Guest Post by Eric Peters

One of the reasons – probably the main reason – people buy a new car is because their old car has gotten to the point that it is costing them too much to keep. Repair bills vs. monthly car payment bills. You reach that tipping point in a vehicle’s life when it makes more sense to spend money on a new car than to keep on spending money on the old car.

But what happens when that dynamic reverses?

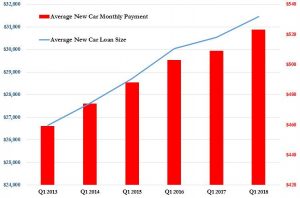

The average monthly new car payment is currently an almost unbelievable $525, according to Experian – the credit reporting agency. And the average new car loan is now six years (72 months) long.

Four months of payments out of those 72 months is more than $2,000.

Six months of those payments is $3,150.

That’s a whole lot of regular paying.

As expensive as car repairs often are, $3,150 pays for a lot of fixing. A year’s worth of $525-per-month new car payments pays for fixing almost anything that could possibly go wrong with a car.

It might be worth not making those payments.

Think about it. How likely is it that something big ticket will go wrong with whatever you’re driving that will cost you not just $525 once but every month – for the next six years?

And if the car is paid for and nothing goes wrong this month or next month, you just banked what you would have had to spend on a new car payment. On a car that is losing value in exactly the same way that the Titanic lost buoyancy after it kissed the iceberg. Which has created a problem almost as serious as the one faced by the passengers on the ill-starred liner that cold April night. Like them, you are likely to find yourself under water . . . owing more in payments yet-to-make than the car is currently worth. This problem has become so common – and so bad – that some new car loans even include what is called “gap” coverage, an extra charge added to your tab to make up for the loss of the car’s value (depreciation) which someone (you) has to pay for in the event it is totaled in an accident.

You won’t die, but the lender is making a killing on you.

The paid-for car, on the other hand, has already probably lost most of its value – which is a good thing in the same way that it would have been a good thing if Titanic’s water-tight doors had gone all the way up to the boat deck. If you have to spend say $800 on brake work, at least you didn’t also just lose $800 in book value.

And if you live in a state or county that applies a personal property tax to motor vehicles – which tax is based on the retail value of the motor vehicle – you may save the equivalent of several $525/monthly car payments each year just by not buying a new car. The property tax is obnoxious in principle – you’ve already been income-taxed at least twice (federal and state) and now the cretins are going to tax you again on the value of whatever “personal property” you managed to acquire with the remainder?

But the hit you take on a new car is particularly punishing – given how much new cars cost. The property tax hit on a $35,000 car – the average price paid for a new car – can be $1,000 or more annually, for several years – until the car has lost enough value to ease up on this third-tier form of extortion.

Looked at another way, the money you didn’t spend on taxes can be put aside to pay for repairs. And if the repairs aren’t necessary – or cost less than the money you would have had to pay in taxes – then you come out ahead.

Insurance costs should be taken into account as well. These are going up – regardless of your driving record – because of the cost to fix new cars. A busted headlight assembly can cost as much as a new car payment; a deer strike can result in body damage equivalent to a year’s worth of $525 monthly payments. These costs are not only reflected in the insurance premiums you pay to cover a new car, you have to pay them.

Unless the car’s paid-for, which is a tough trick for most people – who haven’t got the scratch in the bank to cut a check for $35,000 or even $15,000. So they are obliged to carry full coverage (replacement coverage) on the car – reasonable, since otherwise the lender would be the one left holding the wet-bottomed bag.

But if it’s a paid-for older car, you can (wisely) skip the full coverage; which is wise because unless the car is less than five years old,if you ever do get into anything worse than a fender-bender accident, it is very likely the insurer will total the car and cut you a check for the much-depreciated value of the car. You’d have saved money by putting the money you spent on the full coverage in a mason jar. Because you’d at least still have the money.

And the difference in cost to fully cover a new car vs. the cost to minimally insure a paid-for car can amount to several $525 monthly payments you didn’t have to pay, too.

