Isn’t it interesting the mainstream media makes barely a peep about the ongoing and worsening Obamacare debacle. Healthcare premiums, co-pays and deductibles are soaring, while doctor and plan choices contract to a minuscule level. Recent surveys reveal the hardship being inflicted upon families across the nation. Those who are willfully baffled by the lack of consumer spending need look no further than Obamacare and its impact on the budgets of hard working Americans.

According to a survey by LIMRA, an insurance and financial services trade association, six in 10 workers agreed that the rising cost of health insurance directly affects how much they set aside in their workplace retirement savings plan. Employees are being forced to cut back on their retirement savings in order to meet the skyrocketing cost of their health insurance. Based on the numbers being bandied about by the Kaiser Family Foundation, it seems average families will soon have to decide between food and healthcare. Remember Obama’s quotes in 2008- 2009 when he was selling this bloated pig of a plan to you?

“We will start by reducing premiums by as much as $2,500 per family.”

“If you like the plan you have, you can keep it. If you like the doctor you have, you can keep your doctor, too. The only change you’ll see are falling costs as our reforms take hold.”

Millions of people have been kicked out of their existing health plans and have seen their premiums and deductibles go up by double digits. Small business owners are being forced out of business. And now the fines, mandates, and taxes really begin to kick in. At least median household real wages are lower than they were in 1989. According to the Kaiser Family Foundation:

Single and family average premiums for employer-sponsored health insurance rose 4% this year over last. The average annual premium for single coverage is $6,251, of which workers pay an average of $1,071; the average family premium is $17,545, of which workers pay an average of $4,955. Deductibles have risen more sharply than premiums. That’s the amount that consumers must pay out of pocket before insurance pays for anything, except for certain preventive services that are covered at 100%. The average deductible for workers with employer-sponsored health insurance who face a deductible is $1,318 for single coverage this year, up 44% from $917 in 2010. By contrast, over that same period, single premiums are up 24% and wages have risen 10%, just outpacing general inflation at 9%.

The brain dead proponents and cheerleaders for Obamacare reveal themselves to be nothing more than liberal control freaks who care not for the people they supposedly are helping with “free” healthcare. They need to falsify enrollment figures in order to prove how successful they’ve been in destroying the health system. They only care about press releases and winning the PR battle with the Republicans. It’s all about votes. It’s not about what is best for the uninsured. Families being forced into the limited number of Obamacare plans are seeing weekly costs of $300 to $400 for barely acceptable coverage.

The poor suckers forced into the Obamacare marketplace have to contend with health plan deductibles that are even higher than those with workplace-based coverage. The average 2016 deductible for a silver plan on the Obamacare exchanges is $3,117 for individual coverage, up 6% from 2015, while the average silver family deductible is $6,480, up 8% from this year, according to a recent analysis by HealthPocket, a technology company that ranks and compares health plans.

The entire reason Obama and his liberal minions forced Obamacare down the throats of a public that did not want it, was to provide insurance for the 30 million uninsured Americans. He failed, as there are still close to 30 million uninsured Americans, only they now get to pay a penalty to the IRS. It’s laughable for the MSM and brainless liberal twits to hail Obamacare as a huge success in covering the low income uninsured, when a poor family has to meet a $6,480 deductible before insurance pays a dime. How many poor families have $6,480 to spare? We know for a fact that more than half the households in the country don’t have $1,000 in savings, let alone the poor households. It’s a joke to say they have health coverage.

Obamacare is an unequivocal disaster that has resulted in less job growth, small business closures, worse care, less options for consumers, higher health insurance premiums for all, and soaring profits among mega-insurers, mega-hospital corporations, drug conglomerates, drug stores, drug wholesalers, and the political campaign coffers of corrupt bought off politicians. It’s the gift that keeps taking from hard working Americans.

@Sensetti,

Greetings,

True. Even a broken clock is right twice a day and the Republicans were right on the ACA. Still, I’m not a fan of faction politics and in no way do I support the two party system. In the end, there are not enough dump trucks in the world to haul away all the stupidity in D.C.

Even if the ACA is taken off of the books, the insurance companies are under no obligation to lower rates or make any changes. Only collapse and a clean slate will undo all of this damage.

