Guest Post by Lance Roberts

My…my…how quickly we forget.

Yesterday, as the markets rocketed higher, my email lit up with questions surrounding the discussion from this last weekend’s newsletter.

“I have questioned over the last couple of weeks exactly how much volatility the Fed would allow before stepping into the fray to keep the markets stable.

We now know it is roughly a 10% decline.

Specifically were the comments about QE being ‘useful to have in the toolkit for those times when the short-term interest rate tool may not be available,’ adding that the Fed is ‘quite likely’ to require large-scale asset purchases again because real rates will remain low due to slow productivity and labor-force growth. They also added that ‘if LSAPs are indeed not effective, then the Fed may need to take other measures.’ (Zerohedge has the complete article.)

In other words, despite the rhetoric to the contrary, the Fed isn’t going away…….ever!”

The deluge of emails revolved around much of the same premise.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

“If the the Fed isn’t going away, then why would there ever be another bear market?”

It is certainly an interesting question, particularly as the Fed continues to trot out officials to make market supporting statements such as Fed Vice Chairman Quarles who stated on Monday:

“It might seem reasonable to assume that faster growth would lead to firmer inflation. However, I think a lot remains to be seen.”

Or even Mario Draghi, Chairman of the ECB, who said:

“In the presence of an economic situation that is improving constantly, we need the right blend of measures. Uncertainties continue to prevail.”

So, despite economies that are supposedly improving, Central Banks continue into their tenth year of “emergency measures.” As Michael Lebowitz recently stated:

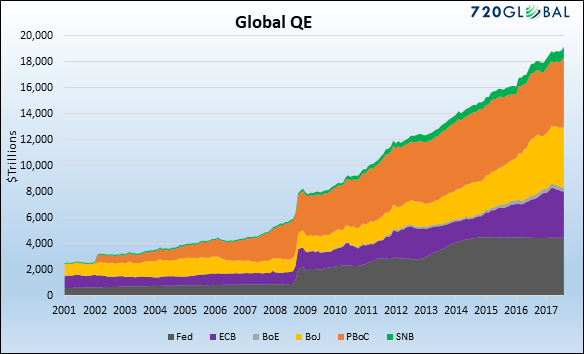

“Global central banks’ post-financial crisis monetary policies have collectively been more aggressive than anything witnessed in modern financial history. Over the last ten years, the six largest central banks have printed unprecedented amounts of money to purchase approximately $14 trillion of financial assets as shown below. Before the financial crisis of 2008, the only central bank printing money of any consequence was the Peoples Bank of China (PBoC).”

With that, I certainly understand the reasoning that if indeed “Central Banks” are now committed to monetary interventions going forward, the financial markets have been effectively “fire-proofed against bear markets.”

But such a belief is extremely dangerous.

