Submitted by Charles Hugh-Smith of OfTwoMinds blog,

If the four structural trends highlighted below don’t reverse, the middle class is heading for extinction.

Everyone knows the middle class is fading fast. I’ve covered this issue in depth for years, for example: Honey, I Shrunk the Middle Class: Perhaps 1/3 of Households Qualify (December 28, 2015) and What Does It Take To Be Middle Class? (December 5, 2013)

This raises an obvious question: what killed the middle class? While many commentators try to identify one killer cause (for example, the U.S. going off the gold standard in 1971), the die-off of the middle class is more akin to the die-off in honey bees, which is the result of the interaction of multiple causes (factors that increase the toxic load dumped on bees and other pollinators by modern agriculture).

Longtime collaborator Gordon T. Long and I discuss the decline of the middle class and other key topics in a new 29-minute video How did that work out for you?

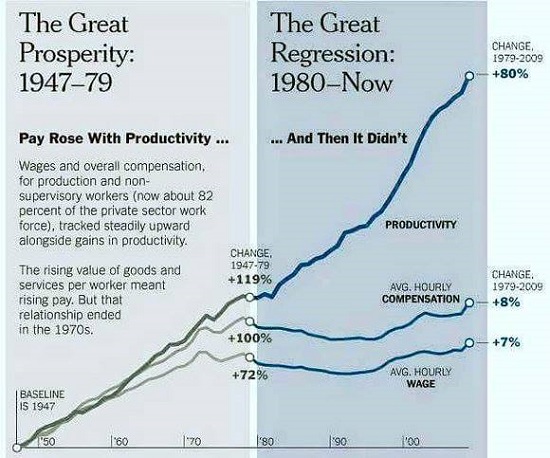

So where do we begin this detective story? With the engine of all real prosperity, productivity. This chart reveals that wages stopped rising with productivity around 1980.

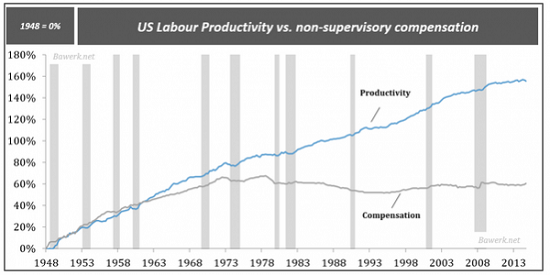

Here’s another look at the same phenomenon:

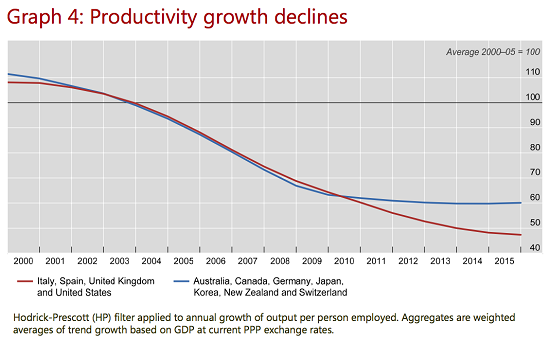

Productivity has been slipping since around 2003: Alan Greenspan:”Productivity is Dead”

Cause #1: declining productivity, which means the pie of real wealth is no longer expanding.

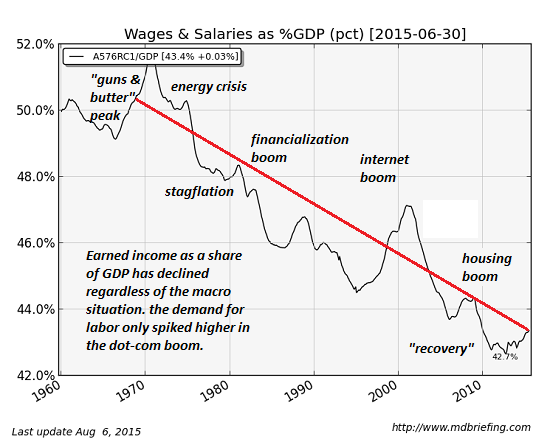

Exhibit #2: middle class wage earners have not received any of the gains. Wages as a percentage of GDP have been falling for decades, with occasional blips up in tech/housing bubbles:

