This week John Hussman’s pondering about the state of our markets is as clear and concise as it’s ever been. He starts off by describing the difference between an economy operating at a low level versus a high level. He’s essentially describing a 2% GDP economy versus a 4% GDP economy. We have been stuck in a low level economy since 2008. And there is one primary culprit for the suffering of millions – The Federal Reserve and their Wall Street Bank owners. They are the reason incomes are stagnant, the labor participation rate is at 40 year lows, savers can only earn .25% on their savings, and consumers have been forced further into debt to make ends meet. Meanwhile, corporate America and the Wall Street banks are siphoning off record profits, paying obscene pay packages to their executives, buying off the politicians in Washington to pass legislation (TPP) designed to enrich them further, and arrogantly telling the peasants to work harder.

In economics, we often describe “equilibrium” as a condition where demand is equal to supply. Textbooks usually depict this as a single point where a demand curve and a supply curve intersect, and all is right with the world.

In reality, we know that economies often face a whole range of possible equilibria. One can imagine “low level” equilibria where producers are idle, jobs are scarce, incomes stagnate, consumers struggle or go into debt to make ends meet, and the economy sits in a state of depression – which is often the case in developing countries. One can also imagine “high level” equilibria where producers generate desirable goods and services, jobs are plentiful, and household income is sufficient to demand all of that output.

The problem is that troubled economies don’t just naturally slide up to “high level” equilibria. Low level equilibria are typically supported and reinforced by a whole set of distortions, constraints, and even incentives for the low level equilibrium to persist. In developing countries, these often take the form of legal restrictions, price controls, weak property rights, political and civil instability, savings disincentives, lending restrictions, and a full catastrophe of other barriers to economic improvement. Good economic policy involves the art of relaxing constraints where they are binding, and imposing constraints where their absence allows the activities of some to injure or violate the rights of others.

In the United States, observers seem to scratch their heads as to why the economy has shifted down to such a low level of labor force participation. Even after years of recovery and trillions of dollars directed toward persistent monetary intervention, the economy seems locked in a low level equilibrium. Yet at the same time, corporate profits and margins have pushed to record highs, contributing to gaping income disparities.

Dr. Hussman presents his case against the Federal Reserve as clearly as anything I’ve ever read. Bailing out criminally negligent Wall Street banks with taxpayer money, allowing fraudulent accounting to cover up insolvency, printing $3 trillion out of thin air and handing it to the Wall Street banks, penalizing savings while encouraging consumers and corporations to go further into debt, and gearing all of your efforts towards creating stock, bond, and real estate bubbles, is the height of lunacy – unless you are a captured entity working on behalf of a corrupt status quo.

From our perspective, the fundamental reason for economic stagnation and growing income disparity is straightforward: Our current set of economic policies supports and encourages a low level equilibrium by encouraging debt-financed consumption and discouraging saving and productive investment. We permit an insular group of professors and bankers to fling trillions of dollars about like Frisbees in the simplistic, misguided, and repeatedly destructive attempt to buy prosperity by maximally distorting the financial markets. We offer cheap capital and safety nets to too-big-to-fail banks by allowing them to speculate with the same balance sheets that we protect with deposit insurance. We pursue easy monetary fixes aimed at making people “feel” wealthier on paper, far beyond the fundamental value that has historically backed up that wealth. We view saving as dangerous and consumption as desirable, failing to recognize a basic accounting identity: there can only be a “savings glut” in countries that fail to stimulate investment. We leave central bankers in charge of our economic future because we’re too timid to directly initiate or encourage productive investment through fiscal policy. When zero interest rates don’t do the trick, we begin to imagine that maybe negative interest rates and penalties on saving might coerce people to spend now. Look around the world, and that same basic policy set is the hallmark of economic failure on every continent.

Our leaders have failed the American people. We had an opportunity as a country in 2009 to purge our system of our unpayable debt. We could have allowed the orderly liquidation of the Too Big To Fail Wall Street banks, GM, Chrysler, and thousands of other over indebted bloated corporate pigs. We would have had a short deep depression. The excesses would have been wrung out of our economic system and we would have experienced a real recovery based upon savings and investment. Instead we allowed politicians and central bankers to do the complete opposite. We believed their lies. The system was not going to collapse if the Wall Street banks went down. Rich people and bankers would have been wiped out.

