Did you ever notice that government reported numbers are revised downward in future months about 90% of the time? If they weren’t purposely reporting optimistic estimates, then revisions would be 50% up and 50% down. Not only is today’s “tremendous” new home sales a crock, but annual sales were flat with last year, and still linger 57% below the long-term average of 1 million home sales per year.

And now for the best part. There were only 34,000 new homes sold in the entire country versus the POLAR VORTEX devastated 31,000 last December. And only 13,000 of these new homes are actually built. The contracts can be cancelled before the sale goes through. Cancellation rates were close to 30% during the last downturn. The government actually reports this drivel with a straight face, despite admitting they are 90% confident the number they are reporting is within plus or minus 17% of the number they report. Basically they are taking a wild ass guess based upon some bullshit model. And it WILL be revised lower next month in the small print of the press release.

With Case Shiller reporting a decline in national home prices, I have a feeling there won’t be closings on all of those 34,000 new home sales. The lies, bullshit and propaganda is so deep you need hip boots.

Seven Consecutive Downward Revisions To New Home Sales Data Place Serious Doubts On Report Accuracy

Submitted by Tyler Durden on 01/27/2015 10:17 -0500

You will pardon us if we don’t “buy” the latest attempt by the Census Department to telegraph housing euphoria with the just reported number of 481K new December home sales, a surge of 11.6% compared to November, an increase which was expected by the consensus to be only 2.7%. In fact, the 481K print is now the “highest” since June of 2008.

The reason for our disbelief? Because as we have been tracking for the past 6, and now 7 months, every single such euphoric print since May of 2014 has been revised substantially lower after the fact (and after the headline-scanning algos promptly gobbled up stocks on the initial “beat”), and sure enough, the November print of 438K, was also just “revised” downward to 431K.

Putting today’s “highest in 7 years” new home sales print in context: consider that in May 2014 the same data series was originally reported at 504K… only to be revised to 458K!

In other words, there has now been 7 consecutive downward revision to the New Home Sales data!

As we said: forgive us, but we will once again refrain from drinking the Department of Truth’s cool aid.

We might as well have Glozell Green giving us economic numbers.

After all her youtube series gets about 2 million hits and Preezy Obongo thought she was important enough to “interview” while the world is on fire.

[img [/img]

[/img]

More of her “handiwork” here:

[img [/img]

[/img]

And here she is when told that the economic numbers totally suck:

[img]https://tse3.mm.bing.net/th?id=HN.608025910521498792&pid=1.7[/img]

I hate their black president. One low life POS.

Last year we put the house on the market … and then withdrew after we actually had an offer …. because we didn’t have a place to go. We ain’t that smart sometimes.

Anyway … our name is “out there” on the MLS as someone who recently tried to sell.

Sooooo … we get about 5-8 calls PER WEEK from various realtors; 1) telling us the market is re-a-a-ally great right now, and 2) can they list the property — which they can sell in 30-45 days, they say.

All those cold call from desperate Realtors? That tells me something.

Yes, and as I’ve pointed out here before. The government always publishes good news with the bad news.

Consumer confidence is up today! Woo Whooooo!

Sold my house in one day. Apparently, used houses sell fine.

Wyoming Mike

If you sold it in one day, you were asking too little. Don’t worry. You’ll pay a lot more back in good old Pennsyltucky.

You may want to make this it’s own post… of course, no coverage from the US media.

CBO Report: Obamacare program costs $50,000 in taxpayer money for every American who gets health insurance

It will cost the federal government – taxpayers, that is – $50,000 for every person who gets health insurance under the Obamacare law, the Congressional Budget Office revealed on Monday.

The number comes from figures buried in a 15-page section of the nonpartisan organization’s new ten-year budget outlook.

The best-case scenario described by the CBO would result in ‘between 24 million and 27 million’ fewer Americans being uninsured in 2025, compared to the year before the Affordable Care Act took effect.

Pulling that off will cost Uncle Sam about $1.35 trillion – or $50,000 per head.

The Fed’s Massive QE Failed To Revive Housing “Demand”: Home Prices Now Heading Down, Again

by Mark Hanson • January 26, 2015

This “housing recovery” has not been about demand, rather house-price super-inflation, which is suspect as price is a “lagging” indicator to demand.

•Existing Home demand has been extremely weak since mid-2013, when rates popped and the unorthodox demand began to dry up. “End-user” Existing home demand has been weak since 2007.

•Builder demand, more directly related to “end-user shelter” than Existing Sales, has also been weak since 2007.

•Prices have been parabolic in both segments, in spite of the underlying demand weakness and in the absense of meangul credit easing or wage gains (symptoms of rampant speculation).

•Demand / price dislocations can last longer than anybody expects, but eventually will righten, and demand will win out. The last time demand and prices were so diverged was 2007.

•The housing market will seek out demand, it’s what it does. And after so many years of such extreme stimulus that is now running off, the path of least resistance is through lower prices in 2015.

Historical housing economics suggest that “substantial house-price appreciation” – or “durable demand recovery with escape velocity” — is unlikley in the absense of meaningful “end-user” demand, credit easing, or wage gains.

But, from late 2011 to early 2014 (not coincidentally the Fed Twist thru QE era) that’s exactly what we got. Thinking back to 2006-2007, the conditions were very similar (massive demand / price divergence) following the surge in demand brought on by exotic credit from 2002 to 2005.

Bottom line: Housing demand and price dislocations can occur and last for longer than anybody expects. But, in the end demand will win out in what’s better known as “letting the air out”.

