The group that would benefit most from abolishing either, or all, of the three income taxes is the 1%, and if they have to pay any income tax, they’d prefer the currency-regulating income tax established in Springer v. U.S. (1880), which is the income tax most of us are dealing with today (though we tend not to recognize the Springer origins of the tax).

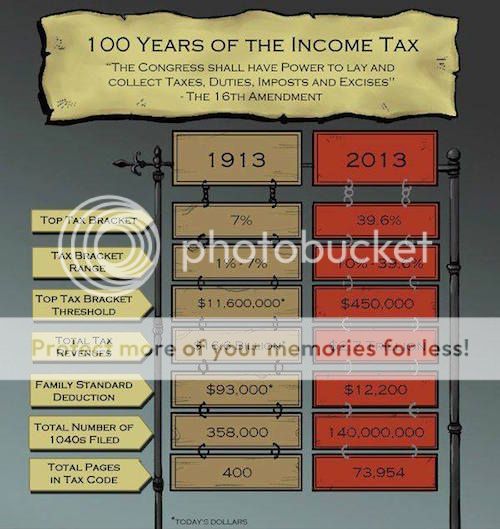

The 1% favor the “Springer income tax” because in recent decades they’ve succeeded in destroying the progressivity of the tax (which is now around 40% on the top income bracket, but used to be as high as 94%), substantially reduced the rates on capital gains (to about 15%-20%, below half the top bracket rate), and created key loopholes that entirely exempt some unearned income.

In this Doc, I’d like to experiment with labeling the 3 income taxes by the Supreme Court cases which Constitutionalized the tax. Hopefully, this will make the distinction between the three income taxes easier to understand, rather than trying to explain them from discussions about the 16th Amendment, which is always how the 1% want to frame the discussion, i.e., that the 16th Amendment is the cause of the problem and we’d all be better off without it.

As I often warn so-called tax protesters, abolishing the 16th Amendment would make matters much worse because it would simply exempt taxation of landlords, lenders, employers and speculators (the targets of the “Pollock income tax”) from the Springer income tax, while keeping wage-earners firmly in its grip.

THE “SPRINGER INCOME TAX”

I often call this the “currency-regulating income tax” or the “legal tender privilege income tax,” but the tax is basically derived from England’s 1799 income tax, which was used by the Crown to support the Bank of England as it came off the coin standard.

The U.S. version was first levied 1862-1872, the Civil War income tax. William Springer, an attorney, challenged the tax on his 1865 law practice earnings (along with some interest income) in Springer v. U.S. (1880), but lost his case. He argued that the income tax on his wages was a direct tax on his personal property, and therefore that the tax needed to be apportioned under the Direct Tax Clauses (which meant Congress couldn’t collect the tax; only levy it against the states).

The Supreme Court did not explain themselves very well, but essentially held that since the target of the tax was on Springer’s use of currencies not issued and controlled exclusively by the peoples’ Congress (the U.S. “sovereign”), the tax was ruled to be indirect on Springer’s wages.

In effect, because Springer received his wages in currencies not under Congress’s direct and exclusive control, his “wages as personal property” (which could only be levied under the Direct Tax Clauses) was converted into “wage income” (which could easily be levied under the Indirect Tax Clause).

The word “income” was not yet in the Constitution when Springer lost his case, but nevertheless the Court in 1880 considered the tax on Springer’s income to be an indirect “income duty” or “income excise tax” under Article 1, Section 8, Clause 1 (the Indirect or Uniformity Clause).

As I just mentioned, one of the problems with the Springer case was that in addition to “wage income” he also earned some interest income, so in addition to money “incoming” to Springer from national banks and their (legal tender) notes, money was also coming from Springer’s savings, his personal property.

Some pro-Georgist Congressmen accentuated the difference between the two income taxes in the 1894 income tax by adding a tax on landlord rental income, where land was the personal property of the landlord, from which the rental income was derived. The Supreme Court struck down this 1894 income tax in Pollock v. Farmers’ Loan (1895), and because of this, I will refer to taxes on income derived from property sources as “Pollock income taxes.”

I sometimes refer to this income tax as the “property income tax” or “tax on property income” or “tax on income derived from property,” but since Pollock is the case that really highlighted this kind of income tax, I think it’s most appropriate to use that case name.

Incidentally, as many of you know, it was the ruling in Pollock that led to the need for the 16th Amendment, though it’s hard to tell by simply reading the Amendment.