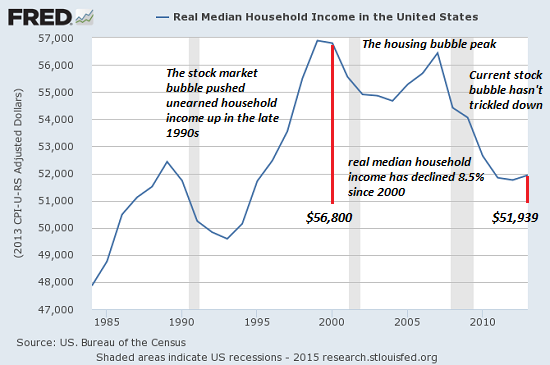

Inflation-adjusted household income has dropped back to levels first reached in the 1980s:

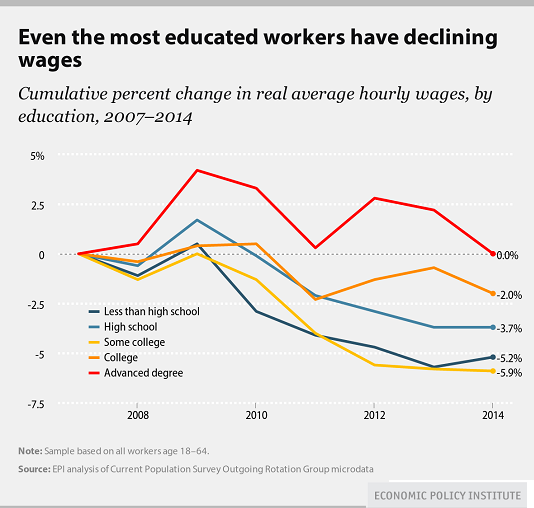

More recently, wages have actually declined, regardless of educational attainment:

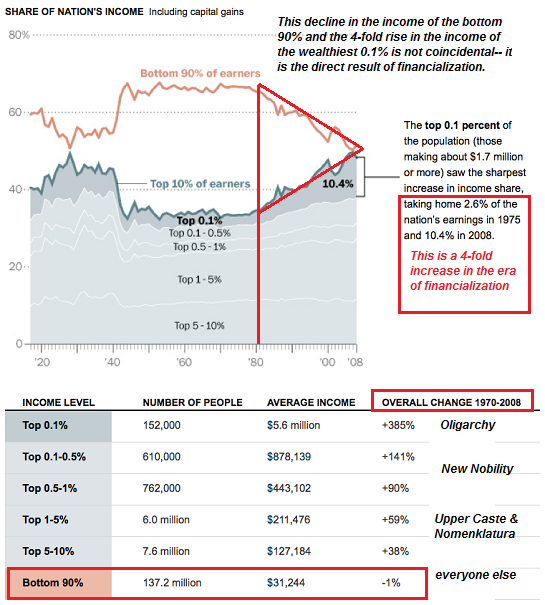

Income gains have all flowed to the top 10%, with most of the gains being concentrated in the top 5% and top 1%:

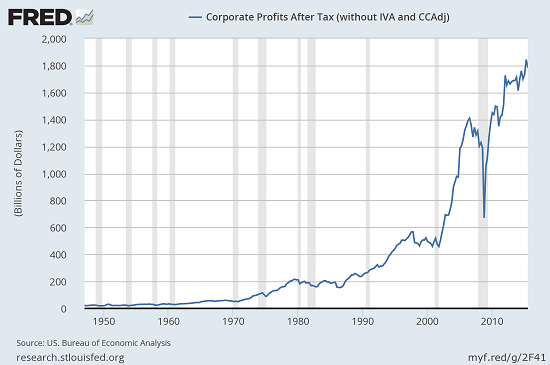

If the middle class didn’t receive any of the gains, who did? Corporate profits have soared to unprecedented levels:

Cause #2: all the gains in the economy have flowed to corporations and the top 10% of financiers, managers and technocrats.

