Two recent surveys, along with numerous other studies and data, reveal most American households to be living on the brink of catastrophe, but continuing to act in a reckless and delusionary manner. There have certainly been economic factors beyond the control of average Americans that have resulted in real median household incomes remaining stagnant for the last 36 years. The unholy alliance of mega-corporations, Wall Street and bought off corrupt politicians have gutted the nation of millions of good paying jobs under the guise of globalization, while utilizing debt, derivatives and financial schemes to enrich themselves. The malfeasance of the sociopathic privileged class does not discharge the personal responsibility of citizens for living within their means. A lack of discipline, inability to delay gratification, failure to understand basic mathematical concepts, materialistic envy, absence of critical thinking skills, and a delusionary view of the world have left the majority of Americans broke and in debt.

The data that captured my attention was how little the average American household has in savings. Roughly 62% of Americans have less than $1,000 in savings and 21% don’t even have a savings account, according to a new survey of more than 5,000 adults conducted this month by Google Consumer Survey for personal finance website GOBankingRates.com. This dreadful data is reinforced by a similar survey of 1,000 adults carried out earlier this year by personal finance site Bankrate.com, which also found that 62% of Americans have no emergency savings for a medical crisis, car repair, or unanticipated household expenditure.

The fact is these are not highly unlikely scenarios. They happen every day as part of our routine existence. Everyone gets sick. Every car eventually needs new tires or an engine repair. Every home will need a new hot water heater or roof at some point. It is foolish and short sighted to not expect “unexpected” expenditures. Living in the moment and fulfilling your immediate desires may feel good today, but leaves you susceptible to disaster tomorrow. Gradually building a rainy day fund over time is what adults should do. Only immature children operate with no safety net. Everyone has an excuse for why they end up living on the edge, but the data exposes us to be an infantile nation of spendthrifts incapable of distinguishing between wants and needs. It might be understandable for young adults who are burdened by student loan debt and entry level jobs to have little or no savings, but the data for older Americans is most disturbing.

It seems 51% of all Generation X adults between the ages of 35 to 54, in the prime earning years of their lives, have ZERO savings, the highest among all age cohorts, with over 20% of them not even having a savings account. This is incomprehensible and reveals an almost juvenile approach to life. Approximately 70% of all 35 to 54 year old households have $1,000 or less in savings. These are people who should have been working for the last 10 to 30 years. To not have put aside more than $1,000 is beyond irresponsible, and the justification of earning no interest on savings is disingenuous as they could have earned 5% up until 2008. This shocking state of affairs can’t only be laid at the feet of the evil bankers and rich corporate titans.

Every person has to accept personal responsibility for their own life. There is one sure fire way to accumulate savings and that is to spend less than you earn. It sounds simple, but the vast majority of Americans have chosen to live beyond their means by allowing themselves to be lured into debt by the Wall Street debt peddlers and their Madison Avenue media maggots selling dreams to willfully ignorant delusional consumers. Consumer dependent corporations hawking autos, electronics, glittery baubles, fashionable attire, toxic processed sludge disguised as food, and other slave produced Chinese crap, require a vast unlimited supply of easy money debt to keep profits rolling in. And the Federal Reserve has been willing and able to accommodate them.

Those who control the levers of this perverted economic system utilize Fed easy money, propaganda advertising messages, and the susceptibility of an oblivious populace, suffering from delusions of grandeur, to create generations of debt enslaved hamsters running on the wheel of life. But, we were not forced into this enslavement. Millions have chosen to live lives of quiet desperation in order to keep up with the Joneses. They would rather portray themselves as successful and wealthy, rather than make the necessary sacrifices required to achieve success and wealth. Everyone has the ability to live beneath their means. Millions have made the choice to do so. The chart above shows 10% to 20% of people do have $10,000 or more in savings, including young people. Many are average middle class Americans, not the despised 1%.

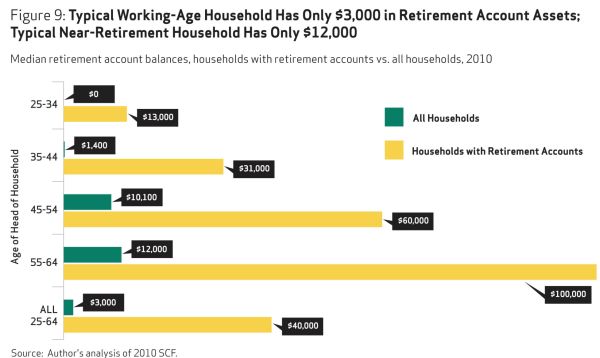

It is certainly not easy to accumulate savings in an economy stacked against the working middle class, but it is possible. It requires self-discipline, deferring gratification, patience, budgetary skills, staying employed, and not coveting your neighbors’ possessions. The lack of short-term savings is not an isolated data point. It is representative of a nation of narcissistic live for today ne’er-do-wells who rarely concern themselves with the future or the consequences of their actions. They haven’t been putting all their spare cash into their retirement plans either. When you realize the typical household between the ages of 35 to 54 has less than $10,000 saved for their retirement, the mass delusion becomes clear. How could Boomers, who have worked for 30 to 40 years, and experienced the greatest bull market in history (1981 – 2001) have only $12,000 of retirement savings as they approach retirement?

