After the victory of Donald Trump in 2016, the GOP held the Senate and House, two-thirds of the governorships, and 1,000 more state legislators than they had on the day Barack Obama took office.

“The Republican Party has not been this dominant in 90 years,” went the exultant claim.

A year later, Republicans lost the governorship of Virginia and almost lost the legislature.

Came then the loss of a U.S. Senate seat in ruby-red Alabama.

Tuesday, Democrats captured a House seat in a Pennsylvania district Trump carried by 20 points, and where Democrats had not even fielded a candidate in 2014 and 2016.

Republicans lately congratulating themselves on a dominance not seen since 1928, might revisit what happened to the Class of 1928.

In 1930, Republicans lost 52 House seats, portending the loss of both houses of Congress and the White House in 1932 to FDR who would go on to win four straight terms. For the GOP, the ’30s were the dreadful decade.

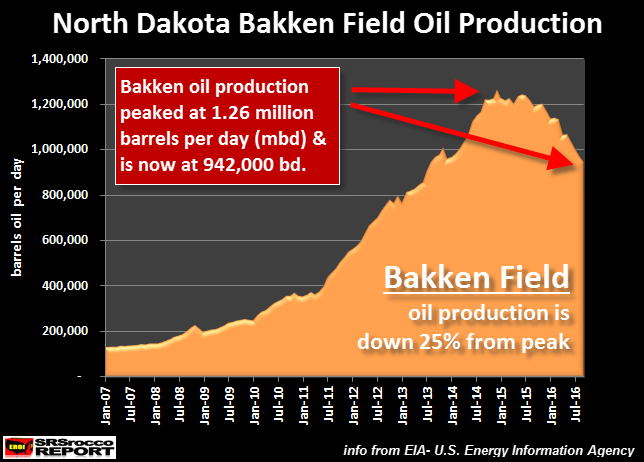

The Death of the Great Bakken Oil Field has begun and very few Americans understand the significance. Just a few years ago, the U.S. Energy Industry and Mainstream media were gloating that the United States was on its way to “Energy Independence.”

Unfortunately for most Americans, they believed the hype and are now back to driving BIG SUV’s and trucks that get lousy fuel mileage. And why not? Americans now think the price of gasoline will continue to decline because the U.S. oil industry is able to produce its “supposed” massive shale oil reserves for a fraction of the cost, due to the new wonders of technological improvement.

I actually hear this all the time when I travel and talk to family, friends and strangers. I gather they have no clue that the Great Bakken Oil Field is now down a stunning 25% from its peak in just a little more than a year and half ago:

Elites need to figure out how to understand the demands of those left behind

Getty Images

LONDON (MarketWatch) — The pound is sailing up past $1.60. The FTSE-100 index is breezing past 7,000. The euro is strengthening, and business confidence is gaining ground across the continent.

A raft of M&A deals, and a few big initial public offerings are unveiled as the investment bankers push forward with deals that had been kept on hold until the uncertainty resolved itself. And British Prime Minister David Cameron is pictured disappearing off to the Mediterranean to enjoy a well-earned break.

Many investors must be hoping that somehow they can wake up from a very bad dream and get on with their lives in a world where the U.K. had decided to stay in the European Union.

That, as we now know, is not what happened. Instead, while the FTSE UKX, -1.52% has been surprisingly buoyant, sterling GBPUSD, -0.9675% has been plunging, and there is already plenty of evidence of deals being pulled, and a damaging hit to business confidence.

I find J.C. Penney to be a sick joke. The executives of this company think they can put out positive press releases and have their financial statements not properly show in the earnings press release to cover up the fact their financial results are deteriorating – not improving. CNBC will dutifully report the corporate lies. Checkout the press release where, for some reason, the financial results don’t format. Must be a glitch. Right?

The press release heading makes you think business is booming. Whenever a corporation crows about EBITDA, you know they are covering up their true results. Of course, a company with $4.7 billion of debt wouldn’t want to include interest expense in the results they announce.

