The facts speak for themselves. Your choice is to believe in the almighty ability of academic bankers to keep their confidence game going, or exit now before the apocalypse hits. I got no dog in this hunt. I ain’t selling newsletters, gold, or investment ideas. I strictly look at the facts. And they tell me to stay as far away from the financial markets as humanly possible. It isn’t a matter of if, only a matter of when. Here are the pertinent snippets from Hussman’s Weekly Letter:

Unless we observe a rather swift improvement in market internals and a further, material easing in credit spreads – neither which would relieve the present overvaluation of the market, but both which would defer our immediate concerns about downside risk – the present moment likely represents the best opportunity to reduce exposure to stock market risk that investors are likely to encounter in the coming 8 years.

Last week, the cyclically-adjusted P/E of the S&P 500 Index surpassed 27, versus a historical norm of just 15 prior to the late-1990’s market bubble. The S&P 500 price/revenue ratio surpassed 1.8, versus a pre-bubble norm of just 0.8. On a wide range of historically reliable measures (having a nearly 90% correlation with actual subsequent S&P 500 total returns), we estimate current valuations to be fully 118% above levels associated with historically normal subsequent returns in stocks. Advisory bullishness (Investors Intelligence) shot to 59.5%, compared with only 14.1% bears – one of the most lopsided sentiment extremes on record. The S&P 500 registered a record high after an advancing half-cycle since 2009 that is historically long-in-the-tooth and already exceeds the valuation peaks set at every cyclical extreme in history but 2000 on the S&P 500 (across all stocks, current median price/earnings, price/revenue and enterprise value/EBITDA multiples already exceed the 2000 extreme). Equally important, our measures of market internals and credit spreads, despite moderate improvement in recent weeks, continue to suggest a shift toward risk-aversion among investors. An environment of compressed risk premiums coupled with increasing risk-aversion is without question the most hostile set of features one can identify in the historical record.

Short term interest rates remain near zero, 10-year bond yields have declined below 2%, and our estimate of 10-year S&P 500 total returns has declined to just 1.4% (see Ockham’s Razor and the Market Cycle for the arithmetic behind these historically-reliable estimates). Recent weeks mark the first time in history that our estimates of prospective 10-year returns on all conventional asset classes have simultaneously declined below 2% annually. We don’t expect a portfolio mix of stocks, bonds and cash to achieve any meaningful return over the coming 8-year period. The fact that the financial markets feel wonderful right now is precisely because yield-seeking speculation and monetary distortions have raised security prices today to levels where they are likely to stand years from today – with steep roller-coaster rides in the interim.

Even so, historical considerations that have been effective in market cycles across history (and that also would have captured the majority of the market advance since 2009) presently suggest considerable risk of what we’ve often called an “air pocket” – similar to what we observed last October – over the coming 10-12 weeks, with much more severe downside risk possible over the course of the next 18-24 months.

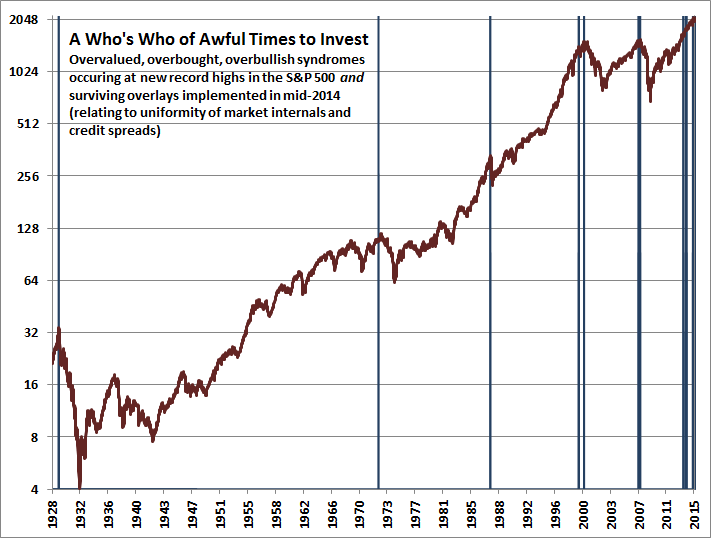

Extremes in observable conditions that we associate with some of the worst moments in history to invest include: Aug 1929 (with the October crash within 10 weeks of that instance), Aug-Oct 1972 (with an immediate retreat of less than 4%, followed a few months later by the start of a 50% bear market collapse), Aug 1987 (with the October crash within 10 weeks), July 1999 (associated with a quick 10% market plunge within 10 weeks), another signal in March 2000 (with a 10% loss within 10 weeks, a recovery into September of that year, and then a 50% market collapse), July-Oct 2007 (followed by an immediate plunge of about 10% in July, a recovery into October, and another signal that marked the market peak and the beginning of a 55% market loss), two earlier signals in the recent half-cycle, one in July-early Oct of 2013 and another in Nov 2013-Mar 2014, both associated with sideways market consolidations, and the present extreme.

On valuation measures most reliably correlated with actual subsequent market returns (a test that is never imposed on popular measures), current valuations now exceed 1929 levels.

The fact is that since 2000, the S&P 500 has achieved an annual total return of 4.1% annually, and doing so has required a speculative push to valuations exceeding those of every other market cycle in history, including 1929. In the interim, we’ve seen two separate market collapses of 50% and 55%, and I suspect that a third is in the offing. But again, the financial markets feel wonderful here precisely because security prices today already stand at the same levels that are likely to be seen 8-10 years from today, with one or two exciting roller-coaster rides in-between.

What we should all remember, however, is what happens when the Fed eases in an environment of risk-averse investor preferences: nothing. Recall that the Fed did not tighten in 1929, but instead began cutting interest rates on February 11, 1930 – nearly two and a half years before the market bottomed. The Fed cut rates on January 3, 2001 just as a two-year bear market collapse was starting, and kept cutting all the way down. The Fed cut the federal funds rate on September 18, 2007 – several weeks before the top of the market, and kept cutting all the way down. Understand that dynamic. The conflicting responses of the stock market to Fed easing can be resolved by remembering that monetary policy should always be examined through the lens of market internals.

The central banksters have been able to stave off disaster for more years than most of us have believed could happen. An unchanged truism: “Just because it’s inevitable doesn’t mean it’s imminent.” — Doug Casey.

Who knows? Everybody knows!

“With equity markets galore hitting record highs clearly I must be missing something big! We are at that stage in the cycle where I begin to doubt my own sanity. I’ve been here before though and know full well how this story ends and it doesn’t involve me being detained in a mental health establishment (usually).”

“Investors are transfixed instead by the Fed and when it will tighten rates and can’t see the wood for the trees. The Fed’s focus on payrolls, a lagging indicator, is most perplexing but not unusual at this stage in the cycle. The reality is that the vast bulk of economic, as well as earnings, data (even outside the energy sector), has been simply dreadful.”

Albert Edwards