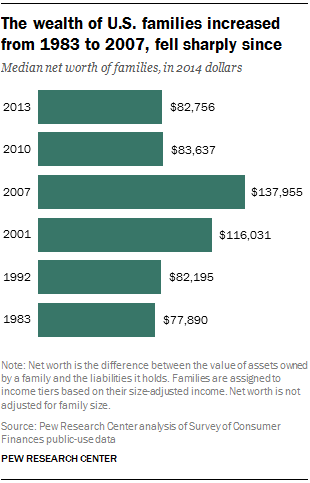

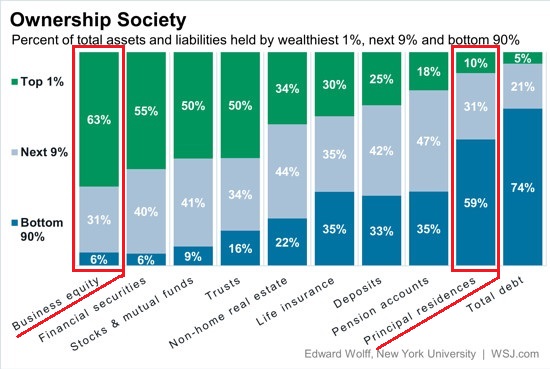

But wait a minute–hasn’t the rising stock market enriched the middle class? Short answer: no. Middle class household wealth has absolutely cratered since the top of the housing bubble in 2007, and hasn’t recovered.

Why? Middle class wealth is based not in stocks but in the family home. The middle class does not own enough financial assets to have participated in the latest stock market bubble, while the majority did not recover the wealth lost in the housing bubble bust. This is the cost of allowing the financial sector to financialize housing and mortgages in the 2000s.

Cause #3: the middle class doesn’t own the “right” assets to benefit from systemic financialization and financial speculation.

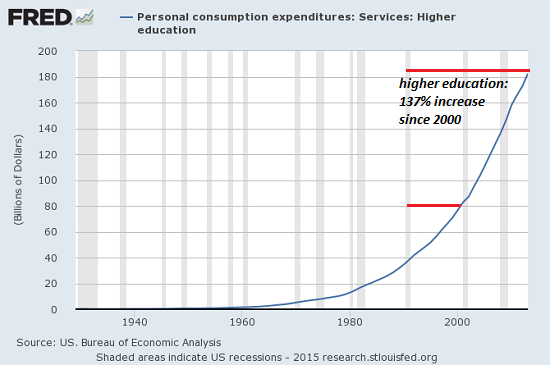

How about rising costs? The federal agencies tasked with measuring inflation assure us inflation is near-zero. But these measures underweight big-ticket costs like healthcare and higher education, where costs have exploded higher, greatly increasing the burden on the middle class:

Cause #4: soaring costs of big-ticket expenses such as higher education and healthcare. Saving $10 on cheap jeans imported from Asia does not make up for 135% jumps in tuition and college fees, and $100 decline in the cost of a laptop computer does not make up for healthcare insurance and out-of-pocket expenses in the tens of thousands of dollars per household.

Correspondent Kevin K. submitted this article and accompanying note: Colleges with the biggest tuition hikes (my ala mater University of Hawaii-Manoa clocked in with an increase of 137% since 2004.)

“It looks like the article linked above didn’t do much research since:

University of California Davis

2004 in-state tuition $5,684

2015 in state tuition $13,951

Percentage increase 145.44 percent”

There is no way middle class households with declining real incomes can pay soaring costs imposed by state-enforced cartels and gain ground financially. If the four structural trends highlighted above don’t reverse, the middle class is heading for extinction, the victim of financialization, the glorification of financial speculation via central bank-central state policies, the decline of productivity and rising costs imposed by state-enforced cartels.

The Vampire Squid sucked the blood out of the Goy and the brains out of the Liberals.

The middle class will not become extinct, it will be mostly Government wage recipients. Remember non productive employment pays better than productive work and Government produces nothing but barriers to productive work.

Remember Obama voter Obama Is Going To Pay For My Gas And Mortgage!!!

Uploaded on Oct 31, 2008

This lady, Peggy Joseph, thinks Barack Obama will pay for her gas, mortgage, and who knows what else.