AWD, Hope and myself, along with a few others burned this platform down railing against Obamacare before it was passed. How did we all know it was a disaster while O dumbass was touting how wonderful it would be. The difference? Reasonable Conservative minds at work vs Delusional Democratic minds at work.

Vote for Trump, shake the system!

@Westcoaster, the “program” wasn’t from the insurance company, I expect them to try to get as much info about me as they can to use against me. It is the company that I work for!

Sensetti said:

“Westcoater you’re a prime example of a fucked up democratic mind at work.”

Preach it brother Sensetti. Liberalism really is a mental disorder. However, Republipukes are right on their heels in lockstep. Even if both houses and the oval office go to Republipukes, nothing will improve. Book it!

Hope@ – interesting comments, and in reply to your question, the Aussie version of “Single Payer” is neither efficient, nor particularly “Patient friendly”, which is why we are “encouraged” to have Private Insurance (or be “fined” via our Medicare system).

Compared with the UK NHS, Australia is literally miles (light-years) behind, yet the “We are so exceptional” mindset is right up there on display. EACH State runs their “own” healthcare system – OK we have Medicare (Federal) but Hospitals are State funded, and inpatients are paid for by the State. Add in the fact that each State negotiates their own Pharmaceuticals / Consumables Contracts, and the duplication / bureaucracy is amazing (remember, these “bums on seats” get paid VERY big bucks). When most of the States have tiny populations (by any standard), commonsense would suggest FEDERAL negotiation might bring better prices, but no, the petty bureaucracies have to be seen to be “important” so we have what we have.

The UK NHS worked VERY well (though things went downhill post Thatcher – “Competition” simply meant opportunities for much more non-Clinical (but highly-paid) “Management” and “Financial Planning” positions, with all he attendant waste and pretty rampant cronyism) which is the main reason I left.. Australia could have exactly copied a good, cheap, and very efficient system, but I strongly suspect the “fingers in the pot” made sure we got the system “they” wanted, not the system the Patients want.

Chlorhexidine is a problem, and not just for resistance. I too have “Dishwashers Hands” and I had to request an exemption (from one of the NURSING “Management” – not ID / Clinical Services!!) to use plain alcohol. A LOT of our nursing staff have left owing to dermatological problems, sometimes very severe, and we see more instances of this problem every day.

Then, we see the respiratory consequences. Aerosolised chlorhex. is a known irritant (LOTS of refs via Medline), and so we have staff with underlying COPD becoming rather ill as a result of exposure to chlorhex aerosols. Only had a “few” severe problems (full-blown respiratory emergency scale) but those with a history of atopy must be at risk, and there is at least one ref. linking peanut allergy to development of (dermal) chlorhex. allergy.

Antibiotic resistance? We’ve been forced to adopt “Antibiotic Stewardship” where only ED may have unrestricted access to many agents. Other wards have to get Clinical “Approval” via a system which is not always that good. I no longer count the cases of “first dose in ED them subsequent doses missed – Waiting for Pharmacy Approval” – yet we’re told that this is the most effective way to create resistance- allowing concentrations to become sub-lethal for an extended period. Add in the carefully ignored but widespread use of similar agent classes as feedstock “Growth Promoters”, and the completely ignored final destination of 98% of ALL antibiotics – wastewater treatment (and the most biologically diverse microenvironment on the Planet), and you will understand my complete dis-interest in continuing the “Preserve the Miracle” charade, because charade is all it is.

We “want” all-new antibiotics. Yet, we refuse to use the “New” ones, ’cause they are the only ones that work. Far less profits for the Manufacturers, but the Patent’s ticking away, so far, far less incentive to develop anything, let alone anything “really” novel. Maybe if we stopped using the “old” off-patent stuff and ONLY used the new stuff, there just might be a financial incentive to develop, ’cause right now the only development I do see is in the blossoming of “Me Too” drugs for management of chronic, maybe “lifestyle” problems – Type II diabetes (ALL my chronic ulceration / incipient gangrene Patients are DM2 (along with COPD / IHD / dyslipidaemia), GORD (dozens of PPIs on the Market, all pretty much identical in performance), and IHD / dyslipidaemia – Statins everywhere.

Chronic disease “management” means lifelong revenue stream. Antibiotics either work, or they don’t. In MOST cases the courses are short, so the “return” is minimal by comparison. My few “long duration Tx.” Patients are only of long-term orals for maybe months, and I have only TEN Patients on lifelong orals (and their oral abx’s are all well off-patent!)

