Guest Post by Peter Schiff

Just over a week ago, President Trump delivered the State of the Union speech. The president gave a speech with a decidedly optimistic tone. This was certainly welcome with the increasingly fractured and divided American political landscape. But it’s important to focus beyond the political theater and take a hard look at where the US economy really is and where it is heading. Unfortunately, the political rhetoric doesn’t always line up with economic reality.

As Peter Schiff has said on numerous occasions, President Trump has taken full ownership of the current bubble economy. In doing so, he’s setting himself up as the fall-guy when things turn sour. Peter put it in pretty stark terms during an interview with Stock Pulse at the Vancouver Resouce Investment Conference.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

He is so caught up in this bubble now in the stock market. He’s branded it … The stock market has a big ‘T’ on it for Trump, like one of his buildings.”

So, how exactly does the political rhetoric coming out of the Oval Office stack up against the current economic realities? Dan Kurz at DK Analytics provided a pretty good breakdown of some key issues where the positive talk doesn’t line up with what’s actually going on.

![]()

1. What used to be an ugly stock market bubble that would be pricked by higher interest rates, according to candidate Trump, is now proof that president Trump is doing a great job. Yet, the S&P 500 is currently trading nearly 25x EPS, the broader Wilshire 5000 Index has rocketed higher, and margin debt is nearly $600 billion – a record.

2. In the interim, a recession, which is way overdue, will crush earnings; US aggregate debt rises between $1 trillion and $2 trillion a year; and interest rates are rising smartly, which will pummel valuations if it continues, especially with a recessionary EPS downdraft of 50% plus being likely in the near future based on precedents. (We review such a scenario in some detail in posts #25 and #24, wherein we quantify the rising interest rate impact on the S&P 500’s NPV and wherein we remind investors that markets are “reversion beyond the mean” machines, respectively.)

3. What used to be a fake unemployment rate when Trump was a candidate is now lauded as the “real deal,” even as the civilian labor force participation rate of 62.7% hovers near four-decade lows and two or three low-paying, no-benefit part-time jobs swell the employed ranks while full-time positions continue to be culled. This is insincere.

4. During the address, Trump also stated, “Under my administration, wealth is starting to return to America instead of leaving it.” Mr. President, sadly the opposite has been happening, at least so far, as evidenced by a continued rise in the US trade deficit, a substantial portion of which is due to rising oil import prices (and no, Donald Trump, we are not energy self-sufficient. We remain net importers of oil, and our gap could expand as the fracking bubble collapses). Once again, the president’s claims here are misleading at best.

5. President Trump talks a lot about regulatory reform liberating businesses to hire and invest. According to the American Action Forum outfit, regulatory relief of $560 million p.a. from Executive Order 13,771 (two struck for every new regulation or “reg”) can be expected. While praiseworthy, this is but a rounding error compared to an estimated $2 trillion-plus in annual regulatory compliance costs for US economy. While a sharp reduction in federal register pages (where federal rules and regs are published) from Obama’s “out the door” bloat looks promising, we wonder how any true or lasting reforms can be achieved until regulatory agencies are shut down and statist/leftist bureaucrats are fired, esp. given the risk that the GOP control of the fed government could prove only temporary — which Trump himself recently warned about.

6. Trump protectionism – a disconnect. On the heels of going to Davos and touting that America is again open for business thanks to tax cuts and regulatory reform, Trump was quick to slap high tariffs on solar panels, washing machines, and on select steel imports. Three issues here: first, lots of stuff just isn’t made in America anymore, so higher tariffs line government pockets and hurt consumers and producers alike — such as those installing foreign made solar panels that stand to lose customers or those using cheaper foreign steel in high value-added finished products that are exported — while they raise inflation. Second, raising tariffs on US imports will quickly result in higher tariffs on US exports. Third, we all know what can happen to the global economy if countries get into trade wars. It’s spelled Smoot Hawley, revisited and the 1930s depression.

7. Speaking of policy destructiveness; bloated federal government spending is up 3.8% year-over-year and is set to increase faster as Trump touts various new spending initiatives from (what will sadly ultimately prove to be) pork barrel, crony infrastructure projects to “offensive capacity” military spending growth de facto financed by the “rest of the world.” In the interim, tax rate reductions will pressure tax receipts. Finally, weaker economic growth will dramatically increase government spending on welfare and transfer payments. Talk about a perfect deficit-widening storm dead ahead! And this is before secular challenge known as an aging society and its impact on public sector solvency! Is any of this discussed, much less addressed, in Washington D.C.?