Weak demand coupled with cost to own a house 20% more than in 2006; “In-spite of” historically low rates

To be sure, “end-user” housing demand is absolutely, relatively, and historically weak with 2014 house sales lower than 2013. In fact, demand in 2014 was between 15% and 30% weaker than year and two ago sell-side forecasts. No analysts were predicting that (expect me!).

I think by now we can all agree there is been no “durable recovery with escape velocity” in “end-user” demand “in spite of” how low rates were pushed.

People still blame “tight mortgage credit”, as the number one demand inhibitor. But, how can that be with FHA loans that allow 3% down, $625k loan amounts, and 580 credit scores. In addition, medical delinquencies were removed from traditional credit ratings last year raising averages scores.

The housing “conundrum” I have been waiving my arms over for two years should finally be obvious to everybody else; critically weak housing demand coupled with parabolic prices in the absence of meaningful “end-user” demand, sale volume, credit easing, or wage gains.

These are “symptoms” of rampant speculation, once again. In retrospect, most should now see that the period from the bottom of this cycle in Jan 2012 (not coincidentally just following when rates plunged on Twist and QE) to early 2014 when prices ended their parabola, was driven by stimulus-induced speculation, which is always a primary input to asset price bubbles.

In fact, from January 2012 — not coincidentally right after Twist and QE was put into place — through the peak of this cycle in June 2014, house prices rose by a bubbliscious 34%. Looking back, from Jan 2003 to June 2005 — a period affectionately known as the “housing bubble“ — prices only rose 33%. If it walks like a duck and quacks like a duck, then…

Volume is always supposed to precede price. It certainly did from 2002 to 2005. Then, volume fell off sharply from 2006-2007 when prices became out of reach for the end user to afford. On an apples to apples basis, prices today are certainly out of reach for the end-user; more expensive on a monthly payment basis than in 2006 by 20%. History proves that without underlying demand prices are volatile and unsustainable.

Bottom line: There was no “end-user” housing demand “recovery”. Rather, a speculator-driven “house price” super-inflation, which is abnormal and unsustainable in the absence of underlying strong demand driven by end-user wage or credit expansion. Existing sales demand – although anemic – bounced much harder than builder demand, which are still in depression, a feature unique to this speculative bubble in which single-family houses were purchased by institutional investors as bond and dividend stock replacements. The last time house prices were so diverged was in 2007.

Looking forward, the housing market will continue to seek out demand and will find it one way or another. It’s what it does. Stimulus and lower rates are not doing the trick any longer. As such, like in 2006, it’s my belief that the simplest path to increased demand is through lower prices, which will be the theme in 2015.

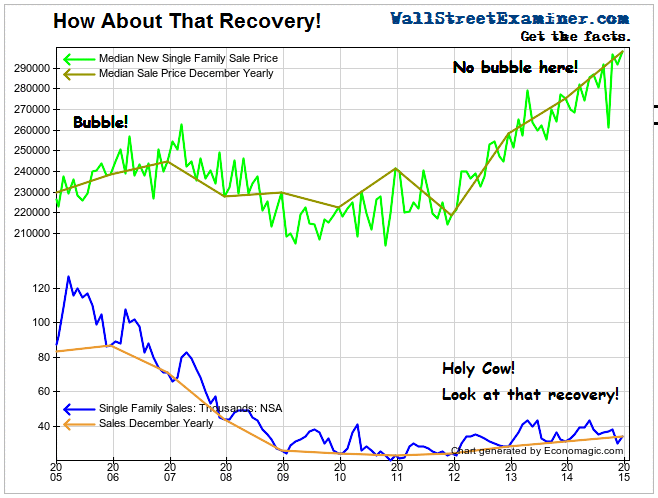

SF Housing In One Picture: Holy Cow! This Makes 6 Years Of Non-Recovery

by Lee Adler • January 27, 2015

The talking heads are gushing about December new home sales, but……..

[img [/img]

[/img]

In case you’re wondering, the seasonally adjusted (SA) headline, larger than expected gain, was due to calendar factors and the bogus drill of annualizing monthly SA data, which merely magnifies the monthly error times 12. But hey, who thinks about that! Certainly not mainstream financial news repeaters.

Builders typically don’t book sales on weekends, even though contracts are often signed on weekends. The worker bees who review the contracts and enter the data, work regular business hours Monday to Friday. Sales from November 29 and 30 were booked on December 1. That’s why the headline number “beat” Wall Street conomist consensus expectations. Likewise, the November number “missed” by a significant margin because those end of month sales in November weren’t booked in November, but in December.

To get around that problem I looked at the two months combined. This year, November-December actual monthly sales were down an average of 4,000 units from October. In 2013 they were down an average of 5,000. In 2012 they were down 1,000. So there’s just no news here. A drop of an average of 4,000 unit sales per month in November and December is par for the course for this time of year. At an average of 32,000 unit sales for November-December, total sales stink on a historical basis. There’s no sign in the current data that they will stop stinking any time soon.

When you take the time to look at the actual unadjusted data, you see these things. If you’re the mainstream media, you just ignore the facts and parrot everybody else–crowd behavior at its worst. So if you feel compelled to read and believe the headlines, you’ll be misled time and again. At least look at a chart of the actual data over time, see the trend for yourself, and ask yourself the question, “Has anything changed here.” Amidst all the media histrionics, either jumping up and down and cheering, or hand wringing and gnashing of teeth, most of the time the answer will be, “No, nothing has changed.” And that’s the answer here.