‘If you’re committed enough, you can make any story work. I once told a woman I was Kevin Costner, and it worked because I believed it’ – Saul Goodman – Breaking Bad

“As calamitous as the sub-prime blowup seems, it is only the beginning. The credit bubble spawned abuses throughout the system. Sub-prime lending just happened to be the most egregious of the lot, and thus the first to have the cockroaches scurrying out in plain view. The housing market will collapse. New-home construction will collapse. Consumer pocketbooks will be pinched. The consumer spending binge will be over. The U.S. economy will enter a recession.” – Eric Sprott – 2007

In Part One of this article I provided the background of how our current debt saturated economy got to this point of ludicrousness. The “crazy” bloggers, prophets of doom, and analysts who could do basic math were warning of an impending financial crisis in 2006 and 2007, which would be caused by the issuance of hundreds of billions in subprime slime by the Too Big To Trust Wall Street shysters. Subprime mortgages, auto loans, and credit card lines provided the kindling for the 2008 conflagration.

Under normal circumstances we wouldn’t have seen such irrational, reckless, greedy behavior from Wall Street for another generation. But, Wall Street didn’t have to accept the consequences of their actions. They were bailed out and further enriched by their puppets at the Federal Reserve, the lackey politicians they installed in Washington D.C., and on the backs of honest, hard-working, tax paying Americans. The lesson they learned was they could continue to take excessive, reckless, unregulated risks without concern for losses, downside, or consequences.

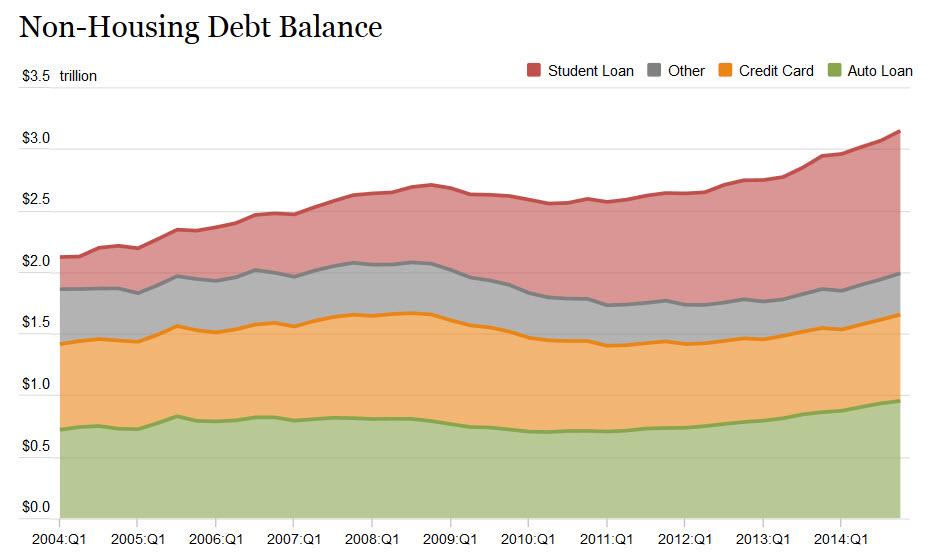

In reality, the Fed and government have worked in tandem with Wall Street to create the subprime economic recovery. The scheme has been to revive the bailed out auto industry by artificially boosting sales through dodgy, low interest, extended term debt. With the Feds taking over the entire student loan market, they have doled out hundreds of billions to kids who don’t have the educational skills to succeed in college, in order to keep them out of the unemployment calculation.

That’s why you have a 5.7% unemployment rate when 41% of the working age population (102 million people) is not working. The appearance of economic recovery has been much more important to the ruling class than an actual economic recovery for average Americans, because the .1% have made out like bandits anyway. Who has benefited from the $650 billion of student loan and auto debt disseminated by the oligarchs in the last four years, the borrowers or lenders?

Continue reading “BREAKING BAD (DEBT) – EPISODE TWO”