Current developments on the inflation front should be a stark reminder that discretionary monetary policy is one of the great–if not the greatest— statist cons of our times. At the end of the day, modern central banking is simply a cover story to enable expansion of government activities either by creating unnecessary crises and dislocations or owing to falsely cheap interest rates which enable vast increases in the public debt.

In the present chapter of post-Volcker monetary policy machinations the Fed is allegedly attempting to thread the needle to bring inflation back to the sacrosanct 2.00% “goal” while not sending the economy into the recessionary drink. But in that mission it will positively fail (again).

That’s because it has neither the tools to control the inflation rate with any precision (or any other macro-target), nor even measure it with the accuracy implicit in its policy targets. In this respect, monetary-policy-in-one-country is no more valid than was socialism-in-one-country when Stalin advocated it upon Lenin’s death in 1924. The predicate was just plain wrong, then and now.

In the current case, the Fed can do one tangible thing alone (aside from jaw-boning and open-mouth policy which can’t be taken seriously in today’s world). To wit, it can create or extinguish fiat dollar credits via its open market operations, but it has virtually zero control over the subsequent destiny and impact of these credits as they wind their way through the canyons of Wall Street initially, and eventually through the real economy and its global linkages to merchandise trade, international labor cost arbitrage and money and capital markets flows over the length and breadth of the world economy.

For instance, it has no control whatsoever over the Brent global marker price for crude oil, which has again pushed over $90 per barrel, bringing the related domestic WTI price up from a recent low of $65 per barrel (May 2023) to nearly $85. Moreover, crude oil supply is fixing to remain materially shrunken by upwards of 1.7 million barrels per day owing to the recently announced extension of production cuts by Russia, Saudi Arabia and lesser OPEC members.

As a result of these supply constraints and continuing healthy global demand, US crude oil inventories have hit a 40-year low of 46 days consumption. In part this is due to the foolish Biden policies which drained nearly 300 million barrels from the nation’s strategic reserve (SPR) in a blatant effort to lessen pump prices during last November’s Congressional elections.

As is shown so dramatically by the graph, current inventories are just 50% of the peak inventory that was reached in May 2020. Again, this was owing to a non-monetary development—the economic crash from the Covid Lockdowns—which caused oil demand to plunge, bringing prices down to the sub-basement with it.

Needless to say, that 46 days inventory swing was no drop in the bucket. It amounted to the equivalent of nearly 800 million barrels of crude oil or more than two-months of domestic crude production. And this was magnified globally owing to demand and inventory swings on a world-wide basis of equivalent magnitude.

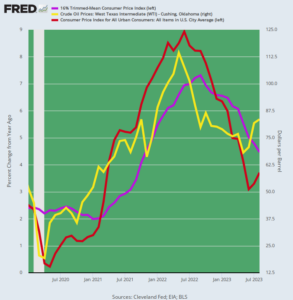

Accordingly, the path of the WTI price (yellow line) in the chart below was violent, to put it mildly. Even on a monthly average basis, the price path plunged by 63%, from $52 in January 2020 to a low of $19 at the bottom of the Lockdown crash in April 2020; it then climbed relentlessly by 500% to a peak of $114/bbl. two years later in May 2022, only to fallback to the aforementioned $65 low in May 2023, thereby representing a 43% decline. And now its up by more than 30%, and destined to go considerably higher as inventories continue to shrink owing to daily consumption well above daily production on a global basis.

Goldman Sachs therefore now projects that the Brent market price may again exceed $100 per barrel by late 2024.

The bank had expected that in January the countries would bring back half of the 1.7 million barrel per day cut that was announced in April. Now the bank is floating the possibility of an even longer extension.

“Consider a bullish scenario where OPEC+ keeps the 2023 cuts…fully in place through end-2024 and where Saudi Arabia only gradually raises production,” analysts at Goldman Sachs wrote in the report.

In that scenario, Brent oil prices would likely climb to $107 a barrel in December 2024, the bank said.

Of course, with variable lags and coefficients, the drunken sailor path of the crude oil price pulled the headline CPI (red line) and the more stable 16% trimmed mean CPI (purple line) along with it. In the case of the former, the pre-pandemic headline CPI rate of 2.5% on a Y/Y basis in January 2020 plunged to just 0.2% by May 2020, and then was off to a wild romp, rising to 8.9% Y/Y in June 2022, then falling to just 3.0% by June 2023 before climbing higher again, to 3.3% in July.

Owing to the inherent smoothing mechanism built into the 16% trimmed mean CPI (purple line), the path over this 42-month period was much flatter, but still far from the Fed’s targets. Thus, the 2.4% Y/Y increase posted in January 2020 fell only slightly to 2.3% in May 2020 and then climbed smartly but far less dramatically to a peak of 7.3% in September 2022 and has now settled at 4.8% in July.

