Update (0835ET): After another massive bank failure – and taxpayer-funded bailout – JPMorgan CEO Jamie Dimon told listeners on an investor call this morning that “The system is very, very sound.”

Doesn’t seem like it Jamie, old chap?

But hey, whatever you say now as the CEO of a bank that holds over 10% of America’s deposits.

“We need large, successful banks in the largest economy,” Dimon continued, proclaiming that “this is nothing like ’08 or ’09.”

Well he is right, in so much as this is far larger… and we really don’t know where the CRE holes on bank balance sheets are (even as Charlie Munger warns they are everywhere).

The good news, Dimon declares regarding bank failures, “this is getting near the end of it.” Thought how he would know that is hard to comprehend?

Finally, the too-biggest-to-fail bank CEO warned, “we are clearly gong to see some reduction in bank lending,” implying JPMorgan will be doing “God’s work” for The Fed by contracting credit without the need for rate-hikes.

For now, it’s clear what the market thinks of JPM’s state-sponsored buyout of FRC assets…

Dimon’s closing comments were the most prophetic, stating that they “support community banks” and that “banks will consolidate.” Of course they will, once the banks are pushed into FDIC hands and assets scooped up by JPM with govt bankstops…

Translation: We will wait for the bank run (thanks Fed for the hike to 5.25%) to cripple them all, then buy them all for cents on the dollar with the FDIC keeping the toxic crap.

* * *

Heading into the weekend, US regulators were facing a dilemma over the fate of First Republic Bank: either let the insolvent California bank fail and bail-in some (or all) of the $30 billion in uninsured rescue deposits given to the bank by a consortium of banks including JPMorgan, BofA, Goldman and others so as not to appear like the Biden admin is bailing-out big, bad banks again a la 2008, but in the process restarting the bank run panic as an impairment of all bank depositors would reverse Janet Yellen’s vow not to do just that in the aftermath of the SVB collapse, or bail out FRC including all of its depositors, both retail and institutional, insured and uninsured, and spark a fresh political crisis where republicans accuse democrats of rescuing Jamie Dimon and his banker pals.