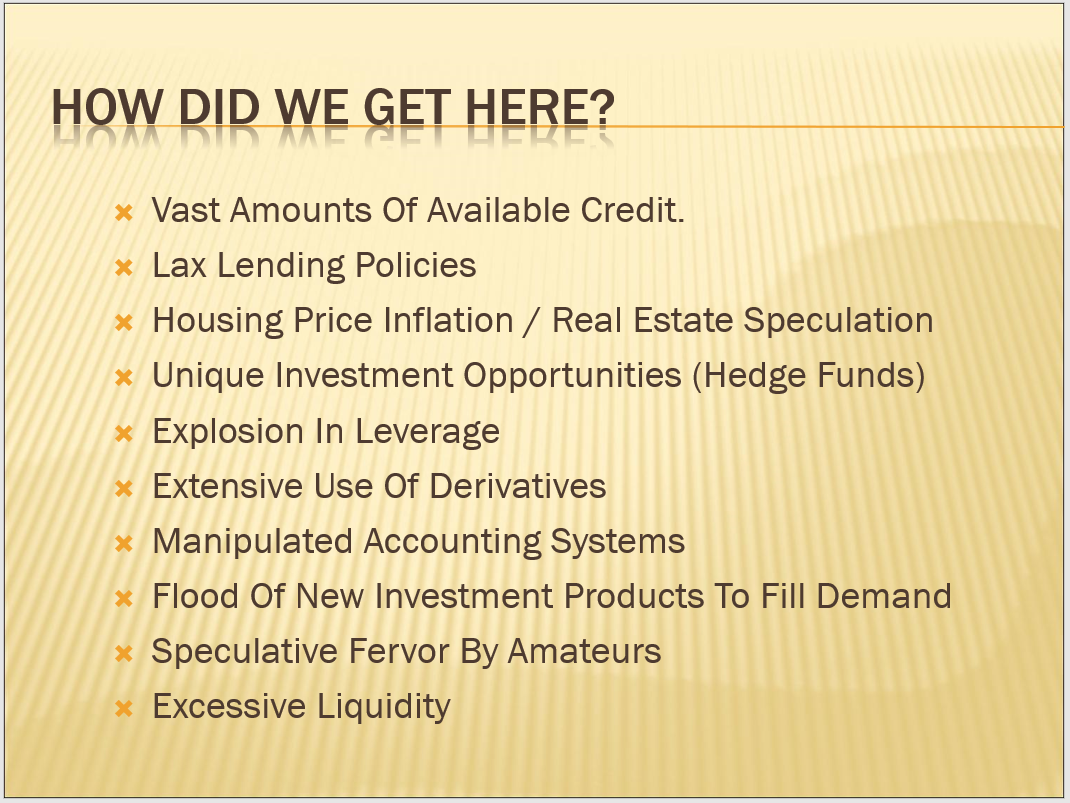

It is also the same “belief” every major bubble was built upon throughout history and driven by the same underlying foundations.

Which created the bubble in “THE” asset class of choice at that time…

Which created the bubble…

Which always ended badly for investors.

Every. Single. Time.

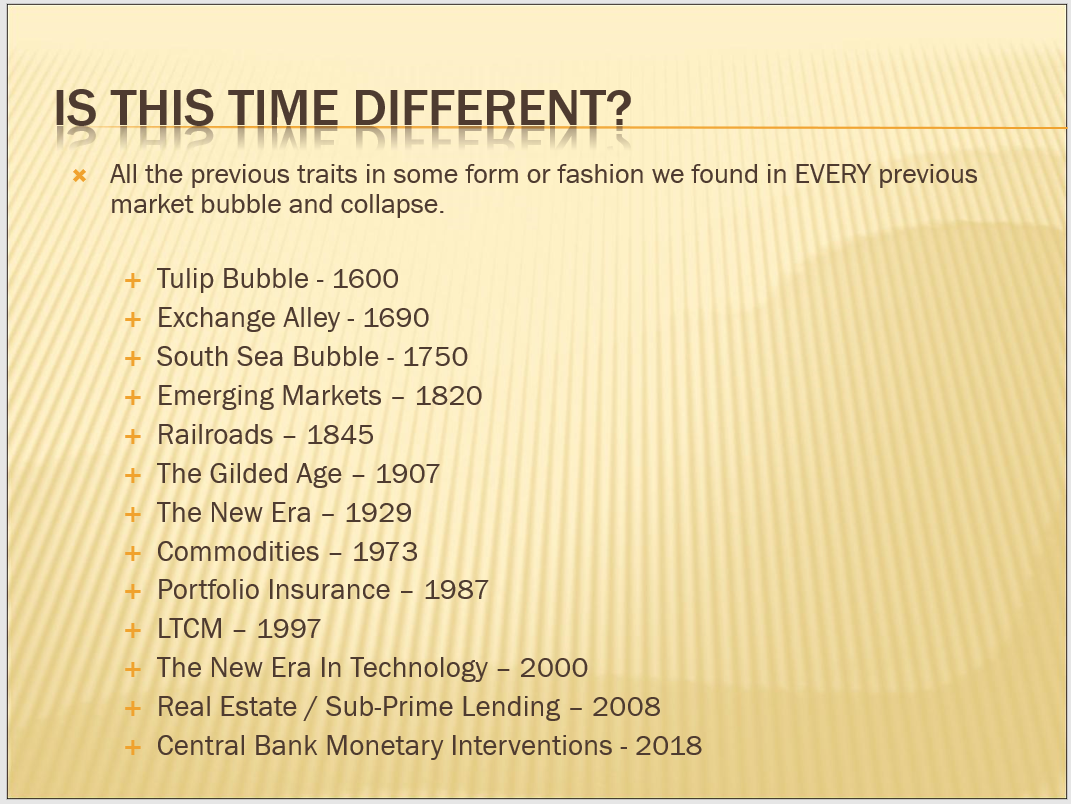

Is “this time different?”

