Real estate developers must really have short memories. They get hit over the head with the sledgehammer of reality every few years, declare bankruptcy or beg for their drug dealer at the Fed to give them some more of the good stuff, and come back for another round of idiocy.

Total hotel revenue in the U.S. was 4.2% higher in 2013 than it was in 2007. But, over this time frame the number of new hotels has increased total hotels by 11%.

Almost 2,700 new hotels were built at the peak of the market in 2008/2009. Revenue declined, occupancy rates plunged, and revenue per room plummeted. New hotel construction collapsed by 70% in 2011 and 2012. Now here we go again.

New hotel construction doubled in 2013 and will approach record levels again in 2014. If real median household income is lower than it was in 1999 and real wages are stagnant, who is staying at all these hotels? Are the 1% really having that much fun?

The reason for the building boom in 2007 – 2009 was the easy money policies of the Federal Reserve. Hundreds of real estate developers should have gone under after 2008, but the Fed propped them up with 0% interest rates and allowing them to extend their loans and pretend they were making their loan payments.

The current Fed created easy money bubble has convinced these developers to do it all over again. I’m sure it will work out this time.

For those who are chart oriented, here are a couple of interesting charts. An 11 year continuous bull market in gold ended in 2012. The entire 500%+ move was missed by douchebags like Barry Ritholtz and the other blowhard Wall Street shysters. They have been joyous over the last three years as gold has fallen a whole 35%.

The efforts of the Federal Reserve and their Wall Street owners to suppress the price of gold has been blatant. The massive sell orders designed to drop the price can be clearly identified. Rising gold prices reveal the economic dysfunction and Fed created inflation. Therefore, optics are everything while the ruling class finalizes their pillage-fest. But gold has begun to test resistance in its downtrend. If it breaks through the $1,300 level, it could be off to the races.

The price of gold has had a 93% correlation to the national debt over the last 114 years. This makes total sense, as the debasement of a fiat currency through debt creation makes hard assets that have retained value for centuries more valuable. The Fed’s manipulation and Wall Street’s rigged markets, with the blessing of the Federal government, has put a lid on the price of gold for the time being. Based on the historic correlation, gold should be priced at $1,700 today. The government adds $2 billion of debt per day. They are only men attempting to retain their wealth and power though dishonest means. They will fail. The US fiat currency will ultimately achieve its true value – ZERO.

If someone offered you 100 ounces of gold or $125,000 in fiat currency today and told you it couldn’t be touched for 20 years, which would you choose?

These charts never grow old whenever you want to reveal the truth about the “healthy” market driven housing recovery touted by the moronic media, the Wall Street shysters and the national association of lying realtors. Shockingly, mortgage applications to purchase a home FELL again last week.

Mortgage rates have been falling for the last 14 straight months to a new low of 4.25% for a 30 Year Mortgage. According to the MSM and the government we’ve been adding jobs at a rapid clip for the last year. Obama tells me we’ve added 10 million jobs since he assumed command. The stock market is at all-time highs. It sure sounds like everything is coming up roses. Ask yourself a couple questions.

Why are mortgage applications to purchase a home down 12% versus one year ago?

Why are they lower than they were in 2010 at the recession lows?

Why are they at 1997 levels, well before the housing boom took hold?

How could home prices rise by 25% since 2012 even though mortgage applications have plunged?

How could mortgage applications be 65% BELOW 2007 levels when mortgage rates were 6.7%?

There were 272 million Americans living in 101 million households in 1997. Today, there are 320 million Americans living in 122 million households. But mortgage applications to buy a house are at the same level as 1997. And this is what is being touted as a housing recovery? You’d have to be asleep or brain dead to believe it. Check out CNBC for proof.

All of the freed up money from refinancing over the last five years, which created additional spending by delusional consumers, is history. Refinancing applications are DOWN 73% from the last gasp in May 2013. Anyone who doesn’t have a mortgage rate below 5% is either a fool or a tool.

The answer to all of the questions above is:

COLLUSION BETWEEN THE FEDERAL RESERVE, THE WALL STREET BANKS, AND YOUR FEDERAL GOVERNMENT.

You were wondering why retailers are reporting dreadful results? Look no further than Obamacare. Manufacturers overwhelmingly report higher employee contributions, deductibles, out-of-pocket maximums and copays, with a lower range of medical coverage and a lower size and breadth of the network.

Have your health insurance costs gone down since Obamacare was passed in 2009? And now for the best part. Obama illegally delayed all the really bad stuff until after the November elections. It seems the Democrats don’t want to run on this abortion of a program.

I’m still waiting for my $2,500 of savings. I’m sure the check is in the mail.

Was Dear Leader misquoted?

Obamacare Is A Disaster For Businesses, Philly Fed Finds

Submitted by Tyler Durden on 08/21/2014 10:35 -0400

Remember all those allegations that Obamacare would be an unmitigated disaster for businesses, especially smaller companies? Well, now we have proof.

As the Philly Fed, which mysteriously soared at the headline level even as the vast majority of its components tumbled, reported moments ago, “in special questions this month, firms were asked qualitative questions about the effects of the Affordable Care Act (ACA) and how, if at all, they are making changes to their employment and compensation, including benefits.”

What the survey found was very disturbing: not only did businesses report that as a result of Obamacare the number of workers they employ is lower than higher (18.2% vs 3.0%), that there has been an increase in part time jobs (18.2% higher vs 1.5% lower), leading to a big increase in outsourcing and most importantly, Obamacare costs are being largely passed on to customers (28.8% reporting higher vs 0.0% lower), the punchline was that while there is basically no change in the number of employees covered (17.6% higher vs 14.7% lower and 67.6% unchanged), there has been a big jump in Premiums, Deductibles, Out-of-pocket maximums, and Copays, which has been “matched” by a far greater reduction in the range of medical coverage and the size of the network.

In short a disaster.

And what’s worse, this sentiment will persist long after the current subprime auto loan-driven manufacturing renaissance is long forgotten.

More proof that Bennie and Bubbles have created a 2nd housing bubble that will pop again. Prices are up 35% from their lows even though home sales languish at 1999 levels. Mortgage applications are at 1998 levels when inflation adjusted home prices were $190,000. Today inflation adjusted prices are $240,000. This bubble is 100% driven by Federal Reserve monetary policies and the buy to rent scheme hatched by Wall Street and their puppets at the Fed and Treasury. When this bubble pops (they always do) home prices will drop 20% to 30% from current levels. The dupes who’ve bought in the last two years will be underwater and over their heads. Some things never change.

For some perspective on the all-important US real estate market, today’s chart illustrates the inflation-adjusted median price of a single-family home in the United States over the past 44 years. There are a few points of interest. Not only did housing prices increase at a rapid rate from 1991 to 2005, the rate at which housing prices increased — increased. All those gains and then some were given back during the following 6.5 years. Over the past two years, however, the median price of a single-family home has trended significantly higher. More recently, the inflation-adjusted price of the median single-family home has declined and is now testing support of its two-year upward sloping trend channel.

IBM is a poster child for the ill-effects of the Fed’s financial repression. In effect, the Fed’s zero interest rate policies are telling big companies to issue truckloads of debt and use the proceeds to buyback shares hand-over-fist. That way fast money speculators on Wall Street are appeased by the resulting share price lift, and top executives collect bigger winnings on their stock options.

In its recently completed quarter, IBM again repurchased nearly $4 billion of stock—which amounted to about 93% of its net income for Q2. Likewise, IBM also reported lower sales versus prior year for the ninth quarter in a row

This juxtaposition should not be surprising. For more than a decade now, IBM has been eating its seed corn. Since the beginning of fiscal 2004, Big Blue has posted $131 billion in cumulative net income, but saw fit to reinvest fully $124 billion or 95% of its earnings in its own balance sheet, which is to say, in buying back its own stock.

At the same time, it also paid out nearly $30 billion in dividends. In combination, therefore, it disgorged $153 billion in buybacks and dividends—-or 117% of its net income! And this wasn’t a temporary maneuver: These figures represent the results of IBMs last 42 quarters. In short, IBM has become a stock price inflation machine, driven by the pressures and opportunities emanating from the Wall Street casino fostered by the Fed.