When a country allows its central bank to encourage yield-seeking speculative malinvestment; suppresses interest rates in a way that punishes those on fixed incomes and destroys the incentive to save; allows too-big-to-fail institutions to use deposit insurance as a public subsidy to expand trading activity instead of traditional banking; focuses fiscal policy on boosting transfer payments to make up for lost income without at the same time encouraging investment – both private and public – that could create new sources of income; that country is going to keep failing its people.

Jim Grant, Bill Gross and a number of other truth telling financial analysts have described how QE and ZIRP have done nothing but allow zombie corporations which should have gone bankrupt to survive and contribute to the low level economy we are experiencing. The creative destruction essential to produce a dynamic economy has been outlawed by the Federal Reserve. The encouragement of consumption through low interest rates has failed. Economies grow through investment, not consumption.

Every economy funnels its income toward factors that are most scarce and useful. If a country diverts its resources toward consumption and speculation rather than productive investment, it shelters the profitability of existing companies by making their capital more scarce and therefore more profitable, while at the same time discouraging new job creation. A vast pool of unused labor also has little ability to demand more compensation. In contrast, when an economy encourages productive investment at every level, more jobs are created, and yet capital becomes less scarce – so profit margins fall back to normal. The income from economic activity is then available to both labor and capital, rather than funneling income into a basket that reads “winner-take-all.”

It seems the Fed’s motto is: “The Lunacy Will Continue Until Moral Improves”. The Fed has accomplished only one thing over the last six years – creating multiple bubbles with no exit plan that will not pop those bubbles. The Fed has trapped themselves and there is no way out. They must either raise rates now and trigger the next market collapse or wait and trigger an even larger collapse. Hussman thinks legislation may be necessary to restrain the Fed, but he fails to realize the politicians are captured by the very banks who control the Fed.

We need to re-think which constraints are actually binding us. With trillions of dollars sitting idly in bank reserves, and interest rates next to zero, the Federal Reserve continues to behave as if bank reserves and interest rates are a binding constraint – that somehow loosening those further might free the economy to grow. This is lunacy. Fed policy is no longer relieving constraints; it is introducing distortions. That – not the exact level of wage growth, inflation, or unemployment – is the primary reason to normalize policy, and to start along that path as soon as possible. Current Fed policy discourages saving while diverting the little saving that remains toward yield-seeking malinvestment. If the members of the FOMC cannot restrain themselves from extraordinary policy distortions on their own, it may be time for legislation to explicitly remove the discretion from their hands.

Those who think low interest rates will forever sustain extremely overvalued financial markets are kidding themselves. First of all, the Fed can’t ease. When interest rates are at 0%, there is no place left to go. The credibility of the Fed is already declining rapidly. Once faith in their ability to elevate markets is lost, the collapse will commence. The slope of hope will become the crash of cash.