No, and it will end just the same as every previous liquidity driven bubble throughout history.

Of this, there is absolute certainty.

There are only TWO questions that must be answered:

- What will cause it, and;

- When will it happen?

What Will Cause The Next Crash

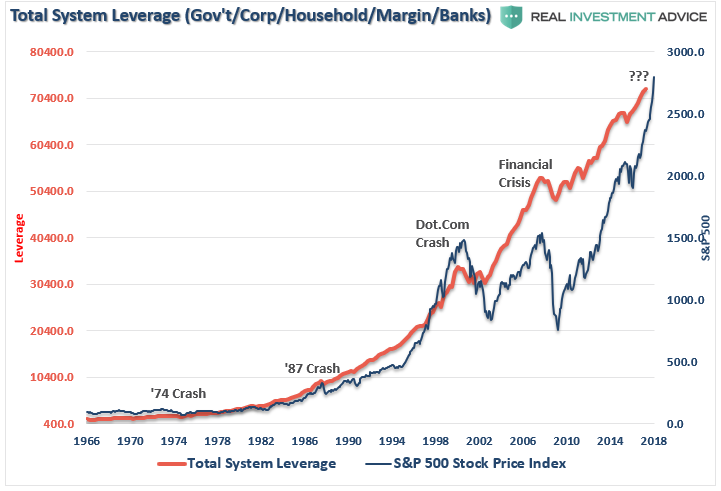

No one knows for certain what will cause the next financial crisis. However, in my opinion, the most likely culprit will be a credit-related event caused by the Fed’s misguided policy of hiking interest rates, and tightening monetary policy, when the financial system is more heavily levered than at any other point in human history.

The illusion of liquidity has a dangerous side effect. The process of the previous two debt-deleveraging cycles led to rather sharp market reversions as margin calls, and the subsequent unwinding of margin debt fueled a liquidation cycle in financial assets. The resultant loss of the “wealth effect” weighed on consumption pushing the economy into recession which then impacted corporate and household debt leading to defaults, write-offs, and bankruptcies.

With the push lower in interest rates, the assumed “riskiness” of piling on leverage was removed. However, while the cost of sustaining higher debt levels is lower, the consequences of excess leverage in the system remains the same.

You will notice in the chart above, that even relatively small deleveraging processes had significant negative impacts on the economy and the financial markets. With total system leverage spiking to levels never before witnessed in history, it is quite likely the next event that leads to a reversion in debt will be just as damaging to the financial and economic systems.

Since interest rates affect “payments,” increases in rates negatively impact consumption, housing, and investment which ultimately deters economic growth.

It will ultimately be the level of interest rates which triggers some “credit event” that starts the “next bear market”

It has happened every time in history.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will force investors to dump positions to meet margin calls at a time when the lack of buyers will create a vacuum causing rapid price declines.

When Will It Happen

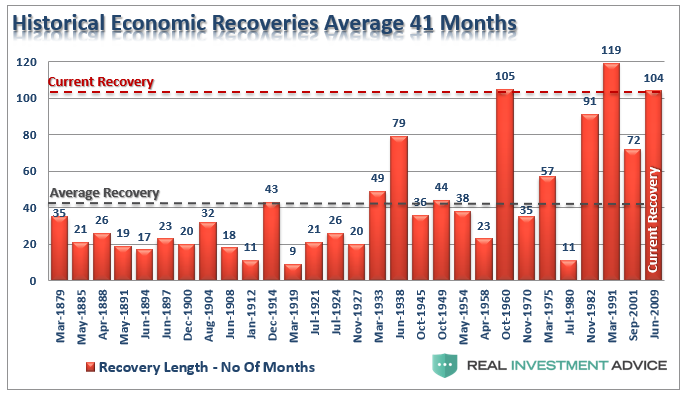

Honestly, no one knows for sure. However, history can give us some guide.