During that same period, IBM invested a mere $45 billion in CapEx, and that was hardly 90% of its charges for depreciation and amortization of existing capital assets. Given the fact that Capex is measured in current dollars, and D&A allowances are expressed in historical dollars, it is evident that in real terms IBM has been drastically underinvesting in its capital base.

Moreover, the same thing is true when the investment component that is charged to the current P&L is examined. As a giant in the global technology industry, IBM needs to spend heavily on research, development and engineering (RD&E) to keep up with the competition. But it hasn’t. During fiscal 2013 it spent $6.2 billion on RD&E—but that represented a 14% decline in real terms from the $7.2 billion (2013$) it spent ten years ago.

So how has it managed to keep the game going? In a word, by means of financial engineering. Its tax rate has been cut in half—from 30% to barely 15%. It has spent nearly $30 billion on acquisitions, repeatedly creating accounting reserves (i.e. cookie jars) at the get-go in order to insure that the dozens of small companies bought with cheap debt were highly accretive to EPS.

But at the end of the day, it was done by sacrificing its balance sheet. In 2004 IBM had $13 billion of net debt. Today the figure stands at just under $37 billion. And why not. IBM’s average weighted cost of debt last year was just shy of 1%. Thank you, monetary politburo!

Needless to say, under a honest free market in the financial sector, America’s once greatest technology company would not be functioning as a slush fund for Wall Street gamblers.

The Wall Street shysters have no morality, conscience or humanity. They are nothing but blood sucking parasites. Their sole purpose is to enrich themselves, while impoverishing their hosts (clients & customers). They destroyed the lives of millions with their fraudulent subprime housing scheme and were bailed out by the very people they screwed. Their hubris and arrogance knows no bounds. With encouragement from their captured central bank and the Obama administration, they are resorting to subprime fraud again in an effort to revive our dead economy. It worked so well the first time with houses, it will surely work a second time with automobiles. They prey upon the ignorant, stupid, and math challenged masses.

The entire engineered auto “recovery” is nothing but an easy money debt financed fraud. It will end in tears for millions and the government will insist you bail out the bankers again.

In a Subprime Bubble for Used Cars, Borrowers Pay Sky-High Rates

Rodney Durham stopped working in 1991, declared bankruptcy and lives on Social Security. Nonetheless, Wells Fargo lent him $15,197 to buy a used Mitsubishi sedan.

“I am not sure how I got the loan,” Mr. Durham, age 60, said.

Mr. Durham’s application said that he made $35,000 as a technician at Lourdes Hospital in Binghamton, N.Y., according to a copy of the loan document. But he says he told the dealer he hadn’t worked at the hospital for more than three decades. Now, after months of Wells Fargo pressing him over missed payments, the bank has repossessed his car.

This is the face of the new subprime boom. Mr. Durham is one of millions of Americans with shoddy credit who are easily obtaining auto loans from used-car dealers, including some who fabricate or ignore borrowers’ abilities to repay. The loans often come with terms that take advantage of the most desperate, least financially sophisticated customers. The surge in lending and the lack of caution resemble the frenzied subprime mortgage market before its implosion set off the 2008 financial crisis.

Auto loans to people with tarnished credit have risen more than 130 percent in the five years since the immediate aftermath of the financial crisis, with roughly one in four new auto loans last year going to borrowers considered subprime — people with credit scores at or below 640.

The explosive growth is being driven by some of the same dynamics that were at work in subprime mortgages. A wave of money is pouring into subprime autos, as the high rates and steady profits of the loans attract investors. Just as Wall Street stoked the boom in mortgages, some of the nation’s biggest banks and private equity firms are feeding the growth in subprime auto loans by investing in lenders and making money available for loans.

And, like subprime mortgages before the financial crisis, many subprime auto loans are bundled into complex bonds and sold as securities by banks to insurance companies, mutual funds and public pension funds — a process that creates ever-greater demand for loans.

The New York Times examined more than 100 bankruptcy court cases, dozens of civil lawsuits against lenders and hundreds of loan documents and found that subprime auto loans can come with interest rates that can exceed 23 percent. The loans were typically at least twice the size of the value of the used cars purchased, including dozens of battered vehicles with mechanical defects hidden from borrowers. Such loans can thrust already vulnerable borrowers further into debt, even propelling some into bankruptcy, according to the court records, as well as interviews with borrowers and lawyers in 19 states.

In another echo of the mortgage boom, The Times investigation also found dozens of loans that included incorrect information about borrowers’ income and employment, leading people who had lost their jobs, were in bankruptcy or were living on Social Security to qualify for loans that they could never afford.

Photo

Credit

Many subprime auto lenders are loosening credit standards and focusing on the riskiest borrowers, according to the examination of documents and interviews with current and former executives from five large subprime auto lenders. The lending practices in the subprime auto market, recounted in interviews with the executives and in court records, demonstrate that Wall Street is again taking on very risky investments just six years after the financial crisis.

The size of the subprime auto loan market is a tiny fraction of what the subprime mortgage market was at its peak, and its implosion would not have the same far-reaching consequences. Yet some banking analysts and even credit ratings agencies that have blessed subprime auto securities have sounded warnings about potential risks to investors and to the financial system if borrowers fall behind on their bills.

Pointing to higher auto loan balances and longer repayment periods, the ratings agency Standard & Poor’s recently issued a report cautioning investors to expect “higher losses.” And a high-ranking official at the Office of the Comptroller of the Currency, which regulates some of the nation’s largest banks, has also privately expressed concerns that the banks are amassing too many risky auto loans, according to two people briefed on the matter. In a June report, the agency noted that “these early signs of easing terms and increasing risk are noteworthy.”

Despite such warnings, the volume of total subprime auto loans increased roughly 15 percent, to $145.6 billion, in the first three months of this year from a year earlier, according to Experian, a credit rating firm.

“It appears that investors have not learned the lessons of Lehman Brothers and continue to chase risky subprime-backed bonds,” said Mark T. Williams, a former bank examiner with the Federal Reserve.

In their defense, financial firms say subprime lending meets an important need: allowing borrowers with tarnished credits to buy cars vital to their livelihood.

Lenders contend that the risks are not great, saying that they have indeed heeded the lessons from the mortgage crisis. Losses on securities made up of auto loans, they add, have historically been low, even during the crisis.

Autos, of course, are very different than houses. While a foreclosure of a home can wend its way through the courts for years, a car can be quickly repossessed. And a growing number of lenders are using new technologies that can remotely disable the ignition of a car within minutes of the borrower missing a payment. Such technologies allow lenders to seize collateral and minimize losses without the cost of chasing down delinquent borrowers.

That ability to contain risk while charging fees and high interest rates has generated rich profits for the lenders and those who buy the debt. But it often comes at the expense of low-income Americans who are still trying to dig out from the depths of the recession, according to the interviews with legal aid lawyers and officials from the Federal Trade Commission and the Consumer Financial Protection Bureau, as well as state prosecutors.

While the pain from an imploding subprime auto loan market would be much less than what ensued from the housing crisis, the economy is still on relatively fragile footing, and losses could ultimately stall the broader recovery for millions of Americans.

Photo

Rodney Durham, 60, of Binghamton, N.Y., had his car repossessed.Credit Heather Ainsworth for The New York Times

The pain is far more immediate for borrowers like Mr. Durham, the unemployed car buyer from Binghamton, N.Y., who stopped making his loan payments in March, only five months after buying the 2010 Mitsubishi Galant. A spokeswoman for Wells Fargo, which declined to comment on Mr. Durham citing a confidentiality policy, emphasized that the bank’s underwriting is rigorous, adding that “we have controls in place to help identify potential fraud and take appropriate action.”

The Mitsubishi was repossessed last month, leaving Mr. Durham without a car. But his debt ordeal may not be over.

Some lenders go after borrowers like Mr. Durham for the debt that still remains after a repossessed car is sold, according to court filings. Few repossessed cars fetch enough when they are resold to cover the total loan, the court documents show. To get the remainder, some lenders pursue the borrowers, which can leave them shouldering debts for years after their cars are gone.

But for now, Mr. Durham, who is disabled, has a more immediate problem.

“I just can’t get around without my car,” he said.

The Brokers

Outside, the banner proclaimed: “No Credit. Bad Credit. All Credit. 100 percent approval.” Inside the used-car dealership in Queens, N.Y., Julio Estrada perfected his sales pitches for the borrowers, including some immigrants who spoke little English.