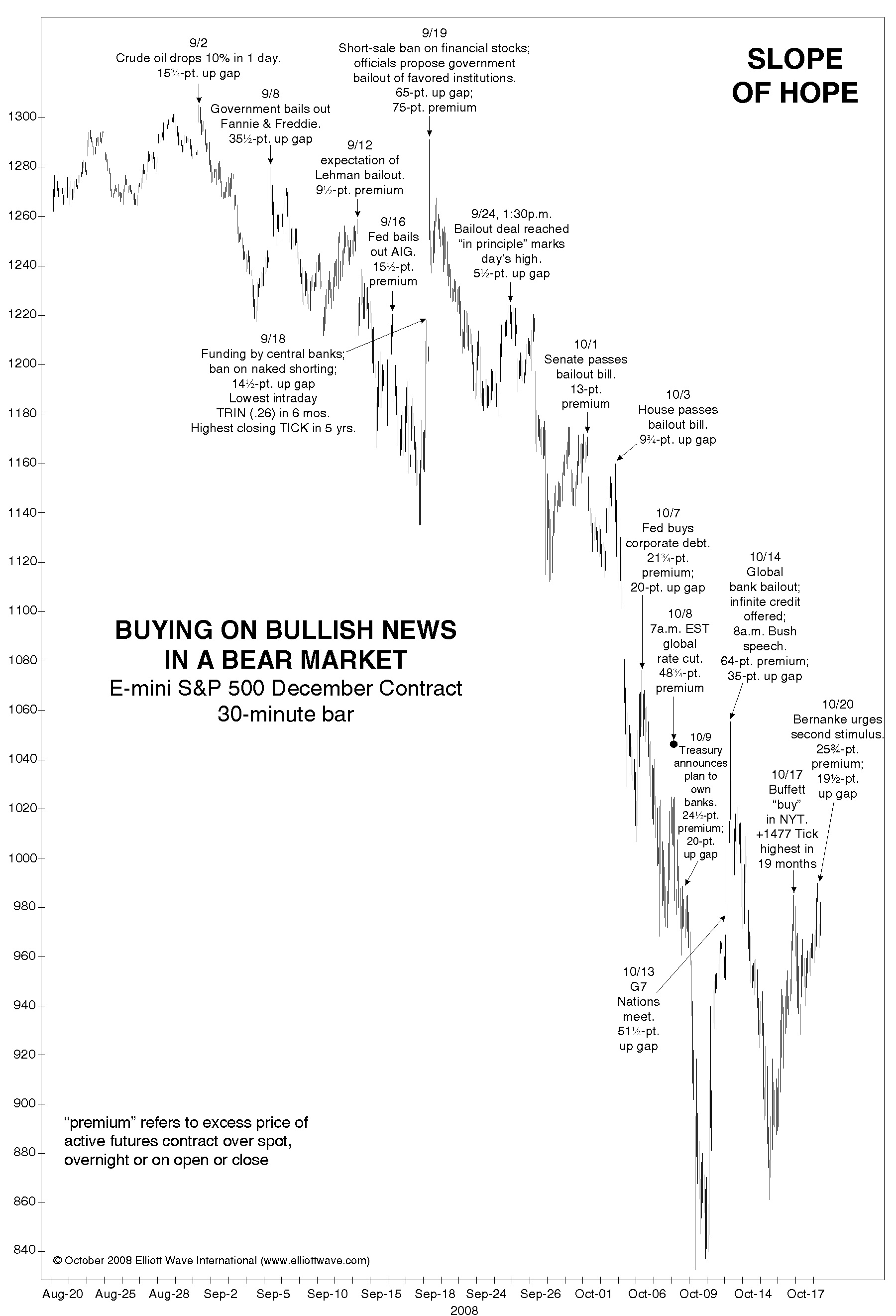

The difficulty with creating a bubble of speculative distortion is that there is always hell to pay, and once valuations have already been driven to extreme levels, that hell is baked in the cake. It can’t be avoided, and once investors have shifted toward risk-aversion, history indicates it can’t even be managed well. Recall that the Fed was easing persistently and continuously throughout the 2000-2002 and 2007-2009 market collapses. As a reminder of how fruitless official interventions can be once investors have shifted to risk-aversion, I’ve reprinted the instructive chart that Robert Prechter of EWT published in October 2008, as the S&P 500 was on its way to the 700 level. Investors who actually believe that Fed easing creates a “put option” for stocks have a very short memory of the past two bear market collapses.

As Sergeant Esterhaus used to say on Hill Street Blues, be careful out there. We are presently at the 2nd most overvalued point in stock market history. It’s dangerous out there. The Fed doesn’t have your back. Anyone in the stock market today has a high likelihood of losing 50% of there money in a very short time. If you think you can get out when everyone else decides to get out, you’re a lunatic. Lunacy does seem to be the primary trait amongst our financial elite, political class, and willfully ignorant masses.

Be careful here – deteriorating internals matter. The condition of market internals is precisely the same hinge that – in market cycles across history – has separated overvalued markets that continued to advance from overvalued markets that collapsed through a trap door.

Put simply, the recent market peak represents the second most overvalued point in history for the capitalization-weighted stock market, and the single most overvalued point in history for the broad market.

When weak participation has been accompanied by rich valuations, scarce bearish sentiment, and recent market highs, the number of instances narrow to some of the worst points in history to invest.

When weak participation, rich valuations and scarce bearish sentiment accompanied a record high in the same week, the handful of instances diminish to surround the precise market highs of 1973, 2000, and 2007, as well as 1929 on imputed sentiment data – and the week ended July 17, 2015.