“In the past six decades, the average length of time from the first tightening to the end of the business cycle is 44 months; the median is 35 months; and the lag from the initial rate hike to the end of the bull equity market is 38 months for the average, 40 months for the media.” – David Rosenberg

Averages and medians are great for general analysis but obfuscate the variables of individual cycles. To be sure the last three business cycles (80’s, 90’s and 2000) were extremely long and supported by a massive shift in financial engineering and a credit leveraging cycle. The post-Depression recovery, and WWII, drove the long economic expansion in the 40’s, and the “space race” supported the 60’s.

Currently, employment, economic and wage growth remain weak with 1-in-4 Americans on Government subsidies and the majority living paycheck-to-paycheck. This is why Central Banks, globally, have continued aggressively monetizing debt in order to keep growth from stalling out. With the Fed now hiking rates, and reducing market liquidity, the risk of a policy mistake has risen markedly.

If David is correct, given the Fed began their current rate hiking campaign in December 2015, the next recession would occur 38-months later or February 2019. Such a span would make the current economic expansion the second longest in history based on the weakest economic growth rates.

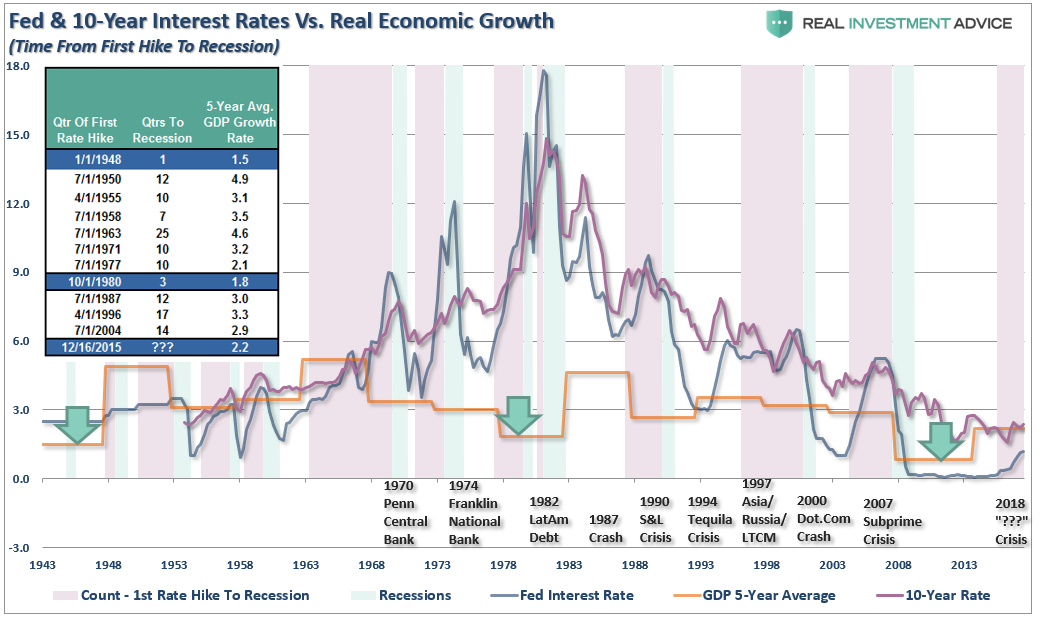

The chart and table below compares real, inflation-adjusted, GDP to Federal Reserve interest rate levels. The vertical purple bars denote the quarter of the first rate hike to the beginning of the next rate decrease, or onset of a recession.

If you look at the underlying data, which dates back to 1943, and calculate both the average and median for the entire span, you find:

- The average number of quarters from the first rate hike to the next recession is 11, or 33 months.

- The average 5-year real economic growth rate was 3.08%

- The median number of quarters from the first rate hike to the next recession is 10, or 30 months.

- The median 5-year real economic growth rate was 3.10%

The importance of this reflects the point made previously, the Federal Reserve lifts interest rates to slow economic growth and quell inflationary pressures. Yet, economic growth and inflation are running well below historical norms and system-wide leverage has surged to new records as individuals and corporations have feasted on debt in a low-rate environment.