However, the latter is still nearly 2.5X the Fed’s inflation target—even as global oil and other commodity price development now threaten to send the consumer inflation gauges higher once again.

Crude Oil Price Versus Headline CPI and 16% Trimmed Mean CPI, January 2020 to July 2023

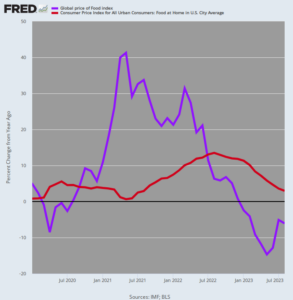

For avoidance of doubt, here is a similar story for food prices over the same 42-month period since January 2o2o. In this case, the global food price index (purple line) was running at +4.9% in January 2020 and then dropped to negative -8.5% on a Y/Y basis at the April lockdown bottom—before soaring to +41% Y/Y gain in May 2021. Thereafter it headed violently southward, bottoming at -14% in May 23, only to hook sharply upward as of July, rising at a +22% annualized rate.

The food component of the CPI (red line), of course, followed a similar, if more modulated, path. But it did rise from less than 1% Y/Y in January 2020 to a peak increase of 13.5% in August 2022. By July 2023 the Y/Y measure had cooled to 3.6% but again the global trend is now rising sharply, meaning that this CPI component has likely bottomed as well.

In either case, wars, weather and government supply control policies all around the world vastly outweigh any negligible impact on food prices which may result from the machinations of the Fed. Indeed, we doubt whether such impacts are even detectable since even if the Fed manages to trigger a notable recession, food demand will be scarcely impacted.

Y/Y Change in Global Food Index Versus Grocery Store Prices in the CPI, January 2020 to July 2023.

Tens of millions of actors on the free market—producers, workers, distributors, retailers, savers, investors and speculators—have a far better chance of “discovering” the right price for economic inputs than the 12 supposed geniuses who sit on the FOMC.

Moreover, the advantage of price discovery on the free market is that it is continuously adjusted and self-corrects as new information arises and new economic conditions unfold. Indeed, on the free market there is virtually zero chance that interest rates would be held too low for too long, as was the case with the monetary politburo’s 12 decision-makers during the recent past.

Yes, inflation is still everywhere and always a monetary phenomena but the money in question is that produced by dozens of fiat central banks, not simply the Federal Reserve; and its lag effects are so variable and extended in time as to be unknowable for any practical purpose, such as monthly Fed meetings or even a whole year’s worth.

That’s why at the end of the day, the best case for even general price level inflation is to leave it to the free market.

Editor’s Note: The Fed has already pumped enormous distortions into the economy and inflated an “everything bubble.” The next round of money printing is likely to bring the situation to a breaking point.

If you want to navigate the complicated economic and political situation that is unfolding, then you need to see this newly released video from Doug Casey and his team.

In it, Doug reveals what you need to know, and how these dangerous times could impact your wealth.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

Really? @ THIS late stage of the charade?

CRAZY Talk!

Just Might work?

If rates are not discovered by the markets they are merely darts thrown by PhD monkeys. They can NEVER be right from the start if the assumption is that a small group can sit around a table and act as the proxy for hundreds of millions of people making billions of individual independent financial actions.

Governor Iffy Macklem of the Bank of Canada is promulgating fraud

in so far as he lies to the Canadian taxpayers every time he opens his

mouth. Moreover, he is telling Canadian taxpayers that he still expects

a return to 2% Core Inflation whereby our headline print for September

is 3.8% even after the bastardization of the Board of Governors on the

fraudulent CPI calculations.

Stockman is right that these mindless retards follow the goddamned

Federal Reserve imbeciles in lockstep on a handcart to Hell.

Cha ching

Cha ching

Cha ching

Trickledown Economics was always just peeing on our collective

pant legs whilst informing us via media that it’s raining.

Even Judge Judy knew better than this.

MOU

WHY are we still so dependent / beholden to ONE commodity price? Natural Gas should NOT be used to generate electricity, uranium should be! This would lower the cost of natural gas to a range household heating could afford it, and partially diversify the dependence. Likewise, as many more sources of electrical generation (hydropower, geothermal steam, wind if ever feasible) should be used as are economical, to further reduce dependence on coal and natural gas.

The fact Dementia Joe has REDUCED oil leases / drilling / acreage as well as limited nuclear powerplant approvals shows how stupid he and everyone else in W.D.C. are, since they have had DECADES to diversify electrical power generation and done ALMOST NOTHING.

Stupid is as stupid does.