Understand that the present deterioration of market internals is broad-based, unusual, and historically dangerous.

So Noted…Mike

I for one am sick of the daily “guess which way the Fed is moving” charade. And you’re absolutely right Admin, a huge crash is coming. Put simply, things are fucked up and shit.

“In the United States, observers seem to scratch their heads as to why the economy has shifted down to such a low level of labor force participation.”

The analysis is fine but don’t you think that our gov’t is complicit in sending our manufacturing jobs overseas as part of the UN Social Justice agenda and to de-industrialize the western developed economies.This has a definite impact on the labor participation rate.

Westcoast , what do your hippie brothers and sisters say about all the shit the is fucked up and shit ?

@bb and Westcoaster

Get it right…”Shit is fucked up and bullshit.”

Should my wife and I empty our 401s?

My guess is that the next 12 months will include a major decline in the markets, but the US banking system will remain intact.

If Mr. Market is on script (a big if), a major bounce will follow the expected decline, and after the bounce will come the real fireworks…at the end of which should be a banking “event.”

I sure hope we get some warning on the bank issue. Greek citizens had a solid 3 months of warning before their SNAFU.

What incredibly moronic and utterly stupid assertions. The Federal Reserve has nothing whatsoever to do with the stock markets. Helllllllllllllooooooooooooooooooo?

by Karl Denninger

Paying Attention Yet?

One thing I’ve said repeatedly over the years is that on the evidence The Fed doesn’t actually “set” rates; rather, it follows the market.

This is not universally true, but an overlay of actual short-term rates with the Fed Funds rate shows that most of the time, by a wide margin, the market moves first and the Fed basically gets dragged by the nose in the direction the market wishes to go.

If you think about it this makes sense; nobody can subsidize an uneconomic transaction forever, yet this is exactly what you’d have to do if you were going to “fight” the market on a permanent basis. Either you can lead the market or you can’t, but if you can’t then you must conform to it because otherwise you will run out of money — it is simply a matter of when.

So with that backdrop, you might want to read this…

NEW YORK (Reuters) – As traders, market pundits and economists jaw over whether the Federal Reserve this year will lift its benchmark lending rate for the first time in almost a decade, several corners of the U.S. bond market are not waiting around.

A wide range of short-term interest rates, which tend to be the most sensitive to Fed policy expectations, has been quietly grinding higher for weeks, or in some cases much longer. Several have even surpassed their levels of two years ago during the bond market’s “taper tantrum,” when prices dropped steeply and yields shot up as the Fed pondered whether to halt its massive asset-purchase program.

This has nothing to do with what traders “expect”; it has everything to do with the fact that below-market rates rob people and eventually those who are getting robbed revolt by demanding a higher coupon!

The Fed wants you to believe that it can drag the market around by the nose. It cannot; at best it can jawbone and threaten, and if you believe them then you will do what they want.

But if not it is The Fed, not the market, that has to make the adjustment.

Adam Price representing the willfully ignorant masses.

Thanks for dropping by you dumbass douchebag.

Hovnanian Shares Plummet 14 Percent, Homebuilders Standing At The Precipice

by Aaron Layman

“Oh, what a tangled web we weave, when first we practice to deceive.”

Shares of Hovnanian Enterprises fell out of bed again today, plummeting 14 percent to close at $1.71 per share. Hovnanian Enterprises (HOV) is now down a whopping 50 percent YTD, with no signs of the hemorrhaging ending anytime soon. If anything, the drop in Hovnanian’s stock seems to be picking up steam. Other homebuilders were clipped today as well. Beazer Homes (BZH) dropped more than 6 percent today after reporting tepid third quarter results, and several other builders were selling off with Hovnanian’s demise. How could a national homebuilder be self-destructing before our eyes in this supposedly robust economy? Well, it’s simple really. This is the type of carnage and destruction that results when you intervene in markets, attempt to remove risk, inflate asset prices to the moon, and absolve banks from the consequences of their actions.