Sure, the double-digit interest rates might seem steep, Mr. Estrada told potential customers, but with regular payments, they would quickly fall. Mr. Estrada, who sometimes went by John, and sometimes by Jay, promised others cash rebates.

If the soft sell did not work, he played hardball, threatening to keep the down payments of buyers who backed out, according to court documents and interviews with customers.

The salesman was ultimately indicted by the Queens district attorney on grand larceny charges that he defrauded more than 23 car buyers with refinancing schemes.

Relatively few used-car dealers are charged with fraud. Yet the extreme example of Mr. Estrada comes as some used-car dealers — a business that has long had a reputation for aggressive pitches — are pushing sales tactics too far, according to state prosecutors and federal regulators.

And these are among the thousands of used-car dealers who are working hand-in-hand with Wall Street to sell cars. Court records show that Capital One and Santander Consumer USA all bought loans arranged by Mr. Estrada, who pleaded guilty last year. Since then, Mr. Estrada was indicted on separate fraud charges in March by Richard A. Brown, the Queens district attorney. That case is still pending.

To guard against fraud, the banks say, they vet their dealer partners and routinely investigate complaints. Capital One has “rigorous controls in place to identify any potential issues,” said Tatiana Stead, a bank spokeswoman, adding that last year “we terminated our relationship with the dealership” where Mr. Estrada worked. Dawn Martin Harp, head of Wells Fargo Dealer Services, said that “it’s important to note that not all claims of dealer fraud turn out to be fraud.”

James Kousouros, Mr. Estrada’s lawyer, said that “for those individuals for whom Mr. Estrada bore responsibility, he accepted this and is committed to the restitution agreed to.” Some civil lawsuits filed by borrowers were found to be without merit, he said.

For their part, car dealers note that like any industry they sometimes have rogue employees, but add that customers are overwhelmingly treated fairly.

“There is no place for fraud or any other nefarious activities in the industry, especially tactics that seek to take advantage of vulnerable consumers,” said Steve Jordan, executive vice president of the National Independent Automobile Dealers Association.

In their role as matchmaker between borrowers and lenders, used-car dealers wield tremendous power. They make the pitch to customers, including many troubled borrowers who often believe that their options are limited. And the dealers outline the terms and rates of the loans.

In interviews, more than 40 low-income borrowers described how they were worn down by used car dealers who kept them in suspense for hours before disclosing whether they even qualified for a loan. The seemingly interminable wait, the borrowers said, left them with the impression that the loan — no matter how onerous the terms — was their only chance.

The loans also came with other costs, according to interviews and an examination of the loan documents, including add-on products like unusual insurance policies. In many cases, the examination by The Times found, borrowers ended up shouldering loans that far exceeded the resale value of the car. A reason for that disparity is that some borrowers still owe money on cars that they are trading in when they purchase a new one. That debt is then rolled over into the new loan.

“By the end, they are paying $600 a month for a piece of junk,” said Charles Juntikka, a bankruptcy lawyer in Manhattan.

The dealers have an incentive to increase both the size and the interest rate of the loans.

The arithmetic is simple. The bigger size and rate of the loan, the bigger the dealers’ profit, or so-called markup — the difference between the rate charged by the lenders and the one ultimately offered to the borrowers. Under federal law, dealers do not have to disclose the size of the markup.

Photo

Dolores Blaylock, 51, of Austin, Tex., and her father, Fidencio Muñiz, 84. Like many buyers, she found she had unwittingly purchased an add-on — in her case, a life insurance policy.Credit Erich Schlegel for The New York Times

To buy her 2004 Mazda van, Dolores Blaylock, 51, a home health care aide in Austin, Tex., said she unwittingly paid for a life insurance policy that would cover her loan payments if she died.

Her loan totaled $13,778 — nearly three times the value of the van that she uses to shuttle her father, who uses a wheelchair, to his doctor’s appointments.

Now, Ms. Blaylock says she regrets ever buying the van, which frequently breaks down. “I am afraid to drive it out of town,” she said.

In some cases, though, the tactics veer toward outright fraud. The Times’s scrutiny of loan documents, including some produced in litigation, found that some used-car dealers submitted loan applications to lenders that contained incorrect income and employment information. As was the case in the subprime mortgage boom, it is unclear whether borrowers provided incorrect information to qualify for loans or whether the dealers falsified loan applications. Whatever the cause, the result is the same: Borrowers with scant income qualified for loans.

Mary Bridges, a retired grocery store employee in Syracuse, N.Y., said she repeatedly explained to a car salesman that her only monthly income was about $1,200 in Social Security. Still, Ms. Bridges said that the salesman falsely listed her monthly income as $2,500 on the application for a car loan submitted by a local dealer to Wells Fargo and reviewed by The Times.

As a result, she got a loan of $12,473 to buy a 2004 used Buick LeSabre, currently valued by Kelley Blue Book at around half that much. She tried to keep up with the payments — even going on food stamps for the first time in her life — but ultimately the car was repossessed in 2012, just two years after she bought it.

“I have always been told to do the responsible thing, but I said, ‘This is too much,’ ” the 76-year-old widow said.

The dealer agreed to pay Ms. Bridges $1,000 after Syracuse University law students threatened to file a lawsuit accusing the company of violating state and federal consumer protection laws.

But Wells Fargo, which resold the car for $4,500 last July, is still pursuing Ms. Bridges for $2,900 — a total that includes her remaining loan balance and an $835 fee for “cost of repossession and sale,” according to a copy of a letter that Wells Fargo sent to Ms. Bridges last August. (Wells Fargo declined to comment on Ms. Bridges.)

Photo

Shahadat Tuhin, 42, with his daughter Sadia Oishika, 10. He says his auto dealer used deceptive practices.Credit Hiroko Masuike/The New York Times

Even when authorities have cracked down on dealers, borrowers are still vulnerable to fraud. Last June, Shahadat Tuhin, a New York City taxi driver, bought a car from Mr. Estrada, the salesman in Queens who less than a year earlier had been indicted.

The charge by the Queens district attorney didn’t keep him out of the business. While his criminal case was pending, the salesman persuaded Mr. Tuhin to buy a used car for 90 percent more than the price he agreed upon. Needing the car to take his daughter, who has a heart condition, to the doctor, Mr. Tuhin said he unwittingly signed for a $26,209 loan with completely different terms than the ones he had reviewed.

Immediately after discovering the discrepancies, Mr. Tuhin, 42, said he tried to return the car to the dealership and called the lender, M&T Bank, to notify them of the fraud.

The bank told him to take up the issue with the dealer, Mr. Tuhin said.

M&T declined to comment on Mr. Tuhin, but said it no longer does business with that dealership.

The Money

Investors, seeking a higher return when interest rates are low, recently flocked to buy a bond issue from Prestige Financial Services of Utah. Orders to invest in the $390 million debt deal were four times greater than the amount of available securities.

What is backing many of these securities? Auto loans made to people who have been in bankruptcy.

An affiliate of the Larry H. Miller Group of Companies, Prestige specializes in making the loans to people in bankruptcy, packaging them into securities and then selling them to investors.

“It’s been a hot space,” Richard L. Hyde, the firm’s chief operating officer, said during an interview in March. Investors are betting on risky borrowers. The average interest rate on loans bundled into Prestige’s latest offering, for example, is 18.6 percent, up slightly from a similar offering rolled out a year earlier. Since 2009, total auto loan securitizations have surged 150 percent, to $17.6 billion last year, though some estimates have put the total volume even higher. To meet that rising demand, Wall Street snatches up more and more loans to package into the complex investments.

Much like mortgages, subprime auto loans go through Wall Street’s securitization machine: Once lenders make the loans, they pool thousands of them into bonds that are sold in slices to investors like mutual funds, pensions and hedge funds. The slices that include loans to the riskiest borrowers offer the highest returns.

Rating agencies, which assess the quality of the bonds, are helping fuel the boom. They are giving many of these securities top ratings, which clears the way for major investors, from pension funds to employee retirement accounts, to buy the bonds. In March, for example, Standard & Poor’s blessed most of Prestige’s bond with a triple-A rating. Slices of a similar bond that Prestige sold last year also fetched the highest rating from S.&P. A large slice of that bond is held in mutual funds managed by BlackRock, one of the world’s largest money managers.

