As close as you are ever going to get to complete honesty from a Federal Reserve Governor.

Via Dallas Fed President Richard Fisher

Beer Goggles, Monetary Camels, the Eye of the Needle and the First Law of Holes

During the holiday break, I spent a good deal of time trying to organize my thoughts on how I will approach monetary policy going forward. Today, I am going to share some of those thoughts that might be of interest to you as corporate directors.

At the last meeting of the Federal Open Market Committee (FOMC), it was decided that the amount of Treasuries and mortgage-backed securities (MBS) we have been purchasing should each be pared back by $5 billion, so that we would be purchasing a total of $75 billion a month (in addition to reinvesting the proceeds of maturing issues we hold) rather than $85 billion per month. In addition, it was noted that “if incoming information broadly supports the Committee’s expectation(s) … the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings.” And it was made clear that the FOMC expects it will hold the base rate that anchors the yield curve—the federal funds rate, or the rate on overnight money—to its present near-zero rate well past the time when unemployment is reduced to 6½ percent.

I was pleased with the decision to finally begin tapering our bond purchases, though I would have preferred to pull back our purchases by double the announced amount. But the important thing for me is that the committee began the process of slowing down the ballooning of our balance sheet, which at year-end exceeded $4 trillion. And we began—and I use that word deliberately, for we have more to do on this front—to clarify our intentions for managing the overnight money rate.

As an economist would say, “on net” I was rather pleased with the decision taken at the December FOMC meeting.

Under the chairmanship of Ben Bernanke, all 12 Federal Reserve Bank presidents, together with the sitting governors of the Federal Reserve Board, have input into the decision-making process. There is a formal vote—regardless of who is the Fed chair—that includes only five of the 12 regional Bank presidents plus the governors, but all of the principals seated at the table participate fully in the discussion of what to do. And yet, either because we will effect a change in the chairmanship starting in February or because at the last meeting we took the step of tapering back by a small amount our massive purchase of Treasuries and MBS, great attention is being placed on the voters for 2014, of which I am one.

Two comments I recently read have been buzzing around my mind as I think about the many issues that will condition my actions as a voter.

Beer Goggles …

The first was by Peter Boockvar, who is among the plethora of analysts offering different viewpoints that I regularly read to get a sense of how we are being viewed in the marketplace. Here is a rather pungent quote from a note he sent out on Jan. 2:

“…QE [quantitative easing] puts beer goggles on investors by creating a line of sight where everything looks good…”

For those of you unfamiliar with the term “beer goggles,” the Urban Dictionary defines it as “the effect that alcohol … has in rendering a person who one would ordinarily regard as unattractive as … alluring.” This audience might substitute “wine” or “martini” or “margarita” for “beer” to make it more age-appropriate, but the effect is the same: Things often look better when one is under the influence of free-flowing liquidity. This is one reason why William McChesney Martin, the longest-serving Fed chairman in our institution’s 100-year history, famously said that the Fed’s job is to take away the punchbowl just as the party gets going.[2]

… and the Eye of the Needle

The other eye catcher for me was a cartoon in the Jan. 6 issue of The New Yorker. Sitting in a room are two businessmen who are apparently conversant with the New Testament’s book of Matthew. One says to the other, “We need either bigger needles or smaller camels.”

Today, I want to muse aloud about whether QE has indeed put beer goggles on investors and whether we, the Fed, can pass the camel of massive quantitative easing through the eye of the needle of normalizing monetary policy without creating havoc.

Free and Abundant Money Changes Perspective

Boockvar is right. When money available to investors is close to free and is widely available, and there is a presumption that the central bank will keep it that way indefinitely, discount rates applied to assessing the value of future cash flows shift downward, making for lower hurdle rates for valuations. A bull market for stocks and other claims on tradable companies ensues; the financial world looks rather comely.

Market operators donning beer goggles and even some sober economists consider analysts like Boockvar party poopers. But I have found myself making arguments similar to his and to those of other skeptics at recent FOMC meetings, pointing to some developments that signal we have made for an intoxicating brew as we have continued pouring liquidity down the economy’s throat.