So, there you are. “Lots of Talk”, but almost no “Do”. And, don’t rock the boat, ’cause there are plenty with the right “connections” and mindset to give you the shove – as you well know, behind the “Professional” façade, it’s pretty much dog-eat-dog, especially as you progress up the food chain!! 🙂

Hey, I live in Canada, and we have free medical care. You go to a hospital…its paid, however if you have prescriptions or need glasses hopefully your employer, like mine, offers Blue Cross, which pays for prescriptions, glasses, massage, physio, etc. Our free healthcare is a result of a 10% sales tax on whatever you buy. And everyone is covered for Drs and hospital visits and operations, babies, etc. I try to understand Obamacare but I just don’t seem to understand it. I know nobody likes another tax, and 10% can be a lot on big ticket purchases, but it seems to be better than a 6000$ deductible. So if you spent all of your 60000$ income, you’d pay 6000 in tax, the same amount and sometimes less than some of your deductibles. It just seems to me, and only my opinion, if you had a similar system, even the poor people would be paying the tax on their expenditures to help their needs and the extremely wealthy would be paying more sales tax obviously, and the rest fall in the middle, but it would save what some of you have companied about 20 and 30 % increases per year, where 10% stays stable. I just wish I knew more about your system because at the beginning it seemed like OBCARE was the cats ass. Anyway. Be well with deductibles like that.

IS

Trump “might be” a game changer! He doesn’t need money to run and he’s not worried about money to retire on. Trumps a wild card no doubt,GOP establishment fears him because they can’t control him. Trumps may not change anything, but he might, he’s a business man that does know how to lose. I hope he gets the chance to change our downward trajectory.

Sensetti said:

“Trumps a wild card no doubt,GOP establishment fears him because they can’t control him.”

Trump might be allowed to be president if he toes the line. They can and will control him if he does not or he’ll go the way of other assassinated presidents. He might go down in history as the first assassinated presidential candidate. Our owners don’t fuck around. Just ask Jackson, Lincoln, Garfield and Kennedy.

Before long he’ll be getting the “Ross Perot” talk and after that we’ll see if he has intestinal fortitude to be the next criminal in chief.

Sensetti- You may be needed for round two of ( Stucky ass-whooping) in the Dalton Trumbo thread.

Bea

I grow weary beating on Stuckys hard head. His decades long addiction to pornography and self pleasuring has polluted all his neural pathways, he’s a lost cause. But I will take a look at his mindless drivel.

Negrocare. Overpriced and soon you won’t be able to find a doctor.

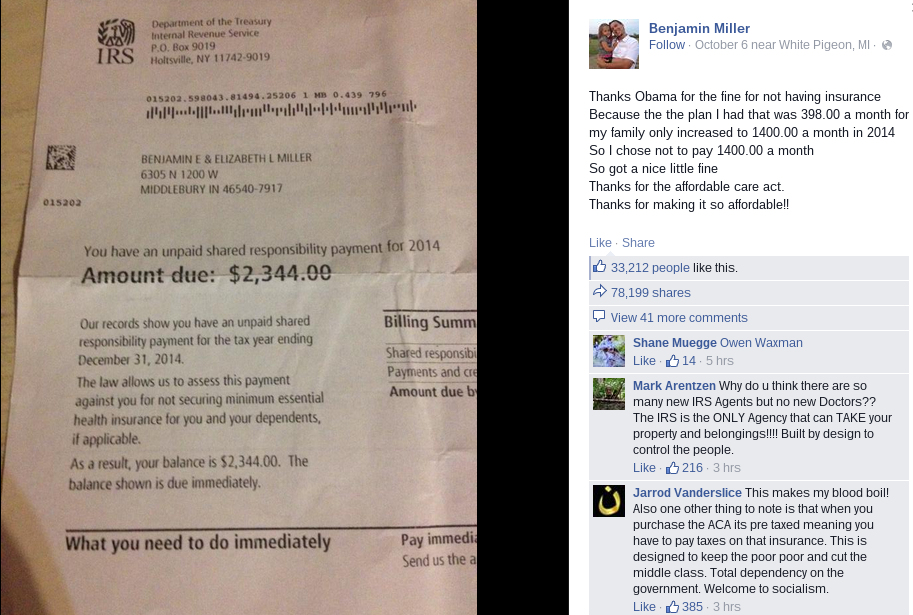

I just received my notice that my Obamacare Premium effective 01/01/2016 will increase from $591.63 to $802.43 a 35.63% increase! I have noted that the quality of care has declined significantly in recent years and understandably so, as what the Dr.’s are being paid are ridiculously low, so if you see a specialist with a problem that is serious its 15 minutes and visit over.