Private equity firms have also seen the opportunity in auto subprime lending. A $1 billion investment by Kohlberg Kravis Roberts & Co., Centerbridge Partners and Warburg Pincus in a large subprime lender roughly doubled in about two years. Typically, it takes private equity firms three to five years to reap significant profit on their investments.

It is not just the private equity firms and large banks that are fanning the lending boom. Major insurance companies and mutual funds, which manage money on behalf of mom-and-pop investors, are also snapping up securities backed by subprime auto loans.

While there are no exact measures of how many of these loans end up on banks’ balance sheets, interviews with consumer lawyers and analysts suggest the problem is spreading, propelled by the very structure of the subprime auto market.

The vast majority of banks largely rely on dealers to screen potential borrowers. The arrangement, which means the banks rarely meet customers face to face, mirrors how banks relied on brokers to make mortgages.

In some cases, consumer lawyers say, the banks actually ignore complaints by borrowers who accuse dealers of fabricating their income or even forging their signatures.

“Even when they are presented with clear evidence of fraud, the banks ignore it,” said Peter T. Lane, a consumer lawyer in New York. “The typical refrain is, ‘It’s not our problem, take it up with the dealer.’ ”

It could quickly become the banks’ problem, analysts say, if questionable loans sour, causing losses to multiply.

For now, the banks are not pulling back. Many are barreling further into the auto loan market to help recoup the billions in revenue wiped out by regulations passed after the 2008 financial crisis.

Wells Fargo, for example, made $7.8 billion in auto loans in the second quarter, up 9 percent from a year earlier. At a presentation to investors in May, Wells Fargo said it had $52.6 billion in outstanding car loans. The majority of those loans are made through dealerships. The bank also said that as of the end of last year, 17 percent of the total auto loans went to borrowers with credit scores of 600 or less. The bank currently ranks as the nation’s second-largest subprime auto lender, behind Capital One, according to J. D. Power & Associates.

Wells Fargo executives say that despite the surge, the credit quality of its loans has not slipped. At the May presentation, Thomas A. Wolfe, the head of Wells Fargo Consumer Credit Solutions, emphasized that the overall quality of its auto loans was improving. And Tatiana Stead, the Capital One spokeswoman, said that Capital One worked “to ensure we do not follow the market to pursue growth for growth’s sake.”

Prestige says its loans experience relatively low losses because borrowers have discharged many of their other debts in bankruptcy, freeing up more cash for their car payments. Another advantage for the lender: No matter how tough things get for troubled borrowers, federal law prevents them from escaping their bills through bankruptcy for at least another seven years.

“The vast majority of our customers have been successful with their loans and leave us with a much higher credit score,” said Mr. Hyde, Prestige’s chief operating officer.

The Risks

All it took was three months.

Dolores Jackson, a teacher’s aide in Jersey City, says she thought she could handle the $540 a month on the 2012 Chevy Malibu she bought in January 2013.

But the payments on the $27,140 loan from Exeter Finance, which is owned by Blackstone, quickly overwhelmed her, and she prepared to declare bankruptcy in April.

“I was drowning,” she said.

Other borrowers have also found themselves quickly overwhelmed by car loan payments.

Even after getting a second job at Staples, Alicia Saffold, 24, a supply technician at the Fort Benning military base in Georgia, could not afford the monthly payments on her $14,288.75 loan from Exeter. The loan, according to a copy of her loan document reviewed by The Times, came with an interest rate of nearly 24 percent. Less than a year after she bought the gray Pontiac G6, it was repossessed.

Photo

Marcelina and Jonathan Mojica, and their dog, Lilly. “The car gets more money than what we put in our fridge,” Mr. Mojica said.Credit Damon Winter/The New York Times

In the case of Marcelina Mojica and her husband, Jonathan, they are keeping up with their payments on their $19,313.45 Wells Fargo auto loan — but just barely. They are currently living in a homeless shelter in the Bronx.

“The car gets more money than what we put in our fridge,” said Mr. Mojica, 28. Such examples of distress underscore the broader strains within the subprime auto loan market.

Exeter Finance declined to comment on Ms. Saffold or Ms. Jackson, but Blackstone, its parent company, emphasized that the credit quality of its lender’s loans was improving and that it worked hard to ensure its customers received the best rates. To ensure the accuracy of loan documents, Blackstone said, employees vet both dealers and borrowers.

“Exeter Finance believes it’s important to provide people with the option to finance transportation essential to their livelihood,” said Mark Floyd, the company’s chief executive.

Still, financial firms are beginning to see signs of strain. In the first three months of this year, banks had to write off as entirely uncollectable an average of $8,541 of each delinquent auto loan, up about 15 percent from a year earlier, according to Experian.

Some investors think the time is right to start selling their holdings. Earlier this year, for example, private equity firms, including K.K.R., sold most of their stake in the subprime auto lender, Santander Consumer USA, when the lender went public. Since the company’s initial public offering, the stock has fallen more than 16 percent.

While losses from soured car loans would be far less than those on subprime mortgages, the red ink could still deal a blow to the banks not long after they recovered from the housing bust. Losses from auto loans might also cause the banks to further retrench from making other loans vital to the economic recovery, like those to small business and would-be homeowners.

In another sign of trouble ahead, repossessions, while still relatively low, increased nearly 78 percent to an estimated 388,000 cars in the first three months of the year from the same period a year earlier, according to the latest data provided by Experian. The number of borrowers who are more than 60 days late on their car payments also jumped in 22 states during that period.

As a result, some rating agencies, even those that had blessed auto loan securitizations with high ratings, are starting to question the quality of the loans backing those securities, and warn of losses that investors could suffer if the bonds start to sour. Describing the potential trouble ahead, Kevin Cole, an analyst with Standard & Poor’s, said, “We believe these trends could lead to higher losses and weakened profitability in a few years.”

If those losses materialize, they could pummel a wide range of investors, from pension funds to insurance companies to mutual funds held by Americans preparing for retirement. For the huge baby-boomer generation, including many whose savings were sapped by the 2008 crisis and the ensuing recession, any losses from the auto loan securities could deal them another setback.

“Borrowers are haunted by this debt, and it can crater their credit scores, prevent them from getting other loans and thrust them even further onto the financial margins,” said Ahmad Keshavarz, a consumer lawyer in New York.

Some borrowers are stuck making payments on loans that were fraudulently made by dealers, according to an examination of dozens of lawsuits against dealers. There are no exact measures of just how many people whose cars have been repossessed end up in this predicament, but lawyers for borrowers say that it is a growing problem, and one that points to another element of subprime auto lending.

Thanks to an amendment to the Dodd-Frank financial overhaul, the vast majority of dealers are not overseen by the Consumer Financial Protection Bureau. Since its start in 2010, the agency has earned a reputation for aggressively penalizing lenders, but it has limited authority over dealers.

The Federal Trade Commission, the agency that does oversee the dealers, has cracked down on certain questionable practices. And although the agency has won a number of cases against dealers for failing to accurately disclose car costs and other abuses, it has not taken aim at them for falsifying borrowers’ incomes, for example.

Photo

Alicia Saffold, 24, received a loan with an interest rate of nearly 24 percent. Her car was soon repossessed.Credit Tami Chappell for The New York Times

And the help is not coming fast enough for borrowers like Mr. Durham, the retiree in Binghamton; Mr. Tuhin, the taxi driver in Queens; or Ms. Saffold, the technician in Georgia.

“Buying the car was the worst decision I have ever made,” Ms. Saffold said.

Applications for mortgages to purchase a house are 17% below last years level. They are 30% below levels in 2009/2010 during the depths of the recession. They are 12% below the level of 2012 when national home prices bottomed out.