The final argument in favor of fixing vs. buying is that buying anything new amounts to a guarantee you will either be spending much more than $525 to fix things when they fail – because of the lunatic overcomplexity of almost every new car on the market (and, arguably, almost every new car built since the early-mid 2000s) or you will be buying an even more expensive new car when the one you just bought begins to fail.

Nice bumpers.

The car’s OK too…

Yeah I’d drive a beater with bumpers like that..

Any time, any place..

After I paid off my truck 6 and a half years ago the dealer was working me to buy another. I decided not to and instead put money I would have laid out in RRSP (401k).

Since then those payments have been squirreled away. Now the 20 Grand or so saved makes cash instead of costing money… Yeah lots of folks make fun of my Ranger. It is old now. Has spots where the paint came covered with Tremclad that doesn’t match but I dont care. Job now is to keep the rust bugs away. Sure ain’t big and flashy like a new F150. Yet it still it gets me to work and back. And at the end of the day that is all that matters…

+100

And that’s the way you do it. Nick and I have purchased exactly ONE brand new vehicle in our marriage. The Hyundai Tucson was brand new off the lot, with less than 100 miles on it. They discounted it $5K because it was a five-speed. I didn’t care. I’d grown up driving a tractor and, on a hard summer’s day, had even managed to get that 1958 John Deere Combine from the field to the equipment shed when a sudden summer storm arose and Dad had asked me to watch for it, but had hoped I wouldn’t have to move the thing. I did and it was one of those rear wheel drive monsters which required the driver to turn the opposite way to turn the combine from the back wheels.

Giving me 5 grand to drive a manual transmission seemed like a pretty darn good reward for loving to pop clutches and get the little bit of burn.

We drove second purchase cars and pocketed the rest. Am pretty happy about that right now.

1992 bought new runs just like new ….afrer a new water pump and radiarer at 80K.

Newest car in my fleet is a 2005. Last time I purchased a new car off the show room floor was in 2001.

Love that new car smell but hate those new car payments and add ons. Last vehicle I paid the property tax for to get the State tag on it was a whopping $30. Sweet. I like to keep a car 6 or 7 years minimum

and I don’t drive rent-a-wrecks either. ” Take care of your equipment and it will take care of you.”

Last note: I only carry liability insurance on each vehicle. Yes, I am watching my middle class dreams slip away. Thank you, 1% for all your help.

I’m worried people are going to wise up and start bidding up the price of used cars. 2 years ago I bought a 2002 6 cylinder Camry with 25,000 miles on it for $2,400 that passed inspection. I bought a 2000 Dodge Intrepid 6 cylinder with 76,000 miles on it for $500 that passed inspection. My father just paid $5,400 for a 2006ish Ford Ranger 4×4 with 170,000 miles on it. The Ranger might seem a bit high except that the last Ranger he had is still going strong at 300,000 miles. He sold it for $2,000.

Wip,great deal on the toyota.This is why I build/maintain 70’s stuff,a breeze to work on and looks different then average trucks/van ext,plus,customize the way I want.Rust free examples can be found with a little work,just not interested in new cars/trucks unless given to me for free,even then,too much of a pain to work on.The lass with the Chevy reminds me of me and Lori owning the Trans Am together,good and bad memories there!

The price of 70’s stuff around here is absurd. C-10 daily driver for 15,000. In 2 wheel drive. Beat near dead el caminos for 5 and 6 grand. Insane. 60’s and solid trucks are going even higher. I would rather drive something older, but i need reliable transport that can tow, and i drive windy ass roads. New trucks drastically out handle older cars and trucks. A 32 ft ladder doesnt strap on an old camry.