This is good but doesn’t really address the cause. I’d say maybe offshoring of jobs, illegal immigration and too much immigration, NAFTA, CAFTA.

The first graph was exactly what happened in the meat packing industry. Stagnation after 1982. KaD hit the nail on the head with reasons at 5:57. Working people have been sold out by politicians who put government favoritism up for bid.

Strip-mined of all wealth, well at least the set up is nearly complete, the mother load is within sight. Very few ‘middlers’ own anything,illiquidity will finalize the title transfer of almost all assets. Americans have no savings or staying power, all title will transfer to the source(DTC) as the papers burns at all levels, personal, city, state, and federal.

The scene will be ripe for Globalist Colonization, possessing title via DTC, sweeping the dollar off to the dust bin, coronation of 3rd world status. No middle class. Yea!!

Thanks for posting, Smith and Long are long time favorites, this was an excellent article,with the kind of graphic support that makes one wonder….WTF.

KaD, right on. I always wonder when someone like CHS, who has been around a long time, and doesn’t seem stupid, writes a bunch of Okey doke gobbledygook like this. What happened? Sold out. Had to. I can’t believe for one second he thinks this is true. Hey charles, fuck you, traitor. This sort of work might have slid by ten years ago.

The death of the American middle class began in the 70s, when our manufacturing began to move offshore at the same time our domestic supplies of cheap, plentiful, easy-to-extract resources began to dwindle, making us dependent upon foreign sources.

The only way to “work around” these two conditions was to “financialize” our economy, and start racking up debt in an effort to maintain the lifestyles to which we had become accustomed, but could no longer afford.

Debt creation enabled us to tell ourselves lies about our true financial condition, and the condition of our economy. Thus, not only did we maintain our extravagant, wasteful lifestyles by pulling out the plastic, we doubled down and decided to party like there was no tomorrow. We vastly expanded our lifestyles, as witness the massive increase in the size of the typical new suburban home, and the increase in the number of cars owned per household. The typical modest 3-bed ranch house of the 50s became an anachronism, replaced by a 2,500 sq ft center hall colonial- AS A STARTER HOUSE! You saw blue-collar workers here in the Chicago suburbs, who bought 3500 sq foot houses with spa tubs and 4 bathrooms, a Ford F-350 and a new Honda Accord plus a boat in the driveway, while welfare recipients paying their rent with Section 8 vouchers consider a place with 2 baths and a dishwasher to be a birthright.

Now we confront the biggest economic shift since the last industrial revolution, with a population acclimated to an insane level of luxury while dealing with the inevitable deflation of wages in the wake of increasing automation and resource depletion.. and swelling hordes of employment-age people who have no hopes of getting a job that will pay back the money they borrowed to obtain mostly-useless degrees, but who have extremely elevated expectations from the debt-driven consumer extravaganza of the past 35 years. You can bet that the slide downhill back to reality is going to burn the backside.

You get an idea of about how well people are going to deal from the increasing number of murder-suicides, where one or the other of family ices all his kids and then turns the gun on himself, and it is always the last person you’d expect to do this. You may have read about the tragic event in Louisville, KY, a few days ago, in which a young father killed his wife, his kids, and himself, after setting his house on fire. He had been a very nice guy with a nice job at Humana, a practicing Catholic, a good neighbor. He was only 33 years old but suffered from PTSD. Well, I took one look at the huge, extravagant house he and his family were living in, and felt like I knew what the last straw on the camel’s back was- this guy was staring down a catastrophic financial situation. I expect to hear of many more tragedies just like this as we head further down the slope.

Llpoh would say, and I agree, the middle class was a mirage and never sustainable.

The middle class sure as hell is not sustainable when it tries to live like it’s upper-class, on borrowed money. That is the easiest way in the world to end up living in your car… if it doesn’t get repo’d.

We could have sustained the modest luxury of the 50s, especially with the tech advances of the past 30 years. I remember how life was then for most lower-middle class people- by the way, 80% of the population is lower-middle-class or lower. The broad “middle class” of truck drivers, factory workers, secretaries, and such, has always been lower-middle, and in the past, they were sensible and realistic, and knew where they stood.

