The Fed is raising rates, forecasting more hikes and the stock market is falling. Fed Chair Powell says he can’t promise a soft landing. Pundits are peering into the future expecting the stock market to continue down.

The Fed is raising rates, forecasting more hikes and the stock market is falling. Fed Chair Powell says he can’t promise a soft landing. Pundits are peering into the future expecting the stock market to continue down.

The Fed proclaims the days of easy money are behind us; many expect bond defaults and a slowing of the business cycle. I read where Jeff Bezos net worth dropped $20 billion in one day; wonder what it will look like at the end of summer.

Subscriber Rick G. asked an interesting question, “What do you think of the age-old strategy of cost averaging?” Rick is referring to owning a stock, seeing the market price drop, and then buying more to bring down your average cost per share.

While it sounds like a simple question, the answer is quite the opposite.

I am not a registered financial advisor, nor did I spend last night at a Holiday Inn Express…. However, I do have a lot of experience with the theory Rick asked about. To address his question, I need to break things down.

Understanding the standard myths…

My first real exposure to dollar cost averaging was during the internet boom/bust in the 1990s. People were getting rich buying overpriced internet stocks, riding the price up, seeing the value of their portfolios hit new highs regularly. Buy high and hope to sell to a bigger fool down the road.

The market and economy were booming. When the bubble finally burst, it wasn’t pretty.

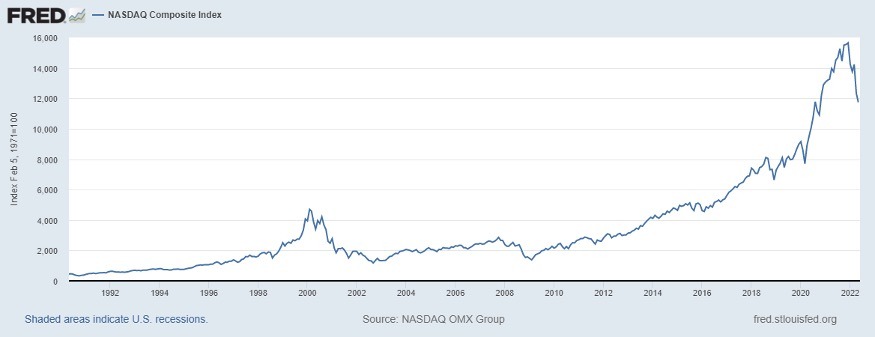

The NASDAQ dropped from a high of around $4,700 in February 2000 to approximately $1,175 in September 2002. When adjusting for inflation, it took almost 20 years to return to the previous high. A lot of investors saw their net worth crumble.

The brokerage community was preaching dollar cost averaging, reminding investors the market always comes back. As they were encouraging their retail clients to stay invested, the major investment houses were shorting the daylights out of the market.

The first question we must ask is, can anyone guarantee the market or the individual stocks I own will return to their previous high in my lifetime?

Does the market always come back to the previous high? Absolutely! It may take a decade or more, but eventually it will get there. Does the individual stock price always come back – NO!

I saw EMC drop from $104 down to $4. Many of the high-flying internet stocks never came back. You can dollar cost average all you want, but it is not a blanket rule; look at each investment you own individually.

The first question I’d ask is why did I buy the individual stock in the first place? Did I buy it for dividend income, was I thinking like a trader, hoping to see the stock appreciate and selling it for a profit down the road?

If the reason you bought the stock was primarily to profit from price appreciation, that is why you set stop losses. In a down market, it’s easy to see the price drop, agonize about selling it, holding on while it continues to drop along with the market. I recall one conversation with my broker where we both concluded, “EMC can’t go any lower.” The heck it can’t, and it did. That is a hard lesson to learn and why you have stop losses. The purpose is to prevent catastrophic losses in one investment from destroying the rest of the good returns in your portfolio.

I rode EMC from approximately $104 down to $40, what I paid for it, and learned an expensive, valuable lesson. Before you consider cost averaging, do you think it is realistic to expect the market and the individual stock to go back up? How long do you feel it will take? Not just hope, but some solid reasons the price should come back.

Try to fight the panic, stay logical and think things through. Sometimes you may be better cutting your losses than compounding them. Preserve your capital. A down market is not the time to get greedy, taking profits is a good thing. Trying to time the market tops and bottoms is impossible, particularly with the program traders controlling much of the markets.

Try to fight the panic, stay logical and think things through. Sometimes you may be better cutting your losses than compounding them. Preserve your capital. A down market is not the time to get greedy, taking profits is a good thing. Trying to time the market tops and bottoms is impossible, particularly with the program traders controlling much of the markets.

What about stocks I bought for income?

Friend Tim Plaehn of the Dividend Hunter reminds us we buy dividend stocks for their income stream. We recently wrote about preferred stocks and how many are now selling below par value.

If there is any general rule regarding dividend stocks it is each investment must be looked at individually. Some preferred stocks, selling below par value are yielding 8% or more. If they are solid, you may want to buy more.

If you own a CD paying 5% and now, they are paying 6%, you may buy some more. The market price of the security is not a major concern like stocks you buy for appreciation. You are buying an income stream.

When solid dividend-paying stocks go on sale, you not only get additional yield, but you also have room for price appreciation when interest rates cool. In addition, common stocks can always raise their dividends, and many have a decades-long history of doing so, no matter what the market may bring.

MarketWatch recently reported “Dividend stocks have trounced the market this year.”

Personally, I avoid funds focusing on dividend income. Bunching a group of high dividend payers together in a fund, hoping not too many cut their dividends is fraught with risk and ongoing fees.

