Guest Post by John Mauldin

I have long said I don’t want to retire. I enjoy my work. It’s not too physical, other than the travel (which is finally beginning to wear on me). Also, my savings are not yet sufficient to sustain the retirement lifestyle Shane and I want. I could retire now but would rather wait.

Fortunately, I have the choice of continuing to work and adding to those savings. I realize many Americans don’t have that luxury. Some have to retire because of illness, or because their work requires more physical ability than their age allows. Many others don’t retire because they just can’t afford to.

TV commercials suggest a financial advisor is key to a leisurely retirement. A good one certainly can help, but only to the extent you’ve saved enough cash to give them something to invest. And as we’ll see, many Americans haven’t.

My readers tend to be conscious of these things. You probably have above-average income and savings. Maybe your retirement plan is on track, but that doesn’t mean you can rest easy. We all exist within a society and an economy. Its problems are ours, too, as we may find out when taxes rise to help pay for others to retire.

Today, we’ll look at the state of retirement in America, updating some data I shared a couple of years ago. Then we will look at some strategies to keep your plan realistic and on track.

Social Security Is Not Enough

How much money will you need to retire, and how much will you have? Answering those questions is one reason a good financial advisor is worth every penny you pay them. But let’s talk about some generalities.

Say you want to stop working at 65. You’re in good health and your family tends toward long lives. You expect to reach 90, having been retired for 25 years. Will Social Security alone be enough?

If you spent most of your life paying as much as legally possible into the system, and you retire in 2019 at age 65, your monthly benefit will be $2,757, which is then indexed for inflation (at least under current law). It jumps to $3,770 if you delay retirement until age 70.

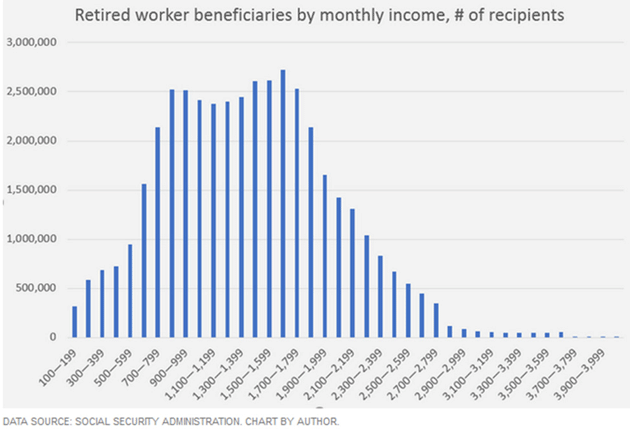

Since I am not yet 70 for another eight months, I really haven’t paid much attention to what I will get when I start my Social Security. I assumed like the charts that I’ve seen below that it would be a couple of thousand a month. I was surprised to learn I may get significantly more. Considering how much I’ve contributed over 50+ working years, it’s probably not that great a return. Yet most people get less. Here’s the distribution.

A solid majority of Social Security recipients receive $2,000 a month or less, and many less than $1,000. The average benefit is $1,413, according to Social Security’s latest fact sheet. If that’s all you have, your retirement lifestyle is not going to include many cruises and golf tournaments.

Of course, it shouldn’t be all you have. Social Security was never supposed to be a complete multi-decade retirement plan. It was designed to keep retired workers out of poverty at a time when lower life expectancies kept retirement much shorter for most—if they lived to 65 at all. Now we live longer, and we have higher expectations, which political leaders have done little to dampen. Often they’ve done the opposite.

Bottom line: Social Security probably won’t give you much security. You need more.

Is That All There Is?