Unfortunately, the 16th Amendment was worded in such a way that makes it appear to have authorized all income taxes in the U.S., when really all it did was eliminate the idea that rental or interest income might be a direct tax on land, labor or capital.

Another common misconception advanced about the 16th Amendment is that it simply blocks us from considering the source of the income, and that all income essentially comes from the same source.

To further prove the point that the 16th Amendment was not the origin of all three U.S. income taxes, in 1909 Congress levied an income tax on corporate privilege, where the corporation’s net income was used to measure the benefit enjoyed while exercising the state-granted privilege.

In Flint v. Stone Tracy Co. (1911) the corporate officers, directors and shareholders challenged the tax and made the same argument that Springer tried to make, i.e., that any tax on the corporation was a direct tax on property, and therefore a violation of the Direct Tax Clauses, which required Congress to apportion such tax liability among the states.

I sometimes refer to this as the “corporate privilege income tax” or “tax on income derived from corporation privilege.”

The Supreme Court disagreed, and essentially used the same argument used by the Springer Court, which is that since the tax is targeting the privilege only, and using income only to measure the benefit under the privilege, the tax is indirect on property, not a direct tax on property ownership, like for example, taxing one’s house, car, bicycle, etc.

The final point I’d like to make in this Doc is that there are only two classes of income taxes, (1) those derived from property sources, and (2) those not derived from property (i.e., government-granted privilege).

This is an important distinction to keep in mind because with “taxes on income not derived from property sources,” the income is simply used to measure the benefit. In other words, the income is really not the prime target, but only used to give the government some reasonable way to fairly tax the (corporate or legal tender) privilege holder (or not tax the privilege holder if there was a loss).

Anyway, the Springer and Stone Tracy income taxes are in the class of income taxes that are NOT derived from the property sources of land, labor or capital, but the Pollock income tax IS in that class.

So, for example, even if a tax patriot were to totally avoid the corporate and legal tender privileges, income tax liability could still arise under the “Pollock income tax” if there was evidence that the individual was acting like a landlord, lender, employer or speculator. These human actors create, respectively, the following kinds of income: rental income, interest income, profits from hiring labor, capital or land gains.

SSS

April 16, 2015 11:31 pm

Brian

I read your similarly long, lawyerly post over on “Tax Day.” Both are dull and boring. Are you writing something for your Juris Doctorate?

This blog isn’t an online course for students in a college of law, nor are we sitting judges on a federal Circuit Court of Appeals. Get to the fucking point, which seems to be your support of the 16th Amendment.

Brian

April 16, 2015 11:42 pm

Well SSS, I guess you don’t really want to know why you’ve been fucked up the ass all your life along with the rest of us. Repealing the 16th amendment will do nothing to end the income tax on wages which is the most offensive tax there is, IMO. Is it really that hard to understand? Perhaps I thought those on here we more enlightened. This is why nothing will ever change because no one will get into the technicalities that make you liable.

Anonymous

April 17, 2015 12:28 am

Brian, whether it’s income tax or excise tax or some other concoction, it’s the financing of all the non Constitutional crap (everything from welfare to studies of brazillian sexual practices) that eat up our money and cause the problems we are facing.

Get rid of everything the government is doing that is not directly permitted it in the Constitution and almost all of our problems are solved.

It’s the amount of debt based spending and the amount of taxation needed to service that debt that is the problem, not the type of taxation used to collect it.

Brian

April 17, 2015 1:57 am

Anon, The 3 primary income taxes are all excise taxes. I agree we as a country need to end the stupid spending on stuff that is twisted into the “general welfare” clause of the constitution. The biggest problem is that people can’t tell the difference between the different types of income tax, they are all lumped together and confused. On purpose. The Springer income tax on wages which finds it authority through the Veazie bank case, legal tender cases, and McCullough.

In order to be liable for an excise tax you have to do something that makes you liable. Like buying gas, smokes, or beer. Don’t buy it….don’t pay the tax. The income tax on wages is the same, but it is hidden. The common wisdom is they are taxing your labor or more properly your time. That is not the case, that would be direct as your time is your property.

What are you paid in? Dollars? Are you sure? Your payroll checks are either handled by direct deposit or old school paper. You sign them, you then deposit them in a bank. Have you received dollars? When you sign a paycheck, you are signing a contract. Your signature and nothing else is a blank endorsement basically telling the bank to do whatever and they do, paying your check in bank credit. Congrats you are now liable for the income tax on wages. Any wage payment not made in money issued directly by the U.S. Treasury (currently coin or USN’s) is bank credit and a taxable event per Veazie Bank v. Fenno.

