Here we go again. After a two year Wall Street engineered fraudulent boost in home prices in the exact markets that led the bubble in 2003 through 2007, the delusional dolts are now acting like the increase in home equity is real. Do delusional idiots congregate in California, Nevada, Florida, Arizona and Ohio for a reason? The morons in these markets are ramping up new home equity lines of credit at a 60% to 90% pace over the prior year.

It’s as if the lesson of the previous bubble was completely forgotten in a couple years. Are these people really that dumb? The housing market started rolling over six months ago. Prices peaked, new single family home sales peaked, existing home sales peaked and the Wall Street investors are exiting stage left. Now the very same Wall Street hucksters want you to borrow against the artificially inflated value of your house and spend that money on more shit you don’t need, or to lease a brand new Escalade. It’s called the American Way. So it goes.

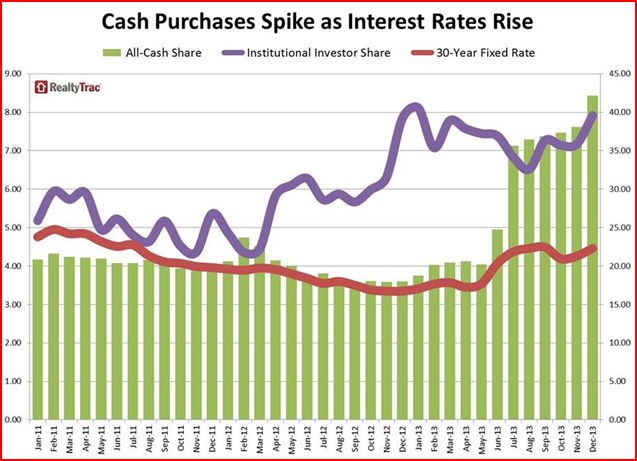

Via RealtyTrac

HELOC Share of Total Loans at Highest Level Since 2008

Biggest Jumps in Inland California, Las Vegas, Cincinnati, Phoenix

RVINE, Calif. – Oct. 9, 2014 — RealtyTrac® (www.realtytrac.com), the nation’s leading source for comprehensive housing data, today released its first-ever U.S. Home Equity Line of Credit Trends Report, which found that in the 12 months ending in June 2014 a total of 797,865 Home Equity Lines of Credit (HELOCs) were originated nationwide, up 20.6 percent from a year ago and the highest level since the 12 months ending in June 2009.

The report also shows HELOC originations accounted for 15.4 percent of all loan originations nationwide during the first eight months of 2014, the highest percentage since 2008.

“This recent rise in HELOC originations indicates that an increasing number of homeowners are gaining confidence in the strength of the housing recovery and, more importantly, have regained much of their home equity lost during the housing crisis,” said Daren Blomquist. “Nearly 10 million homeowners nationwide, representing 19 percent of all homeowners with a mortgage, now have at least 50 percent equity in their homes, according to RealtyTrac data. Meanwhile the percentage of homeowners with severe negative equity has decreased from 29 percent in the second quarter of 2012 to 17 percent in the second quarter of this year.

“The rise in HELOCs also reflects a natural evolution for a lending industry looking for products they can offer to homeowners who have already refinanced their first position loan into a low fixed rate,” Blomquist added. “A HELOC enables homeowners to leverage additional equity they may have gained since refinancing while still preserving the rock-bottom interest rate on their first position loan.”

Inland California, Las Vegas, Cincinnati, Phoenix post biggest annual increases

Among the nation’s 50 largest metropolitan statistical areas with HELOC data available, 49 posted year-over-year increases in HELOC originations in the 12 months ending in June 2014. The only metro area with a decrease was Rochester, N.Y., where HELOC originations decreased 1 percent.

Metro areas with the biggest year-over-year increase in HELOC originations were Riverside-San Bernardino in Southern California (87.7% increase), Las Vegas (85.1% increase), Cincinnati (81.0% increase), Sacramento (65.1% increase), and Phoenix (60.1% increase).

Major metros with the smallest increases in HELOC originations from a year ago were Minneapolis-St. Paul (0.2 percent increase), Louisville, Ky., (3.3 percent increase), Philadelphia (3.6 percent increase), Virginia Beach (4.3 percent increase), and St. Louis (5.6 percent increase).

U.S. HELOC originations 76 percent below 2005-2006 peaks

Despite the year-over-year increases, HELOC originations were well below their peaks from the previous housing boom. Nationwide, the 797,865 HELOC originations in the 12 months ending in June 2014 were 76 percent below the previous peak of 3,299,007 in the 12 months ending in June 2006. The 15.4 percent share of HELOCs year-to-date nationwide was also below the 24.7 percent share in 2005.

HELOC originations were below their previous peaks in 49 out of the nation’s 50 largest metro areas. The only exception was Pittsburgh, where HELOC originations reached a new peak in the 12 months ending in June 2014.

Major metro areas with the biggest decrease in HELOC originations in 2014 compared to their previous peaks were Riverside-San Bernardino (down 93 percent), Las Vegas (down 92.9 percent), Miami (down 92.5 percent), Tucson, Ariz., (down 92.4 percent), and Orlando (down 92.2 percent).

HELOCs biggest share of originations in Honolulu, Upstate NY, Cleveland, Milwaukee

Among the nation’s 50 largest metro areas, those with the highest share of HELOC originations as a percentage of all loan originations year-to-date in 2014 were Honolulu (43.5 percent), Rochester, N.Y., (38.7 percent), Buffalo, N.Y., (32.1 percent), Cleveland (28.5 percent), and Milwaukee (27.5 percent).

Major metro areas with the lowest share of HELOC originations as a share of all loan originations year-to-date in 2014 were Las Vegas (5.8 percent), Dallas (6.5 percent), Riverside-San Bernardino (7.7 percent), Houston (7.9 percent), and Tucson, Ariz. (8.0 percent).

Other markets where HELOC originations represented less than 10 percent of all loan originations year-to-date in 2014 were Atlanta (8.1 percent), San Antonio (8.6 percent), Oklahoma City (9.2 percent), and Austin (9.9 percent).

Report methodology

The RealtyTrac U.S. Home Equity Line of Credit Trends Report provides counts of HELOC loans originated and the HELOC share of total loans originated using mortgage and deed of trust records collected in more than 900 counties nationwide with a combined population of more than 240 million, representing 78 percent of the U.S. population. Home Equity Lines of Credit are non-purchase loans that are secured by the equity (the appraised market value of that property minus any other loans secured by that property) and can be used by homeowners to fund home improvement projects or other purchases.