8. We could see a $1.5 trillion – $2 trillion plus dollar federal deficit within a few years if not sooner. And if the Fed really sells $600 billion of Treasuries a year, at what price — how high of a yield — will investors and the rest of the world be willing to soak up between $1.5 trillion – $2.6 trillion worth of US Treasuries possibly coming on to the market annually for a time?

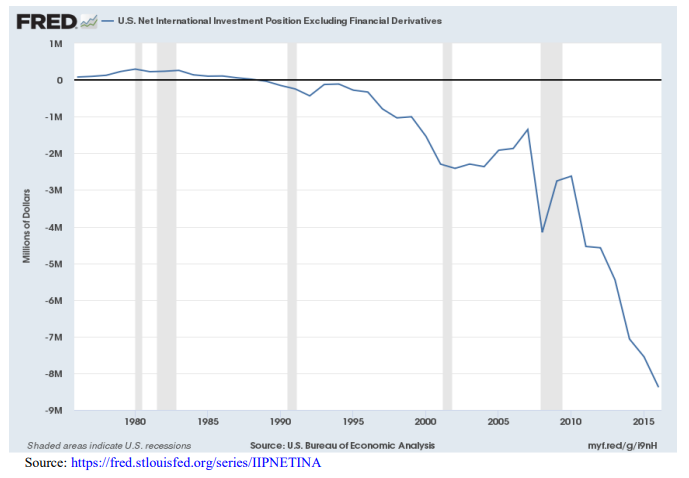

9. The above is of particular concern as the rest of the world finances a US goods and services deficit that averages about $500 billion a year and expanded to $600 billion in 2017. Meanwhile, America is a net debtor nation to the tune of $8.4 trillion. In such a world, when you openly state that the US government would welcome a weaker dollar in a period of low interest rates, great external financing dependency, a weakening currency, and rising inflation, you are driving away potential investors and thus de facto raising the cost of borrowing, especially if sentiment shifts or confidences wanes. And, by the way, if currency debasement helped to reduce trade deficits, America, having the tailwind of a dollar that has fallen about 80% since Bretton Woods dollar-gold standard was terminated nearly 47 years ago, should have huge annual trade surpluses by now in place of gaping deficits.

10. You cannot simultaneously grow a spendthrift federal government, cut taxes, and then be sanguine. You can’t grow spending by $300 billion-plus, reduce tax revenues by an estimated $280 billion, and add it to a $666 billion deficit and over $21 trillion in debt and expect good things.

11. In short, Trump is NOT leveling with the American people in terms of what really needs to be done for the benefit of future generations who will otherwise be hobbled by mountains of debt and the related financing costs, namely: focus on cutting government spending, achieving a balanced budget, aggressively pursuing litigation reform (US liability costs are 2.6 times the EU average), securing long-lasting regulatory relief, and pursuing the solid money that Andrew Jackson pursued when he killed the second US central bank. Noteworthy, the portrait of Andrew Jackson, who Trump greatly admires, adorns the oval office.

12. America is some $68 trillion in debt when combining federal, state, corporate, and individual/family level debt. US GDP is nearly $20trn. Each one percentage point higher borrowing costs from abnormally low interest rates increases America’s cost of funding by roughly $680 billion p.a. (most debt, including the US government’s, is not long-term in nature, thus susceptible to higher refinancing costs if interest rates keep rising). In fact, if the average cost of borrowing rose by just two percentage points — say 10-year Treasuries yielded 4.8% — the US’s financing cost would quickly soar by $1.36 trillion or by 7% of GDP.

13. As we have stated and written, markets are reversion beyond the mean machines. And given the mountains of debt we have accumulated, both solvency and inflation risks (in terms of printing even much more money) suggest that we could easily have a 10-year Treasury that someday yields 7.8% or 8.8% — recall that we exceeded 15% during Volcker’s “tough love” in the early 80s with a fraction of the debt. Five percentage points higher funding costs than today would raise America’s aggregate borrowing cost by roughly $3.4 trillion p.a. from current levels, or by 17% of current GDP. A non-starter. Our point: given the huge indebtedness, relatively feeble manufacturing capacity, and income and debt constrained consumers, higher interest rates could easily choke off and even reverse the positive impact of lower tax rates because they are financed by yet more debt instead of through government spending cuts.