Among them:

- Share buybacks financed by debt issuance that after tax treatment and inflation incur minimal, and in some cases negative, cost; this has a most pleasant effect on earnings per share apart from top-line revenue growth.

- Dividend payouts financed by cheap debt that bolster share prices.

- The “bull/bear spread” for equities now being higher than in October 2007.

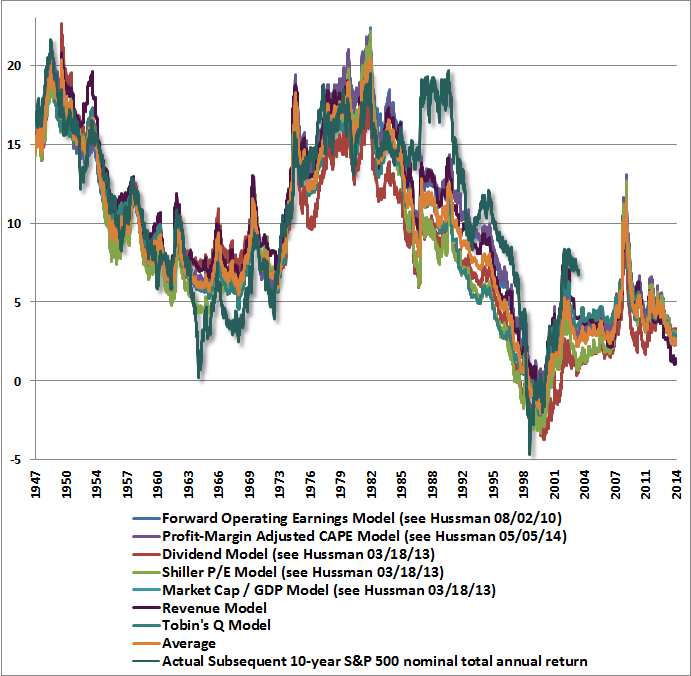

- Stock market metrics such as price-to-sales ratios and market capitalization as a percentage of gross domestic product at eye-popping levels not seen since the dot-com boom of the late 1990s.

- Margin debt that is pushing up against all-time records.

- In the bond market, investment-grade yield spreads over “risk free” government bonds becoming abnormally tight.

- “Covenant lite” lending becoming robust and the spread between CCC credit and investment-grade credit or the risk-free rate historically narrow. I will note here that I am all for helping businesses get back on their feet so that they can expand employment and America’s prosperity: This is the root desire of the FOMC. But I worry when “junk” companies that should borrow at a premium reflecting their risk of failure are able to borrow (or have their shares priced) at rates that defy the odds of that risk. I may be too close to this given my background. From 1989 through 1997, I was managing partner of a fund that bought distressed debt, used our positions to bring about changes in the companies we invested in, and made a handsome profit from the dividends, interest payments and stock price appreciation that flowed from the restructured companies. Today, I would have to hire Sherlock Holmes to find a single distressed company priced attractively enough to buy.

And then there are the knock-on effects of all of the above. Market operators are once again spending money freely outside of their day jobs. An example: For almost 40 years, I have spent a not insignificant portion of my savings collecting rare, first-edition books. Like any patient investor in any market, I have learned through several market cycles that you buy when nobody wants something and sell when everyone clamors for more. During the financial debacle of 2007–09, I was able to buy for a song volumes I have long coveted (including a mint-condition first printing from 1841 of Mackay’s Memoirs of Extraordinary Popular Delusions, which every one of you should read and re-read, certainly if you are contemplating seeing the movie The Wolf of Wall Street). Today, I could not afford them. First editions, like paintings, sculptures, fine wines, Bugattis and homes in Highland Park or River Oaks, have become the by-product of what I am sure Bill Martin would consider a party well underway.

I want to make clear that I am not among those who think we are presently in a “bubble” mode for stocks or bonds or most other assets. But this much I know: Just as Martin knew by virtue of his background as a noneconomist who had hands-on Wall Street experience, markets for anything tradable overshoot and one must be prepared for adjustments that bring markets back to normal valuations.