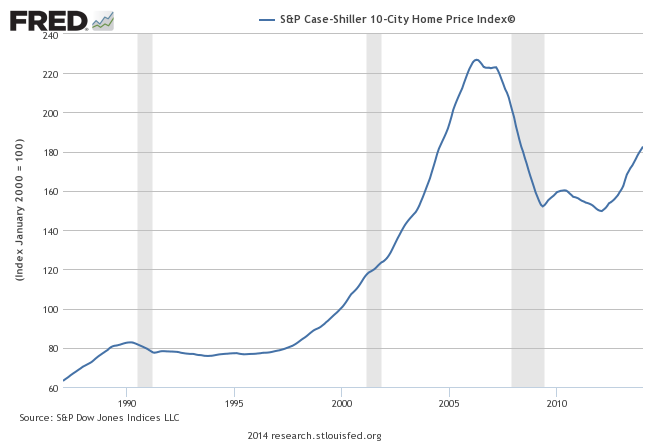

The Case Shiller price index is up 25% from its low and is now back to mid-2008 levels. In mid-2008 mortgage applications to purchase homes were 100% higher than they are today. So we have mortgage applications dramatically lower since 2008, now at levels seen in 1997, but home prices have been driven 25% higher in the last two years. How could that be?

The chart below provides the reason. It’s certainly not growth in real household income, as that has plunged by 8% since 2008 and remains stagnant. Average hourly wages haven’t moved upwards in five years. How can people buy homes when their income is falling? They can’t.

The yellow line tells the story. Helicopter Ben and Bubbles Janet have printed fiat at a phenomenal rate and shoveled it into the troughs of their Wall Street owner pigs. The Wall Street shysters then created a fake housing shortage by withholding foreclosures from the housing inventory while buying up millions of homes in their own to rent scheme. Throw in the Chinese laundering their ill-gotten cash by buying up luxury real estate, and you’ve got a 25% increase in home prices.

Would a spineless, captured politician in Congress dare ask Bubbles Yellen about this immoral, criminal, treasonous act against the American people? Not a chance. So keep believing the economy is recovering, jobs are being created and the housing market is in great shape. The wealth of the oligarch pigs depends upon it.

I wrote an article titled AVAILABLE 15 months ago about the increasing number of Space Available signs in my supposedly upscale Montgomery County, PA.

We supposedly have the same number of people employed today as we did in the fourth quarter of 2007. This is 7 million more than were employed in late 2010.

If this is a real economic recovery, why is there still 68.2 million square feet less occupied office space than there was in 2007? Could it be because the shit jobs added during the Obama “recovery” aren’t well paying office jobs, but crappy retail, fast food, and “self employment” jobs?

My suspicions are confirmed by the chart below. The space available has grown by 120.7 million square feet since 2007, and continues to grow. Can you believe developers continue to build new office space, when this much is available? Can you believe office rent prices have risen by 7.2% since 2010? How can this be?

Look no further than your friends at the Federal Reserve. Zero interest rates allow bankrupt developers to pretend they are solvent. The Fed has allowed banks to “restructure” developer loans, pretending they will eventually make their interest and principle payment with the rent they are pretending to receive from phantom tenants. The extremely low interest rates has resulted in the mal-investment of funds into building more office space. Easy money and accounting fraud can do wonders, for awhile. There is no recovery. There are no new tenants. The space available signs continue to proliferate. How long can negative cash flow be sustained by developers as businesses shut down, while retailers and restaurants go dark?

And now for the really bad news. REIS is a property company skewing the data as positive as possible. Those charts are only for the 79 largest metropolitan areas in the country. And they are only for Class A buildings. If you were to include Class B and Class C buildings in all the markets in the U.S. you would find the true vacancy rate to be in excess of 30%.

As you drive around your neck of the woods, play a little game. Count the number of Space Available signs along your route and calculate whether the true vacancy rate is closer to 17% or 30%.

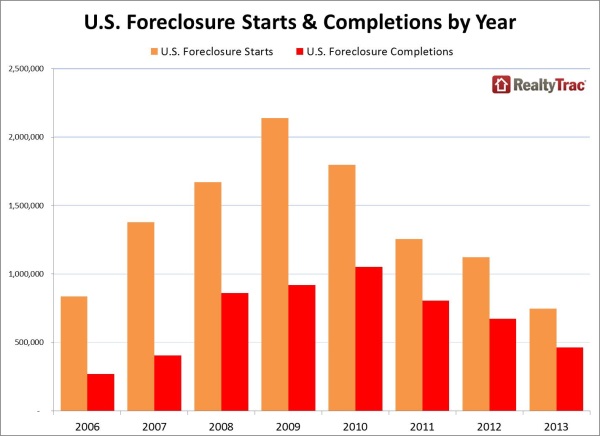

So far we have experienced 7 million foreclosures. Beyond that there are still 9 million homeowners seriously underwater on their mortgages and there are millions more who are stranded in place because they don’t have enough positive equity to cover transactions costs and more stringent down payment requirements.

And that’s before the next down-turn in housing prices—a development which will show-up any day. In fact, another downward plunge is a positive certainty now that the buy-to-rent LBO speculators are rapidly pulling out of those “flash” bull markets in Arizona, California, Los Vegas, Florida and elsewhere. The latter were merely short-lived price eruptions which were an artifact of the Fed’s free money policies.

Yet even as Wall Street heads out of Dodge City the normal wave of organic buyers is nowhere to be seen. That’s because the inexorable normalization of interest rates is already beginning to drive housing affordability even further south among the diminishing cohort of buy-to-occupy households with sufficient income to meet today’s financing standards.

Among the latter, incomes are stagnant in real terms and have been so for a decade. In the absence of real income gains, therefore, the “affordable” price of housing is essentially an inverse function of the cost of leveraged carry. As the latter goes up, the former goes down.

In short, the socio-economic mayhem implicit in the graph below is not the end of the line or a one-time nightmare that has subsided and is now working its way out of the system as the Kool-Aid drinkers would have you believe based on the “incoming data” conveyed in the chart. Instead, the serial bubble makers in the Eccles Building have already laid the ground-work for the next up-welling of busted mortgages, home foreclosures and the related wave of disposed families and social distress.

Yet none of this carnage was inexorable or necessary. In fact, a housing bubble of the fantastic magnitude that unfolded during the Greenspan era could not occur on the free market. The 3X gain in housing prices between 1994 and 2007 was entirely an artifact of the massive outpouring of cheap mortgage debt that occurred during that period. The latter, in turn, is a consequence of the Fed’s financial repression policies—–maneuvers that disable and paralyze market interest rates and thereby enable runaway speculations fueled by virtually unlimited cheap debt.

Case Shiller Index – Click to enlarge

Oddly enough, even the baby-steps toward normalization of interest rates recently taken by the Fed make it easy to benchmark the monumental scale of the mortgage bubble ignited by the Maestro’s abject capitulation to Wall Street after the Bush Republicans gained the White House in December 2000. On an all-in basis, Greenspan’s reckless money printing increased mortgage volumes by up to 5X what would have prevailed in an honest free market.

As I laid out in chapter 20 of the Great Deformation (“How The Fed Brought The Gambling Mania To America’s Neighborhoods”), during the 30 months after the Fed’s first bubble splattered—the dotcom crash—-Greenspan foolishly cut money market interest rates over and over until the 6.5% cost of money on Christmas eve 2000 had been reduced to 1% by June 2003. Never before in the Fed’s 100-year history had rates been reduced by 85% in such a short interval with such reckless abandon.

Not surprisingly, variable rate mortgage issuance exploded because teaser interest rates plummeted to lower levels than even during the Great Depression. Whereas mortgage issuance had rarely topped $1 trillion in earlier years, the run rate of issuance topped $5 trillion during the second quarter of 2003.

Such a massive explosion of ultra-cheap mortgage debt was guaranteed to elicit a frenzy of speculation in residential housing. Indeed, as is evident in the chart above during the roughly 60 months after Greenspan’s panicky rate reductions incepted, the national housing price index doubled.

The great Fed Chairman of yester-year like William McChesney Martin and Paul Volcker would have been appalled by such an outbreak of speculation and would not have hesitated to pick up the punchbowl and march straight out of the party. That’s what Martin did in August 1958 when he suspected too much speculation on Wall Street only six months after a business recovery had started.

But Greenspan had by then been coroneted as the Maestro and proceeded to prove exactly why monetary central planning is such a dangerous doctrine. When it became evident that large amounts of this massive outpouring of mortgage debt were being used as “cash-out” financing and applied to current spending on new carpets, autos and Caribbean cruises, Greenspan pronounced this destructive raid by mortgage borrowers on their own home equity nest-eggs as a fabulous new advance in financial innovation called “mortgage equity withdrawal”. It would even outdo Keynes: the people, not their government, would imbibe the magic elixir of more debt, and thereby generate more spending, income and economic growth.