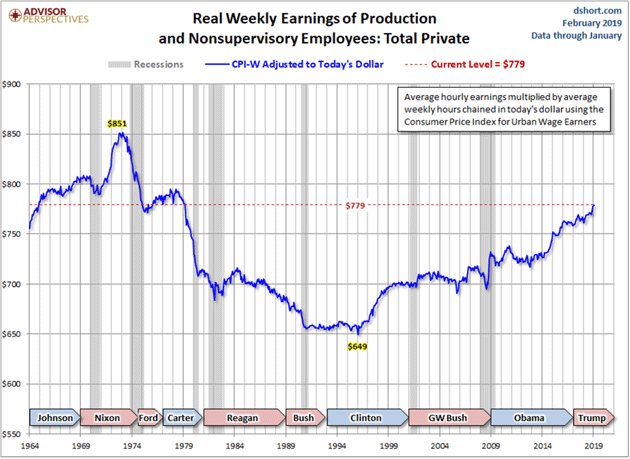

Ideally, people should avoid relying on Social Security and accumulate other savings as well. Many, perhaps most, do not. The reasons vary. I suppose some just spend their money unwisely and neglect to save anything. But income data says many Americans can’t afford to both live a typical middle-class lifestyle and save enough to finance a 20+ year retirement. Here’s a Doug Short chart to illustrate.

Source: Advisor Perspectives

In constant dollars and adjusting for hours worked, average weekly earnings for non-managers are now $779, and that’s an almost 40-year high. Millions of those now approaching retirement age spent their entire lives earning the equivalent of $40,000 a year, at most. Little surprise they don’t have six-figure retirement savings. The simple fact of the matter is, it takes enormous discipline to save even 6% for your 401(k) at that income level.

In a country of 330+ million people, shockingly few have enough retirement savings to support the stereotypical leisurely golden years. Dennis Gartman shared some disturbing numbers last week.

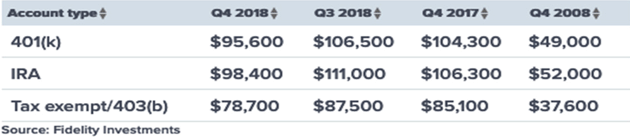

Firstly, we note that there were 133,800 “millionaires” late last year with sums of more than $1 million in their retirement accounts, which on its face, sounds like a large number. But that is down from 187,400 at the end of third quarter of last year, according to Fidelity Investments. According to the Federal Retirement Thrift Investment Board, which oversees TSPs, as of the end of last year, there were 21,432 “millionaires” compared to 34,128 at the end of September in those TSP accounts. The 4th quarter of last year was a disaster to those solely involved with equity investments; it was merely “horrible” for those with a more balanced investment portfolio.

But these are not really our focus this morning; our focus is that the average balance in 401(k)s, 403(b)s, or IRAs fell to $95,600 at the end of last year from $104,300 at the end of the 3rd quarter for 401(k)s, to $78,700 from $85,100 for 403(b)s and to $98,400 from $106,300 for IRA balances. It was not the drops in value that caught our attention; it is the fact that the averages are only at or near $100,000, forcing us to wonder what sort of retirement can the average retiree look forward to with this minimal sum of money set aside? Is that all there is? Really? Is that really all there is? If so, we are in very real trouble.

The average IRA balance is not necessarily indicative of retirement savings generally, as many other vehicles exist, but it’s probably a good proxy. And an average of around $100,000 won’t yield much of a supplement to the monthly Social Security benefits described above.

I found this chart on CNBC, which also refers to the study Dennis quoted:

Many of our parents and grandparents had defined benefit plans and other guaranteed retirement benefits from the corporations they worked for. Those are increasingly an endangered species in the private sector while 401(k)s, IRAs, and Social Security aren’t giving the average person enough to retire on anything close to a comfortable lifestyle.