This need not threaten the real economy. The “slow correction” of 1962 comes to mind as an example: A stock market correction took place, and yet the economy continued to fare well.

Here is the point as to the market’s beer goggles. Were a stock market correction to ensue while I have the vote, I would not flinch from supporting continued reductions in the size of our asset purchases as long as the real economy is growing, cyclical unemployment is declining and demand-driven deflation remains a small tail risk; I would vote for continued reductions in our asset purchases, with an eye toward eliminating them entirely at the earliest practicable date.

How Large Is the Camel?

Let’s turn to the camel, by which I mean the size of the Fed’s balance sheet.

A little history provides some perspective. We began to grow our balance sheet as we approached year-end 2008. On Sept. 10, 2008, the amount of Reserve Bank credit outstanding was $867 billion. On Nov. 25, 2008, we announced a program to purchase $100 billion of securities issued by the housing-related government-sponsored enterprises, together with our intent to purchase up to $500 billion in MBS in order to goose the housing market. I supported these initiatives, recognizing that the economy was in the throes of a financial panic.

Following our December 2008 meeting, the FOMC announced that it had cut the target range for the fed funds rate to 0-to-1/4 of 1 percent, and being thus “zero bound,” we floated the idea of purchasing longer-term Treasuries in order to provide further monetary accommodation (when we buy Treasuries or MBS and agency debt, we put money into the financial system, substituting for further interest rate cuts). On March 18, 2009, we announced additional purchases of up to $750 billion of agency MBS and up to $100 billion of agency debt, plus purchases of up to $300 billion of longer-term Treasury securities over six months. That day, our balance sheet was marked at $2 trillion.

There are some details that impacted our balance sheet, which I have omitted so as not to bore you or entangle you in the entrails of central bank operations: For example, liquidity swaps with other central banks declined from a peak occasioned by the financial crisis of $583 billion the week ended Dec. 10, 2008, to $330 billion the following March, thus somewhat mitigating the growth of our balance sheet over that period.[3]

From my perch, I considered a balance sheet of $2-plus trillion and a base lending rate of 0-to-1/4 of 1 percent more than sufficient to stimulate not just the housing market but the stock market, too, thus placing us on the path of what economists refer to as “the wealth effect”—the working assumption that rising prices for homes, stocks and bonds floats the income boat of all Americans.

I basically said so publicly on March 26, 2009, in a speech to the RISE Forum, an annual student investment conference. At the time, the S&P 500 was priced at 814, the Nasdaq at 1,529 and the Dow at 7,750. The mindset of investors at that moment was summarized at an earlier FOMC meeting by one of my most esteemed colleagues at the Fed, who quipped that in looking at the balance sheets of most financial institutions, “nothing on the right is right and nothing on the left is left.” As I looked at the faces of the students gathered in that vast auditorium, I could see in their eyes a reflection of the gloom and doom of the time.

Here is what I told these young investors that dark morning: “… the current economic and financial predicament represents a potential gold mine rather than a minefield. Historically, great investors have made their money by climbing a wall of worry rather than letting a woeful consensus cow them. … Your job as investors is … to ferret out from the general-market malaise good financial and business operators whose franchises and prospects are overdiscounted at current prices. Were I you … I would be licking my chops at the opportunities that always abound in times of adversity. … There are a lot of dollar bills that can be found in the debris of the current markets that can be picked up for nickels and dimes.”

Of course, I would not mention this today had I been wrong! Currently, the right hand side of the balance sheet of most any well-managed market-traded business is chock-full of restructured, cheap debt and leaner common stock, while the left side is bulging with surplus cash. The S&P closed yesterday at 1,819, the Nasdaq at 4,113 and the Dow at 16,258—a plateau over two times above the valley into which they had descended in 2009.

And, again, there are the signs of conspicuous consumption I mentioned earlier that reflect a fully robust stock market. If there is indeed a wealth effect that spreads from clever market operators to the working people of America, a $2 trillion balance sheet might well have been sufficient to have performed the trick.