These rocket scientists owe their ongoing existence to Bernanke and Yellen. A company with this much debt and billions in losses over the last five years should be paying 20% interest on their debt. Instead they can finance themselves at 8% rates. This bloated pig should have gone belly up by now. That’s how creative destruction works in a free market. Their existence as a dead retailer walking brings down the results of other retailers, creating the current zombie retail environment. These retailers just plod along, losing money, buying back stock, and never dying. The Fed has created this Walking Dead Economy with their warped QE and ZIRP “solutions”.

If you go to JC Penney’s website, you can actually see their income statement, balance sheet and cash flow statement.

UnitedHealth, America’s largest health insurance provider, says it will exit from most ObamaCare exchanges next year, citing more than $1 billion in losses.

CEO Stephen Hemsley says his company “cannot continue to broadly serve the market created by the Affordable Care Act’s coverage expansion due partly to the higher risk that comes with its customers,” as reported by the Associated Press.

The announcement came after UnitedHealth revised its projection for 2016 to $650 million in losses, up from a previous estimate of $525 million, after ending 2015 some $475 million in the red.

As the AP tells it, UnitedHealth had “second thoughts” almost immediately after announcing it would expand participation from four state exchanges to 34.

As of last November, the company was debating a complete exit from all ObamaCare exchanges, but has apparently decided to remain active in a “handful” of states, which Hemsley did not specify in his conference call to report company earnings. It has already been announced that the company was pulling out of Arkansas, Georgia, and Michigan.

The Washington Postcites a Kaiser Family Foundation study that estimated about 1.1 million ObamaCare customers would be left with a single insurance provider to “choose” from, if UnitedHealth withdrew from every ACA exchange. According to this analysis, “the impact could be significant in some areas, particularly in rural areas in Southern states.”

The Associated Press notes that some other big insurance players, such as Aetna, have reported heavy losses from the ACA exchanges, and are expected to “trim their exchange participation in 2017.”

“A dozen nonprofit health insurance cooperatives created by the ACA to sell coverage on the exchanges have already folded, and the survivors all lost millions last year,” the AP adds.

“Stock prices have reached what looks like a permanently high plateau.”

Irving Fisher, October 21, 1929

“Stability leads to instability. The more stable things become and the longer things are stable, the more unstable they will be when the crisis hits.”

Hyman Minsky

“Participants in the speculative situation are programmed for sudden efforts at escape. Thus the rule, supported by the experience of centuries: the speculative episode always ends not with a whimper but with a bang. There will be occasion to see the operation of this rule frequently repeated.”

John Kenneth Galbraith

Despite a near-term outlook that remains rather neutral (though with negative skew), we believe that one requires either a disregard or an ignorance of market history to dismiss the likelihood of a 40-55% market retreat over the completion of the current market cycle. From present valuations, a market loss of that magnitude would not be a worst-case scenario, but merely a run-of-the-mill completion of the current market cycle. On a longer horizon, we presently estimate that S&P 500 nominal total returns are likely to average just 0-2% annually over the coming 10-12 years, with negative expected real returns on both horizons. Since the dividend yield on the S&P 500 exceeds 2% here, that also implies that we fully expect the S&P 500 Index to trade at a lower level in 10-12 years than it does today.

The good news here is that in order to achieve a zero 10-12 year return despite deep interim losses, we should also expect opportunities for strong market advances over this horizon. As I’ve noted frequently over the years, the most favorable market return/risk profile we identify is associated with a material retreat in market valuations that is then joined by an early improvement in our measures of market action. I have every expectation that this opportunity will emerge over the completion of the current market cycle.

Based on valuation measures having the strongest correlation with actual subsequent market returns across history, equity valuations have approached present levels in only a handful of instances: 1901 (followed by a -46% market retreat over the following 3-year period), 1906 (followed by a -45% retreat over the following year), 1929 (followed by a -89% collapse over the following 3 years), 1937 (followed by a -48% loss over the following year), 2000 (followed by a -49% market loss over the following 2 years), and 2007 (followed by a -57% market loss over the following 2 years). A few lesser extremes occurred in the 1960’s and 1970’s, followed by market losses in the -35% to -48% range.