Numbers don’t lie but people sure do. The Affordable Care Act actually refers to two separate pieces of legislation — the Patient Protection and Affordable Care Act (P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010 (P.L. 111-152). Orwellian isn’t it? Affordable means unaffordable, Patient Protection means unprotected. These premium inceaes wil continue to kill the “consumer driven economy” which is a joke as Production and creation of “real” wealth and increased productivity is what drives consumption. The butt wipes in DC have the Caboose pulling the train and yet they expect a good result????? Keynesian nut jobs leading us all off a cliff to the pit of hell!

There is a way to beat Odumbocare…carry no health insurance, pay cash for care…and when you really need it, get a Platinum Plan that covers the best care you want. The penalty is easily waived for many reasons (they want you waived) and you can jump into a plan anytime…(they want you in).

When you are back in good health…dump the insurance.

It is FREE INSURANCE FOR WHEN YOU NEED IT.

Sensetti says: NOT ONE Republican voted for Obamacare. This is a shinning example of why Democratic controlled cities and State’s are bankrupt basket cases, Democrats cannot manage anything. One of these days we’ll hunt democrats with dogs, got keep Ole Red in good shape and keep oil in the lantern.

————————

Sure Sensetti…and NO Republican was able to get it overturned when they got control of Congress in the 2014 elections.

http://www.nytimes.com/2014/11/06/us/politics/victory-assured-gop-to-act-fast-in-promoting-agenda-in-congress.html?_r=0

Bwahahaha! Native Americans are exempt from Obamacare! Bwahaha!

Tough titty to you palefaces.

“$19,000 Premiums, Up 4x Since Passage”: The ‘Crippling Effect’ Of Obamacare On The Middle Class

Submitted by Tyler Durden on 11/07/2015 18:43 -0500

The past month has seen a veritable litany of reports that have slammed Obamacare, from sources on both the left and the right. Some examples:

In Latest Obamacare Fiasco, Most Low-Income Workers Can’t Afford “Affordable Care Act”

The Stunning “Explanation” An Insurance Company Just Used To Boost Health Premiums By 60%

Your Health Insurance Premiums Are About To Go Through The Roof -The Stunning Reason Why

Obama Promised Healthcare Premiums Would Fall $2,500 Per Family; They Have Climbed $4,865

Largest Health Insurer On Colorado Exchange Abruptly Collapses

Co-Op Insurers Across America Are Collapsing, And Now There Is Fraud

As we have warned over the years, all of this was expected, and is precisely what happens when the government tries to take over a critical industry. It may have had “good intentions” but the result has been a total failure.

And nowhere is it seen better than from the laments of those whom it was supposed to benefit, such as Ed Elliott, who has laid out precisely what the “Affordable Care Act” means for the US: “This is crippling effect of ACA on small biz owners & middle class. $19000/yr premiums up 4x since passage.”

This is crippling effect of ACA on small biz owners & middle class. $19000/yr premiums up 4x since passage. #tyranny pic.twitter.com/irHW4Oms2m

— Ed Elliott (@gunsntoolz) October 30, 2015

Still curious why the US middle class is expiring (even as the 1% are thriving), and has no discretionary income left at all? Simple: all of said “discretionary income” was spent to cover a soaring tax which was supposed to make life better for everyone.

Obamacare Premiums Up 20%—-3X More Than Claimed By White House

by Forbes • November 6, 2015

By John C. Goodman at Forbes

The Obama administration claims that the premium increases in the (Obamacare) health insurance exchanges are averaging 7.5% across the country. That figure, however, turns out to be wrong. An analysis by the Daily Caller News Foundation says that the real increase is 20.3% – almost three times as high.