The FOMC is a committee, however, and the majority of my colleagues have disagreed with me on this point. We have since doubled our balance sheet to $4 trillion. This has resulted not only in saltatory[4] housing, bond and stock markets, but a real economy that is on the mend, with cyclical unemployment declining and inflation thus far held at bay.

Here is the rub. We have accomplished the last $2 trillion of balance-sheet expansion by purchasing unprecedented amounts of longer-maturity assets: As of Jan. 8, 2014, 75 percent of Federal Reserve-held loans and securities had remaining maturities in excess of five years.

A Narrow Needle Eye

The brow begins to furrow. To be sure, Treasury and MBS markets are liquid markets. But the old market operator in me is conscious that we hold nearly 40 percent of outstanding eligible MBS and of Treasuries with more than five years to maturity. Selling that concentrated an amount of even the most presumably liquid assets would be a heck of lot more complicated than accumulating it.

Currently, this is not an issue. But as the economy grows, the massive amount of money sitting on the sidelines will be activated; the “velocity” of money will accelerate. If it does so too quickly, we might create inflation or financial market instability or both.

The 12 Federal Reserve Banks house the excess reserves of the depository institutions of America: If loan demand fails to grow at the same rate as banks accumulate reserves due to our hyperaccommodative monetary policy, the resultant excess reserves are deposited with us at a rate of return of 25 basis points (1/4 of 1 percent per annum).

Here is some math confronting policymakers: Excess reserves are currently 65 percent of the monetary base and rising. The only other time excess reserves as a percentage of the base have come anywhere close to this level was at the close of the 1930s, when the ratio hit 41 percent. We are in uncharted territory.

To prevent excess reserves from fueling a too-rapid expansion of bank lending in an expanding economy, the Fed will need to either drain reserves on a large scale by selling longer-term assets at a loss or provide inducements to banks to keep reserves idle, by offering interest on excess reserves at a rate competitive with what banks might earn on loans to businesses and consumers. Or we might employ more widely new techniques we are currently testing, such as “reverse repos,” complex transactions in which we, in effect, borrow cash overnight from market operators while posting securities as collateral.

Such inducements to control the velocity of the monetary base might expose the Fed to intense scrutiny and criticism. The big banks that park the lion’s share of excess reserves with us are hardly the darlings of public sentiment. Raising interest payments to them while scaling back our remittances to the Treasury might raise a few congressional eyebrows. And as to our repo operations, we have never implemented them on anywhere near the scale envisioned.

Of greatest concern to me is that the risk of scrutiny and criticism might hinder policymakers from acting quickly enough to remove or dampen the dry inflationary tinder that is inherent in the massive, but currently fallow, monetary base.

In the parlance of central banking, the “exit” challenge we now face is somewhat daunting: How do we pass a camel fattened by trillions of dollars of longer-term, less-liquid purchases through the eye of the needle of getting back to a “normalized” balance sheet so as to keep inflation under wraps and yet provide the right amount of monetary impetus for the economy to keep growing and expanding?

The First Law of Holes

I have great faith in the integrity and brainpower of my fellow policymakers. I am confident that the 19 earnest women and men that make up the FOMC will do their level best under Chairwoman Janet Yellen’s leadership to accomplish a smooth exit that keeps prices stable and the economy in a job-creating mode. But my confidence will be bolstered if my colleagues adopt the First Law of Holes espoused in the late ’70s by then-British Chancellor of the Exchequer Denis Healey: “If you find yourself in a hole, stop digging.”

The housing market is well along in repair;[5] the economy is expanding; cyclical unemployment is declining. To be sure, there will be individual data points that appear to challenge confidence, like the just-released employment report for December. But I believe the odds favor continued economic progress. And I believe that continuing large-scale asset purchases risks placing us in an untenable position, both from the standpoint of unreasonably inflating the stock, bond and other tradable asset markets and from the perspective of complicating the future conduct of monetary policy.

The eye of the needle of pulling off a clean exit is narrow; the camel is already too fat. As soon as feasible, we should change tack. We should stop digging. I plan to cast my votes at FOMC meetings accordingly.