Of course U.S. homebuilders have been keen to buy into the “recovery” story because it sounds good and there are always homes to sell. As NAR keeps telling us, the water is fine, so jump on in! Interest rates are low, and there are homes for sale that need families in them. Never mind the fact that the rate of U.S. homeownership is at a new 48-year low. Never mind the fact that wage growth is still in the basement while asset prices have spiraled upward. The stock market is just a few percentage points from an all-time high, so everything is surely awesome right? Home prices are still climbing in many U.S. markets, so this is a sign of growth and household formation right?

As I’m watching some local neighborhood home prices roll over, I can’t help but think about the wonderful correlation between the Fed’s balance sheet and the markets. This is something Lance Roberts was musing about yesterday as well. The correlations between the Federal Reserve’s balance sheet and the S&P index deserve more than a little bit of scrutiny. By all appearances, the Fed is the market, interjecting themselves at every turn to prop up the latest bubbles and keep the illusion of growth alive. Lord knows they have inserted a whole host of distortions into the U.S. housing market, and I think Hovnanian Enterprises (aka Brighton Homes) is just the first of what could be several unfortunate victims of a potential mean reversion.

It has been quite an impressive ride. What happens now is anybody’s guess, but it doesn’t take a rocket scientist to see why the Fed keeps jawboning about raising the Fed Funds rate. They have done such a bang-up job of inflating asset prices, that there’s now a shortage of people willing to buy those same artificially inflated assets. If this sounds like a variation of the Shanghai stock market Ponzi scheme, well you’re probably not far off track. By all appearances the the real economy is now choking to death, but it seems our central bankers are willing to overlook this pesky problem because that would necessitate some serious self-reflection and admission of guilt. Will the Fed be able to prop up the markets at current levels? Only time will tell, but the oil market and real estate sector are already pointing to some potentially nasty outcomes. Or as Lance put it:

“The bad news is that the Fed’s own history suggests a probability of success approaching something closer to zero.”

Folks, you know it’s planned!!

M2 is only around $12 trlllion and has not increased by $4 trillion since 2008. None of the QE funds increased the money supply at all but only served to increase the MONETARY BASE with 100% of those funds remaining inside the Federal Reserve.

The Federal Reserve only purchases about 8% of the around $7 trillion a new US Treasuries each year and 92% of those are purchased by PARTIES OTHER THAN THE FEDERAL RESERVE EACH YEAR.

Banks lend to many parties other than the US Treasury and their current outstanding loans to deposits ratio is around 67%. The balance of customer deposits is used to buy US Treasuries, MBS instruments, and put in their reserve and excess reserves accounts inside the federal Reserve.

The Federal Reserve HAS NOT PRINTED ANY MONEY AT ALL TO LEND TO THE US TREASURY as that would be monetizing the federal debt which THEY DO NOT DO AT ALL. The Federal Reserve simply created money to PURCHASE EXISTING US TREASURIES with 100% of those funds GOING TO THE BANKS AND THEN INTO THEIR EXCESS RESERVES ACCOUNTS INSIDE THE FEDERAL RESERVE and with NONE (ZERO) OF THAT MONEY GOING TO THE US TREASURY.

Adam Price

Get the Federal Reserve Dildo out of your ass.

If you actually believe QE and ZIRP haven’t driven stock, bond and real estate markets higher, you are dumber than sack of hammers.

Go jack off to a picture of Janet Yellen and peddle your propaganda elsewhere.

NO MONEY FROM THE FEDERAL RESERVE GOES TO BANKS AT ALL other than for ASSET PURCHASES such as was done with QE and 100% OF THE PROCEEDS FROM QE WERE DEPOSITED IN THE EXCESS RESERVES ACCOUNTS OF THOSE BANKS FROM WHOM THE FEDERAL RESERVED PURCHASE SECURITIES INTO THEIR EXCESS RESERVES ACCOUNTS INSIDE THE FEDERAL RESERVE which is where 100% of those QE funds have always been.

Not a single penny of funds from the Federal Reserve ever went into the stock markets or ever goes into the stock markets.

QE HAS ABSOLUTELY NOTHING TO DO WITH THE STOCK MARKETS and it effectively ended LAST DECEMBER.

You obviously have no comprehension as to what the Federal Reserve versions of QE were and what they were not at all.