Submitted by Tyler Durden on 01/17/2016 18:37 -0500

When Wells Fargo reported its Q4 earnings last week, the one topic analysts and investors wanted much more clarity on, was the bank’s exposure to oil and gas loans, and much more color on its energy book over concerns that Wells, like most of its peers, was underestimating the severity of the upcoming shale default wave.

And while the company’s earnings call indeed reveals that things are deteriorating rapidly in Wells energy book, perhaps an even bigger concern for Wells investors, which just happens to be the largest US mortgage lender, should be what is going on with its mortgage book. The answer: nothing. In fact, at $64 billion in mortgage applications in the quarter, this was not only a major drop from Q3, but also the lowest since the first quarter of 2014.

The housing market peaked in 2005 and proceeded to crash over the next five years, with existing home sales falling 50%, new home sales falling 75%, and national home prices falling 30%. A funny thing happened after the peak. Wall Street banks accelerated the issuance of subprime mortgages to hyper-speed. The executives of these banks knew housing had peaked, but insatiable greed consumed them as they purposely doled out billions in no-doc liar loans as a necessary ingredient in their CDOs of mass destruction.

The millions in upfront fees, along with their lack of conscience in bribing Moody’s and S&P to get AAA ratings on toxic waste, while selling the derivatives to clients and shorting them at the same time, in order to enrich executives with multi-million dollar compensation packages, overrode any thoughts of risk management, consequences, or the impact on homeowners, investors, or taxpayers. The housing boom began as a natural reaction to the Federal Reserve suppressing interest rates to, at the time, ridiculously low levels from 2001 through 2004 (child’s play compared to the last six years).

Yippee!!! JC Penney ONLY lost $167 million in the first quarter. The Wall Street shysters are ecstatic because they BEAT expectations. Buy Buy Buy.

This loss now brings JC Penney’s cumulative loss since 2011 to, drum roll please, $3.5 BILLION. They haven’t had a profitable quarter in over four years. But, they are always on the verge of that turnaround just over the horizon.

Wall Street has told you to buy this stock from $42 in 2012 to it’s current pitiful level of $9. They tout the wonderful 3.4% increase in comparable sales. They fail to mention that first quarter 2016 sales are only 30% below first quarter sales in 2011.

They fail to mention that JC Penney burned through another $274 million of cash in the first quarter. Their equity has dropped by $1 billion in the last year, while their long term debt has gone up by $500 million.

In 2011 they had $5.5 billion of equity and $3.1 billion of debt. Today they have $1.8 billion of equity and $5.3 billion of debt. They are dead retailer walking. The only reason they haven’t gone belly up is the Federal Reserve manipulated ultra low interest rates that encourage mal-investment and keep zombie companies like JC Penney alive.

Being able to borrow at low rates will delay the end, but the end is still coming for this bloated dying pig of a company. The future is certain.

But don’t listen to me. Listen to Wall Street. This is the buy of a lifetime.

Amazon reported their financial results for their first quarter last week. They had sales of $22.7 billion and somehow managed to lose $57 million. So you have a company with revenue growth of 13% that is losing money. The stock was already selling at an outrageous price of $385 per share. Wall Street’s reaction to 13% revenue growth and increasing losses was to drive the price up $65 in one day to $450 per share. It is up 56% in the last 6 months, while it was losing $400 million in the last 12 months. If you look really really hard at the chart below you still won’t see the profit bars. Maybe a magnifying glass will help.