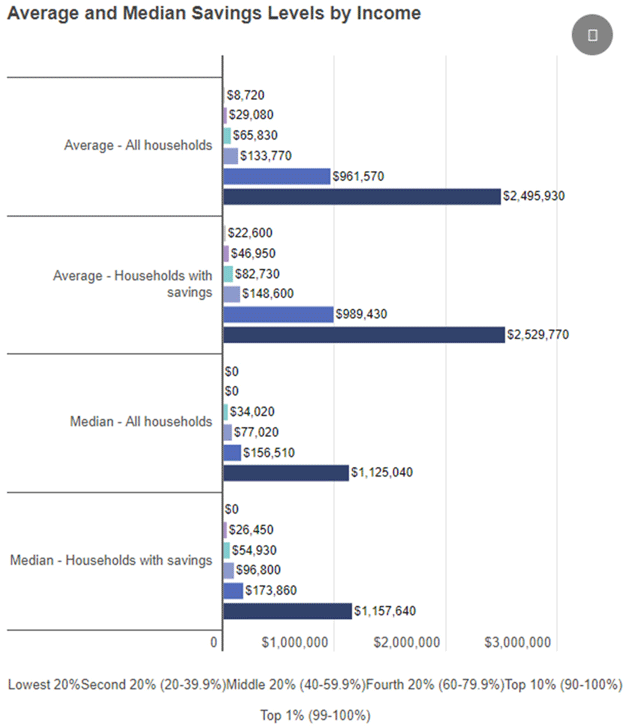

Average household savings for the bottom 40% are under $30,000. Median household savings for the bottom 40% are zero dollars. Clearly the top percentiles and especially the top 1%, skew the average. Note the bottom lines in the chart below is not the top 20%, but the top 1%. And the top 1/10 of 1%? Don’t make me giggle.

Source: cnbc.com

The point is that the 80% of households have less than $100,000 in savings. That is not enough for even a minimal retirement. Let’s make the very aggressive assumption that you can take 5% a year from your savings plan. If you have $100,000, that’s $5,000 yearly or about $417 a month—on top of your Social Security. And if you don’t have your house paid off? Or car?

The Indexing Problem in Retirement Accounts

Nearly every article I read on this topic talks about the fourth quarter’s losses, but something else leapt out at me.

Back-of-the-napkin math (and a rough napkin at that) says these retirement accounts are at least 50% invested in equity index funds. Some of you are now asking, “What’s the problem? All those index funds have come back. Everybody is back to where they started.”

Not so fast, Jack. As I have said until readers are probably tired of it, bear markets (which the last little bump in December barely qualifies for) that are not accompanied by a recession have V shaped recoveries. Which is exactly what we got.

Bear markets that are accompanied by recession take a very long time to recover and will likely be in the 40 to 50% loss range. A 50% loss requires a 100% gain to breakeven. That took about five years from the bottom of the last bear market.

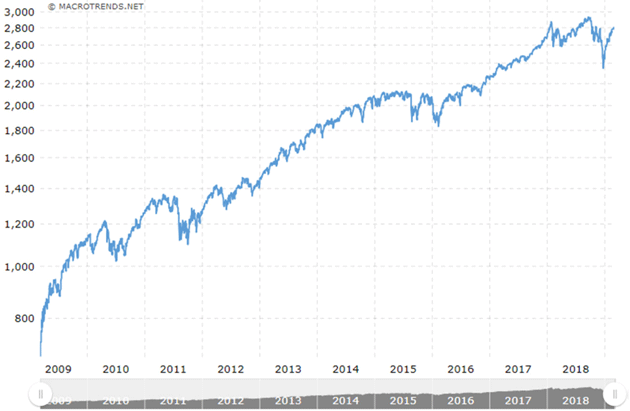

Now, let’s look at the chart from the S&P 500 for the last 10 years courtesy of Macrotrends. Note that the S&P is up well over 3.5x (give or take) in the last 10 years. But the 401(k)s and IRAs did not even double. Some of that is due to investors getting out at the bottom and back in later. Some is maybe due to high bond allocations in 2009 (bond funds had done very well, and we know people chase returns). But nonetheless, retirement funds have not performed as well as you might expect.

Source: Macrotrends

Further, when that next recession and bear market hit, it will take even longer to bounce back. The recovery will be even slower than this last one. As the research I’ve shared in previous letters shows, large amounts of debt slows recoveries. Very large amounts create flat economies. We are approaching large amounts in the US.