FEDERAL RESERVE VERSION OF QE EXPLAINED:

1) Federal Reserve buys securities from banks

2) Federal Reserve deposits cash proceeds in excess reserves accounts of those banks at the Federal Reserve

3) Securities stay parked on assets side of Federal Reserve GL

4) Proceeds funds stay parked on liabilities side of Federal Reserve GL in the excess reserves accounts of the banks at the Federal Reserve

The process is an ENTIRELY CLOSED LOOP just as if it were done inside a VACUUM.

http://www.federalreserve.gov/releases/h8/current/

http://www.federalreserve.gov/monetarypolicy/bst_fedfinancials.htm

How many times does this have to be stated before it actually sinks in, folks?

The QE funds are sitting parked in the excess reserves accounts of the banks and none of them ever got into the economy at all as is clearly established y the evidence on that matter. The total amounts in those excess reserves accounts now exceeds $2.5 trillion.

EXCESS RESERVES ACCOUNTS OF BANKS TOP $2.5 TRILLION – WSJ

So what exactly are excess reserves, and why should you care? Like most central banks, the Fed requires banks to hold reserves—mainly deposits in their “checking accounts” at the Fed—against transactions deposits. Any reserves held over and above these requirements are called excess reserves.

Not long ago—say, until Lehman Brothers failed in September 2008—banks held virtually no excess reserves because idle cash earned them nothing. But today they hold a whopping $2.5 trillion in excess reserves, on which the Fed pays them an interest rate of 25 basis points—for an annual total of about $6.25 billion. That 25 basis points, what the Fed calls the IOER (interest on excess reserves), is the issue.

http://online.wsj.com/news/articles/SB10001424052702303997604579238403178592262

As to the stock markets, the primary drivers of those markets have been the publicly listed stock companies themselves with HUGE SHARE BUYBACKS plowing back nearly all of their record earnings plus record bo0rrowing s into the stock markets to pump up the prices of their own shares of stock.

Bloomberg this week did an excellent piece on that and the fact that this is the PRIMARY DRIVER OF HIGH STOCK PRICES.

http://www.businessinsider.com/stock-buybacks-are-in-a-bull-market-2015-3

CNBC reviewed the situation with corporate debt last March 2014 when it was $13.6 trillion:

Corporate debt fever rises to new record in 2014 Corporate America’s love affair with debt has intensified in 2014, with record levels of borrowing happening as feared rate increases have yet to materialize.

In total, corporate debt among non-financial companies has ballooned to $13.6 trillion, increasing 7.1 percent in the fourth quarter, according to the latest Fed data.

Companies have put all that debt—which has increased from about $11 trillion during the darkest days of the financial crisis in late 2008—to a number of uses.

The most noted from the investor perspective has been the trillion dollars or so that have gone to boost share prices through buybacks.

http://www.cnbc.com/id/101481029

You must be even MORE STUPID than you are foul mouthed, dude. What an utter IGNORAMUS.

Adam Price

You are nothing but a willfully ignorant mouthpiece for a corrupt organization of bankers. Only a total douchebag with an IQ of 85 would believe the Federal Reserve does not impact stocks. I guess you’ve never heard of the Greenspan Put.

Who pays you to peddle this propaganda?

Your copy and paste bullshit with CAPITAL letters won’t fly on this site. Take it elsewhere you maroon.

Adam Priceless

Learn something you dumbass. Fed balance sheet & the S&P 500. Any correlation numnuts? Or just a coincidence?

Your total stupidity and utter ignorance are beyond utterly mind boggling, dude. How can anyone be so ignorant and utterly stupid?

Adam Nitwit

Dallas Fed President Richard Fischer direct quote:

“QE3 WAS A GIFT TO THE RICH”

Read it and weep you ignoramus. You must be some low level Fed lackey assigned to troll websites that reveal the truth about your beloved Federal Reserve doing the bidding of the criminal Wall Street banks.

“I would say [Fed policy] has been in some sense reverse Robin Hood.”

~Kevin Warsh, Stanford University and former Federal Reserve governor

“Maybe the Fed is delusional about the effects of its policy . . . in widening the gulf between rich and poor in this country.”

~William Cohan

“Part of the impact of these very, very low interest rates is that we’ve created this disparity. The wealthy are benefiting from government policy and the non-wealthy aren’t. We have a president who says we’ve got to fight this disparity, and we have a Fed who’s encouraging it everyday.”