That is now changing as the Fed hikes interest rates. Notice in the chart above, that recessions occur when the Fed starts hiking interest rates and the Fed rate approaches the 10-year Treasury rate. In every instance, a recession or “crisis” occurred.

Crisis, Recession & Bear Markets

If historical averages hold, and since major bear markets in equities coincide with recessions, then the current bull market in equities has about one year left to run. While the markets, due to momentum, may ignore the effect of “monetary tightening” in the short-term, the longer-term has been a different story.

As shown in the table below, the bulk of losses in markets are tied to economic recessions. However, there are also other events such as the Crash of 1987, the Asian Contagion, Long-Term Capital Management, and others that led to sharp corrections in the market as well.

The point is that in the short-term the economy, and the markets (due to momentum), can SEEM TO DEFY the laws of gravity as interest rates begin to rise. However, as rates continue to rise they ultimately act as a “brake” on economic activity.

While rising interest rates may not “initially” impact asset prices, it is a far different story to suggest that they won’t. In fact, there have been absolutely ZERO times in history that the Federal Reserve has begun an interest rate hiking campaign that has not eventually led to a negative outcome.

What the majority of analysts fail to address is the “full-cycle” effect from rate hikes. While equities may initially provide a haven from rising interest rates during the first half of the rate cycle, they have been a destructive place to be during the second-half.

It is clear from the analysis that “bad things” have tended to follow the Federal Reserve’s first interest rate increase. While the markets, and economy, may seem to perform okay during the initial phase of the rate hiking campaign, the eventual negative impact will push most individuals to “panic sell” near the next lows. Emotional mistakes are 50% of the cause as to why investors consistently underperform the markets over a 20-year cycle.

The exact “what” and “when” of the next “bear market” is unknown. It has always been some unanticipated event that triggers the “reversion to the mean.”

It will be obvious in “hindsight.”

While the media will loudly protest that “no one could have seen it coming,” there are plenty of clues if you only choose to look.

The Fed has not put an “end” to bear markets.

In fact, they have likely only succeeded in ensuring the next bear market will be larger than the last.

For now, the bullish trend is still in place and should be “consciously” honored. However, while it may seem that nothing can stop the markets rise, or seemingly the Fed will never let it fall, it is crucial to remember that it is “only like this, until it is like that.”

For those “asleep at the wheel,” there will be a heavy price to pay when the taillights turn red.

“It is clear from the analysis that “bad things” have tended to follow the Federal Reserve’s first interest rate increase. ”

That and all the other predictions in the article are based on knowledge and analysis of prior history.

This Time IS Different.

I said it, so it shall be.

The US and the World financial status has never, absolutely never, been this bankrupt; openly bankrupt without off balance sheet items.

Governments will not allow a major market downturn.

Period……Double Period.

There used to be GAP Accounting; now it is Unicorn Accounting.

Up, Up, and Away

EDIT: A Nuclear War will change the status quo.

Congress -even the President as Kennedy demonstrated- has the Constitutional authority to just have the Treasury issue as much money to pay off all debts and as much more as it needs to do what it wants to do.

They also have the authority to buy the Federal Reserve and make put under Congressional ownership or just dissolve it with the money they can issue as they choose.

Everyone just seems to think this option will be off the table if a real monetary crunch happens and Congress needs to deal with it, but it won’t.

I’m boiling mad.

Housing debt ………. in the trillions

Credit card debt …… in the trillions

Student loan debt …. in the trillions

Auto debt ………………. over a trillion

Maybe The Big Bad Bear arrives when enough people say “fuckit’ and default?

That’s essentially what happened back in 2008.

We recovered from it, with those that were both observant of the real world and smart as well making a great deal of money from it.

Same will happen next time, when it finally comes, as the cycles of boom and bust have existed forever and will continue to do so.

We didn’t recover from 08-09, we simply papered it over with a blizzard of borrowing and money printing…In the real world, most people are falling further and further behind.