(Think what that large debt and recession did to Japan. What’s that song? Turning Japanese by The Vapors. The official 1980 video is not politically correct by 2019 standards but has some interesting historical tidbits along with the WWII propaganda silliness.)

In any event, the next recession will shortly cause a $30 trillion debt for the US government, soon to be followed by $40 trillion. Will that much debt turn us Japanese? That’s not entirely clear, since we have the world’s reserve currency and a unique role in global commerce and finance, but I think the recovery will be much slower, at a minimum. A double dip recession is clearly possible, making those stock market index fund losses even worse.

You must have some kind of strategy for dealing with market volatility. I don’t know how many times I can say that. But that’s the case only if you have savings to lose. Millions don’t, which means they have an even harder challenge.

Double Problem

I speak at a variety of investment events every year. Some are for high net worth investors, but others draw a broader crowd. Lack of retirement savings, both their own accounts and those of their neighbors and the rest of the country, is by far the most common worry I hear at those events. Sometimes it verges on panic, even among people who spent decades earning good incomes and saving all they could.

The Baby Boom generation that is now reaching retirement age has a double problem. First, many of its members didn’t save enough cash to support a comfortable retirement. Second, those many who did save enough could see it evaporate when we get into another bear market, which we certainly will at some point.

What can you do? Some suggestions.

First, whatever your age, save as much as you can. Stash it in your IRA, 401k, defined benefit plan, or whatever other tax-advantaged vehicles are available to you. Then save more outside them. If you look at your income and expenses and think “I just can’t do this,” think again. Start saving something, even if it’s $20 or $50 a month. Get in the habit and it will become easier.

(A personal note: If you have a small business, you should at a minimum have 401(k)s and business employment retirement plans. If you’re making a relatively good income, you should think about getting your own defined benefit plan. DB plans are not just for monster corporations. They can work extremely well for small, very closely held businesses. You can put away over $2 million of total contribution over your lifetime. If you start your plan and your age is 60, those can be some hefty annual contributions. Just another reason a good financial advisor can be useful.)

Second, invest in programs that give you at least a chance to dodge bear markets. Buy and hold works in theory, but not for most people because we are humans with emotions. We should recognize that and take steps to control it. As I continually say, we should invest in trading strategies and not buy-and-hold index funds in this environment. And of course, fixed income strategies like actual bonds, real estate, private credit, and so on.

Third, forget about retiring at 65 unless you are in truly dismal health (in which case, financing a long retirement is probably not your top worry). Keep working a few more years, even if you have to find a new career that better fits your circumstances. This will let your capital accumulate longer and you’ll get a higher Social Security benefit by waiting until 70 to start collecting.

Fourth, take care of your health. It will both reduce your medical expenses and keep you in shape so you can work and produce income longer. Further, staying physically active will keep you healthier. If that physical activity is involved in a job, that counts. There are studies that actually associate retirement with lower life and health spans. But gym time and a healthy diet are still important.

I’m personally doing all of the above, and I’m still concerned it won’t be enough. Laugh if you want to, but that concern for me is real. Relaxing is not in my personal makeup. I know a lot of people like me. I can only imagine the panic of those less fortunate and prepared. Their problems are yours and mine, too, because an economy with so many low-income elderly people has less opportunity for everyone.

While I think socialist and progressive policies are terrifying, they are spot-on when talking about wage and income disparity. Corporate profits are at their highest level ever percentage wise, yet labor is back to Great Depression levels. That is not healthy for our society. I am not going to start singing 1930s union songs, but this is a problem we must address. It is only going to get worse and the longer we wait, the more expensive the solution is going to be. Those of us with a libertarian bent may just have to suck it up and become part of the solution.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

John, don’t overthink it. By the time you retire you may be dead. Downsize, minimize strive for simple things and the appreciation of simple things that are a deep down pleasure. I understand that you have a certain life style that you want to maintain. I found that retirement is the icing on the cake. I can now pursue those things that are a passion for me. Fortunately my passions are reading, writing , cooking taking a walk in the woods, going to the beach. I retired at 62 so that I could enjoy the golden years of my life. We have cut back on so many unnecessary expenses. I am really building my library with books that have lasting value and are interesting, informative and inspirational. We don’t need two cars…we got rid of one. We don’t need cable TV so we got rid of it and now use Netflix and pay half the cost. It is possible to live well on a smaller budget.