14. Sadly, too many of Trump’s policies will ultimately rely on the very printing press that has gotten us deeper and deeper into debt, into yield starvation, into huge misallocations, into cratering productivity growth, and into accelerating solvency risks and inflation risks. Inflation is the largest stealthy property thief for the average person, and especially for retired folks, who are dependent on a fixed income stream and bond investment returns.

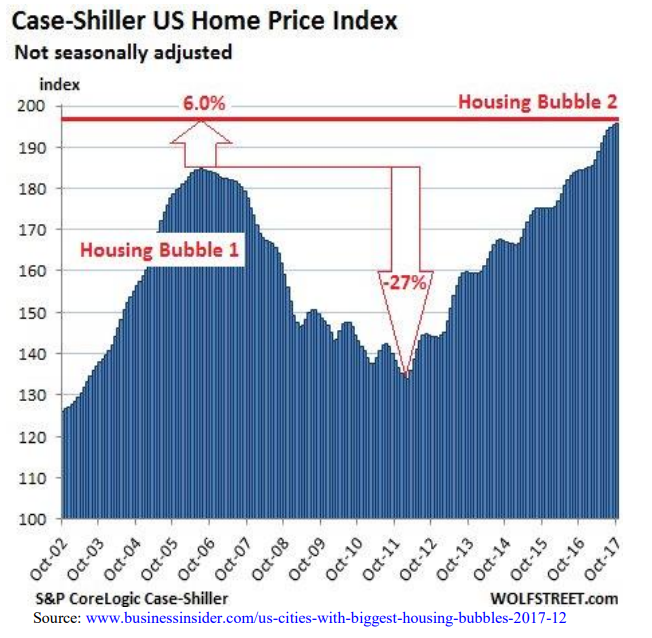

15. Year-over-year wage growth is 2.4% overall and but 2.2% in supposedly robust manufacturing while inflation is picking up, the housing bubble has eclipsed the 2006 highs, and mortgage rates are rising briskly — in short, housing is increasingly unaffordable for most Americans. In a related sense, we wonder how a 65-year low in the unemployment rate and low wage growth rates are possible at the same time?

16. The personal savings rate has plummeted to 2.4% from 5.9% two years ago as record auto loans ($1.1 trillion) and student loans ($1.5 trillion plus) suggest tapped out consumers. It also implies substantial demand has been borrowed from the future, i.e., that it won’t be there this year or next. If the “consumption function” is over 70% of GDP, this isn’t an academic issue.

Yup. As my old professer’ George Carlin said about what we get from politics: It’s all bullshit and it’s bad for ya.

There is a huge fucking disconnect out here. When I start talking to just almost anyone about the massive debt and out of control spending, people look at me like I’m nutz. We’ve dialed down to the metaphorical fairy dust printing presses for trillions of dollars that weren’t earned, worked for or produced by a fucking thing other than some 1s & 0s.

Jim shows me all these charts and graphs and economic Brainiacs like him can understand all of them. Not me. But I know down to my bones you can’t continue printing these lies by the 100s of billions, month in and month out. You can’t.

All I can say is it’s going to be spectacular when it does blow up. Millions are going to be in a world of hurt, like me.

I see the fat fucks McConnell and Schumer smiling as they sign off on another trillion in deficit spending. A TRILLION, just like that, added to the pile of trillions in fake IOUs. These assholes and every GD member of Congress are traitors. In all of my life there have been just a couple politicians I’ve ever seen that have been honest about the fucking lies we get hammered into out heads 24/7.

Ron Paul has always tried to warn us about this massive debt idiocy and Tom Tancredo has always done the same about immigration. Both of these men are publicly regarded as nutz. And all the while my worthless Congressman prattles on about cotton subsidies. Fuck me.

Too bad. For us.

I was somewhat giddy after Trump’s SOTU.

This articles puts it all in perspective. I am no longer giddy.

Kind of a shame, really, that this most excellent article only has 4 comments (and that includes this one). It must be because we all already know this stuff or, Trump isn’t the only one sticking his head in the sand.

You want to talk giddy, how about that Inauguration Speech?

You want to look at PCE. And the Philly Fed state coincident index. And also the jobless claims. CalculatedRisk presents all this data in a very readable form. You also want to keep an eye on the yield curve. None of these indicators are bad right now. The Philly Fed state coincident index is the worst of them right now, but nothing that screams recession.