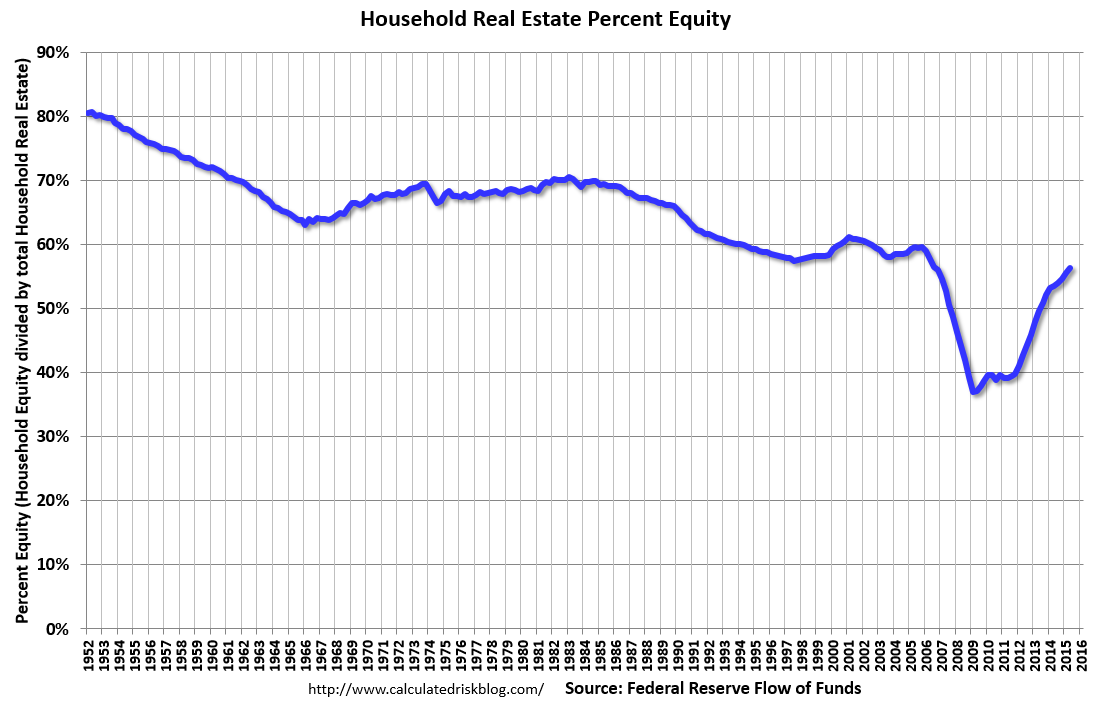

These are median figures, so half the households have even less retirement savings. It requires decades of living above your means to accumulate such little in savings. The apologists for the non-saving masses often argue Americans were utilizing their homes as a store of wealth to be used in retirement. This is just another false storyline, as the savings poor public used their homes like an ATM machine from 2001 through 2008, extracting hundreds of billions to spend on granite countertops, exotic Caribbean vacations, home theaters, BMWs, Olympic sized pools, bling, and new boobs for mommy. Equity in homes plunged from 60% to below 40% in the space of a few years and has only recovered to 55% after the Fed induced faux housing recovery. There are still millions of homeowners underwater, with the next leg down guaranteed to add millions more.

The millions of American households living on the edge and headed for a poverty stricken old age have a million excuses for why they never saved a dime. These are the same people who will demand the government save them from their own foolishness and irrational life choices. They will demand the rich (anyone who worked hard, saved, and planned for their future) be taxed more, so they don’t have to live with the consequences of their reckless disregard for common sense and self-discipline. These people should have read some Shakespeare in high school, and maybe they wouldn’t be in this predicament.

“The fault, dear Brutus, is not in our stars, but in ourselves.” – William Shakespeare, Julius Caesar

We are all responsible for our own lives and our own decisions. It isn’t complicated regarding how to save money. But it is hard. It requires simple math skills like addition, subtraction, multiplication and division – concepts not thought too important in our government controlled educational system. It requires self-control, acting like an adult, and distinguishing between what you want versus what you need. It’s OK to splurge once in a while, but since around 1980, multiple generations have been binge spending in an orgy of debt debauchery unmatched in human history. Since 1980 the U.S. population has gone up by a factor of 1.42, GDP has expanded by a factor of 6.3, and consumer debt has exploded by a factor of 10. The amount of consumer debt per person in 1980 was $9,300. Today, the total is an astounding $65,200 per person, a 700% increase in 35 years. We owe $21 trillion of mortgage, credit card, student loan and other debt to the felonious Wall Street bankers. This nation has gone insane.

“In individuals, insanity is rare; but in groups, parties, nations and epochs, it is the rule.” – Friedrich Nietzsche

With a median household income of about $56,000 and median net wages per worker of $29,000 it is fairly easy to grasp the monthly inflow of a middle income household. In Median World, taxes will take about a 16% chunk out of those figures, so the median household ends up with about $4,000 of take home pay per month. If they own a median priced home of $189,000, their monthly mortgage payment would likely be about $850. Add another $200 to $300 per month for property taxes and you are on the hook for $1,100 per month. A median rent figure would be in the same ballpark, unless you live in SF, NYC or a few other overpriced markets. This is where many people go off course, allowing themselves to be lured into more house than they can really afford with low down payments guaranteed by the government, driving the monthly housing burden north of $1,500. McMansion envy has destroyed more lives in the last ten years than any other delusion.

Food, clothing, utilities, and home upkeep expenses could total $1,500 per month for a family with kids. If one or both parents are stuck with student loan debt, a monthly payment of $200 to $400 would be normal. There isn’t much spare change left to fund their remaining needs, wants and desires. But their neighbors and coworkers are all driving new cars. They can’t be seen driving a used 10 year old clunker. People will think they’re poor. Shallow appearances are all that matter to a vast swath of America. According to Edmunds.com, the average monthly payment on a new vehicle is $479. We can’t have one spouse driving a new car, while the other slums it on public transportation, so two newer cars will add another $900 or so of expenses to the monthly budget.

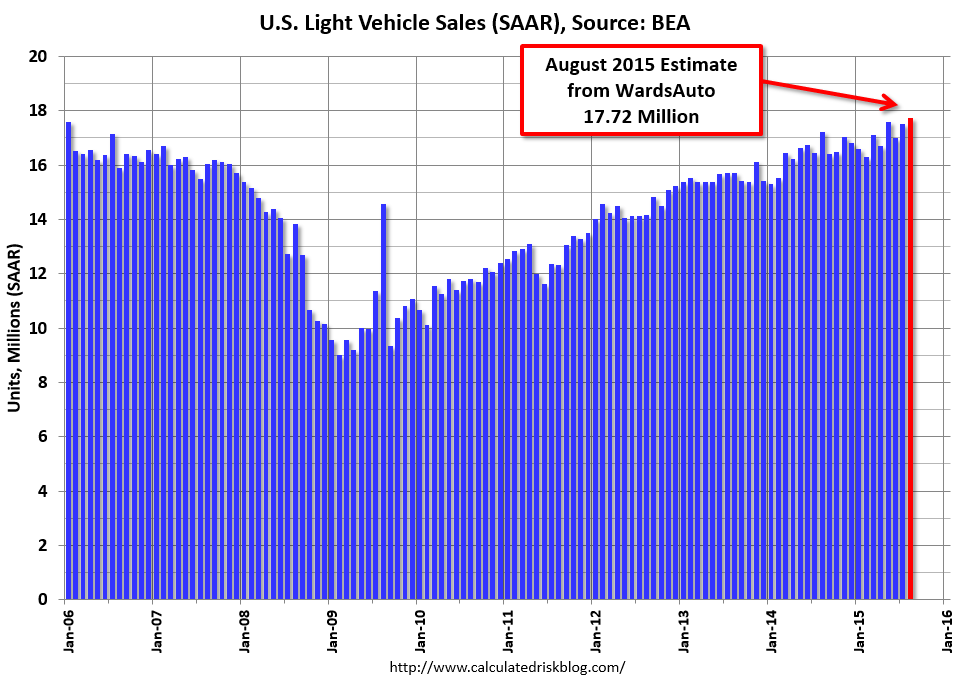

Wall Street and the automakers are only too glad to offer those with good credit a 7 year 0% loan, guaranteeing a permanent status of being underwater on your loan until you must have that new model after four years, rolling the underwater loan into the next purchase. The permanent leasers convince themselves they are making a good deal as they sign their lives away every three years without understanding the financial implications of the leases. And then there are the 20% subprime auto buyers who pretend to pay until the repo man shows up in the middle of the night. This delusion of debt is how annual auto sales have soared from 10 million in 2009 to almost 18 million today.

