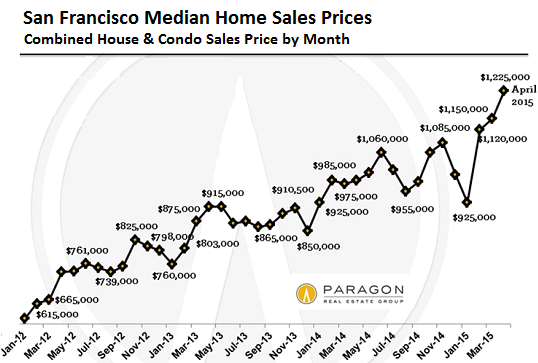

The charts below certainly reflect a rational free market trend. Right? Home prices always double in the space of three years when the economy is limping along with sub 2% GDP growth and median real household income is still 7% below the levels of 2007 and equal to levels of 1989. These are the median home prices, so they aren’t even skewed by the really high end prices.

San Francisco is now unaffordable to 99% of the US population. Only the richest of the rich can afford to live there. The titans of technology usually lean to the left and spout gibberish about equal rights, going green, and fighting poverty as they occupy gated estates with armed guards to keep the riff raff out. They want the rest of the country to do what they say, not what they do. They don’t want the peasants living near them. The help can live in Stockton and take the bus to arrive on time to clean their toilets.

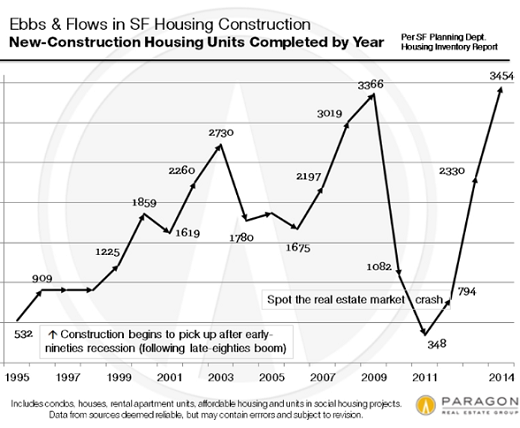

We’ve been here before, twice in the last fifteen years. If you thought the Dot.com created the biggest housing bubble in SF history, you would be wrong. New construction of homes tripled from 1998 to 2002 as Greenspan reduced interest rates and creating his first bubble. They then crashed by 40% over the next couple years. Greenspan re-inflated the bubble with even lower rates, doubling the number of new home constructed over the next three years. They then crashed by 90% over the next two years. Not to be outdone by the Maestro, Bennie and Yellen have kept interest rates at zero for the last six years, creating the biggest bubble in history. New homes built in SF are now 27% above the peak in 2002 and even higher than the housing bubble high in 2008.

We live in a bubble economy created and maintained by the Ivy League hacks at the Federal Reserve, whose only purpose is to do the bidding of their Wall Street owners and the .1% who occupy the NYC penthouse suites, the summer estates in the Hamptons, and the palatial mansion in San Jose. They don’t give a shit about you – the peasants. They’ve proven they can blow bubbles. They just have a little trouble maintaining them. I wonder how many tears will be shed when the SF housing bubble pops for the third time in the last fifteen years and a bunch of rich arrogant tech pricks take it up the ass?

In some parts of KY you could buy a small town for 1,225,000.00……. No bubble here.

Last and 3rd time.

No bubble here:

Amid boom, fears of too many $20 million Manhattan apartments

It’s getting crowded at the top of Manhattan’s apartment market.

As condo developers chase billion-dollar paydays through the construction of luxury dwellings, the cranes dotting the city are sparking fears of a supply glut.

Builders are plowing ahead with scores of condominiums priced above $20 million in skinny glass towers throughout Manhattan.

One building, the 66-story tower at 220 Central Park South, is listing more than 60 apartments above $20 million, according to filings made with the New York attorney general’s office. By comparison, in 2008, just 29 new condos sold for $20 million or more across all of Manhattan, according to appraisal firm Miller Samuel.

“There are a finite number of people that will buy these,” said Jonathan Miller, president of Miller Samuel. As for the developers kicking off projects now, “You are going to have haves and have-nots.”

The boom in the upper echelons of residential real estate is touching a handful of cities around the world, including London, Singapore and Dubai, where the global elite are pouring money into top-quality homes. But the demand is particularly acute in New York, reshaping its skyline to an extent few would have predicted during the real-estate bust.

There are signs demand for this rarefied product might be nearing its limits. The 1,004-foot green glass tower One57 remained about 25% unsold for much of last year. Its builder, Extell Development Co., lowered its expected total revenue from the building by about 4%, or $100 million, in part because of the slowdown, according to filings made with the Tel Aviv Stock Exchange in Israel, where Extell has issued $300 million in debt.

Extell founder Gary Barnett said sales have picked up substantially in the past couple months. He declined to discuss specifics but said he hoped to fully sell out the tower by the end of the year.

An expanded version of this report appears at WSJ.com.

More on New York real estate:

Bob.

Link to the original article:

http://www.wsj.com/articles/with-manhattan-luxury-property-hitting-highs-some-fear-air-is-getting-thin-1431458875?link=mktw

Bob

Foreign money parking their illicit gains and getting out of Dodge.

Or is the SF real estate market a preview of what hyperinflation looks like. Property values and wages are out of alignment in lots of places. I think it was bob who asked the right question somewhere else, where are the jobs that support these valuations?

My bad, rise up asked the question