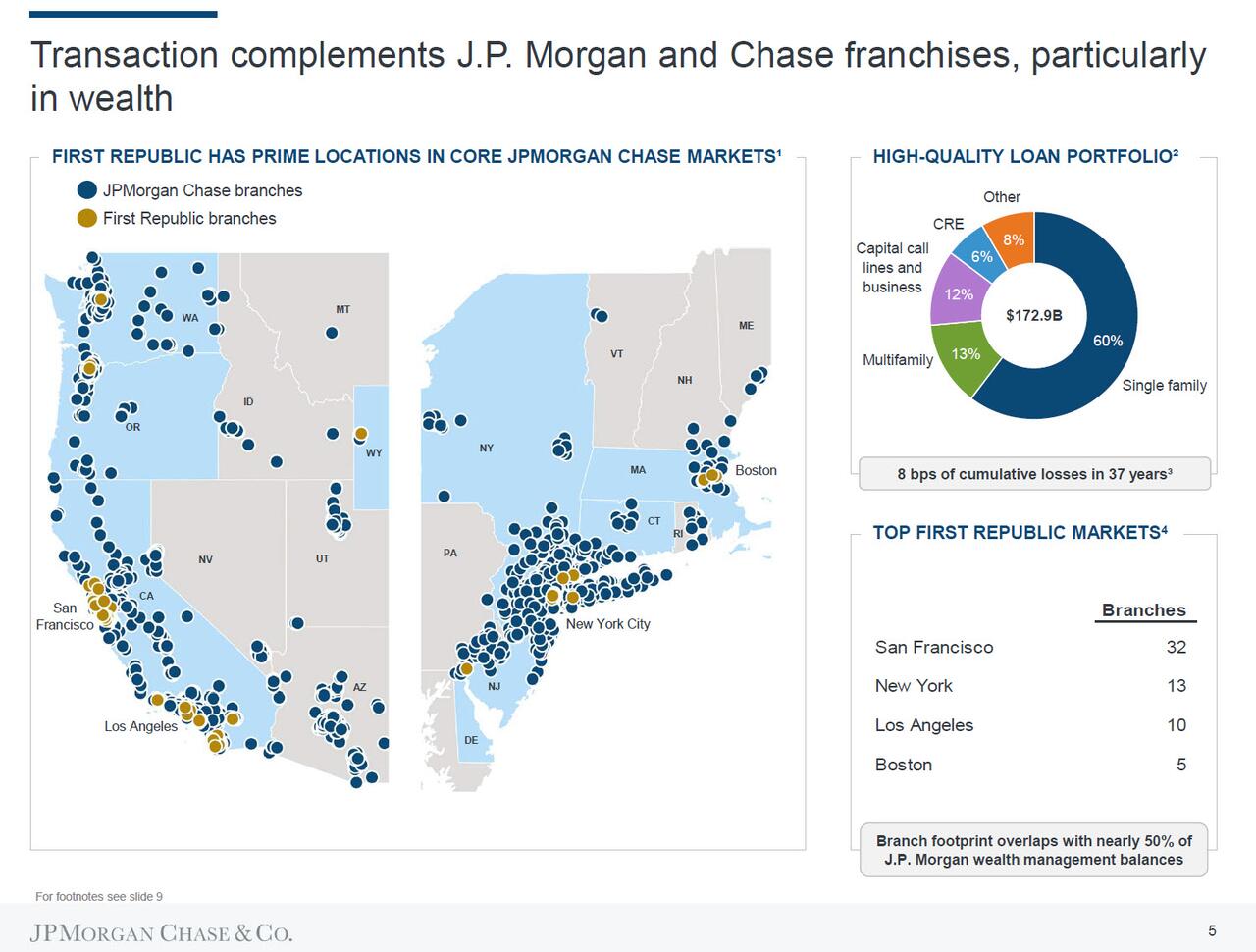

In the end, early on Monday morning, the US unveiled a hybrid solution – after all other attempts at a private rescue effort failed – one where the FDIC would seize the insolvent First Republic, the 14th largest US bank by assets, making it the second biggest bank failure in US history, and immediately sell the bulk of its assets and all of its deposits to JPMorgan after a sham but “highly competitive bidding process” had taken place over the weekend (one in which virtually nobody wanted to participate as nobody would buy FRC without explicit government backstops, which in the end is precisely what they ended up getting on FRC’s IO and CRE loan portfolio) while keeping FRC’s toxic Interest-only mortgages to Hamptons’ billionaires.

According to the FDIC announcement, JPMorgan would assume all of First Republic’s $92 billion in deposits — insured and uninsured, including the $5 billion in deposits gived by JPM to First Republic on March 16. It is also buying most of the bank’s assets, including about $173 billion in loans and $30 billion in securities.

As part of the agreement, the Federal Deposit Insurance Corp. will share losses with JPMorgan on First Republic’s loans. The agency estimated that its insurance fund would take a hit of $13 billion in the deal, which is precisely the hole that prevented a private sector solution from being reached. JPMorgan also said it would receive $50 billion in financing from the FDIC to consummate the deal.

More importantly, the FDIC and JPMorgan also entered into a “loss-share transaction on single family, residential and commercial loans it purchased of the former First Republic Bank.” As part of this transaction, the FDIC as receiver and JPMorgan will share in the losses and potential recoveries on the loans covered by the loss-share agreement.

The loss-share transaction, the FDIC said, is projected to maximize recoveries on the assets by keeping them in the private sector, and “is also expected to minimize disruptions for loan customers. In addition, JPMorgan Chase Bank, National Association, will assume all Qualified Financial Contracts.”

The second largest US bank failure in history become a fact after the San Francisco-based First Republic lost $100 billion in deposits in a March run following the collapse of fellow Bay Area lender Silicon Valley Bank, a testament to the catastrophic supervision of the Mary Daly-led San Fran Fed, which was more worried about rainbow flags and DEI than making sure banks in its regions were, you know, solvent. It limped along for weeks after a group of America’s biggest banks came to its rescue with a $30 billion deposit. Those deposits will be repaid after the deal closes, JPMorgan said.

And with the collapse of FRC, three of the four largest-ever U.S. bank failures have occurred in the past two months. First Republic, with some $233 billion in assets at the end of the first quarter, ranks just behind the 2008 collapse of Washington Mutual. Rounding out the top four are Silicon Valley Bank and Signature Bank, a New York-based lender that also failed in March.

Meanwhile, just as we said a month ago when we joked that the regional bank crisis is meant to make JPM even bigger and more systematically important than ever, as it pays just 0.01% on its deposits as it remains the only truly “safe” bank for US depositors, in effect collecting a $90 billion annual subsidy courtesy of its TBTF status…

JPM's "Too Biggest To Never Fail" subsidy: if it paid 4% on its $2.3 trillion in deposits, it would pay out $90BN per year. Instead it pays nothing to fund its assets thanks to 0.01% deposit rates pic.twitter.com/w7D4oCZ2HN

— zerohedge (@zerohedge) April 25, 2023

… both First Republic and Washington Mutual are now substantially owned by JPMorgan. The nation’s largest bank, it has been known to step in during banking crises. Chief Executive Officer Jamie Dimon was pivotal in earlier efforts to rescue First Republic.

“Our government invited us and others to step up, and we did,” Dimon said Monday.

Following the transaction, First Republic’s 84 branches will reopen as part of JPMorgan Monday during normal business hours, and customers will have full access to their deposits, the FDIC said.