Why the difference? The administration looked only at the prices of Silver plans, ignoring the prices for Bronze, Gold and Platinum alternatives. The Daily Caller, by contrast, looked at all four metallic levels. Furthermore, Richard Pollock explains that:

The 20.3 percent figure is the average for all plans. Premium increases in some states will be much higher. In Utah, for example, some enrollees in an individual plan will face a 45 percent price jump. In Illinois, the highest price hikes for individuals in the federal exchange will be 42.4 percent. Some insurers in Tennessee will experience a 36.3 percent price rise.

The Obama administration says that people will be able to avoid high premium increases in many cases by switching plans and it is encouraging enrollees to shop and compare premiums during the current open enrollment period. However, a Morning Consult poll finds that almost half (47%) of respondents plan to sign up for the same health plan they already have. Only one-third say they plan to shop for a new plan.

There are good reasons for the reluctance to change plans. The most important is the potential lack of continuity of care. Once people find doctors they trust they are reluctant to switch to a new set of doctors – providers they have never met.

Another reason is concern over privacy. Writing at the Morning Consult, John Reid notes that:

Americans are also less confident that their private information is secure on the Obamacare exchanges. In a September 2014 poll, 43 percent of respondents said they thought their private information was safe on HealthCare.gov or a state Obamacare exchange. This year’s poll put that percentage down to 34 percent.

The shift in secure health web sites comes amid high-profile cyber attacks on health plans across the country. In one such attack, hackers were able to steal the Social Security numbers of 10.5 million customers covered by the New York health plan Excellus BlueCross BlueShield.

But even if people remain in the plan they have, the plan itself may change. Writing in the Washington Times on Sunday, Sen. John Barrasso (R-WY) explains that:

In some states, plans are changing dramatically even if the company remains. A patient may find that her longtime doctor will no longer be a part of her plan’s network. Maybe the hospital nearest to her home is no longer included by her insurance. These kinds of changes can leave people with very different coverage than they had before.

As people work their way around the website, they may notice that the remaining options are slimmer than ever. Analysts at the Robert Wood Johnson Foundation say that more of the choices will be HMOs this time around. That can mean narrower networks and no out-of-network coverage.

Meanwhile, a significant number of enrollees have dropped their coverage, in part because of the higher premiums they are already being forced to pay and the narrowing choices of providers. For example, between January and September of this year, 1.8 million people (more than 10%!) allowed their coverage to lapse by not paying their premiums.

And although the Obama administration has stressed that the Obamacare model is based on the idea of competition, most of the insurers lost money last year and many of them are leaving the market. Robert Pear and Amy Goodnough wrote last Saturday in The New York Times:

[A]n administration report said Friday, only one insurer is offering coverage in the marketplace in Wyoming, and consumers have a choice of just two insurers in Alaska, Hawaii, Oklahoma, South Dakota and West Virginia. And that data, current as of Oct. 19, did not reflect the recent collapse of nonprofit insurance cooperatives in South Carolina and Utah.

The Obama administration is now predicting a leveling off of enrollment and more than one observer is asking whether we are headed toward a death spiral in some or all of the exchanges.

When Collapse Is Cheaper and More Effective Than Reform: http://charleshughsmith.blogspot.com/2015/11/when-collapse-is-cheaper-and-more.html?m=1

[img [/img]

[/img]

You are only beginning to see the pitfalls of this ” Affordable Care ” system, trust me.

Like it or not, Single Payer is coming, that dreaded government controlled health care system. How the average US citizen thinks that our profit based system in contrast to the Government Sponsored systems of every other developed nation in the world is better is a complete mystery to me. The facts are there – we pay more for less – no where even close to the top of the list as far as health care access and services on a worldwide basis. And this fantasy of ‘how it used to be’ is just that. It wasn’t working before – that’s why we got Obamacare – and it’s not working now. We are trying to support these unnecessary insurance companies who contribute nothing but take much. I guarantee they are far worse than any government sponsored system, systemic parasites we can no longer afford, the true leeches. It’s coming, like it or not.

Readers may find the following discussions on the matter of health care and insurance of interest:

http://tomwoods.com/podcast/ep-516-listen-to-this-episode-your-life-may-depend-on-it-how-to-secede-from-a-perverse-medical-system/

http://tomwoods.com/podcast/ep-481-how-capitalism-can-fix-health-care/

the ad hominem attacks on the proponents of ACA plan make it impossible for me to share with anyone who may have a desire to learn more, including the skeptical. you’re merely preaching to the choir here…