In truth, America’s baby-boom generation was robbing its own future retirement years, but the Maestro was oblivious. Instead, he was busy tracking the quarterly rate of MEW (“mortgage equity withdrawal”) and crowing about how it was contributing to unprecedented prosperity on Main Street. It ended up in a conflagration of exploitive lending, fraud, default and trillions of financial losses, of course, but not until $5 trillion of cumulative MEW during the decade through 2007 had ruined the financial well-being of America’s middle class for a generation to come.

Under a regime of free market interest rates $5 trillion of MEW—that is, robbing from the future to party today—could not have happened. Long before the 2003-2006 blow-off top, mortgage interest rates would have soared to double digit levels, causing monthly debt service requirements to double or triple. Moreover, in an environment of market-set interest rates there would have been no Greenspan Put or ultra cheap wholesale financing that enabled Wall Street to fund mortgage boiler shops with warehouse credit lines and buyers of its toxic securitization products with cheap repo.

In short, free market interest rates are the vital check and balance mechanism which prevents runaway spirals of debt issuance and frenzied bidding-up of asset prices. Yet it was Greenspan’s “wealth effects” doctrine that destroyed the mechanism of honest price discovery once and for all. The carnage that has ensued in the nation’s credit and housing markets, therefore, is on you, Alan Greenspan.

The outcome of the Bernanke money printing spree of 2008-2013 provides even further evidence of Greenspan’s original culpability. During that five-year period, the Fed drove the 30-year mortgage rate from 6.5% to a low of 3.3%, thereby trigging a renewed wave of “refi madness” as shown below:

Since the spring of 2013 when the Fed signaled that its massive bond purchases would enter the “taper”, however, the mortgage rate has rebounded to about 4.5%. Accordingly, about 35% of the Bernanke repression has already been retraced and even that modest start toward interest rate normalization has had dramatic impacts on mortgage volumes.

The mortgage refi machine is now virtually shutdown, meaning that the run rate of mainly purchase money mortgage originations has plummeted to about a $1 trillion per year. So the math is pretty basic: During much of the Greenspan housing bubble the mortgage origination rate was $3-4 trillion annually—a level dramatically above what is being generated right now in a market that has taken only a baby step toward normalization.

Needless to say, it was this massive and artificial excess of mortgage financing that created the original Greenspan housing bubble; that induced his successor to try to overcome the carnage of the bust with a new round of refi madness; and that has now left the nation’s residential housing market high and dry for the fourth time since 1990.

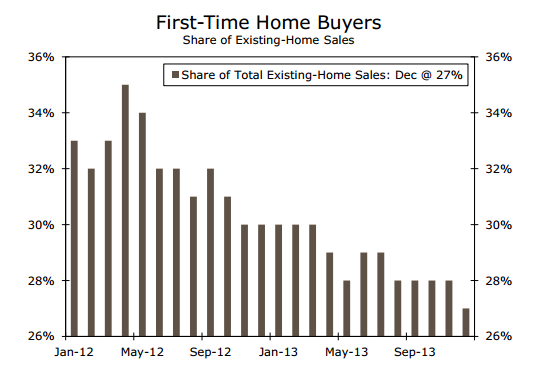

As shown below, this short-term flash boom in housing prices induced by Bernanke’s money printing spree has driven first time buyers out of the market. And now more and more “trade-up” buyers will be forced out too— as they face steadily higher interest rates on new purchase mortgages and therefore progressively lower levels of home price affordability:

So the housing market is on the eve of another trip through the grinder of falling prices, rising defaults and spreading socio-economic distress on Main Street. Yet because the Fed gets away with ludicrous excuses about the mayhem it causes—such as Greenspan’s pathetic claim that the housing bubble was caused by the propensity of ex-rural serfs in China to save too much when they moved into the factory cities— the debilitating cycle of bubble finance goes on.

As this recent Wall Street Journal story so starkly conveys—policy makers and lenders are so desperate to restart a new round of phony housing finance that the 3% down mortgage is already back, and 10,000 pages of Dodd-Frank regulations have done nothing so stop it:

One such lender is TD Bank, Toronto Dominion’s U.S. unit, which on Friday began accepting down payments as low as 3% through an initiative called “Right Step,” geared toward first-time buyers and low- and moderate-income buyers.

I’m sure this is a coincidence. The Fed and their Wall Street puppet masters certainly don’t coordinate their buying, selling, and suppression of gold prices. That would be immoral and wrong, just like front running customers with HFT supercomputers. They would never do that. 🙂

And people wonder why bankers are hated. Real median household income is lower than it was in 1999. Wages are stagnant. Young people are stuck with a trillion dollars of student loan debt and part time jobs at TGI Fridays. Average Americans don’t have money left to consume, so retailers are being destroyed and closing thousands of stores.

Too Big To Trust Wall Street Mega-Banks have been handed billions of newly printed dollars on a daily basis by the their wholly owned central bank to gamble with no risk of loss. They can borrow at 0% from this same central bank and then deposit those funds back with the central bank to earn .25%. This generates billions in risk free profits.

These same banks can mark the toxic loans on their balance sheet at whatever they choose. This allows them to release billions of loan loss reserves every quarter, generating accounting entry profits. They have no interest in making loans to small businesses or little people. That’s old school banking. Gambling with derivatives knowing the Fed has their back is how it’s done today.

What a business model. These parasites on the ass of America add absolutely no value to society. NONE. They have destroyed our economic system and won’t be satisfied until it is a smoking ruin. For this they reward themselves with $26.7 billion of bonuses for a job well done. There aren’t enough lampposts for what needs to be done.

Wall Street bonuses rose 15% in 2013 to post-financial-crisis high

The average person working in the securities industry earned a cool $164,530 bonus last year — 15% more than a year before.

An aggregate $26.7 billion was paid out in 2013 bonuses to the industry’s 165,200 employees, the highest figure since the 2008 financial crisis, according to figures released Wednesday by New York State Comptroller Thomas P. DiNapoli.

To put that bonus-pool figure in perspective, it would be enough to more than double the pay of the more than 1 million full-time workers earning the federal minimum wage, which is currently $7.25 per hour, according to the Institute for Policy Studies.

The bonus increase on Wall Street is a result of firms’ engaging in deferred compensation, according to the comptroller’s report. Financial firms are now paying out a smaller share of bonuses immediately and are instead deferring a larger share into future years.

DiNapoli’s office noted that the securities industry “navigated through some rough patches last year” and yet was profitable. “Although profits were lower than the prior year, the industry still had a good year in 2013 despite costly legal settlements and higher interest rates,” said DiNapoli. “Wall Street continues to demonstrate resilience as it evolves in a changing regulatory environment.”

Major regulatory reforms since the financial crisis have changed the way the industry does business. Firms are now required to maintain larger reserves, and proprietary trading has been limited, while additional changes are aimed at reducing unnecessary risk and enhancing transparency, the report notes.

The statue of the Wall Street Bull, on Bowling Green in New York

Several firms, including J.P. Morgan Chase & Co. JPM and Citigroup Inc. C, have indicated weakness in these areas.

Total Wall Street profits for the broker-dealer operations of New York Stock Exchange member firms were $16.7 billion in 2013, the comptroller’s office said.

Other nuggets gleaned from the report:

• The average salary, including bonuses, paid to securities-industry employees in New York City in 2012 was 5.2 times the average pay in the rest of the private sector, which was about $69,200 as of 2012.

• The securities industry, considered one of the city’s major economic engines, accounts for 22% of all private-sector wages paid in New York, despite accounting for just 5% of the city’s private-sector jobs.

“I was part of that strange race of people aptly described as spending their lives doing things they detest, to make money they don’t want, to buy things they don’t need, to impress people they don’t like.” ― Emile Gauvreau

If ever a chart provided unequivocal proof the economic recovery storyline is a fraud, the one below is the smoking gun. November and December retail sales account for 20% to 40% of annual retail sales for most retailers. The number of visits to retail stores has plummeted by 50% since 2010. Please note this was during a supposed economic recovery. Also note consumer spending accounts for 70% of GDP. Also note credit card debt outstanding is 7% lower than its level in 2010 and 16% below its peak in 2008. Retailers like J.C. Penney, Best Buy, Sears, Radio Shack and Barnes & Noble continue to report appalling sales and profit results, along with listings of store closings. Even the heavyweights like Wal-Mart and Target continue to report negative comp store sales. How can the government and mainstream media be reporting an economic recovery when the industry that accounts for 70% of GDP is in free fall? The answer is that 99% of America has not had an economic recovery. Only Bernanke’s 1% owner class have benefited from his QE/ZIRP induced stock market levitation.