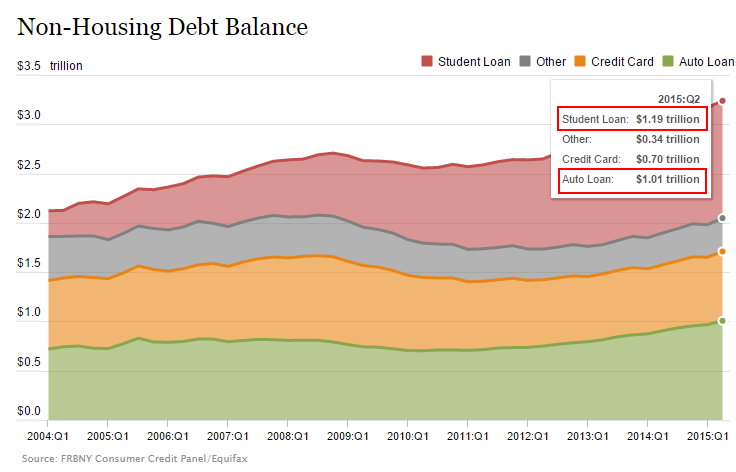

I’m on the road every day and it is mind boggling to see the number of newer $30,000 to $50,000 vehicles cruising the highways and byways of America. Even in the poverty stricken neighborhoods of West Philly, brand new BMWs, Cadillacs, and other $25,000 or more vehicles are parked in front of dilapidated hovels and low income housing complexes. Virtually none of these vehicles are owned outright. Americans are essentially renting their luxury wheels so they can appear successful. The way to become financially successful on a modest income is to buy used cars and drive them for ten or more years. The years of no car payment can be directed into savings. Very few people chose this path. That is why auto loan debt has now exceeded $1 trillion, up 40% since 2010. Wall Street wants you in perpetual debt and millions have bought it hook line and sinker. But at least they appear prosperous to their neighbors, while they’re really in debt up to their eyeballs.

The choice to indulge in driving over-priced ornamental transportation basically leaves the average household with little or no discretionary income at the end of the month. But that doesn’t stop spendthrift nation from becoming addicted to their mobile phones and binge watching reality TV. The average American, who had never heard of a mobile phone in 1990, now can’t go 20 seconds without checking their phone. And they are paying through the nose for the privilege of staying terminally connected. We have smart phones for dumb people. Even welfare recipients without jobs, living in low income housing and dependent on food stamps, somehow find the funds to have a smartphone in their hand 24/7. Maybe directing those funds towards books might give them a better chance of exiting poverty.

In one survey, 46% of Americans with mobile phones said their monthly bill was $100 or more and 13% said their monthly bill topped $200 per month. The average individual’s cell phone bill was $73 per month last year, a 33% increase since 2009, according to J.D. Power & Associates. When they aren’t texting, tweeting, or facebooking on their iGadgets, they are watching basic cable boob TV at average price of $100 per month, up 39% since 2010. But our connoisseurs of crapola need the NFL Package, HBO, Showtime, Netflix, and on demand porno. Tricked out smart phones and cable packages are not necessities. They are wants. Wasting $200 to $300 per month on narcissistic compulsions is a choice.