So for all the downvoter aging boomer fucks who perpetuated this system, fuck you! I’m trying to figure out what happened through years of researching this subject. What are you doing besides bitching all day and night about shit you can’t control. Does no one wants to see the mechanism of their enslavement? The Federal Fucking Reserve!

The group that would benefit most from abolishing either, or all, of the three income taxes is the 1%, and if they have to pay any income tax, they’d prefer the currency-regulating income tax established in Springer v. U.S. (1880), which is the income tax most of us are dealing with today (though we tend not to recognize the Springer origins of the tax).

The 1% favor the “Springer income tax” because in recent decades they’ve succeeded in destroying the progressivity of the tax (which is now around 40% on the top income bracket, but used to be as high as 94%), substantially reduced the rates on capital gains (to about 15%-20%, below half the top bracket rate), and created key loopholes that entirely exempt some unearned income.

In this Doc, I’d like to experiment with labeling the 3 income taxes by the Supreme Court cases which Constitutionalized the tax. Hopefully, this will make the distinction between the three income taxes easier to understand, rather than trying to explain them from discussions about the 16th Amendment, which is always how the 1% want to frame the discussion, i.e., that the 16th Amendment is the cause of the problem and we’d all be better off without it.

As I often warn so-called tax protesters, abolishing the 16th Amendment would make matters much worse because it would simply exempt taxation of landlords, lenders, employers and speculators (the targets of the “Pollock income tax”) from the Springer income tax, while keeping wage-earners firmly in its grip.

THE “SPRINGER INCOME TAX”

I often call this the “currency-regulating income tax” or the “legal tender privilege income tax,” but the tax is basically derived from England’s 1799 income tax, which was used by the Crown to support the Bank of England as it came off the coin standard.

The U.S. version was first levied 1862-1872, the Civil War income tax. William Springer, an attorney, challenged the tax on his 1865 law practice earnings (along with some interest income) in Springer v. U.S. (1880), but lost his case. He argued that the income tax on his wages was a direct tax on his personal property, and therefore that the tax needed to be apportioned under the Direct Tax Clauses (which meant Congress couldn’t collect the tax; only levy it against the states).

The Supreme Court did not explain themselves very well, but essentially held that since the target of the tax was on Springer’s use of currencies not issued and controlled exclusively by the peoples’ Congress (the U.S. “sovereign”), the tax was ruled to be indirect on Springer’s wages.

In effect, because Springer received his wages in currencies not under Congress’s direct and exclusive control, his “wages as personal property” (which could only be levied under the Direct Tax Clauses) was converted into “wage income” (which could easily be levied under the Indirect Tax Clause).

The word “income” was not yet in the Constitution when Springer lost his case, but nevertheless the Court in 1880 considered the tax on Springer’s income to be an indirect “income duty” or “income excise tax” under Article 1, Section 8, Clause 1 (the Indirect or Uniformity Clause).

http://en.wikipedia.org/wiki/Springer_v._United_States

THE “POLLOCK INCOME TAX”

As I just mentioned, one of the problems with the Springer case was that in addition to “wage income” he also earned some interest income, so in addition to money “incoming” to Springer from national banks and their (legal tender) notes, money was also coming from Springer’s savings, his personal property.

Some pro-Georgist Congressmen accentuated the difference between the two income taxes in the 1894 income tax by adding a tax on landlord rental income, where land was the personal property of the landlord, from which the rental income was derived. The Supreme Court struck down this 1894 income tax in Pollock v. Farmers’ Loan (1895), and because of this, I will refer to taxes on income derived from property sources as “Pollock income taxes.”

I sometimes refer to this income tax as the “property income tax” or “tax on property income” or “tax on income derived from property,” but since Pollock is the case that really highlighted this kind of income tax, I think it’s most appropriate to use that case name.

Incidentally, as many of you know, it was the ruling in Pollock that led to the need for the 16th Amendment, though it’s hard to tell by simply reading the Amendment.

Unfortunately, the 16th Amendment was worded in such a way that makes it appear to have authorized all income taxes in the U.S., when really all it did was eliminate the idea that rental or interest income might be a direct tax on land, labor or capital.

Another common misconception advanced about the 16th Amendment is that it simply blocks us from considering the source of the income, and that all income essentially comes from the same source.

http://en.wikipedia.org/wiki/Pollock_v._Farmers%27_Loan_%26_Trust_Co.

