This is probably day 1,001 for some livestock on Hardscrabble’s farm.

As an Amazon Associate I Earn from Qualifying Purchases

Click to visit the TBP Store for Great TBP Merchandise

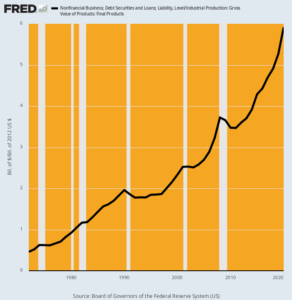

The massive leveraging of US nonfinancial businesses over the last several decades is utterly incompatible with the stock market cap rising from 62% to 204% of GDP.

The US business economy is now carrying 13X more leverage than it did 50 years ago.

Nonfinancial Business Debt as % of Gross Production, 1972–2020

Here is what has actually happened to business balance sheets:

In Part 1 of this article I pointed out how we have allowed ourselves to be cowed by authoritarian “experts” who have proven to be nothing but incompetent and wrong every step of the way, while the financiers have used the crisis once again to pillage the citizens as they did in 2008/2009.

The absurdity of shutting down this country based on academic death models that make economist and climatologist models look highly accurate in comparison, can be seen in the ludicrousness of the following chart. And realize we did this on purpose because of a virus that will kill .018% of the U.S. population. And most of those deaths will occur in several highly dense urban enclaves, with the rest of the country barely affected.

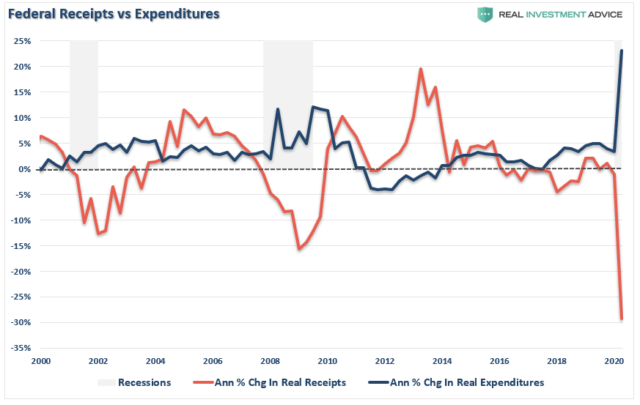

By shutting down the country the government has crushed virtually every business in the country and putting tens of millions out of work, with resulting crash in tax revenues at the Federal, State and Local level. At the same time, Trump and everyone in Congress have become Bernie Sanders socialists, except most of it is corporate socialism. The deficit was already on track to top $1.2 trillion, but with the $2.2 trillion stimulus package, and more to come, the deficit this year and next will approach $3 trillion.

“It has been more profitable for us to bind together in the wrong direction than to be alone in the right one. Those who have followed the assertive idiot rather than the introspective wise person have passed us some of their genes. This is apparent from a social pathology: psychopaths rally followers.” ― Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable

Continue reading “THE ROAD TO PERDITION IS PAVED WITH EVIL INTENTIONS – A FINAL RECKONING”

BTW, from The Black Swan, in 2007. pic.twitter.com/IdbFjunEg1

— Nassim Nicholas Taleb (@nntaleb) March 8, 2020

The black swan in plain sight does emit the Donald’s orangish glow, but at the end of the day its true color is actually red.

That is, monumental towers of rapidly rising debt loom everywhere on the planet. For the moment, the artificial cash flow from this unsustainable borrowing spree is keeping a simulacrum of growth and prosperity alive. Yet this whole outbreak of debt madness—-represented by $225 trillion outstanding on a global basis—-is careening toward a financial and economic dead end that will soon crush today’s fiscally profligate politicians and heedless financial punters, alike, in a devastating reset of bond yields.

For our first case in point, the always excellent Wolf Richter published a great chart over the weekend on the exploding US public debt. To say the least, it constitutes a clanging wake-up call amidst the absolute fantasy world that prevails on both ends of the Acela Corridor. That’s because during the mere 8 weeks since the public debt ceiling was suspended by the Donald’s end-run with Nancy and Chuckles in September, the national debt has spiked by $640 billion.

Continue reading “The Black Swan In Plain Sight—Debt Out The Wazoo”

“The inability to predict outliers implies the inability to predict the course of history”

― Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable

“I know that history is going to be dominated by an improbable event, I just don’t know what that event will be.” ― Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable

Nassim Taleb is a prickly arrogant SOB who doesn’t give a crap what intellectuals, academics, and other establishment elitists think about him. He has an Ivy league MBA, but despises everything about the curriculum of Ivy League MBA programs. He has a PhD, but scorns academics and their worship of theories and models. He enjoys poking holes in the storylines of the propaganda spewing corporate media. He glories in ridiculing the predictions of captured “experts” mouthing the talking points of whichever corporate interest is paying them blood money.

I read his brilliant Black Swan book back in 2008. It was a difficult read, but there were so many gems of wisdom throughout the book, it was a powerful tome predicting the financial collapse in real time. He wrote it in 2006. He understands the world doesn’t operate the way Ivy League models say it is supposed to operate. The world is propelled by black swans, not a normal distribution of the world. He was right in 2006 and he’s right now. The paragraph below has been making the rounds in the alternate media this past week. The establishment media would never publicize it, as their job is to protect the crumbling social order.

