees” is 20,420,007 thousand (Excel: 2985KB)

The timing of the move is very suspect.

As is the smash in gold and silver, and blowup in stock prices world wide.

One of the world’s largest five economies goes on a historic obscene money printing binge and everything rises while Gold and Silver crash?

Something appears amiss and clandestine about this outcome.

Taking orders from the BIS.

Yeap, and guess what they are buying with all this fiat money? They are buying U.S. Equities for their pension system, wink, wink. Kyle Bass thinks Japan will be the first big country to implode, we will see.

The BOJ Resorts To “Monetary Shamanism”……Financial Calamity Now Guaranteed

by Wolf Richter • November 2, 2014

With impeccable timing – on Halloween, which is increasingly popular in Japan among adults who are trying to escape their reality – Bank of Japan Governor Haruhiko Kuroda formally announced that he’d cure Japan’s economic and fiscal ills by resorting entirely, and not just partially, to “monetary shamanism.”

That’s what Izuru Kato, an economist and president of Totan Research, calls Kuroda’s dubious strategy. Japan practiced QE before it ever become a term in English. With predictable results: it did nothing for the economy but triggered unbridled government profligacy that generated ever larger budget deficits and an insurmountable mountain of debt.

But the QE that the BOJ has unleashed since April 2013 isn’t just QE anymore. It’s QQE: quantitative and qualitative easing. No-holds-barred QE. So in the true spirit of Halloween, Kuroda promised that the BOJ would:

•Increase the monetary base by ¥80 trillion annually (over 16% of GDP!), up from the previous commitment of ¥60-70 trillion. In a few years, its balance sheet will exceed Japan’s GDP.

•Increase its JGB holdings by ¥80 trillion annually, up 60% from the prior insanity.

•Lengthen the average remaining maturity of its JGB holdings to 7-10 years, up from the current goal of 6-8 years. Before Kuroda arrived at the BOJ, the average maturity was under 3 years.

•Triple the annual purchases of ETFs and J-REITs.

•And keep doing all of this until hell freezes over.

The goal is to demolish the yen, savings, real wages, people’s wealth, and that onerousness mountain of debt, much of which will end up on the BOJ’s balance sheet in a few years. And it seems to be working.

As planned under the economic religion of Abenomics, inflation has roared higher. In September, prices were up 3.2% compared to a year ago, with goods prices up 4.6% and service prices up 1.9% (service providers are so pressured by struggling consumers and businesses that they’re eating the 3-percentage-point consumption tax increase rather than passing it on). Here is what that inflation looks like:

Japan-CPI-2010-2014_September

Unperturbed, the BOJ uses its own and more convenient measure of inflation, taking out just about everything that adds to it, such as food, energy, and the impact of the consumption tax increase, to come up with a new and much tamer price index – the yellow dotted line in the chart above – which is still too low and has to be jacked up further.

But wages aren’t rising, so households – which do have to pay for food, energy, and the consumption tax hike – are having a hard time making ends meet. And the increasingly numerous retirees are losing purchasing power and wealth as their savings are being devalued. They’re all coming to grips with the scourge of Abenomics: “inflation without compensation.” It boils down to this, as the Statistics Bureau reported today with equally impeccable timing: In September, inflation-adjusted household incomes plunged 6.0% from a year ago.

And demand? Average monthly inflation-adjusted consumption expenditures by two-or-more-person households plunged 5.6% from a year ago. It’s the sixth month in a row that expenditures and incomes have plunged in this manner.

The Bank of Japandemonium at work in all its glory!

Its announcement was also impeccably coordinated with another hocus-pocus announcement, this one by Japan’s Government Pension Investment Fund (GPIF). It confirmed that the mega-fund would slash its holdings of Japanese Government Bonds (JGB) down to 35% of its ¥127 trillion in assets (from 53% at the end of September). The fund will dump its JGBs at a pace that is slightly below the additional purchases by the BOJ. This way, everything remains under control. The market only gets involved for the sake of appearances. Beyond the charade, the GPIF will hand its JGBs to the BOJ.

But then the GPIF will plow the newly liberated funds into the stock market to buy up domestic and foreign stocks and foreign bonds – by June! This announcement has been made in various forms for months. Each time such verbiage hit the news, stocks jumped on cue, which was the sole purpose of those announcements.

With the total commitment to monetary shamanism artfully pronounced on Halloween during Japan’s trading hours, pandemonium followed. The Nikkei stock index instantly jumped 5%. The yen collapsed by over 3.5%. In one fell swoop, it cut a big chunk out of the still considerable yen-denominated wealth of the Japanese. And JGB yields dropped further.

It is now perfectly clear that the Bank of Japandemonium has imposed a yield peg, which it continues to tighten. There will never again be a market-based yield for JGBs. Whoever bought them originally will get their money back eventually, but that money will be worth a lot less than what it was worth yesterday. In the interim, they will not earn any measurable yield. And shorting them is useless because the BOJ will simply buy every one that isn’t nailed down.