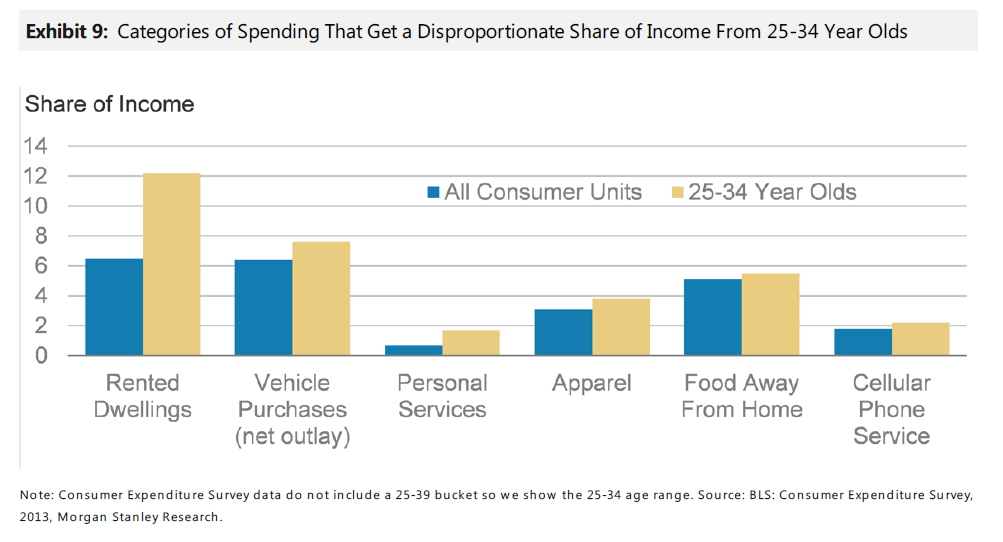

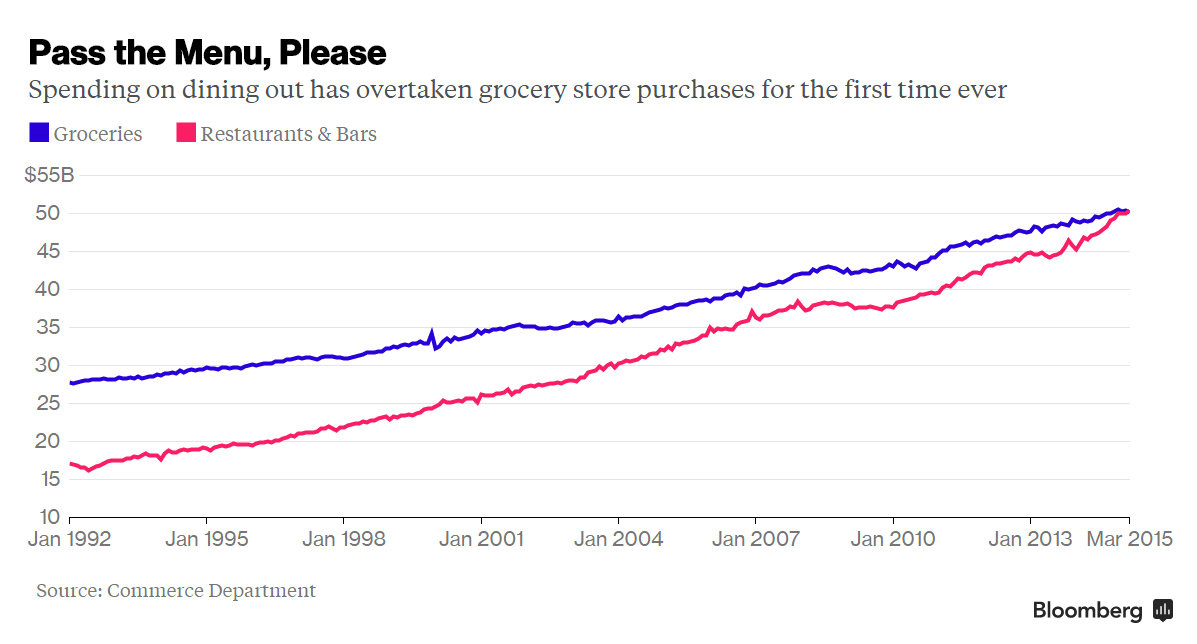

Possibly the largest squandering of resources occurs on a daily basis, as Americans spend money they don’t have on $5 lattes, toxic fast foodstuff, craft beers, and whatever else strikes their fancy. According to the most recent Bureau of Labor Statistics consumer expenditure surveys, the typical household spends $2,625 each year, or around $219 per month, on food away from home. Those in higher income brackets spend the most on restaurants at around $370 per month. Millennials, with the least amount of discretionary funds, view dining out as a social event, and choose fun and frivolity over finances. The concept of brown bagging your lunch for $1 rather than spending $10 at Paneras, or brewing a pot of coffee for 25 cents rather than paying $5 at Starbucks is inconceivable to the live for today credit card cowboys and cowgirls.

Dining out is the ultimate personal choice and a huge factor in the non-existent savings of American households. Over the last two decades Americans have abandoned the frugality of buying food at the grocery store on sale, using coupons in favor of eating out at a hefty premium on a daily basis. The result has been a $10 billion gap in spending between groceries and dining out being obliterated by an army of live for today for tomorrow we can make the minimum payment on our credit card juveniles. Not only has this penchant for satiating their hunger contributed greatly to their lack of savings, but has been financed on their credit cards. That $25 Applebees dinner, financed at 18% interest over the next ten years ends up costing $54. Multiply this foolishness hundreds of times per year over decades and you understand why Boomers have less than $1,000 in savings accounts and $12,000 or less in retirement savings. It’s just math.

The expenditures detailed above don’t include healthcare, entertainment, vacations, government extractions (tolls, fees, fines, taxes) and assorted other miscellaneous wastes of money. It is pretty clear the monthly outflow exceeds the monthly inflow for the majority of Americans. That is why the average household has credit card debt of $7,500 and those carrying a balance pay an average interest rate of 14% on their $16,000 ball and chain. This is on top of an average mortgage obligation of $155,000 and average student loan commitment of $32,000. The Wall Street hucksters are only too happy to help you finance a lifestyle well above your true means. They borrow from the Fed at .25% and charge you 10% to 20% for the use of credit created out of thin air. They always win. The willfully ignorant are thrilled they can now pay their IRS bill, property taxes, utilities, and just about every daily expense with a credit card. They fail to acknowledge the insanity of their chosen lifestyle path.

I still remember something my sophomore English teacher Mr. McGrath taught the class, based upon the writings of Aristotle. Human beings are rational, sentient, living, corporeal substances. What separates us from animals is our ability to think and act in a rational manner, rather than just on instincts and urges. Based on what has occurred in this country over the last 35 years, I’m starting to question the rational part. It’s almost as if a mental illness has befallen a majority of Americans. The Deep State and their minions on Wall Street and the corporate media certainly attempt to mold and manipulate the minds of the masses, but at the end of the day people are free to disregard those messages and live meaningful lives on their own terms. Even though living above your means has become “normal”, it is only normal in relation to our profoundly abnormal society. Telling people the truth today is meaningless, as they don’t want their illusions destroyed. But destroyed they will be, when this teetering edifice of debt comes crashing down on their heads.

“The real hopeless victims of mental illness are to be found among those who appear to be most normal. Many of them are normal because they are so well adjusted to our mode of existence, because their human voice has been silenced so early in their lives, that they do not even struggle or suffer or develop symptoms as the neurotic does.” They are normal not in what may be called the absolute sense of the word; they are normal only in relation to a profoundly abnormal society. Their perfect adjustment to that abnormal society is a measure of their mental sickness. These millions of abnormally normal people, living without fuss in a society to which, if they were fully human beings, they ought not to be adjusted.” – Aldous Huxley – Brave New World Revisited

“Sometimes people don’t want to hear the truth because they don’t want their illusions destroyed.” – Friedrich Nietzsche

I’ll be 75 shortly. Married 51 years. 4 kids. All college educated. Retired at 59. I won’t tell you all my financial conditions but I’ll give you one piece of advice. I’ve had NO debt for the past 27 years and it is the one thing that made the past 27 years possible. It doesn’t take a lot to live when you have no debt.

Oh, and one other thing. I’m so glad I was born 75 years ago because 20-30 years later and I wouldn’t have a fucking dime.

Acetinker, flips the porcupine over. Now what?

starfcker has his ass kicked all over this thread so he cheers on the troll acethinker. That says a lot about starfcker and his intellect.

If things are so bad then HOW THE FUCK do these sports arenas get filled out every night … $200 to watch a meaningless baseball game yet somehow the country is on the verge of collapse. I mean come on dude if I can afford to buy a prostitute one night a week then shit must still be pretty damn good.

procrastinator

Are you as dumb as you seem? Did you read the fucking article or is it above your 85 IQ level. CREDIT cards you douchebag.

first and last time to this shitbag site… wow.

Paul

Don’t let the fucking door hit you in the ass on the way out. Make sure you make the minimum payment on that credit card.

Well – after reading through almost all of the comments here I can tell you for sure I’m the dumbest son of a bitch in the bunch.

Gen X’er mid 40’s.

I started a business, sold and bought a house and moved 1000 miles in 2008.