Submitted by Tyler Durden on 01/15/2015 06:07 -0500

“As if millions of macro hedge funds suddenly cried out in terror and were suddenly silenced”

Over two decades ago, George Soros took on the Bank of England, and won. Less than two hours ago the Swiss National Bank took on virtually every single macro hedge fund, the vast majority of which were short the Swiss Franc and crushed them, when it announced, first, that it would go further into NIRP, pushing its interest rate on deposit balances even more negative from -0.25% to -0.75%, a move which in itself would have been unprecedented and, second, announcing that the 1.20 EURCHF floor it had instituted in September 2011, the day gold hit its all time nominal high, was no more.

What happened next was truly shock and awe as algo after algo saw their EURCHF 1.1999 stops hit, and moments thereafter the EURCHF pair crashed to less then 0.75, margining out virtually every single long EURCHF position, before finally rebounding to a level just above 1.00, which is where it was trading just before the SNB instituted the currency floor over three years ago.

Visually:

The SNB press release:

Swiss National Bank discontinues minimum exchange rate and lowers interest rate to –0.75%

Target range moved further into negative territory

The Swiss National Bank (SNB) is discontinuing the minimum exchange rate of CHF 1.20 per euro. At the same time, it is lowering the interest rate on sight deposit account balances that exceed a given exemption threshold by 0.5 percentage points, to ?0.75%. It is moving the target range for the three-month Libor further into negative territory, to between –1.25% and -0.25%, from the current range of between -0.75% and 0.25%.

The minimum exchange rate was introduced during a period of exceptional overvaluation of the Swiss franc and an extremely high level of uncertainty on the financial markets. This exceptional and temporary measure protected the Swiss economy from serious harm. While the Swiss franc is still high, the overvaluation has decreased as a whole since the introduction of the minimum exchange rate. The economy was able to take advantage of this phase to adjust to the new situation.

Recently, divergences between the monetary policies of the major currency areas have increased significantly – a trend that is likely to become even more pronounced. The euro has depreciated considerably against the US dollar and this, in turn, has caused the Swiss franc to weaken against the US dollar. In these circumstances, the SNB concluded that enforcing and maintaining the minimum exchange rate for the Swiss franc against the euro is no longer justified.

The SNB is lowering interest rates significantly to ensure that the discontinuation of the minimum exchange rate does not lead to an inappropriate tightening of monetary conditions. The SNB will continue to take account of the exchange rate situation in formulating its monetary policy in future. If necessary, it will therefore remain active in the foreign exchange market to influence monetary conditions.

The resultant move across all currency pairs has seen the EUR and USD sliding, the USDJPY crashing, and US futures tumbling even as European stocks plunged only to kneejerk higher as markets are in clear turmoil and nobody knows just what is going on right now.

Submitted by Charles Hugh-Smith via OfTwoMinds blog,

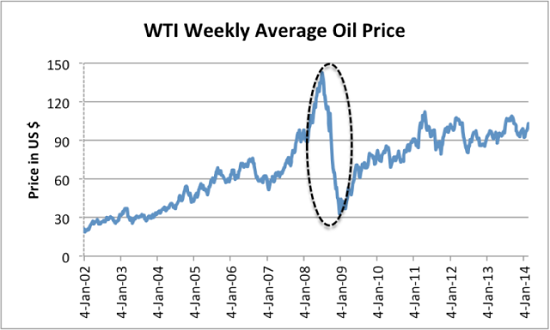

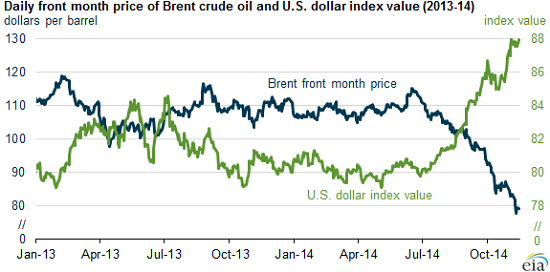

Given the presumed 17% expansion of the global economy since 2009, the tiny increases in production could not possibly flood the world in oil unless demand has cratered.

The term Black Swan shows up in all sorts of discussions, but what does it actually mean? Though the term has roots stretching back to the 16th century, today it refers to author Nassim Taleb’s meaning as defined in his books, Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets and The Black Swan: The Impact of the Highly Improbable:

“First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility.

Second, it carries an extreme ‘impact’.

Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.”

Simply put, black swans are undirected and unpredicted. The Wikipedia entry lists three criteria based on Taleb’s work:

1. The event is a surprise (to the observer).

2. The event has a major effect.3. After the first recorded instance of the event, it is rationalized by hindsight, as if it could have been expected; that is, the relevant data were available but unaccounted for in risk mitigation programs.

Every sustained action has more than one consequence. Some consequences will appear positive for a time before revealing their destructive nature. Some will be foreseeable, some will not. Some will be controllable, some will not. Those that are unforeseen and uncontrollable will trigger waves of other unforeseen and uncontrollable consequences.”