I’m with you. Many people want to retire and live the same way they are now while they are working. I guess part of it is how much your income and health are like. Do you enjoy working until your mid-sixties? Or do you have to?

Some people love their work and that is another story.

I doubt 1% of the people will retire. 75 is the new 65. It costs me $2,000 month to live in my paid for home. Real estate taxes, insurance, utilities. Then there’s maintenance: new roof / AC / boiler / appliances all these things need repair or wear out. Cars need repair. Let’s not forget $135 month for Medicare part B + $99 for an Advantage plan. And that doesn’t cover all the medical expenses. I figure you need $50k to live near a metropolitan city.

We have kicked out of Health Insurance altogether. We could not get an affordable plan with a reasonable deductible. We pay by the visit and we go to a holistic doctor who also has an MD. It costs a lot less. We have adopted a new paradigm for healthcare that puts responsibility for our health..squarely where it belongs….in our hands. We take no pharmaceutical medications and eat only nutritious, whole foods that are generally organically produced. Also we live in a state where the taxes are low and the cost of living is affordable.

What happens if someone in your family gets a terminal illness? Serious question. We’ve pondered going off the grid, but fear of the healthcare industrial complex keeps us hooked.

Comedian John Oliver on Retirement Plans:

is Shane a girls name?

I didn’t know Shane was a woman’s name.

Maybe his dog? Let’s hope not a goat.

“save your money inside a 401”? While he has good intentions, he and you should understand the simple allegory in the video below. THE MONEY IS ALREADY GONE !! All paper assets are junk, crap, empty promises. Too many promises, too many people who have nothing. The government will be looking to steal your funds to give to themselves and the idiots who saved NOTHING over a lifetime. Just looking at the demographics alone will wipe out any future growth in the stock market. As Boomers sell their assets who will buy them? Who wants or can afford all the McMansions. There will have to be extreme means testing in the future. Next, pile on all the other problems and predicaments we have like decreasing available energy, political insanity and a million other things. Get out of the system and into the timeless wealth preservation of real tangible assets, NOT PAPER. You’ll have to keep working until the final face plant on the floor of wherever you’re employed.

Niall Furgesons version is better. Also, generations are already acclimated to the fiat paradigm. Too late. That’s why it won’t happen.

Most men fear retiring when the time comes because they feel like they will be of little value. Too many have made work their god and without other interests, those that have made it their god, will probably be dead within 6 – 12 months of retiring. The key is to have multiple interests beyond the workplace. A year or so before I retired at 61 I took up beekeeping. I also have a small homestead where I put in a big garden and I also have a small flock of chickens. I volunteer with my county with the local CERT team and, multiple things through my church. I am able to apply skill sets I had as a project manager to many of the volunteer positions I have so, I still have the sense of being valuable. I also was out of debt when I retired and, I actually live a little better than when I was working. I’m not touching my principal but, between SS & a monthly payout from an insurance annuity (NOT from my former company), my wife and I live very comfortably.

Honestly, if you are pushing 70 and still feel like you need to work, I honestly believe you are in denial. You may be feeling good at the moment but, that can change in a heartbeat. Go now, enjoy your life and, give back to your community.

Finally, and I know many of the regulars on here probably won’t agree with this — get right with the Almighty! To me, this is #1 — you will have a peace about things that transcends this world because whether you believe it or not, there is an eternal existence beyond the mortal world we live in now.

