Guest Post by Dr. Housing Bubble

The house humping pundits lock into anecdotal evidence and ignore larger changes in the housing market. For example, many kept harping on the fact that the Fed would never raise interest rates. Well here we are, with the first rate increase in many years. Many also claimed we were going to have a flood of Millennials buying homes but that also never materialized. The only thing they are focused on is price and that is being driven by big money, foreign investors, and people stretching their budgets to the max making their wallets burst at the seams.

The housing calculus overall is not good for most Americans. We have gained nearly 9 million rental households since 2005, the largest 10-year increase in history. At the same time, we have 8 million people that lost their home through foreclosure since 2004. Of these foreclosures 1 million happened in California, the perpetually sunny state. This seems to go against the notion that buying at any price makes sense. The reality is, we are undergoing a major rental revolution across the United States and a comprehensive Harvard study arrives at the same conclusion.

Renting instead of owning

It might be useful to add some color before diving into the study:

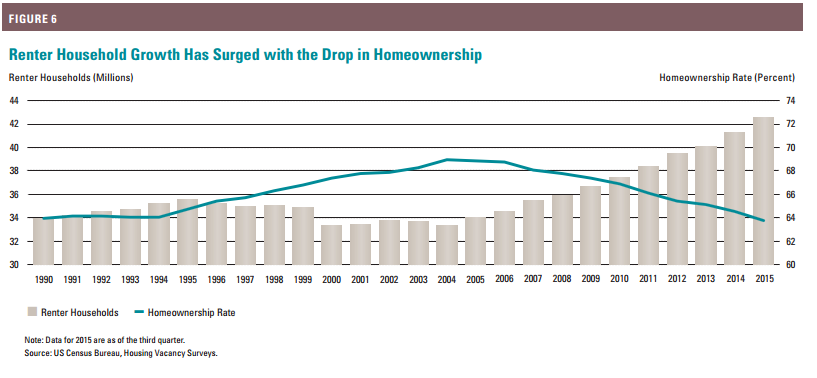

“The decade-long surge in rental demand is unprecedented. In mid-2015, 43 million families and individuals lived in rental housing, up nearly 9 million from 2005—the largest gain in any 10-year period on record. In addition, the share of all US households that rent rose from 31 percent to 37 percent, its highest level since the mid-1960s.

A number of factors have fueled soaring demand. The bursting of the housing bubble played an important role, with nearly 8 million homes lost to foreclosure since the homeownership rate peaked in 2004. Household incomes have also fallen back to 1995 levels and access to mortgage credit has tightened, making the transition to homeownership more difficult for many who might otherwise buy homes.”

I would add that mortgages are still easy to get if you have the income. The only thing that got “tightened” is the toxic junk mortgages but even those are making a slight comeback. This is not a minor change or a slight deviation from the norm. This is a big structural change in how people look at housing. The growth in rental households is so dramatic it has shifted our homeownership rate dramatically:

What is interesting is that we started seeing a steady nominal decline in rental households starting in 1995 all the way to 2004. Of course this coincided with the raging housing bubble. But since then, we’ve added nearly 9 million additional rental households.

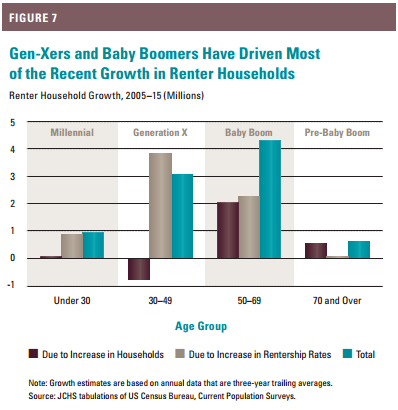

The idea is that somehow, this rental growth is being driven simply by younger households. We’ve already pointed out that in many high cost areas young people are stuck living at home with parents. The Harvard study backs this up and shows that older generations are the large driving force in rental growth:

The biggest rental household growth came from Generation X and the Taco Tuesday Baby Boomers. So much for thinking all of this rental growth was coming because of young Millennials being driven to rent. In fact, many Millennials can’t even afford the rent so they have to shack up with mom and dad or roommates.