The entire economic recovery storyline is a sham built upon easy money funneled by the Fed to the Too Big To Trust Wall Street banks so they can use their HFT supercomputers to drive the stock market higher, buy up the millions of homes they foreclosed upon to artificially drive up home prices, and generate profits through rigging commodity, currency, and bond markets, while reducing loan loss reserves because they are free to value their toxic assets at anything they please – compliments of the spineless nerds at the FASB. GDP has been artificially propped up by the Federal government through the magic of EBT cards, SSDI for the depressed and downtrodden, never ending extensions of unemployment benefits, billions in student loans to University of Phoenix prodigies, and subprime auto loans to deadbeats from the Government Motors financing arm – Ally Financial (85% owned by you the taxpayer). The country is being kept afloat on an ocean of debt and delusional belief in the power of central bankers to steer this ship through a sea of icebergs just below the surface.

The absolute collapse in retail visitor counts is the warning siren that this country is about to collide with the reality Americans have run out of time, money, jobs, and illusions. The most amazingly delusional aspect to the chart above is retailers continued to add 44 million square feet in 2013 to the almost 15 billion existing square feet of retail space in the U.S. That is approximately 47 square feet of retail space for every person in America. Retail CEOs are not the brightest bulbs in the sale bin, as exhibited by the CEO of Target and his gross malfeasance in protecting his customers’ personal financial information. Of course, the 44 million square feet added in 2013 is down 85% from the annual increases from 2000 through 2008. The exponential growth model, built upon a never ending flow of consumer credit and an endless supply of cheap fuel, has reached its limit of growth. The titans of Wall Street and their puppets in Washington D.C. have wrung every drop of faux wealth from the dying middle class. There are nothing left but withering carcasses and bleached bones.

The impact of this retail death spiral will be vast and far reaching. A few factoids will help you understand the coming calamity:

There are approximately 109,500 shopping centers in the United States ranging in size from the small convenience centers to the large super-regional malls.

There are in excess of 1 million retail establishments in the United States occupying 15 billion square feet of space and generating over $4.4 trillion of annual sales. This includes 8,700 department stores, 160,000 clothing & accessory stores, and 8,600 game stores.

U.S. shopping-center retail sales total more than $2.26 trillion, accounting for over half of all retail sales.

The U.S. shopping-center industry directly employed over 12 million people in 2010 and indirectly generated another 5.6 million jobs in support industries. Collectively, the industry accounted for 12.7% of total U.S. employment.

Total retail employment in 2012 totaled 14.9 million, lower than the 15.1 million employed in 2002.

For every 100 individuals directly employed at a U.S. regional shopping center, an additional 20 to 30 jobs are supported in the community due to multiplier effects.

The collapse in foot traffic to the 109,500 shopping centers that crisscross our suburban sprawl paradise of plenty is irreversible. No amount of marketing propaganda, 50% off sales, or hot new iGadgets is going to spur a dramatic turnaround. Quarter after quarter there will be more announcements of store closings. Macys just announced the closing of 5 stores and firing of 2,500 retail workers. JC Penney just announced the closing of 33 stores and firing of 2,000 retail workers. Announcements are imminent from Sears, Radio Shack and a slew of other retailers who are beginning to see the writing on the wall. The vacancy rate will be rising in strip malls, power malls and regional malls, with the largest growing sector being ghost malls. Before long it will appear that SPACE AVAILABLE is the fastest growing retailer in America.

The reason this death spiral cannot be reversed is simply a matter of arithmetic and demographics. While arrogant hubristic retail CEOs of public big box mega-retailers added 2.7 billion retail square feet to our already over saturated market, real median household income flat lined. The advancement in retail spending was attributable solely to the $1.1 trillion increase (68%) in consumer debt and the trillion dollars of home equity extracted from castles in the sky, that later crashed down to earth. Once the Wall Street created fraud collapsed and the waves of delusion subsided, retailers have been revealed to be swimming naked. Their relentless expansion, based on exponential growth, cannibalized itself, new store construction ground to a halt, sales and profits have declined, and the inevitable closing of thousands of stores has begun. With real median household income 8% lower than it was in 2008, the collapse in retail traffic is a rational reaction by the impoverished 99%. Americans are using their credit cards to pay their real estate taxes, income taxes, and monthly utilities, since their income is lower, and their living expenses rise relentlessly, thanks to Bernanke and his Fed created inflation.

The media mouthpieces for the establishment gloss over the fact average gasoline prices in 2013 were the second highest in history. The highest average price was in 2012 and the 3rd highest average price was in 2011. These prices are 150% higher than prices in the early 2000’s. This might not matter to the likes of Jamie Dimon and Jon Corzine, but for a middle class family with two parents working and making 7.5% less than they made in 2000, it has a dramatic impact on discretionary income. The fact oil prices have risen from $25 per barrel in 2003 to $100 per barrel today has not only impacted gas prices, but utility costs, food costs, and the price of any product that needs to be transported to your local Wally World. The outrageous rise in tuition prices has been aided and abetted by the Federal government and their doling out of loans so diploma mills like the University of Phoenix can bilk clueless dupes into thinking they are on their way to an exciting new career, while leaving them jobless in their parents’ basement with a loan payment for life.

The laughable jobs recovery touted by Obama, his sycophantic minions, paid off economist shills, and the discredited corporate legacy media can be viewed appropriately in the following two charts, that reveal the false storyline being peddled to the techno-narcissistic iGadget distracted masses. There are 247 million working age Americans between the ages of 18 and 64. Only 145 million of these people are employed. Of these employed, 19 million are working part-time and 9 million are self- employed. Another 20 million are employed by the government, producing nothing and being sustained by the few remaining producers with their tax dollars. The labor participation rate is the lowest it has been since women entered the workforce in large numbers during the 1980’s. We are back to levels seen during the booming Carter years. Those peddling the drivel about retiring Baby Boomers causing the decline in the labor participation rate are either math challenged or willfully ignorant because they are being paid to be so. Once you turn 65 you are no longer counted in the work force. The percentage of those over 55 in the workforce has risen dramatically to an all-time high, as the Me Generation never saved for retirement or saw their retirement savings obliterated in the Wall Street created 2008 financial implosion.

To understand the absolute idiocy of retail CEOs across the land one must parse the employment data back to 2000. In the year 2000 the working age population of the U.S. was 213 million and 136.9 million of them were working, a record level of 64.4% of the population. There were 70 million working age Americans not in the labor force. Fourteen years later the number of working age Americans is 247 million and only 144.6 million are working. The working age population has risen by 16% and the number of employed has risen by only 5.6%. That’s quite a success story. Of course, even though median household income is 7.5% lower than it was in 2000, the government expects you to believe that 22 million Americans voluntarily left the labor force because they no longer needed a job. While the number of employed grew by 5.6% over fourteen years, the number of people who left the workforce grew by 31.1%. Over this same time frame the mega-retailers that dominate the landscape added almost 3 billion square feet of selling space, a 25% increase. A critical thinking individual might wonder how this could possibly end well for the retail genius CEOs in glistening corporate office towers from coast to coast.

This entire materialistic orgy of consumerism has been sustained solely with debt peddled by the Wall Street banking syndicate. The average American consumer met their Waterloo in 2008. Bernanke’s mission was to save bankers, billionaires and politicians. It was not to save the working middle class. You’ve been sacrificed at the altar of the .1%. The 0% interest rates were for Jamie Dimon and Lloyd Blankfein. Your credit card interest rate remained between 13% and 21%. So, while you struggle to pay bills with your declining real income, the Wall Street bankers are again generating record profits and paying themselves record bonuses. Profits are so good, they can afford to pay tens of billions in fines for their criminal acts, and still be left with billions to divvy up among their non-prosecuted criminal executives.