Just buried a father-in-law at 76. He couldn’t retire. Not because of monetary issues, but he was a just a workaholic and had no other outlets. Worked full-time till 70 (university teacher), started part time after that. Had an accident 6 months into this situation that left him an invalid. Family took care of him for 6 years until he passed.

Time is precious. Use it wisely…

“Time is precious”

If you steal my money, I can get more money. If you steal my time, I can never get that back.

brewer55,

I had been intensely career minded most of my life. A senior VP of a national retail company once told me I was the most driven executive he had ever managed.

At 60 I found myself at a crossroads. Was offered a VP position with the 13th largest company in the world. I had been on again off again consulting for them for years. It was a huge salary/bonus and a prestigious position that was whispering to my ego…but I would be on the road constantly, some international travel.

The other choice was at a local company I had consulted for, the same industry. The offer was on retainer on a month to month handshake (solid owner who I liked) three days a week/24 hours billable (max) a week. Being debt free and living modestly I could still save and live well on the comparatively modest salary compared to the big corporate job/bucks.

I took the local job and ended up staying 5 years.

The most valuable hard assets of all…TIME…was now mine.

I retired completely at 65 after the same company who offered me the big job bought my 5 year client out and then made me another offer. But I wanted more freedom and time not less.

During those years from 60 to 65 I found the freedom of four day weekends allowing me the TIME to build a farm/homestead one of the greatest experiences of my life.

Your post hit the bullseye for me buddy. Especially the last paragraph about…eternity…now that’s a lot of TIME.

Thanks for the reply, Mark. I’m glad you made the right choice, for you.

Stay active appears to be key. My granddad retired from the fire department at age 66 and lived in retirement to age 93. He ran a little rooming house on the side and was active in several fraternal and charitable groups. There are no guarantees, but it can’t hurt to stay a little busy.

Without a doubt MR…You can’t control your genes, but you can control the size of the jeans you have to wear through DIET and EXERCISE (activity – mental as well as physical. I get my mind exercised here quite a bit.)

One fact about running a modest working farm/homestead of any size, you won’t need a gym membership and the quality and nutrition of much of the food you produce/eat is another gift to your health and longevity.

The other major factor is not to let your occasional vices become your daily habits.

Are you talking to Stucky? He’s assured us he has no hair on his palms yet.

No one will able to retire after this next collapse . We are head to hell when the shit finally hits the fan. I would say prepare and pray. Alot of older people will become easy targets for hungry and or scared people.

BB,

Working on forming a CMSG (Christian Mutual Support Group) starting with two friends/neighbors who are of a like mind and then hope to spread it throughout my small country church and neighborhood.

Local organization and mutual support and citizen support for law and order and its enforcement will be critical. Almost everyone around here (north east NC) is seriously armed.

Not too far from you.

Hope your Mom is doing well…my 92 year Mom is ailing with a serious heart issue.

How The World Could Change In 7 Days: One Moment The Building Is Alive, Bright, Vibrant, Buzzing. With The Flip Of A Switch, It Lays Still, Cold And Dead

Average middle income Americans have been financially squeezed out of not just retirement but nearly out of existance .

The private sector employment opportunities do not offer salary and benefits so retirement and medical insurence are all piled on what has been stagnent or reduced salaries . Consequently saving and investing for an adequate retirement is impossible . Not from bad financial decisions for a huge percentage of people just the reality of current economic issues as a nation circles the drain financially .

The fact that government pension plans are $7 trillon dollars short on all levels local state and federal . Judges have already deciding they must be full funded after decades of mismanagement ! Where to get that funding you might ask ? The middle class left standing with real property and savings will be seen as a revanue source for government employees to continue that mid 50’s retirement by forcing others into working till they drop . See , socialism works for government employees by way of government controlled orginized theft !

They must be paid as promised and screw everybody else .

Trouble in River City … riot and civil unrest awaits !

Your point is the one I made above. The middle class has been hammered and most will need to work until the final face plant. I see a few high execs talk about time in retirement- Good for them but it’s not like that for the middle class. You quit your job and 5 years down the road the is too much month for your money.