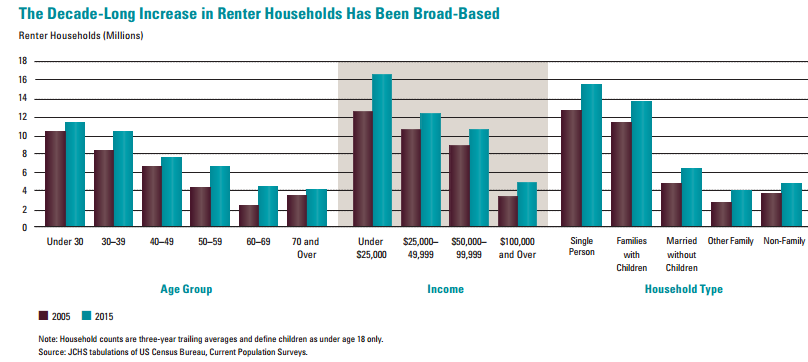

And this rental growth has been broad-based:

In other words, a rental revolution. Of course, a large part of this is being driven by stagnant incomes and housing prices outstripping any income gains. So how can prices rise? Introduce exogenous variables into local markets (i.e., foreign buyers, big money investors, flippers). Housing is driven at the margins. When inventory is tight, prices can zoom up especially in a low rate environment. We have seen this in many metro markets. But the opposite is also the case. When corrections hit, prices can slide at the margins quickly as well.

The rental growth is being driven by housing being unaffordable to many families. Affordability stems from household incomes. Those same people that thought the Fed would never raise rates are also the people that can’t foresee any correction in housing values. What the Harvard study finds is that millions are priced out and their only option is renting. And this is the “good” scenario as headline unemployment is low and the stock market has been in a six-year bull run. What happens when the inevitable correction hits?

I believe Obamacare tax and house tax will crush home ownership.That all property will be taxed back to the communist gov.Of course congress is exempt

What the hell is a “Taco Tuesday Baby Boomer”?

This is what happens when bankers use people as prey to enrich themselves “because they can”. It’s especially fruitful when the prey contributes to the scheme by being willfully ignorant and greedy.

Judging from the average renter my best friend has in his properties, these people are barely capable of maintaining a rental contract and should never have been allowed anywhere near a mortgage contract.

Personally, after the “treatment” I received from Chase, I would NEVER buy another house again unless through seller financing. Why? Because the big banks have proven to me beyond a shadow of a doubt that they can’t be trusted.

When your lender suddenly announces your fixed rate loan monthly payment is increasing by 1/3 for the next year, then $300 more per month for the remainder of the 30 year term, AND you have nothing to say about it, then it’s time out for me. And I think others feel the same way.

I/S- My client base is turning into “Taco -Tuesday”, “Ramen Noodle Wednesday” and “Frozen Pot Pie Friday” boomers. They are getting broker by the day and to top the cake have their adult children living off them.

The collapse is happening now, just slowly. The paced will accelerate and at that point get some Depends.

Umm- That should be (pace will accelerate).

@Bea said:

“They are getting broker by the day and to top the cake have their adult children living off them.”

Unfortunately, that’s mostly self inflicted. I don’t understand these parents who allow their kids to live “off” them as you say. My dad would put up with that shit for about one weekend then it would be “contribute or get the fuck out”. And by contribute, he would mean cash for rent/food/utilities AND manual labor such as lawn care, doing laundry, dishes, cooking, cleaning etc.

Time to invest in tents.

Can you believe, LLPOH, houses in East Santa Clarita selling for >$500K? This is the former community of Saugus! That would be like if Pasadena incorporated East LA and started selling old houses for premium prices.

Since we’ve been talking conspiracy theories, I might as well throw this out there. I think this “rental revolution” is being driven by someone or something nefarious. In my area, new construction of high density rental housing abounds. The rental market is good here but it always is fairly good anyway because of the subsidies for the military for housing.

Now go read Agenda 21 (or 30 or whatever they’re calling it these days). I think we’re being pushed into rentals, the higher the density the better.

@El Caballo

I could understand paying that here in Ventura but Santa Clarita is hot as balls and in the middle of nowhere. I wouldn’t live there if you gave me a house. When this bubble bursts, you wont be able to give a house away there.