As the WSJ notes, First Republic’s failure seems unlikely to spur another crisis of confidence in the Main Street lenders that serve a large chunk of America’s businesses and consumers. Regional lenders uniformly lost deposits during the first quarter, but the declines were modest compared with First Republic’s $100 billion outflow.

“This is the last stages of that initial panic. First Republic’s problems started as a result of SVB and Signature,” said Steven Kelly, a senior researcher at the Yale Program on Financial Stability. “This isn’t the story of 2008, where one bank went down and investors focused on the next biggest bank, which would wobble.”

Actually, it is, because only now does the solvency crisis courtesy of trillions in commercial real estate on bank books start to manifest itself, as we also warned it will. But it will take a while for that to trickle down to the rest of the population.

As for the immediate cause of First Republic’s collapse, just like in the case of Silicon Valley Bank, was a smartphone-enabled exodus of panicked depositors with big uninsured balances, but the bank’s problems were rooted in a wrong-way bet on interest rates. A focus on America’s coastal elite helped First Republic become one of the most valuable U.S. banking franchises. Big deposits from customers with lots of cash funded low-rate jumbo mortgages to wealthy home buyers in both California and New York. Ultralow interest rates and a pandemic savings boom supercharged the bank’s growth.

When the Fed began raising interest rates last year to cool inflation, customers began demanding higher yields to keep their money at First Republic. Rising rates also dented the value of loans the bank made when rates were near zero.

The chronic problem turned into an acute one in March, when the collapse of Silicon Valley Bank sparked fears about the overlooked risks lurking in the banking system. Investors and customers were especially worried about banks, such as First Republic, that relied heavily on uninsured deposits and had large unrealized losses in their loan and securities portfolios due to rising rates.

“It was a run on the business model,” Kelly said.

First Republic’s badly damaged balance sheet left it with few good options. In a dismal quarterly-earnings report last week, the bank disclosed the extent of the deposit run and said it had filled the hole on its balance sheet with expensive loans from the Federal Reserve and Federal Home Loan Bank. An untenable future, in which it earned less on its loans than it paid on liabilities, appeared all but certain. The earnings report sent the bank’s stock down nearly 50% in one day. First Republic shares ended the week at $3.51. They closed at $115 on March 8, the day before SVB’s disastrous run. They traded around $1.9 in the premarket following news of the FDIC seizure which effectively wipes out the equity.

As the WSJ notes, while some employees started jumping ship after SVB’s collapse, many stayed and watched the bank’s stock crater last week and frantically texted friends about how they feared the bank would go under soon. Some said they wished management had provided clearer communication about where the bank was headed.

Business had grown quieter since the banking turmoil started, current and former employees said. First Republic bankers who previously focused on luring in deposits found there was little they could do to reverse the tide when customers started pulling cash. Pay took a hit too: Bankers were compensated in part by how much in customer deposits they brought to the bank.

In a pair of emails late Friday and Saturday morning, CEO Michael Roffler and Executive Chairman Jim Herbert thanked First Republic employees for staying focused during the turmoil.

“Throughout our history and in these past weeks, we have done what we always do—serve our clients, support our communities, and take care of one another,” Roffler wrote. “When we come in next week, we will continue to do the same.”

Hoping that the bank crisis is over now that First Republic has been tucked away, the US Treasury issued a statement on Monday morning after the deal was announced, saying that the US banking system remains sound, resilient, and with the ability “to fulfill its essential function of providing credit to businesses and families.”

The good news is that we will very soon test just how resilient the banking system is after the full extent of the CRE crisis become evident over the coming year.

As for the biggest winner from the FRC bank failure and the regional banking crisis in general, it should be quite clear to all who that is by now.

In a presentation published by JPMorgan laying out the transaction details, the bank explained just how it would clean up the various odds and ends from the failed March rescue: it will repay $25B of deposits from large U.S. banks and eliminate a $5B deposit from JPMorgan Chase on consolidation. It will also make a $10.6 billion payment to the FDIC, while the FDIC will provide a new $50B five-year fixed-rate term financing to cover the liability shortfall as a result of the bank’s historic bank run. To be sure, there were some questions here with former Fed staffer Julia Coronado trying to understand how the FDIC is lending directly to JP Morgan: “Where will they get the money? What terms?”

I am trying to understand this part of the First Republic deal. The FDIC is lending directly to JP Morgan? Where will they get the money? What terms?

FDIC will provide a new $50B five-year fixed-rate term financing

— Julia Coronado (@jc_econ) May 1, 2023

Additionally, as noted above, the FDIC will provide loss share agreements with respect to most acquired loans: Single family residential mortgages: 80% loss coverage for seven years; Commercial loans, including CRE: 80% loss coverage for five years.