It was understood, for example, that most people could not afford 2000 sq ft suburban houses with all the luxury trimmings, or two newer cars, or luxury vacations, or meals out every other night, or expensive designer hand-bags and 30 pairs of shoes, or speedboats and jet skis. It was accepted that only rich folks could afford housekeepers and second homes, and very few rich people had more than one servant, and that part time. My grandparents were quite prosperous and very high in the middle class, and would have been considered to be wanton show-offs if they’d employed a maid. They lived in a modest 3-bed Cape Cod house, which they could not buy until they were nearly 40 years old.

We just might have to adjust our ideas about what constitutes “middle class”, and a number of people are doing that now, unloading their big houses and divesting themselves of tons of possessions to move into tiny houses, unloading tons of stress and simplifying their lives as they do.

Great post, chicago. And great defense of the middle class. That middle class wasn’t a mirage.

Yes, great posts Chicago. To add a mere observation, the term Homeowner has been perverted beyond recognition. Actually owning the home is not even on most radars these days.

The root of the problem is actually very simple but very few people understand it. The bankers like it that way. The whole financial system is based on a simple underlying fraud. What almost everyone considers a dollar is really just a federal reserve note. FRN. Or as I like to call a Fedbuck. The real dollar is a silver coin weighting about an ounce. That fraud allows the bankers and their associates to strip mine the wealth of the nation.

“The real dollar is a silver coin weighting about an ounce.”

True, it’s a 90% silver alloy coin that contains about .77 ozt. of silver. The last year they were struck for circulation was 1935.

Ottomatik: Can you believe there is such a thing as an INTEREST ONLY home loan? Yes, you pay ONLY the interest! What the actual fuck! http://www.thetruthaboutmortgage.com/interest-only-home-loans/

KaD

The interest-only portion lasts a maximum of 10 years, then principal is included for the remainder of the mortgage. One reason people choose that loan is because the initial interest payment is lower than a full payment (duh!) … which means it’s easier to qualify for the mortgage.

It’s not THAT bad of an option … for the right buyer. For one thing, it’s a fact that most mortgages die after 7 years, either because of a refinance or selling the home. Also, VERY LITTLE principal is paid in the first 10 years anyway. On a 30 year mortgage at 6%, it take 22 YEARS to reach the half-way point.

KaD, I can’t believe that interest-only loans are actually coming back. Shows you how desperate our bankster-class is for more suckers to pay re-inflated prices for their remaining foreclosure inventory from the 00s, of which there is still a lot…. and it also shows you that they have complete faith that they will be bailed out of their malfeasance and risk taking by the taxpayers just as they were after the bust of ’08.

I was introduced to these loans in the 00s, and was flabbergasted that they existed. When the loan begins to amortize and the principal comes due, the borrower gets back-loaded with an immense balloon payment. The idea is, supposedly, that the house will inflate in value enough for the borrower to refi into a conventional fixed loan, or sell the place, but it didn’t work that way for hundreds of thousands of sucker borrowers in the 00s, who found themselves facing humongous balloon payments at just the moment their houses started dropping drastically in value.

The most diabolical loan, though, is the “pick-a-pay” or “pay option” loan that enables the sucker to defer both interest and principal. The borrower saps of course usually elected to make the very minimum payment permitted, which meant that both unpaid principal AND interest accumulated, with the result that, a few years later, the loan balance had swelled considerably over the original amount. That was always a big surprise to the borrowers, who somehow imagined that they would be able to make super low payments against monster loans forever. Remember those ads you used to see on Yahoo’s site, that said get, say a $700,000 mortgage with a $798 payment?

People will still fall for these dishonest gimmicks, but not in the numbers they did a decade ago. The memory of the bust and the millions of ruined home buyers is still too fresh in the minds of many, including the minds of youngsters laboring under a pile of college debt. But you never know when the population may fall prey to another spate of hysteria, given the numbers of people who’ve bought cars that cost more than their yearly incomes with 8-year loans.

As usual, you can totally bet on the stupidity and gullibility of the general population.

Chicago999444 says: You may have read about the tragic event in Louisville, KY, a few days ago, in which a young father killed his wife, his kids, and himself, after setting his house on fire. He …. was staring down a catastrophic financial situation.