Finger,agree you can pay a lot for mint 70’s stuff,but nice body4x4/rebuilt transmission/pumpkins ect. can be had for the 15000 range.Me,willing to do the mechanical the body work out of my skills,hence,needs motor/tranny or say just a bunch of smaller stuff can do and enjoy,have seen good el camino frames/bodies with need for motor transplant for 2-3 range,my point is still much cheaper and more dependable and ease to work on.I do get me stuff appraised for rebuild vale/market when done yet pay nothing in taxes.I realize a lot of folks not into that stuff but can with work find the good stuff very reasonable compared to new garbage.For older cars look at the retirement states,a lot of good deals there on low mileage stuff,albeit usually not trucks and vans1

The problem with paying for those major fixes that may occur occasionally, is that the repairs are only guaranteed for a limited period of time, like 30 days, where as a new car can come with a 5-10 years warranty.

I try to buy a 1 owner around 50k that’s maybe 3 or 4 years old, direct from the owner, not a dealer. Buy a carfax, it tells you a lot. I violated my own rule last time and bought from a dealer. But so far 2 1/2 years later, it’s been great and I paid about 1/2 the original cost. Got a $9k tax credit for my old ride too. I put 50k+ on that car and the tax credit was more than I paid for it 9 years later!

Haven’t purchased a new car since 2001 and probably will not buy new ever again . There are so many cars out there in the market low miles former fleet rentals or elders unloading that crown Vic with 30,000 Miles on it . Save my cash do some repairs because I was a natural with a wrench . I fix most things on my vehicles and have several good dependable repair shops you can trust so I drive them into the dirt

WARNING

Do not listen to Eric Dingleberry Peters when it comes to disabling the airbags in your used car!

Modern seatbelts are designed to stretch more than the seatbelts in pre-airbag cars and THEY ARE NOT DESIGNED TO ADEQUATELY RESTRAIN (PROTECT) YOU WITHOUT FUNCTIONING AIRBAGS.

Can you share your source for this information? Smells like bullshit.

It makes no sense. SRS stands for Supplemental Restraint System; as in “not the primary means of restraint”. If the airbag failed, you would want the seatbelt to function as normal.

Last time he brought that up i couldnt find anything to verify it. But seat belts are single use fwiw. Brought that up at the shop. Insurance wont pay for it unless they are shot deployed tighteners like on mercedes.

I’ve seen it stated in owners manuals as the rationale for getting your car serviced quickly when the SRS light comes on.

Airbags exist to lessen the injuries from seatbelts, not the other way around.

If seatbelts in airbag equipped cars didn’t stretch more, you wouldn’t come in contact with the airbag- and the airbag wouldn’t have a chance to do it’s job and spread the impact over a much greater area.

No, airbags do not exist to lessen the injuries from seatbelts. They are there mostly so your noggin won’t flail around or smack into stuff since the seatbelts only restrain your torso.

No, seatbelts don’t stretch to allow you to come into contact with the airbag; the airbag inflates momentarily to meet you.

I haven’t been able to find any mention of “more stretchy” seatbelts in any web search, nor can I find it in the owner’s manuals of either of my cars.

I’m all for buying used, but if you’re going to add a pussy magnet, make sure you get OEM.

Nope,rebuild the way I wanted them to come out of factory,will save stock stuff in garage ect. but I basically abhor factory original,want built up better motors/trams shifters/mags ect.

https://m.youtube.com/watch?v=mTdnm9xUNuE

The simple answer is to not finance your vehicles. Save up and buy something when you can afford it.

I’ve been critical of EP in the past. However the man hit it out of the park here. I recently had to pay $500.00 for an alternator and battery. It use to be something I could tackle myself but this 2005 Chevy grocery getter needs to practically have the whole body disassembled to get at the alternator. Plus it’s been hot as shit here in VA . The month before it was $600.00 for brakes. So I started the fantasy of getting that Dodge Charger or Mustang that I would love to have. Monthly payments. Uug. Then called my insurance guy. $ 1700.00 a year . Ouch. Then the God damned personal property shakedown of $1000.00 yearly. Add the depreciation and worries of every little ding and scratch on a new car and well I fell back in love with my little silver sedan. Buying a new car isn’t fucking worth it. My wife can have the new car. Peace.