When you own a mutual fund, you have a business partner. Should some partners panic, the fund may have to sell good dividend payers to meet the redemption demands. I would rather deal with individual stocks and not see the value of my holdings go down because others have panicked.

Exceptions

One type of cost averaging seldom mentioned is automatic dividend reinvestment programs. We have some long-term holdings where the broker automatically reinvests the proceeds in additional stock. We have a little over 11% more shares than we originally purchased, and the dividend income keeps on growing.

Another exception is stocks like Wheaton Precious Metals, which is part of our core holdings. When silver prices drop, along with the stock price, there are times I’ve bought more. The decision is based not only on the company, but the underlying business. With high inflation, we expect the long-term prices of metals to continue up.

A special note for retirees

Retirees no longer have their job and regular income to pay their bills. When you are working, you trade time for money. When retired, you trade money for time. Most retirees supplement their social security or pension with income from their life savings, hoping it lasts throughout their lifetime.

When I retired, I signed up for several investment newsletters touting various types of stocks. Each month they would send out the publications and their recommendations sounded great.

Soon I was fully invested, with ample cash reserves. Each time I got a newsletter, I would ask myself, “What do I have to sell to buy this recommendation?” It was easy to lose sight of the big picture, I was churning stocks based on who had the best writeup.

When a broker recommends dollar cost averaging, the retiree asks, “Where am I going to get the money?”

Hopefully your portfolio is balanced, with ample cash reserves to not only live on, but also take advantage of bargains that will arrive when the market really crashes.

While no one can time the market perfectly, just because something is on sale, does not mean you should buy it. Do you feel the market, or the stock is anywhere close to bottoming out? If you are buying in anticipation of the stock price turning around, what do you see that would cause it to do so?

Dollar cost averaging for the sake of lowering your individual share cost is not enough. Unless you see realistic appreciation on the near-term horizon, might you be better off holding your cash reserves?

Lesson Learned

When the 2008 crash hit, several retired friends took a real hit. Some saw their portfolio drop 40% or more. They told me their young stockbrokers sang the company line, “Don’t worry, the market always comes back.” Some told them to “dollar cost average, stocks were on sale.” They obviously didn’t understand their client’s dilemma.

One friend needed his portfolio to yield 5% to provide enough pay his bills. Unfortunately, he was heavily invested in stocks, looking for appreciation, not dividend payers. What little he had in CDs and bonds got called in and interest rates were below 2%. Buying stocks, dollar cost averaging, with his remaining cash was out of the question, he had bills to pay.

One friend needed his portfolio to yield 5% to provide enough pay his bills. Unfortunately, he was heavily invested in stocks, looking for appreciation, not dividend payers. What little he had in CDs and bonds got called in and interest rates were below 2%. Buying stocks, dollar cost averaging, with his remaining cash was out of the question, he had bills to pay.

With a smaller portfolio he now needed almost 10% return to pay his bills, which was unrealistic. He was forced to sell off some of his stocks at exactly the wrong time to meet his obligation. Yes, the market may come back, but he had bills to pay now.

Each person must balance their portfolio and diversify to protect against catastrophic losses, not only in the market, but also from inflation. Your goal is no longer to get rich; but rather to keep from getting poor.

The answer is….

Rick, do I believe in “dollar cost averaging?” Yes, with a lot of exceptions and caveats. While the market may always come back, it does not guarantee your portfolio will.

For more information, check out my website or follow me on FaceBook.

For more information, check out my website or follow me on FaceBook.

Until next time…

Dennis

“Economic independence is the foundation of the only sort of freedom worth a damn.” – H. L. Mencken

Affiliate Link Disclosure: This post contains affiliate links. If you make a purchase after clicking these links, we will earn a commission that goes to help keep Miller on the Money running. Thank you for your support!

Sage advice.

I am making $92 an hour working from home. i was greatly surprised at the same time as my neighbour advised me she changed into averaging $ninety five however I see the way it works now. I experience mass freedom now that I’m my non-public boss. That is what I do.. http://www.profit97.com

https://newspunch.com/investigators-discover-destruction-of-americas-food-supply-chain-is-an-inside-job-by-new-world-order/

Market comes back. After the crash of ’29 it took 25 years. Do you have that long to break even? When the DJIA hit 1000 in 1972, brokers exclaimed that magic number is a launch pad. Two years later it was 577 and it was ten years before it got back to 1000. To me everything looks bad now. Stocks are going down when interest rates go up, just like in the 70’s. Bonds tumble too to higher yields. Why take market risk when you can get a bank CD paying 10%. I think that’s when brokerage houses and some mutual fund companies got big into money market funds–a compromise between CD interest rates and liquidity.

My wife has bragged about her IRA 50/50 stocks and bonds mutual fund until so far this year she has lost about 10% of the value. Better than the DOW or S&P, but still down. Next year she’ll have to take an RMD, and that may mean selling funds at a low point in order to take a distribution we don’t need and pay taxes on it while at the same time turning a “paper” loss into a real one.

We live a modest lifestyle (at least I do) and haven’t had a mortgage in 15 years, so we actually pretty much make it on Social Security, using my RMDs to pay our property tax and insurance. Our cars are old but still reliable (total 450,000 miles), and I sure wouldn’t buy a car now at sticker + prices.

I keep wondering about gold and silver, in particular “junk silver” (pre 1965 silver coins), but I’m reticent.

Best advice I’ve seen here on Burning Platform is Avoid Philadelphia, and I’ll surely do that!