Bernanke and his financial elite owners have been able to rig the markets to give the appearance of normalcy, but they cannot rig the demographic time bomb that will cause the death and destruction of our illusory retail paradigm. Demographics cannot be manipulated or altered by the government or mass media. The best they can do is ignore or lie about the facts. The life cycle of a human being is utterly predictable, along with their habits across time. Those under 25 years old have very little income, therefore they have very little spending. Once a job is attained and income levels rise, spending rises along with the increased income. As the person enters old age their income declines and spending on stuff declines rapidly. The media may be ignoring the fact that annual expenditures drop by 40% for those over 65 years old from the peak spending years of 45 to 54, but it doesn’t change the fact. They also cannot change the fact that 10,000 Americans will turn 65 every day for the next sixteen years. They also can’t change the fact the average Baby Boomer has less than $50,000 saved for retirement and is up to their grey eye brows in debt.

With over 15% of all 25 to 34 year olds living in their parents’ basement and those under 25 saddled with billions in student loan debt, the traditional increase in income and spending is DOA for the millennial generation. The hardest hit demographic on the job front during the 2008 through 2014 ongoing recession has been the 45 to 54 year olds in their peak earning and spending years. Combine these demographic developments and you’ve got a perfect storm for over-built retailers and their egotistical CEOs.

The media continues to peddle the storyline of on-line sales saving the ancient bricks and mortar retailers. Again, the talking head pundits are willfully ignoring basic math. On-line sales account for 6% of total retail sales. If a dying behemoth like JC Penney announces a 20% decline in same store sales and a 20% increase in on-line sales, their total change is still negative 17.6%. And they are still left with 1,100 decaying stores, 100,000 employees, lease payments, debt payments, maintenance costs, utility costs, inventory costs, and pension costs. Their future is so bright they gotta wear a toe tag.

The decades of mal-investment in retail stores was enabled by Greenspan, Bernanke, and their Federal Reserve brethren. Their easy money policies enabled Americans to live far beyond their true means through credit card debt, auto debt, mortgage debt, and home equity debt. This false illusion of wealth and foolish spending led mega-retailers to ignore facts and spread like locusts across the suburban countryside. The debt fueled orgy has run out of steam. All that is left is the largest mountain of debt in human history, a gutted and debt laden former middle class, and thousands of empty stores in future decaying ghost malls haunting the highways and byways of suburbia.

The implications of this long and winding road to ruin are far reaching. Store closings so far have only been a ripple compared to the tsunami coming to right size the industry for a future of declining spending. Over the next five to ten years, tens of thousands of stores will be shuttered. Companies like JC Penney, Sears and Radio Shack will go bankrupt and become historical footnotes. Considering retail employment is lower today than it was in 2002 before the massive retail expansion, the future will see in excess of 1 million retail workers lose their jobs. Bernanke and the Feds have allowed real estate mall owners to roll over non-performing loans and pretend they are generating enough rental income to cover their loan obligations. As more stores go dark, this little game of extend and pretend will come to an end. Real estate developers will be going belly-up and the banking sector will be taking huge losses again. I’m sure the remaining taxpayers will gladly bailout Wall Street again. The facts are not debatable. They can be ignored by the politicians, Ivy League economists, media talking heads, and the willfully ignorant masses, but they do not cease to exist.

“Facts do not cease to exist because they are ignored.” – Aldous Huxley

A recent post on this site described the Federal Reserve (not Goldman Sachs) as the true vampire squid.

A Predator By Intent

At the Fed’s founding, a few astute critics saw the Ponzi Scheme that it represented. Congressman Lindbergh had this to say:

This [Federal Reserve Act] establishes the most gigantic trust on earth. When the President [Wilson} signs this bill, the invisible government of the monetary power will be legalized….the worst legislative crime of the ages is perpetrated by this banking and currency bill. — Charles A. Lindbergh, Sr. , 1913

Lindbergh was hardly alone. Here is another comment by a legislator:

We have, in this country, one of the most corrupt institutions the world has ever known. I refer to the Federal Reserve Board. This evil institution has impoverished the people of the United States and has practically bankrupted our government. It has done this through the corrupt practices of the moneyed vultures who control it. — Congressman Louis T. McFadden in 1932 (Rep. Pa)

These were two of several US legislators who objected vehemently to the creation and operations of the Federal Reserve.

These objectors were neither prescient nor lucky in their assessment of central banking. Central banking had always been the goal of the monied and financial classes. The most successful banking empire stated:

The few who understand the system, will either be so interested from it’s profits or so dependant on it’s favors, that there will be no opposition from that class. — Rothschild Brothers of London, 1863

This position was stated a half-century before the Federal Reserve was instituted.

Today’s Federal Reserve

Today Fed critics are growing to a large and vocal force. Before this crisis ends, I suspect that many more will have joined this group.

The Fed is at a critical point, one would hope an existential one, in its history. Its necessity and value are no longer blindly assumed. Its ability to affect positive economic outcomes are correctly seriously in doubt. Its importance and necessity are under fire.

The Fed is now beginning to be likened to the phony wizard in “The Wizard of Oz.” It increasingly is disbelieved in its claims and seen by a large minority of the population as a charlatan. Ron Paul is responsible for getting his views through to the masses, including popularizing the notion that the Fed is an evil force rather than one for good.

The Fed reached a decision point recently regarding its QE policy. They came to a fork in the road and, in effect, punted. The left fork represented additional stimulus while the right was a reduction in stimulus. The Fed did nothing. It was paralyzed and chose neither fork. They still stand at this juncture, unsure of which path to take.

The Reason For Paralysis

The Fed should never have set out on this road to perdition. At this point neither fork is palatable. That is because of the dependency effects created by monetary expansion. Alasdair MacLeod describes the problem:

What is not generally appreciated is that once a central bank starts to use monetary expansion as a cure-all it is extremely difficult for it to stop. This is the basic reason the Fed has not pursued the idea, and why it most probably never will.

Years ago, I remember Milton Friedman discussing the point made by Mr. MacLeod. Friedman was careful to distinguish between the level of the money supply and the rate of change in the money supply. He believed that the rate of change was the important variable in regard to short-term economic activity. A decrease in the rate of money production, in Friedman’s opinion, would slow economic activity.

That summary is an oversimplification of Friedman’s position. Friedman did not believe that changes in the money supply could influence economic activity in any long-term sense. To the extent that changes in the rate of money creation surprised the public, economic actors would be forced to alter their expectations and behavior. That view was the basis of McLeod’s comment.

The Fed Will Stop, One Way Or Another

The Fed will stop. That is a certainty. When and whether they stop willingly or markets stop them is a different issue. The Fed stopped twice before recently, only to restart when the economy and financial assets began to slump. I suspect they will stop again, willingly but then follow the previous pattern. Whether they stop at QE4 or 5 or 8, ultimately they will stop completely or be stopped by markets.

The option of standing in place was attractive only because the two other options were deemed unacceptable. Increasing the level of stimulus was not seen as necessary (yet). It also had the disadvantage of contradicting all the optimism expressed by the political class and the Fed themselves. Decreasing the stimulus was apparently seen as too great a risk, ala the Friedman rate of change issue. Chris Martenson deals with this issue (my emboldening):

The simple truth, as I see it, is that the Fed now knows that as soon as it takes the punchbowl away, all of the apparent wealth evaporates and the market crumbles. Here we might note that if several years of truly historic money printing has not yet provided enough self-sustaining recovery, why exactly is it that the Fed thinks more of the same will do the trick?

Something just does not add up in this story. What is it that they are not telling us?

Well, one thing that really does not fit in this story is that oil over $100 per barrel. As far as I am concerned, there will be no such thing as a resumption in the type of growth the Fed wishes to see before it willingly begins tapering (end eventually unwinding), because of the price of oil and debt levels that are still far too high.

Which means the Fed will keep on printing money until something happens. More bluntly, I think the Fed will keep printing until some form of market accident happens that forces it to behave differently.

When that happens, the Fed will be following, not leading. And many will be cruelly punished for believing that the Fed had some magical ability to re-write economic laws.

The Fed As Pusher

The process the Fed is wrestling with is no different than that of the drug addict. After a certain point, dependency develops. Then the withdrawal process is so painful it is not willingly accepted. The drug analogy holds in other respects:

The addict is forced to increase doses over time to achieve the same “hit.” So too is the Fed. Holding stimulus injections at $85 billion will eventually not be enough to sustain the good feeling which currently exists. That is the point made above by Mr. MacLeod.