~Sam Zell, former real estate mogul

“We have [made] a colossal muddle. . . having blundered in the control of a delicate machine we do not understand.”

~John Maynard Keynes

“Savers are figuratively on their hands and knees and rooting around in bushes and between sofa seats for loose change on which to sustain themselves.”

~James Grant, editor of Grant’s Interest Rate Observer

“We make ?money the old-fashioned way. We print it.”

~Art Rolnick, chief economist for the Minneapolis Fed

“But why do I care about some archaic money-market malarkey? Simple. Without collateral to fund repo, there is no repo; without repo, there is no leveraged positioning in financial markets; without leverage and the constant hypothecation there is nothing to maintain the stock market’s exuberance.”

~James Bullard, president of the St. Louis Fed, on the role of the repo markets in blowing bubbles

“Inflation expectations are dropping in the U.S., and that is something that a central bank cannot abide. . . . Without leverage and the constant hypothecation there is nothing to maintain the stock market’s exuberance. . . . I think you should quit numbering the QEs.”

~James Bullard, president of the St. Louis Fed

“This time is different . . . because the Federal Reserve’s zero-interest rate policy has starved investors of all sources of safe return, forcing them to accept risk at increasingly higher prices and progressively dismal long-term prospective returns.”

~John Hussman

“There is agreement in the Fed that QE is about the worst thing you can do. . . . These guys are painting themselves into a corner . . . with great, great negative possibilities. . . . The Fed wants to get out of the QE business because it has brought no success and a great deal of criticism.”

~Art Cashin

“I don’t really like the Fed very much . . . I wish the Fed were not manipulating the market the way it is.”

~Jeffrey E. Gundlach, Doubleline Capital

“A key flaw in US policy is the Fed’s linear thinking—believing that the shock therapy of QE could not only save the patient in the depths of crisis but also foster sustained recovery.”

~Stephen Roach, Yale University and former Morgan Stanley chief economist

“[Yellen] won’t raise rates to fight incipient bubbles. For all of our sakes, we really wish she would.”

~Seth Klarman, Baupost Group

“Where does their confidence come from?”

~Stan Druckenmiller, legendary hedge fund manager, on central bankers

“No one has ever seen anything like this . . . if you look at the details of what these central banks are doing, it’s all very experimental. . . . There is something fundamentally wrong.”

~William White, former chief economist of the Bank for International Settlements

“You will see a system primed for a rerun of 2008, perhaps even faster and more intense this time.”

~Paul Singer, Elliot Management

“We don’t understand fully how large-scale asset purchase programs work to ease financial market conditions.”

~Bill Dudley, president of the New York Fed

“There’s no argument—you have to worry about the excessive printing of money!”

~George Soros, Soros Fund Management

“Today’s levels of interest rates and stock prices offer a historically unacceptable level of risk relative to return unless the policy rate is kept low—now and in the future.”

~Bill Gross, manger at Janus and founder of Pimco

“What we have never had before, at least in my reading of financial history, is governmentally sponsored bull markets superimposed on a structure of low interest rates.”

~James Grant

The Federal Reserve is a fine and honorable and venerable institution that has guided America superbly through all of the financial turmoil of the past century and is now celebrating its joyous 100th Anniversary this year during which America has enjoyed unprecedented success and prosperity.

Without the Federal Reserve and its monetary policy and influence over the past 100 years, wouldn’t the US still be the irrelevant backwater banana republic that it was back in 1913 as opposed to the economic superpower of the world – by far – with the world’s reserve currency used in 85% of all global transactions and the wealthiest nation in the world with over $180 trillion in assets?

The Federal Reserve has an excellent web site which explains all of the operations, functions, and details about the Federal Reserve and the Federal Reserve Act and anyone wanting to learn more about the Federal Reserve can peruse all of that information including their fully audited and highly detailed independently audited annual financial reports as well as a wealth of other information and statistics at:

http://www.FederalReserve.gov

The U.S. Federal Reserve Bank – How it Works, and What it Does – Money, Dollars, & Currency

Your “Burning Platform” is certainly burning up as the price of junk commodities such as gold and silver collapses into the abyss and the US dollar soars upwards towards over 100 and then up to as high as 164 or even higher dead ahead, dude. Your BS propaganda won’t fly at all and is being totally rubbished with the realities of the markets. Commodities are now at 13 year lows on the Bloomberg commodities index and will continue plummeting while the US dollar continues soaring. This kind of utterly idiotic and stupid propaganda that you and utter fools put out is beyond absurd and extremely stupid and totally bogus. What is wrong with people like you, dude? Are you really so clueless and utterly brainless? How can anyone be so extremely stupid?

