Talk about not waiting for the body to get cold. The establishment oracles are out in force today proclaiming that Brexit has already been cancelled. Apparently, like in the case of the first negative vote on TARP, two days of currency and stock market turmoil have taught the rubes who voted for it the errors of their ways.

The argument is that the unwashed masses outside of Greater London have shot themselves in the foot economically based on some atavistic fears of immigrants and cultural globalization. Why, right soon they will demanding a second referendum in order to get back on the EU’s purported economic gravy train.

Thus, Gideon Rachman, one of the Financial Times’ numerous globalist scolds, professed that his depression about the Brexit vote has already given way to a worldly vision of relief:

But then, belatedly, I realised that I have seen this film before. I know how it ends. And it does not end with the UK leaving Europe.

Any long-term observer of the EU should be familiar with the shock referendum result. In 1992 the Danes voted to reject the Maastricht treaty. The Irish voted to reject both the Nice treaty in 2001 and the Lisbon treaty in 2008.

And what happened in each case? The EU rolled ever onwards. The Danes and the Irish were granted some concessions by their EU partners. They staged a second referendum. And the second time around they voted to accept the treaty. So why, knowing this history, should anyone believe that Britain’s referendum decision is definitive?

But of course Rachman’s dismissive meme is exactly why Brexit happened. The international financial apparatchiks, who have been controlling the levers of power at the central banks, finance ministries and supra-national official institutions for several decades now, have become so accustomed to not taking no for an answer that they can’t see the handwriting on the wall.

To wit, the rubes are feed up and are not going to take it anymore. In voting to flee the domineering EU superstate domiciled in Brussels, they saw right through and properly dismissed the establishment’s scary bedtime stories about the economic costs.

After all, the UK is a net payer of $10 billion per year in taxes into the EU budget and gets an economically wasteful dose of continental style regulatory dirigisme in return. And that is to say nothing of the loss of control at its borders and the de facto devolution of its law-making powers and judicial functions to unelected EU bureaucracies.

At the same time, increased trade is generally a benefit, but it is not one that requires putting up with the statist tyranny of the EU. That’s because the EU-27, and especially Germany, need the UK market for their exports far more than the other way around.

So after Brexit is triggered, the EU will come to the table for a new trade arrangement with the UK because these faltering socialist economies desperately need the exports. At the same time, the British negotiators will be free for the first time to seek more advantageous trade arrangements with the US, Canada, Australia and others.

It doesn’t take too much investigation to see that the UK has come out on the short end of the trade stick. And contrary to globalist apologists——-persistent and deepening trade deficits are a big problem. If coupled with a weakening savings rate, they mean that a country is getting ever deeper into international debt.

The UK economy exhibits that dual disability to a fare-the-well. Its current account has been plunging further into the red for 20 years. At 5% of GDP its current account deficit—-which includes the favorable benefits of service exports from the City of London and earnings on foreign investments—-is among the highest in the DM world.

To put it bluntly, the UK is slowly going bankrupt

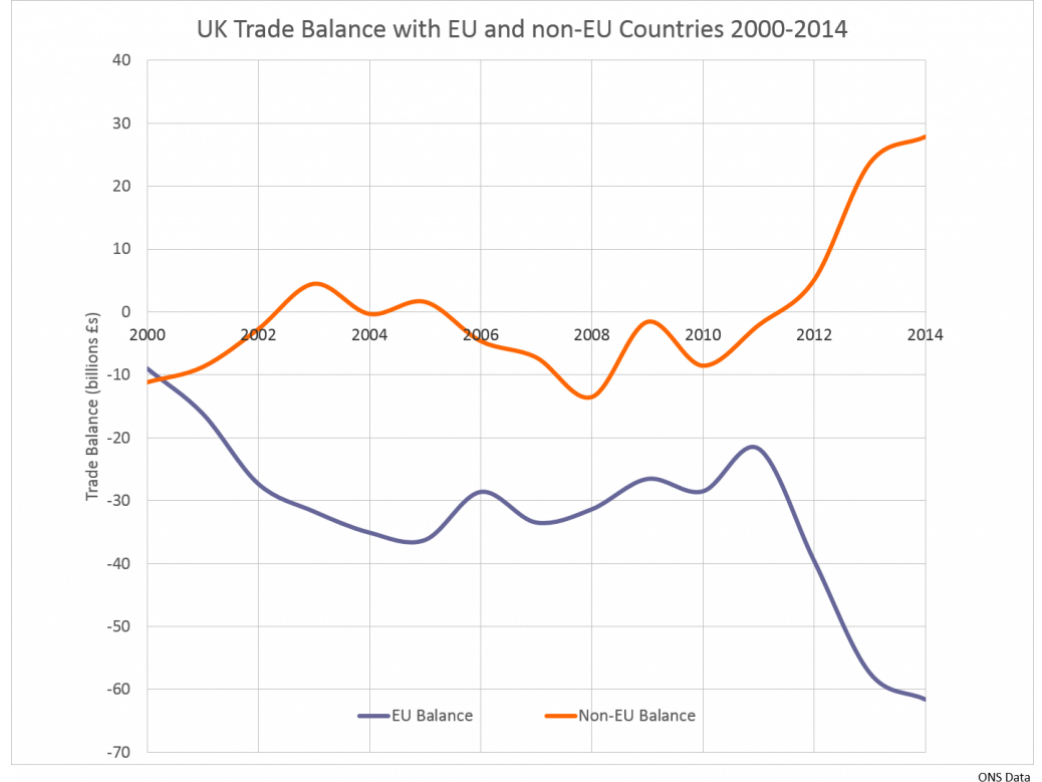

Moreover, the source of the abysmal overall current account trend shown above is absolutely attributable to its one-sided trade imbalance with the EU-27. As shown in the graph below, its EU deficit has been widening ever since 2000, while its trade surplus with the rest of the world has actually been steadily growing.