I’m married with two kiddies – a daughter with some pretty major health issues and a son I am damn proud of. He’s 14, smarter than me and humble about it. What more could a dad ask for? Every night at the supper table we pray together as a family and give thanks mostly for each other. I think it’s more important to love than it is to be bitter (although there are moments). Always remember – no matter how bad you think your life is at that moment some one else’s sucks even more.

I’m still happily married to an attractive, loyal, intelligent woman that I gleefully chase around the house as often as possible. My kids think its gross. I think its funny. Mrs. Marion tolerates all of us. We still plan on getting real old together. It hasn’t always been easy but thankfully she’s a patient woman and I don’t hear very well.

Two years ago I bought a Mercedes C class because I was having my version of a mid life crisis. I also picked up a neat little wool cap to wear while I was driving it. I looked like an idiot. I ditched the cap and gave the car to Mrs. Marion. I now drive her 10 year old SUV and promise to never have another mid life crisis again or buy another funny hat.

I have savings but don’t worry too much about it. Retirement is over rated and besides – I look stupid in funny wool hats. I can barely imagine what I’d look like in fucking white golf pants and a polo shirt. The thought of sitting around some retirement community in Florida or Arizona makes me want to puke anyways. I figure when its time I’ll wander off into the woods and end it “Legends of the Fall” style and let a big G bear chew my ass.

Some times I spend more than I should. When I do I usually sell something or work more doing something on the side of what I normally do to pay it off. Buy shit, sell shit make a profit. Work more when you have too and play more when you can. Some days I’m burnt out by it all but after a day of peace and quiet I am bored and ready to roll. By and large I see life as kind of an adventure.

Currently I am teaching myself to never get too attached to stuff. Including slick looking German sports car and wool hats.

Life is what we make it people. You makes your choices, you live with them. The good ones and the bad ones.

If you think its more important to have money, savings and vacations in Europe than family then go wild. If you spend more on your kids than you earn that’s your choice. Both roads carry some mighty awesome consequences in time. Just make sure you got your big boy panties on when those consequences come a calling. Cause you’re gonna need them.

I know I wear mine every day. God has a sense of humour – he likes to keep me on my toes which means I never take the good stuff for granted or expect things to always go my way. Life would be boring if it were otherwise.

As for sympathy for my fellow Gen X’ers I’ll leave you with a little advice from a guy who had it hard – my dad. He said son – if you are looking for sympathy you can always find it – in the dictionary right between shit and syphilis.

Peace.

Retirement is for pussies…

What do you think? You’re going to live forever?

It’s easy enough to say that men who get married and/or have kids deserve the consequences of their foolish decision (divorce court rape), but there’s a problem: most men have no idea of what really goes on in family courts. It is certainly unconstitutional and unjust, but it is also un-publicized, at least by the MSM.

The message IS starting to get out, however.

Karalan – how can any man not know the ass raping that happens in divorce? Quit making excuses. Sure, divorce and family court is against men. It is no damn surprise.

Marry a bimbo and get what you get.

Marriage is the single most important decision a person ever makes. If you get it wrong, tough titty to you.

Seriously, where did all these whiny-ass punk pussies come from? A lot of folks need to grow a pair and step up close to the plate. I am tired of all these squat to pee types posting. Hell, our womenfolk – TE, Hope, PJ, KaD, et al, all have big brass ones, but these men cannot find a pair.

No wonder the birth rate is down – not a single swimmer do some of these pussies have.

Not late to this party, but too busy enjoying a real life out here in the hinterlands where my husband and I are now retired at 58 and 53 because once I went to work when my son was 9 years old, we pretended I didn’t and paid everything off. Got so used to that that we saved every dime and bought this land, then bought a log home kit on layaway for three years. Then we bugged out.

My son is getting his damned degree debt free (Electrical/Computer Engineering… the brat was supposed to invent a better solar power conversion system for me, but is overly interested in computers) and the chickesn are laying eggs daily now.

My Gen Xer cousin is going to Miami for Halloween and then to Colorado on a ski trip for Thanksgiving and her daughter (12) just got out of the hospital from crashing a dirt bike she wasn’t supposed to be riding when no one was home. Their part of the bill? $33K, but she says as long as she sends ten or twenty a month, no biggie.

I’ve got worms to dig for chickens.

Hey, Admin… if you aren’t too angry at the Sightseer to answer me this? I took some APIJ samples to a gathering last night and received the comment that there was too much coconut in the blend. (I use the coconut oil to carmelize the spices) What are your thoughts? Do you want your quart for forwarding emails?

Maggie

It’s too expensive to keep shipping things to me. You should save your money and enjoy the fruits of your labor.

And LLPOH? My hubs wears the brass ones in the family here. LOL… I just polish them once in a while.[img [/img]

[/img]

And get this… remember how my son got hit on his way back to college a few weeks back? Well, he was driving a POS 2001 Mazda he bought his senior year of High School for 2800 bucks and we’d intended it to last through college, when he would take over my 2009 vehicle and then I get something new.

Well, I explained blue book value to him and told him that it really wasn’t worth much… and FREAKING GUESS WHAT?

State Farm sent him a check for $2983 for the Total of the Mazda and will be contacting him about payment for his injuries.

The kid lives a charmed life, I’m telling you. He must be living right.

Maggie – brass ones are a state of mind, not gender related.

Glad you have done well. Your hubby has too.

Admin – do not forget acetinker. He called you a hypocrîte.

There you go. My bad.

Llpoh

How was that?

I’ve called the waaaaambulance for all the shitheads who forgot life was hard and bad things happen. And most of the bad things are due to their own actions. Whaaaa.

I’m still waiting for Warmongrel’s financial data. Is it possible he really didn’t want my advice and was just being a passive aggressive sarcastic bitch asshole?

Maybe he’s outside smoking and drinking.

We’ve gotten what we’ve rewarded – mindless consumption, high debt, and no savings. To reverse this, get rid of the income tax on married couples making less than $250,000, institute a national sales tax, and get rid of all taxes on investment gains.

When you’re talking free market system, you’re talking Pareto’s Law: 20% will always dominate 80% of the economy. And within this group, 4% will control 64%, and so on until you reach the .01% controlling 50%. The Law deviates a little, maybe 70-30, but it remains fairly constant. Human nature, is like gravity – arguing won’t change it.

The US has been a nation of consumers from day one, first with land, and from there expanding in form and taste by virtue of choice and availability. The 20th century, with the introduction of mass-media advertising and intrastate banking and credit, simply enabled the system to manipulate the masses all the more, such that by the early 1980s credit exploded, to became the third leg of a three-legged stool (two-worker households, longer work hours, and credit).