“The Federal Reserve is a fine and honorable and venerable institution …” —- Adam Priceless

Funniest shit I’ve read in weeks. Thanks for the morning laugh.

Adam Price. Paid Government Troll. One and the same. Avoid them like the plague.

“Commodities are now at 13 year lows on the Bloomberg commodities index and will continue plummeting while the US dollar continues soaring. This kind of utterly idiotic and stupid propaganda that you and utter fools put out is beyond absurd and extremely stupid and totally bogus. What is wrong with people like you, dude? Are you really so clueless and utterly brainless? How can anyone be so extremely stupid?”

I am always open to being educated by my betters and if I am “clueless and utterly brainless” than Adam Price should be able to clear things up for me.

What if I am a producer of a commodity? How is it a benefit to earn less for something I must work as hard at to produce as when it was worth more?

I will await your response.

Jeebuz, we should introduce Adam “the Dumb Ass” Price to Robert Finnegan.

That reminds me, I need to go offer him some encouragement……..

Holy Shit.

Admin is goin’ fucken CRA-A-A-AZY!

“The Federal Reserve simply created money to PURCHASE EXISTING US TREASURIES with 100% of those funds GOING TO THE BANKS AND THEN INTO THEIR EXCESS RESERVES ACCOUNTS INSIDE THE FEDERAL RESERVE and with NONE (ZERO) OF THAT MONEY GOING TO THE US TREASURY.”

Please square with the passage below-

For the quantitative easing policy, the Federal Reserve holdings of U.S. Treasuries increased from $750 billion in 2007 to over $1.7 trillion as of end-March 2013.[23] On September 13, 2012, in an 11-to-1 vote, the Federal Reserve announced they were also buying $45 billion in long-term Treasuries each month on top of the $40 billion a month in mortgage-backed securities. The program is called QE3 because it is the Fed’s third try at quantitative easing.[24] The result is that an enormous proportion of the US debt is actually owed from the Treasury to the Federal Reserve, which according to a 1947 law, the Federal Reserve must return to Treasury annually after expenses.

Adam Priceless

Now pay attention son. I’m going to school you with some facts. I know your pea brain is filled with Fed propaganda and an unhealthy love of bankers, but be prepared for some learning. I know you are slow witted, so get a 3rd grader to explain it to you if it is too hard.

QE begins 12/1/08

Fed Balance sheet – $2.1 trillion

S&P 500 – 896

QE ends – 10/29/14

Fed balance sheet – $4.5 trillion

S&P 500 – 2,018

OK now I’m going to do some math. So pay attention.

Fed balance sheet went up 114% over this time frame, while the S&P 500 went up 125% over the exact same time frame.

Your bullshit is obliterated by the facts and by the quotes I’ve posted by Fed governors and some of the best investment minds on the planet.

Shockingly, since the Fed turned off the spigot the S&P 500 has sputtered to a return that is 75% below what it had been doing when the spigot was wide open.

You paid trolls are so transparent and easy to discredit. Try some other site bozo.

There is no growth in GDP, but there is huge growth of debt. The big banks that are not allowed to fail will wind up with all the marbles when they foreclose on all the real stuff they have financed with money they created out of nothing but air. The bail ins will take even more from large deposits of companies, retirement funds and the like. We have the most dumb down people on earth.

“don’t you think that our gov’t is complicit”

we couldn’t have gotten this far into this big of a decline without deliberate action and steering by those who can so act and so steer.

Guys guys guys….printing money isn’t inflation unless someone is spending it. So because Jim in Topeka Kansas isn’t getting that money to buy milk, its not inflation!

Wait, whats that? You say they are borrowing money at 0% interest but then loaning it for 3-20%? But those are just home/auto/school loans right? Not bread or milk?

Yeah not inflation.

/sc