Bingo. That IS what will take it down. Remember, most, if not all of these debts are in some way supported by your, mine, and your neighbors willingness to get up and produce. As long as we are good little worker bees, and keep on believing that all we have to do to be successful is keep working our butts off, keep paying our taxes on those earnings, keep buying crap we don’t need and keep using the credit card, mortgage etc. to finance it, this will continue. Once a large enough proportion of the tax donkeys, worker drones, sportball sheep, and various other useful idiots wake up and decide it is not worth it to them anymore, or they simply cannot produce enough to maintain the minimum payments; that is when the trouble starts. Considering the numbers involved this go around, it will happen quickly as well. Think of a large star going supernova once gravity wins over the pressure of the nuclear reaction….I doubt the government “stimulus” will be able to work fast enough once the trouble starts. The math is just too big.

End of Bear Markets! Yeah riiiiiiiiiiight.

In the final end of the game – show me the color of your money…….

Is it green or is it gold?

When Will It Happen

“Honestly, no one knows for sure. However, history can give us some guide.”

I have a lot of respect for Lance Roberts and his analyses. But the statement above is not true. The private owners of the Federal Reserve created this boom market and they know exactly when the plug will be pulled to create a bust. That is what they have been doing before 1913 when the unconstitutional Fed was created while enriching themselves at our expense. How could you lose when you control the equity, bond and real estate markets. And it doesn’t stop there. The American people inherit the debt and pay the interest on trillions of dollars created out of thin air by the Federal Reserve, and pay again with the debasement of the US dollar and the accompanying loss of purchasing power. In the core of America’s financial and monetary system is a diabolical system of massive plunder called central and fractional-reserve banking. And who benefits from all the debt and market manipulation? Read below.

Dean Henderson, in his article The Federal Reserve Cartel, clearly explained and confirmed the private ownership of the Federal Reserve:

“J. W. McCallister, an oil industry insider with House of Saud connections, wrote in The Grim Reaper that information he acquired from Saudi bankers cited 80% ownership of the New York Federal Reserve Bank – by far the most powerful Fed branch – by just eight families, four of which reside in the US. They are,

• the Goldman Sachs, Rockefellers, Lehmans and Kuhn Loebs of New York

• the Rothschilds of Paris and London

• the Warburgs of Hamburg

• the Lazards of Paris

• the Israel Moses Seifs of Rome

“CPA Thomas D. Schauf corroborates McCallister’s claims, adding that ten banks control all twelve Federal Reserve Bank branches. He names,

• N.M. Rothschild of London

• Rothschild Bank of Berlin

• Warburg Bank of Hamburg

• Warburg Bank of Amsterdam

• Lehman Brothers of New York

• Lazard Brothers of Paris

• Kuhn Loeb Bank of New York

• Israel Moses Seif Bank of Italy

• Goldman Sachs of New York

• JP Morgan Chase Bank of New York

The down vote must be Greenspan or Bernanke or Yellen, all Ashkenazi or Kazarian Jews who answer to the Rothschild mafia family. Wake up America, you are being controlled and plundered! Keep in mind that all war are bankers’ war, or stated another way “Jewish Wars”.

Keep this in mind: someone who says bankers’ wars synonym jewish wars has too little, maybe none, mind to keep anything in. Such reductio ad is beyond absurdum.

War has been a constant throughout humanimal history, prehistory. Reductio minds have a lot to do with that.

The end of bare markets, which may have never happened – as markets may never have been bare but in theory – guarantees Kodiak size bruins & attendant ruins. Bipolar bears feature prominently, too.

Ya’ know that weird thing that happens to some island creatures…bears on Kodiak archipelago, tortoises on Galapagos archipelago, arch criminal banksters on Jekyll island.

Some huckster’s always importing – the rubes love it – specimens from Kong island, Jurassic Park, to the Lilliputian lands. And then Gulliver fe-fi-fo-fums ‘em. And the stockholm’d, codependent, lilli’s lie about it.

The Fed might step in to halt a 10% decline, but that doesnt mean they wont allow subsequent 10% declines. Beware the next 10 days especially.

Get your head out of your ass and stop looking at statistics. Look at your neighborhoods, the # of business going out, the number of pan handlers on the streets, the potholes and damage from the terrible storms, etc. All are not on a chart or graph. America is a pile of shit headed to the bottom of the sea!