Nowadays, the work is gone, and with it the longer hours, and we’ve maxed out personal credit by encumbering the largest asset most people own, their home, and for youth, their earning power, via the home-equity and student loans.

Mindless, lumbering consumption isn’t going away on it’s on. Neither are those finding blame anywhere but where it belongs. Yes, we were sold an implicit bargain at the turn of the 19th century, mainly that of leaving rural areas where a person had many skills sets, in exchange for accepting one job with few skill sets in an urban environment and a lifetime of supposedly stable income.

That deal is long gone and yet Americans for the most part have been slow to grasp it. Now many find themselves with few or outdated skill sets, no job opportunities, and a mountain of debt. What else did they think was going to happen? Spending mindlessly isn’t a zero-sum game – it enriches one small side and impoverishes the many others: The money winds up in the hands of the few and the masses, by-and-large, end-up broke.

Who didn’t see this coming? The 80%, that’s who. And yes, there were a smaller number of the 80% that did, took action by avoiding mindless consumption, and still struggle. Regardless, the outcome was and is inevitable, and all that remains is to see it through to its logical (illogical?) conclusion: Collapse.

The limbering masses aren’t going to give up the absurd pursuit of crap and the system benefiting from the parasitic arrangement isn’t about to change, regardless of who runs the country. It’s simply sheer inertia.

“AP- Smoothest attempt to pick up a woman (The lovely TE) I have ever seen in a blog.”

———— BEA LEVER

BULLSHIT !!!!!

I got THREE WOMENZ (Avalon, HZK, and Marianne) to go on a DATE with me in NYC a couple weeks ago.

Beat That!!!!!

@Warmongerel,

Your situation is very workable and immediately upgradeable. I sure that divorce, alimony and child support took their toll but shit happens. Learn from it and move on.

My advice? Downsize your home as long as you won’t get raped doing so. Twelve hundred sq ft is a good size and should sell quickly (if you had to) in most markets to those who are downsizing their unaffordable McMansions. You and your daughter can easily get by with less than 1200 sq ft and it will be cheaper to heat, insure and maintain.

Cancel the lesser of your two credit cards. Pay off the other one ASAP as in yesterfuckingday! Regardless of how much your payment is, that payment will benefit you far more than the CC company.

I agree with PJ above regarding the 401k. Reduce contributions to the minimum required to get the match. Use the difference to pay off your credit card and any other debt except for the mortgage. Being cash rich in this economy is far better that having it tied in an inaccessible investment.

After that, build an emergency fund equal to a minimum of one months pay/expenses. That is an absolute minimum. An emergency fund equal to two to twelve months pay would be far better and should be a short/medium term priority.

Skip eating out for the benefit of your daughter. Instead, pick some of her favorite foods and make a day or weekend out of shopping for ingredients and teaching her how to prepare them with you at her side. Teach her how to make a birthday cake for mommy. Trust me, she will treasure the time spent with you teaching her things far more than a few minutes spent at McShits. You’ll both be happier too. Replace an “eating experience” with some other activity that keeps you and your daughter fully engaged with each other. Teach her to plant a garden or something. Maybe you could both take a karate, boxing or swimming class together. Go hiking, camping, hunting or fishing. Equip her with life skills and activities that will help her long after you’re gone. Teach her how to avoid the unfortunate divorce that you suffered.

I don’t know about you but when I was a kid (I’m 47), eating out was not a once of twice a month happening. It was a rare treat for the most part.

Drop the gigs. Drop the cigs. Drop the cigs. Drop the cigs. Drop the cigs. Drop the cigs. Oh yeah……..DROP THE FUCKING CIGS! Sixty extra dollars a months really puts a dent in a puny $2000 credit card debt. There are hidden costs to cigs as well like increased health, life and homeowners insurance premiums. Longer term expenses like high blood pressure, asthma and heart disease drugs that await you in addition to treatment costs. Plus it’s a nasty habit your daughter should see you avoid, not indulge in.

Once the credit card debt is gone, NEVER charge anything to it unless you already have the money on hand to pay it off.

Drop the booze until all debt is paid off. Think of it as a delayed reward for clearing the debt. Now you have $140 extra to put towards the debt! If $60 put a dent in the debt, $140 kicks its ass! You’re welcome!

Want to really kick the savings into high gear? Pretend your house is on fire……you have five minutes to save the most important things you own. Now sell everything else unless you use it daily, weekly or monthly or it can be used to earn an income like tools. You’ll be amazed what you can live without. Use the money to fund savings or eliminate debt. You didn’t mention a college fund for your daughter so get that started.

Snag a second, part time job to fund savings and pay down debt. I’ll bet many of your neighbors pay a lawn service to cut their grass. You could be the guy cutting a dozen lawns each week right in your own neighborhood. You could earn an amount in one day equal to the current value of your savings account. Probably more! Get your daughter involved and teach her the value of savings.

Without knowing more it’s hard to be more detailed but I’d bet there’s a cable/satellite bill that could be eliminated along with a cell phone bill. You’re old enough to know that billions of humans have lived full, meaningful lives on this planet without cell phones. If you have a true emergency and NEED a cell phone, you are surrounded by millions of sheep who could place a call for you or let you borrow theirs.

Stop flipping admin shit and spend that time stepping up your game. Besides improving your life, you have an example to set for your daughter. Teach her what you learn and maybe she can avoid your mistakes.

Admin… excellent work. I visited with an aunt last night and she told me that one of my cousins’ divorce was caused by the husband’s constant insults about her intellect. (Not her child, so we both cracked up because this particular cousin is a booksmart idiot.)

The husband told her “My mother holds a better conversation than you and the only thing she reads are the jokes in Readers Digest.”

I love my aunt, widow of my uncle whose business was downscaled due to his workers suing for backpay for overtime. Which he paid, then closed down his business and turned it over to his son.

Warmongerel called you out too admin. Sick ’em! 🙂

Admin – very nice indeed. Very very nice. These newbies really have no idea. Old dogs that survived here were forged in the fires of hell. I long for another “should have ducked” or “thumb ring” or “OWS” thread. We beat on each other for days. And the differences between us could be measured in microns.

These newbies have it too easy. They cut and run at one “get fucked”. Bah humbug.

I kinda like Warmongerel. I just read a short article on his site called Do-it Yourself Deportation. I’ve the exact same opinion for years with just a couple sadistic tweaks.

@IS… this is what I tell people about how it is done.

All you really need is Enough. And Enough is a hell of a lot less than most people think it is.

Maggie, I just wish I’d learnt that about twenty years earlier. I might be alongside llpoh building my doomstead right now instead of still slogging away. Better late than never no longer applies because this world is a powder keg and even at 47, I certain that collapse and recovery will consume the majority of my remaining days.