This point is not about mercantilism. The bilateral balance with any particular country or trading bloc does not ultimately matter if the overall current account trend is healthy.

Instead, the point is that the EU-27 needs British markets to the tune of a net $65 billion surplus annually. And more than half of that surplus is attributable to Germany, which earns upwards of 40% of its trade surplus with the rest of the EU from the UK.

Continuation of an open trade arrangement, therefore, does not require the sacrifice of British democracy and home rule to the statist overlords of Brussels; it only requires a trade deal that provides mutual economic benefits and no entangling engagements with the socialist infrastructure of the continent.

These negative trade trends are not ameliorated by a domestic savings frenzy that could finance the outflow in a healthy manner. To the contrary, the British household savings rate has been heading dangerously south for the last quarter-century.

Domestic savers are not financing the UK’s current account; foreign lenders and central banks are.

The same is true of the public sector. The UK has run chronic, deep budget deficits since the early 1990s. Since then, its public debt to GDP ratio has soared from 35% to nearly 85%.

These data make crystal clear, of course, that the UK has a giant problem of living far beyond its means, and that all of the leftist kvetching about the conservative government’s so-called “austerity” policies is a lot of political balderdash.

In fact, the Cameron government has buried British taxpayers in debt, even as it proclaimed its adherence to fiscal rectitude. As is evident from the chart, the only reduction in the spending share of GDP on its watch is due to the end of the global recession. At nearly 44%, state outlays still take a larger share of the economic production than they did under the Labour governments which preceded.

Here’s the point. Staying in the EU can not help ameliorate the UK’s real economic and fiscal problems in the slightest. What it needs is lower taxes, less welfare, and a dramatic reduction of government regulatory intervention. These are not policy directions that stir the juices in Brussels.

So today’s noisy meme that the Brexit voters have done themselves irreparable economic harm is patent nonsense. By contrast, whether they fully understood it or not, they have liberated the UK from what will be the economic disaster of “more Europe”.

Indeed, if there ever was a phrase that encapsulated the idea of an incendiary contradiction, “more Europe” is surely it. What it means to the French and Mediterranean Left is debt mutualization and a common treasury from which to expropriate German prosperity.

By contrast, to the Germans it means the imposition of ever more onerous EU fiscal controls so that it can continue to kick the can of its giant liabilities for the EU bailouts and ECB balances down the road.

(to be continued)

I think since low information voters always try to put money into their pocketbook, whomever can convince the most people they will give them free shit wins. Period.

Donald Trump will probably NOT win because he doesn’t seem to want to continue to give free shit away.

As for BREXIT? My Irish friend is “edumacating” me on the issue.

The title does not fit the article IMO. The UK like the US makes money off financial services not manufacturing therefore they are, like us printing to stay afloat. The Brits will be crying like little bitchez when they are paying 30% more for everything and begging to go back in time and change the vote. Stockman’s article says as much and like I said day one of this dog and pony show, it won’t mean anything in the end.

The rubes have voted for their own flogging and the elites are still 100% in control. Just a reminder, Rothschilds made 2.5 trillion last Friday (Brexit day) shorting global markets and going long gold.

Disagree – perhaps your view is too short-term. I don’t confuse the theme of ALL the developed countries printing money, vs the long-term future of Britain with independence. Being able to control immigration is THE canary in the coal mine, for example.

…………………..

I’m ecstatic – burn them all down.

Yo,

I’m using Firefox..After pasting the YT address I hit enter at least 3-4 times and bingo

Copy and paste a you tube address works for me every time.

It doesn’t hi-light as a link until after you select ‘post comment’ and then the page regenerates.

T4C says:

June 29, 2016 at 9:47 am

I can’t post pics anymore in the comments no matter which browser I use (Safari/Firefox).

——————

@T4C – put this immediately in front of your link/URL (remove the spaces–if I put it in with the spaces your browser will think it’s part of the HTML): [ i m g ]

Then put this immediately after the link/URL: [ / i m g ]

[img [/img]

[/img]

testing Youtube from my Firefox (fingers crossed…):

https://www.youtube.com/watch?v=jyRlnn_4CO0

Yumbo ,use that magic bottom to the right. Works on my smart phone every time.

“bottom” or “button”? Your smart phone isn’t too smart.

[img ?w=600&h=748[/img]

?w=600&h=748[/img]

Yeah, straight like that. Thanks. That “add images” button had made me forget HTML bootcamp from the past century.

Do you mean bootie-camp? ?. DAMN! That’s fine

Ed, you must have saved that booty picture I posted some time ago (not a very flattering one, I must say–I think I posted it just for you because you like big bottoms).

More to my liking…

[img ?quality=85&strip=info&w=600[/img]

?quality=85&strip=info&w=600[/img]