There is no exit. In a few years, the BOJ’s balance sheet will reach the size of Japan’s GDP, but it won’t be able to stop there. It can never allow the market to set the yields. It would instantly bankrupt the country. Politicians and the Japanese economy have already become totally addicted to government deficit spending and can’t shake the habit. But they know they don’t have to; the BOJ will just print the money.

And the BOJ socked it to foreigners who thought they could make a lot of money in Japanese stocks and then convert their gains into dollars. The destruction of the yen will see to it that those gains will be minimal. Worldwide, markets rallied after the announcement, in anticipation of what? True financial pandemonium? Because that’s what this sort of monetary shamanism will lead to.

By comparison, and only by comparison, the Fed has been practically tame. But the impact of its policies since the financial crisis are now clear: for individual Americans, economic “growth” has meant the opposite. Read… That Shrinking Slice of a Barely Growing Pie: Why the Glorious Economy of Ours Feels so Crummy

By Robert Fitzwilson of The Portola Group

November 3 (King World News) – Financial Destruction & Why This Fairy Tale Will End In Disaster

For most of us in our later years, the stories of Snow White, Hansel and Gretel, Rapunzel, and Rumpelstiltskin ring in our memories mostly with fond connotations. These stories were derived from ancient German fairy tales collected and popularized in the 1800s by two brothers, Jacob and Wilhelm Grimm.

The brothers developed a keen interest in their ethnic folklore and began collecting and publishing the tales. The collections came to be known as Grimm’s Fairy Tales.

In our time Snow White and the Seven Dwarfs as well as Sleeping Beauty were immortalized by the Disney Studios….

In contrast to the happy and memorable aspects of interpretations used for those two films, the tales were frequently not without dark and socially unacceptable aspects that had to be modified during different cultural eras. Those same dark threads would be celebrated by none other than the Third Reich. As they say, “Different strokes for different folks.”

The financial markets were moved last week by economic fairy tales, and for those invested in the precious metals and miners, the action was grim. The fairy tales came in the form of announcements that happened to coincide with the official ending of QE3 and the November elections in the United States. The number for GDP was greater than expected. No matter that the primary driver was government spending, particularly on the military. The mainstream pundits took the number and ran with it. After all, the pundits have been raised on the notion that government spending is ideal, so they probably did see it as a wonderful number.

Among the other fairy tales was that consumer sentiment was surging. We also have been told that unemployment is back in the “mission accomplished” zone for the Fed. Another tale is that inflation continues to be stagnant and that the central banks are focused on fighting deflation. To the Fed, low inflation, low gasoline prices, low interest rates, low unemployment, and a resurgent stock market are all signs of a job well done.

As the Brothers Grimm discovered, many of the best fairly tales have those dark components. Our modern economic fairy tales are no different. Under all these wonderful pronouncements lie many dark truths. Inflation is tame only for those who don’t eat, require a roof over their head, use transportation, or need education. The unemployment rate is wildly underreported in the U.S. The rate is catastrophically high for the youth of Europe. The price of gasoline is down but not from a lack of demand. As we have seen with gold and silver, it was the withdrawal of demand for “financial oil” in the derivatives markets that caused the price of a barrel to fall.

In one sense QE caused a financial recovery: The banks were saved and enlarged. The stock market, at least for the popular indexes, moved to new highs. Bonds have hit historic highs due to the zero-interest-rate policy but also due to the flood of money that has sought a home as a byproduct of QE. Credit quality considerations have been swept aside as this avalanche of QE-related money was placed. We would have normally said “invested” but at the current rates, the best-case scenario is not losing money. Financial recovery — yes. Economic recovery — tepid at best.

The biggest fairy tale was that quantitative easing would create a sustained economic recovery. Both Japan and Europe are now cascading down that path, despite even former Federal Reserve Chairman Alan Greenspan’s recent admonition that quantitative easing was a failure. In the case of Japan, the numbers involved are staggering. Our suspicion is that the real goal here is to encase government bonds in the bowels of their central bank, never to see the light of day again. In that fashion, the money can be used to purchase another huge portion of the stock market and to recapitalize the Japanese retirement pools facing huge losses on those inevitably toxic government bonds.

Where we go from here is hard to say. From a supply/demand standpoint, none of what happened in the metals and energy markets makes any sense. You should not have plunging prices when demand is surging and supply is tenuous or evaporating. It is probably a combination of official policy as well as the momentum-driven investment world in which we find ourselves. Central banks can trigger these smashes and backstop their proxies against loss. But a potent part of the cascading declines in these markets has to do with the impact of the algorithms, the machines and the mechanics of stop-loss orders.

Unless there is an agenda to destroy the metals and mining markets and companies, we should be approaching a tremendous buying opportunity. This is also particularly true for oil. It was a positive sign that the price of oil was down on Friday but many of the key energy-related entities were rising. We will look for a similar pattern early this week to see if we have reached bottoms in the metals and mining sectors. At a minimum, the U.S. elections will make for a tumultuous trading week. One way or another, this Western central planner concocted fairy tale will end in disaster and hard assets such as gold, silver, and oil will skyrocket.

kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/3_Financial_Destruction_%26_Why_This_Fairy_Tale_Will_End_In_Disaster.html