Admin – Epic

@Llpoh

On your response to Karalan and marriage (back a-ways, up the posts)…AMEN, brother!

Marriage and family are collectively the toughest institution in America, and as the Navy used to advertise, “It’s the toughest job you’ll ever love.”

And any guy that doesn’t quit his job at least once a day isn’t really being tried…it IS hard out there, but as they saying goes, “Once you commit, you don’t quit.” Too many people have their head up their point-of-contact; get married and have a family? It ain’t about “YOU” anymore. Period.

That’s the deal, so don’t enter it lightly and don’t treat procreation or the possibility of it like a game. I’m beyond fed up with the whining crap that comes out of peoples mouths over, “sacrificing my life away,” etc. Of course you are! Who the Hell isn’t? It goes with the landscape, pal. You signed on, you’re in for the duration, or at least as long as it takes to get your kids self-supporting and competent to enter the world. No one walks away from that.

If you’re going to be stupid, you had best be tough, and the more stupid you are, the tougher you better be.

Okay, but what about the coconut oil complaint… whatcha think?

I love coconut oil. I put a tablespoon in my coffee every morning and we use it to cook.

Is my newest marketing idea… my son and other friends have convinced me to pressure can it and sell it. Putting it in a Redneck Wineglass…

[img [/img]

[/img]

Stucky- You are the one blathering BULLSHIT!!!

Them womenz was on a date in NYC WITH their husbands not you, does not count. Even you have to admit AP was delivering a smooth line to TE……..the boy is talented.

I’ll take that as an “ignore” on the complaint… LOL Some people just gotta bitch about something.

I see you hit “target” on your donation clock. Congrats. Glad to see it.

Coconut oil!?!

I eat a straight, heaping tablespoon every AM.

It’ll cure what ails ya.

BEA LEVER

Blow me.

First of all, TE is MY girlfriend. AP’s attempt at hitting that was meager, pathetic, and definitely not sponge-worthy.

Secondly, all three gals in NYC gave me their private cell phone numbers when their husbands weren’t looking.

So, again, blow me. You got nothin’.

” …. the comment that there was too much coconut in the blend” —– Maggie

Tell those folks to go suck ass. “No coconut oil for you, one year!!”

One of the wonderful aspects of coconut oil is that it has NO TASTE …. unlike Olive Oil which imparts its “nutty” flavor to foods. I just went to the cupboard, and tasted a full tablespoon of coconut oil. Yup …. NO taste whatsoever.

As the owner of a small painting company for the last 25 yrs, I learned some pretty hard lessons. Thank God I learned most of the deal breakers in the first couple of yrs.

Here are just a few I learned:

Stay flexible.

Keep your overhead low.

Debt limits your options

Exercise Humility.

Exercise Patience.

If you are not worried of failing, you are not paying attention.

Being flush with cash means you need to be extra cautious, and pay closer attention. i’v managed to resist the easy money, and keep my business relatively debt free

I’m Married, 51 yrs old, and we still don’t have any retirement savings to speak of. But we also don’t have any debt either. we own 2 homes outright , one is a small 5 acre hobby farm in a very desirable area of our state, . We don’t do vehicle payments, credit cards, or vacations, our vacations are spent at the farm. We live pretty conservatively. But that’s what is required in today’s world if you don’t want to be a slave. You have to adopt a personal preservation attitude.. while everybody else is driving around in new cars, we get around in 10 yr old vehicles, bought with cash. We buy our clothes at goodwill and other secondhand stores, we also grow a garden and raise chickens to supplement our grocery bill.

On the plus side of all this frugality when appliances go out, we can replace them outright, when we needed new roofs on both houses, we payed cash for them. My wife wanted solid hardwood floors in the house, and we were able to pay for those outright. But we cant have it both ways and expect a positive outcome….we cant support ourselves, and carry debt at the same time. It’s just not worth the stress, and struggle.

Back table wrote this and I am repeating it:

“That’s the deal, so don’t enter it lightly and don’t treat procreation or the possibility of it like a game. I’m beyond fed up with the whining crap that comes out of peoples mouths over, “sacrificing my life away,” etc. Of course you are! Who the Hell isn’t? It goes with the landscape, pal. You signed on, you’re in for the duration, or at least as long as it takes to get your kids self-supporting and competent to enter the world. No one walks away from that.”

A – freakin – men. Life with another functioning independent human being is hard some times. Deal with it – it’s no longer about you.

http://dictionary.reference.com/browse/compromise

Learn it breath it live it.

Lots of couples splitting around us. It’s mostly woman issues. She is bored and lacking “romance” and eventually ends up with a new boyfriend who has a nice car and will by her a new set of tits. I’m blown away at what people will sacrifice for a new set of melons. Mind boggling. Humanity in the west has become shallow, narcissistic and unable to cope with reality. No wonder our countries are so screwed up politically and fiscally – they just mirror the ethos of the population as a whole.

First, The main theme of this article is silly. No body bothers with savings accounts any more. With interest rates were they are almost everyone just uses checking accounts and mutual funds

Second, the language used in many of the comments herein is disgraceful, and shows a level of stupidity that makes me fear for our country’s future.

This will be my last comment on this site. I don’t want to be associated with such idiots.

Chuck Griffiths

Blow me. If you can’t distinguish between the concept of savings and a savings account, we don’t want you on this site.

There sure are a lot of dumbasses in this world.

Yeah, acetinker, take that. It ain’t the university of phoenix. Donald trump graduated from here. He’s gonna be our next president!

starfcker after fucking with admin.

Admin after slaying all the dumbasses, shitheads, pussies, and idiots on this thread.

The only thing “silly” about this article is the fact we have to discuss this topic at all.

In fact, I’ll pose a simple question wherein embedded lies the ludicrous answer: Why are Savings Accounts no longer a viable investment tool?

Chuck

wow you have managed to destroy the premise with the smite of your great sword of knowledge……

What a childish comment.

anyhoo…

Chuck has left we can all come out and play again………………..

Lipoh, are you aware that men in family court have fewer rights than a serf in pre-Magna Carta England? That’s human rights circa 1215 AD which have been stripped from the citizenry. No matter how ‘aware’ one might be, the reality is something that only sinks in once you’ve been there. You think the TSA, NSA, and all the other bureaucratic human rights abusers etc. are a problem? Family court was there long before any of them, gave them the model, showed them just what they can get away with.

Stop trashing people for being black, husbands, small businessmen, etc. These are almost all good people who want to be allies in the fight for freedom, and who are not universal losers and whiners. Stop hating men who don’t make it to the 1% or who fuck up a little now and then.