THE “STONE TRACY INCOME TAX”

To further prove the point that the 16th Amendment was not the origin of all three U.S. income taxes, in 1909 Congress levied an income tax on corporate privilege, where the corporation’s net income was used to measure the benefit enjoyed while exercising the state-granted privilege.

In Flint v. Stone Tracy Co. (1911) the corporate officers, directors and shareholders challenged the tax and made the same argument that Springer tried to make, i.e., that any tax on the corporation was a direct tax on property, and therefore a violation of the Direct Tax Clauses, which required Congress to apportion such tax liability among the states.

I sometimes refer to this as the “corporate privilege income tax” or “tax on income derived from corporation privilege.”

The Supreme Court disagreed, and essentially used the same argument used by the Springer Court, which is that since the tax is targeting the privilege only, and using income only to measure the benefit under the privilege, the tax is indirect on property, not a direct tax on property ownership, like for example, taxing one’s house, car, bicycle, etc.

http://en.wikipedia.org/wiki/Flint_v._Stone_Tracy_Company

ONE FINAL DISTINCTION

The final point I’d like to make in this Doc is that there are only two classes of income taxes, (1) those derived from property sources, and (2) those not derived from property (i.e., government-granted privilege).

This is an important distinction to keep in mind because with “taxes on income not derived from property sources,” the income is simply used to measure the benefit. In other words, the income is really not the prime target, but only used to give the government some reasonable way to fairly tax the (corporate or legal tender) privilege holder (or not tax the privilege holder if there was a loss).

Anyway, the Springer and Stone Tracy income taxes are in the class of income taxes that are NOT derived from the property sources of land, labor or capital, but the Pollock income tax IS in that class.

So, for example, even if a tax patriot were to totally avoid the corporate and legal tender privileges, income tax liability could still arise under the “Pollock income tax” if there was evidence that the individual was acting like a landlord, lender, employer or speculator. These human actors create, respectively, the following kinds of income: rental income, interest income, profits from hiring labor, capital or land gains.

Brian

I read your similarly long, lawyerly post over on “Tax Day.” Both are dull and boring. Are you writing something for your Juris Doctorate?

This blog isn’t an online course for students in a college of law, nor are we sitting judges on a federal Circuit Court of Appeals. Get to the fucking point, which seems to be your support of the 16th Amendment.

Well SSS, I guess you don’t really want to know why you’ve been fucked up the ass all your life along with the rest of us. Repealing the 16th amendment will do nothing to end the income tax on wages which is the most offensive tax there is, IMO. Is it really that hard to understand? Perhaps I thought those on here we more enlightened. This is why nothing will ever change because no one will get into the technicalities that make you liable.

Brian, whether it’s income tax or excise tax or some other concoction, it’s the financing of all the non Constitutional crap (everything from welfare to studies of brazillian sexual practices) that eat up our money and cause the problems we are facing.

Get rid of everything the government is doing that is not directly permitted it in the Constitution and almost all of our problems are solved.

It’s the amount of debt based spending and the amount of taxation needed to service that debt that is the problem, not the type of taxation used to collect it.

Anon, The 3 primary income taxes are all excise taxes. I agree we as a country need to end the stupid spending on stuff that is twisted into the “general welfare” clause of the constitution. The biggest problem is that people can’t tell the difference between the different types of income tax, they are all lumped together and confused. On purpose. The Springer income tax on wages which finds it authority through the Veazie bank case, legal tender cases, and McCullough.

In order to be liable for an excise tax you have to do something that makes you liable. Like buying gas, smokes, or beer. Don’t buy it….don’t pay the tax. The income tax on wages is the same, but it is hidden. The common wisdom is they are taxing your labor or more properly your time. That is not the case, that would be direct as your time is your property.

What are you paid in? Dollars? Are you sure? Your payroll checks are either handled by direct deposit or old school paper. You sign them, you then deposit them in a bank. Have you received dollars? When you sign a paycheck, you are signing a contract. Your signature and nothing else is a blank endorsement basically telling the bank to do whatever and they do, paying your check in bank credit. Congrats you are now liable for the income tax on wages. Any wage payment not made in money issued directly by the U.S. Treasury (currently coin or USN’s) is bank credit and a taxable event per Veazie Bank v. Fenno.

So for all the downvoter aging boomer fucks who perpetuated this system, fuck you! I’m trying to figure out what happened through years of researching this subject. What are you doing besides bitching all day and night about shit you can’t control. Does no one wants to see the mechanism of their enslavement? The Federal Fucking Reserve!