Why is it always the male who freaks out at the idea of losing everything due to debt? They get this dumb idea that defaulting on debt is a sign of weakness, it’s a threat to their ego and manhood. However, suicide is a coward’s way out.

Chicago is quite right. I disagree that modest luxury could have been sustainable, and would have said frugal comfort, but generally we are in agreement there.

Debt certainly played a part – the US has lived as much as 200 trillion above its means. That is, total debt is often quoted around that figure. That is around 13 years of current GDP, and was incurred over about 40 years. Simple math thus tells us the US is, and has been living, around 50% above its real, sustainable level. Real lifestyle/expenditures should have been about 2/3 what was actual spent.

And so the ability to live in frugal comfort will no longer be possible. You see, it is now impossible to pay off the debt. Even at low interest rates, say paying the debt off over say 50 years would require a yearly outlay of around 5 trillion dollars, or 1/3 of GDP. Subtract taxes from that, etc., and frugal comfort is no longer possible. Perhaps moderate poverty can be obtained as a lifestyle for most.

Again, the best illustration I know is that the US gas about 5% of the world’s population, yet consumes 25% of its resources. That is obviously an unsustainable position. It simply cannot work. The only way it us possible even in the short run is by the subjugation/enslavement of much of the rest of the world. Any guesses why the US is involved in so many foreign conflicts?

My guess is standards of living in the US will need to fall to about 50% of its all time high. Even that may not be sustainable.

The middle class, with low skills, modest to poor education levels, a sense of entitlement, and poor work ethic, is going to get wiped out. And the poor – well, the welfare state is doomed.

It is going to get very ugly indeed.

The debt was never possible to pay off. It’s all part of the financial scam. When banks create money out of thin air, the don’t create enough money to pay off the debt and interest. As such, the debt in the system always increases until the system fails and resets.

https://www.youtube.com/watch?v=fpkPon9A1Vo

“On a 30 year mortgage at 6%, it take 22 YEARS to reach the half-way point.”

Yep. In ’98 when my wife and I bought our place,which we intended to be our final land/house purchase, we took out a 15 year note at 6.25%.

When rates dropped,5 years later, we rolled it into a 10 year note at 4%. I think we saved about 80% of the total we would have paid in interest with a 30 year note.

WHAT KILLED THE MIDDLE CLASS?

There are many reasons. Here are the 3 most important, I believe.

1) Jobs, the lack of and the low quality in terms of pay. Pay not keeping up with the rate of inflation.

2) Debt, the taking on of debt to increase their standard of living and to maintain their standard of living.

3) Inflation, probably the most important of the 3. Inflation in wages and prices provides a flow of revenue to the central government at a cost to the middle class. Inflation allows the government to pay down the debt, now at 19 trillion bucks, over time. But, the needs of government for revenue is increasingly destroying the middle class. The middle class is where the money is and it is systematically being looted. More draconian method are being used to extract more wealth from the middle class to support a bloated, inefficient, and self centered organism. The parasite is killing the host.

You know what, Ilpoh?

Most people in the U.S. could reduce their consumption by 50% and still have the basic comforts AND some amenity. Witness the incredible growth in off-site storage lockers, which people are renting just to stash superfluous consumer goods they never even look at and would be better off getting rid of. Let me tell you that a person could LIVE on what most ordinary people in this country dispose of. I have picked up beautiful, well-made furniture for 10c on the dollar, from people whose houses were bursting at the seams with desirable consumer goods, but were going on broke. I buy about 75% of my clothing from consignment houses. And I STILL find stuff in my own home that has to be disposed of to keep the place from becoming cluttered.

I like to help people “find” money in their regular monthly income, that they are currently letting dribble away on pure waste- i.e. things they didn’t even realize they were spending money on. The first thing I do is have them blot out their ss and bank account numbers on their bank statements, and let me look, and then I go through highlighting the things that are sheer waste. Not extravagance, just plain waste, because they got nothing in return for their money. The first things I highlight are “alien” ATM fees, where a person got money out of an ATM not related to his bank. You get wacked $2.75 to $5 per transaction for that little convenience because you will not be bothered to stop at your own bank’s ATM machine. Then, things like late fees and insurance for your credit cards.