Call me lazy, call me a chauvinist. I don’t care. But when my junk needs licking, I’m no do it yourselfer. Around here, that’s womens work

UpChuck Griffith needs to go visit Finnegan’s Wakeup call.

Star- I’ll bet you a Benjamin that you can’t hike your leg back behind your head while you are “Romancing the Stones” like Admin in the above photo.

That alone tells me you are not even close to Admin’s level in the jungle. Give up while you can still save face.

Bea

I owe it all to my daily yoga routine.

Hey “Administrator”,

Over the years I have read your articles from time to time, and you have now sunk to join the ranks of so many others also observed, since about 2005, coming full-circle to embrace the Stockholm Syndrome: Blame the Loser. Never mind that this “conclusion” is roundly contradicted by your own prior evidence (Thank You!), namely: how Wall Street unjustly and illegally destroyed and continues to parasitize the USeconomy – both in terms of real production as well as wages.

The fact is your current statistics about outcomes prove nothing about causality. Al Gore would be proud of your “logic”. If a losing position alone proves fault, then you could equally argue that Japan deserved to be atom-bombed, Dresden deserved to be carpet-bombed and the Slavs and Jews deserved to be gassed.

Instead of speciously picking which personal anecdotes you do and don’t approve of, as representative (now with absolutely no statistics to back it up), why don’t you show us a plot Wall Street and CIty of London gains versus consumer losses in real weath? You will find a direct correlation – strong presumptive evidence for systematic theft, particularly when all the known criminality and gaming the system is factored in. You can start from the repeal of Glass-Steagall. Or from the “Too BIg To Fail” pronouncements from the President of the United States of America. (Or indeed, from anytime since the Trilaterall Commission’s declaration of the “crisis of too much democracy” in the West.) Consumers don’t just lose their money down some black hole, somewhere – that money GOES TO SOMEONE.

Or would you sink yet further, to say Wall Street’s obscene concentration of wealth only proves the parasitic top 0.1% have been the more admirable, disciplined and natural winners of some (mythical) free market? Because, again, this is the (flip side of the) logic inherent in your present conclusion – and again, starkly at odds with your very own, prior reporting – as you now are delivering to Wall Street their favorite PR wet dream: the pitting of commoners against each other, neighbors blaming each other. And again, you are not the only one, but now a depressing encore of such blogs, seen repeatedly since circa the mid-‘oughties.

And just look how much good they did.

The self-proclaimed “Masters of the Universe”, their machinations self-described as “Doing God’s Work”, are no doubt gratified by your present role as useful idiot, in their service. And it doesn’t even take an idiot to realize that, if Americans do manage to save more, Wall Street will simply (continue to) increase their gaming of the system to cheat everyone out of those savings, as well.

No, it is you who are the Pussy – having failed to see any effective change, since your first posts – now resorting in frustration (or worse), to beating your own peers for their collective problems.

If you want to criticize entire populations, and generations, of Americans for fucking up – and have any hope of contributing anything positive – then beat on us for continuing to shrink from revolution (whose ultimate cost will only continue to rise), in the face of such outright economic warfare, as is being continually and increasingly waged against us.

I therefore challenge you: what – all together, at the end of the day – is your aim? To educate and empower your readers? Or simply to show one and all how to boil, like an enraged frog – and meantime to hell with your neighbors, let The Devil take the Hindmost – from you “Burning Platform”?

Time to Get Real or STFU.

Semper Fi,

– Matty in FL

Just came in from checking on the new litter of piglets. Mmmmm bacon in just six months.

As an aside to the general thrust of this piece, why is it that so many people on the Interwebs feel the need to tell you that they will not be coming back when they were never really here in the first place? Do they do this at department stores? “Your selection of casual wear is appalling, I will definitely NOT be returning to Aeropostale again. Good day, sir.”

It’s odd.

Hope everyone is having a swell afternoon.

Mmmmm Bacon

HSF… excellent point!

“Hello, I am announcing my grand presence here and letting you all know that I have graced this blog with my attention span of a flea for several microseconds and have come to the conclusion that it is not worthy of my time. I shall not return!!!!”

Matty – as a service I will attempt to gently pry you from your position before the angry Pit Bulls (namely Admin and llpoh) rip you a new and superfluous poop shoot.

If yo have really been reading this site for years, you would know that Admin rages against the evils of Wall Street more than virtually anyone.

The bigger issue of course, is that you–as a member of this victim, “poor me” culture–take Admin’s adamant stand on personal accountability and turn it into “blaming the loser.”

As George Carlin once so succinctly pointed out: words matter….the way we say things matter. Calling this article and discussion “blaming the victims” is exactly how our rulers garner and grow their power. If we hold ourselves as victims, they can present themselves as saviors, and we are all damned. If we hold ourselves accountable, they become unnecessary and lose their power. The choice is really ours and so is the power. It is you and your type that gives it to them.

[img [/img]

[/img]

No bacon discussion is complete without this:

I think we know which side most TBPers come down on.

@ starfkr

Your last comment made me chuckle.

+1 for having your big boy panties on. Or off… whichever the case may be at this moment 🙂

To the newbies here. If you don’t have a thick skin you won’t last. Nobody is here to pat you on the back or reinforce your appeal for victim status because you got caught up in shit that seemed beyond your control. The key here is to look inward, address your faults, admit your mistakes and take responsibility for your lives good or bad.

Anyone who was around in the early 80’s when interest rates hit 20% should know that when it comes to money, banking and things that seem too good to be true (like housing values going up year after year) that you should exercise caution. It’s not stockholm syndrom to take responsibility for yourself when you KNOW the system is a fraud. And its been that way for an awfully long time (2008 was really just one of a series of shit storms brought on by central planning and fraud).

I have nothing to say to the guys who are going through divorce hell. Maybe stick to whores. They’re cheaper and there’s no commitment.

@ Jim. Not going to disagree with anything you have to say here – LL wrote a good piece and he’s right. If you play the game without a bit of suspicion or caution knowing what you know about the world then you need your head checked. But you might catch more of the stragglers if you took more of a mentorship role than an ass kicking roll. Not that’s it your responsibility to do so if you choose not to but you have a lot of knowledge that would spread a lot more widely with less anger in response to the ‘victims’ posts here. What I’m delicately trying to tell you is your people skills suck. Other than that carry on brother.

It’s not my job to mentor “victims”. I’m not changing my style for anyone. I present the data. I present my point of view. You can take it or leave it. It’s not my fucking problem.

On any other site, those who criticized my point of view would be banned. Their comments would disappear. Not one person has been banned. Every comment is there to be seen. This site is designed to be a free for all.

I don’t give a fuck about people skills. If people don’t want to hear the truth, hit the fucking road.