![]()

JPM also disclosed that it would take a one-time gain of $2.6B post-tax at closing, not including expected restructuring costs of $2.0B over the course of 2023 and 2024; and perhaps more importantly the fair value marks on acquired loans is ~$22B, with an average loan mark of 87%, while the FDIC’s loss sharing deal reduces risk weighting on covered loans, with an average risk weighting of ~25%.

![]()

As for the deal rationale, well… JPM didn’t have to include this slide – after all the rationale was all about taxpayers getting stuck with FRC’s toxic sludge while JPM getting all the good assets at pennies on the dollar – but it did anyway, so here you are: 20% IRR courtesy of taxpayers.

![]()

Finally, all of FRC’s high net worth clients in California and New York now belong to JPM.

For those wondering, this is the reason why one month ago we changed JPMorgan’s name to JPMega.

The full JPM First Republic integration slideshow is below (pdf link).

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

Isn’t it great that the Global Banksters have our backs. I never felt so secure.

Signed. The creatures from Jekyll island

Run for the hills!!!!

Aren’t there several millionaires who claim to have gotten rich by doing EXACTLY the opposite of what that dipshit says?

Inverse Jim Cramer says sell.

This is Great. Did JPM have a shareholder vote? #BankruptByVoting #RainingBankers #BuyingTies

Do you think shares are distributed well enough for that to matter?

They plunder and plunder and plunder until the CBDCs are ready. But they aren’t and the timeline and the human component of the equation is ever not in their favor.

Yeah, it’s still very sound for Jamie’s chronic grift.

Exactly.

I at least like the fact that some folks are aware of, and revealing the crimes, even though the lumpen response will be indifferent at best, or ignorant of such power corruption at worst.

E.g.;

How’d your NFL team do in this year’s draft? or, What’s on cable tonight honey?

I smile and don’t care one smeg’n iota of any of this BS. I keep only enough in the bank, CU, to pay some bills. All extra gets converted to shiny bits.

The warning bells are clanging and have been for a long time now. We knw the crash is coming, but we also know that someone farts and they start clanging the alarm bells with more vigor. Probably to desensitize the braindead into ignoring the warnings so the parasites can bleed every last penny from the proles pockets.

When it all does finally come down, next week, next year or the year after, soon enough, it will destroy all those holding paper. Stocks, bonds, t bills, mortgages, deposits, everything not shiny or hard asset will be wiped out and there will be wailing and gnashing of teeth.

Greed, utter and complete, will keep the parasites at the trough long after its been emptied. Looking for scraps and finding none. C’est la vie

I am trying farm myself into the poor house.

Keep going.

Your comment reminded me of what My uncle said. He hated the Wheat board and often spoke of the grain companies elevators as the whore houses. Its where farmers go to get raped.

But I said one day that I wanted to buy a farm. He surprised me when he said “What the hell you want to do a stupid thing like that”. After the dressing down on the why I shouldn’t I said because I like the lifestyle. I got a shoulder hug. Love farming to this day, still looking for farmland to buy.

Or, alternatively I could do something more valuable, like voting. Or walking door to door drumming up votes to sustain a corrupt and evil system of slavery.

I’ll go farming.

Farming is not a business, it is a lifestyle. There is an economic side to it, but compared to the rest of farming it is relatively minor.

That said, if you put in the time, the effort, and pay close attention to the land and the seasons, it is the best possible life you can have.

Laura Ingalls disagreed.

So did Charles Moody, Ralph Moody’s father, when he threw in the towel. (Little Britches – excellent, excellent series. I think you’d enjoy them, HSF)

Not saying I disagree with you, but others do. Maybe modern farming is different?? Well, maybe not, lots of modern farmers near me are selling off. 🤔

Commercial farming is profitable or it wouldn’t be done. But commercial farming relies heavily on equipment and chemicals. IMO, that ain’t farming.

Small farming with mixed diversities of animal and feed crops won’t make you wealthy but you will be healthier in body, soul and mind. Whats more important? I’ll take the small time farming any day.

I’d take the idyllic small farm, too.

I have a nice piece of rock candy, but it’s not for eatin, it’s just for lookin thru…

I was look’n for an edge.

I had a horse but he surrendered and didn’t.

So many great scenes in this movie.

So once the free fiat currency stops flowing small banks fail and the big federal reserve banks are there to gobble them up? Sounds like a litmus test me. We will have one bank left standing in the end when this pyramid scheme comes tumbling down. “Grifters Extraordinaire”

Major bankruptcies so far this year = EIGHT. List.

Thx for the link, UD.

https://wallstreetonparade.com/

.

Criminal cartel behavior between government and their banking owners and very few will even realize it.

Aaand…We’re Gone.

[youtube

Captain of Titanic says “Everything is fine….this ship is unsinkable….”

That’s how you know it’s sound.

Clown World all the way down.

Like the vaxx ……its very-very safe and effective.

very very sound & fury, signifying …