THEN, I go after extravagances that people feel they “need” but get no good out of, like 100 channels of cable, $6 lattes at the Starbucks or Metropolis, $12 lunches at work, cash withdrawals for $20-$40 for “walking around” money that got spent on magazines, fast food, and other little incidentals that add up to big waste over time. Then, twice-weekly meals at restaurants- who really can afford that.

Then the BIG extravagances. Do you really need 2 cars? Do you need 2 cars that cost $40K each? Do you need a 9-room house when you spend all your time in the great room and literally never enter the formal living or dining room? How much money would you save by buying a 6 room house closer to work, where you don’t have a 60-mile-each-direction commute? Why are you running the C/A for a $200 per month power bill when you are only occupying one room at a time? Are these things even making you more comfortable? Chances are, these large extravagances are not only making people broke, but are making their lives more complicated and cumbersome.

In my salad days, I used to fantasize about living in a grand vintage co-op here in Chicago with 6000 sq ft of herringbone parquet floors and 4 fireplaces and a 30′ long living room replete with fine French furniture and a garage attendant to bring my car to me on demand. Designer clothes custom-tailored and regular jaunts to the spa. These days, I don’t. I can’t think what I’d do with that much space now. I don’t want to be bothered with things that cost me more in time and trouble than they give me back in productivity and pleasure. I have no car, and my condo is a modest, inexpensive, but beautiful vintage in a distinctly un-trendy neighborhood. I want only the space I can actually use, which is 1200 sq ft or so,and I realize that I could do with much less than I have and still be very well off. By the standards of middle class American suburbanites hooked on consumerism, my lifestyle is modest, but it feels like more than enough to me.

Most Americans would benefit greatly from reducing their lifestyles. They would surely take no loss in comfort and amenity, and would greatly reduce their stress while saving money.

Chicago – I hear you. That is why I said frugal comfort. That was always attainable. And is at the moment, if individual folks do as you suggest. But when very thing goes tits up entirely, I think frugal comfort will be difficult to obtain. There will be no cast offs, etc, to take advantage of.

And of course the debt remains to be paid, which is impossible of course. Walk away bankruptcy us the only option.

Llpoh

What are all of these articles I keep seeing about tumbleweed in the outback? Are you up to your arse in weed or what?

Some articles say it is poisonous? WTF ?

Bea – I think it is called spinifex or some such. It rolls around, and gathers against fences, houses, etc.in huge quantities.

Australia has more stuff that can kill you than any other place on earth. Something like 21 or 22 of the 25 most poisonous snakes on earth are here. I had a five foot red belly black snake curled up in front of my front door recently. Motherfucker! It is like number 10. For comparison the rattler is around 25, barely cracking the list.

There are sea shells, tiny octupuses, several spiders (fucking funnel webs and red backs especially, of which I am surrounded), rock and scorpion fish, jellyfish, crocodiles, sharks, insects, etc. that are deadly in Australia. Some of the damn ants are about the size of small dogs and leave nasty pus fled welts when they bite you, some eagle sized flies will draw blood, the scorpions are all over, and I have heard there are some nasty frigging millipedes as well.

So I would be surprised if the damn tumbleweed is not poisonous. Every other damn thing seems to be.

Dang Llpoh and we thought we were having a hard time with feral kneegrows here in the good ole USSA.

Take care not to step on anything that will jump out and git ya !!

Video of reporter bit by bull ant on live TV. Very funny. They get to about 1 1/2 inches long.

https://m.youtube.com/watch?v=tJWLGahOwGM

I googled those Australian bull ants, and they alone are enough to keep me out of that place. I’ll take the gangs of Chicago anytime.

But they’re a minor nuisance compared to the Army ants of tropical South America. Those are the stuff of horror stories. They’re big suckers, an inch long or more, and carnivorous. When they migrate, they move together in a straight column of 100,000 or so individuals and literally eat anything in their path, including animals. They can overwhelm an animal much larger than they are and reduce it to a skeleton in a half hour. If your house is in their path, you just have to move yourself and your animals to safety quickly, far out of their path.