This company had a negative operating cash flow of $1.5 BILLION for the quarter. It’s free cash flow was NEGATIVE $2.4 billion. It’s price to book value is 13.4. A normal price to book value is 1.0 to 2.0. It doesn’t have a PE ratio because you need earnings to calculate this ratio. This company is the poster child of the delusion that has overtaken our financial markets. Bezos always promises future profits that never materialize. Wall Street buys on the promises and spins stories about new paradigms, blah, blah, blah. We’ve heard it all before. We heard it in 2000 and we heard it in 2007. It always ends the same way. If you don’t believe me then just borrow on margin and pile into this juggernaut of losses.

I love when mortgage products get creative in their titles. We had those wonderful “option ARMs” that basically gave you the option to not pay your mortgage principal. But what people forget beyond the egregious toxic mortgages, most foreclosures hit people with vanilla 30-year fixed mortgages. That is right, of the 7,000,000+ completed foreclosures most were boring traditional mortgages. Since the stock market has been on a massive run for six years now, people have forgotten that recessions routinely hit our economy. It is part of the economic system. If you can’t pay your mortgage, it doesn’t matter if you have a 30-year fixed, ARM, interest only loan, or other variety of payment you are making to the bank. Now that banks know they can boot you out and sell to an investor, the foreclosure process started humming along. A reader pointed out that Freddie Mac is entering once again into offering low down payment loans to cash strapped borrowers dreaming of their first crap shack. The product is called Home Possible Advantage but in reality, you are making a big bet with little equity.

Home Possible Advantage

For all intents and purposes, Freddie Mac and Fannie Mae were nationalized during the housing crisis. Free market Kool-Aid drinkers conveniently forget that we conducted some massive socialism in bailing out the financial sector. In theory the free market sounds good for housing but the housing market is one heavily subsidized segment of our economy (i.e., government backed loans, mortgage deductions, property taxes, etc).

So it was interesting that resurrected and nationalized player Freddie Mac is introducing a very low down payment product:

This is adding a high level of risk for new buyers. Since Americans are tapped out and the banking industry has juiced home values up thanks to investors, it is time to hand this game off to cash strapped Americans. That is, unless you can offer riskier products.

Interesting how the MSM virtually ignored this little tidbit of information. A report from the inspector general for the Federal Housing Finance Agency, which regulates Fannie and Freddie, warns that these two bloated insolvent pigs are going to face declining profits and miniscule capital cushions which will result in the taxpayers getting fucked over once again.

The inspector general’s report noted that for the past few years, Fannie and Freddie’s net income has been driven by major legal settlements as well as the revaluation of tax assets and other one-time items that aren’t sustainable. That, along with the companies’ declining capital cushion, increases the likelihood they could need more government money in the future.

More government money means more of your money.

Here’s the truth about Fannie and Freddie. They hold trillions of mortgages on their books. Their balance sheets were filled with toxic mortgages in 2008 when the financial collapse occurred. You, the taxpayer, were forced to give these criminal government entities $187 billion to cover their losses.

But that was the tip of the iceberg. In March of 2009 the FASB suspended real accounting and allowed fake accounting for financial firms. So, for the last five years Fannie and Freddie could pretend they weren’t insolvent and have reported fake profits of $228 billion. They were nothing but accounting entries. They didn’t generate actual cash. They reduced their loan loss reserves and recorded tax benefit entries and a myriad of other hocus pocus bullshit.

It gets better. They then pretended to “pay back” the US Treasury with these fake profits. This is a major reason for Obama taking credit for declining deficits. These fake profits reduce the real deficit – on paper. Who says accountants aren’t bad asses?

The way you know these profits are fake is the stock price of Fannie and Freddie. Both stocks trade at $2.50. They have supposedly been generating $25 billion per year in profits – each. Back in 2007 they were generating profits of $4 to $6 billion per year and their stock prices were $70 per share. The market knows they are insolvent and knows the profits are a sham.

But now, even the sham profits have dried up. There are no more journal entries to make. No more fake profits to report. The housing market is headed south, the 3% down mortgages to deadbeats is going to blow up in their faces, and the American taxpayer is going to be ass raped again when the billions in losses start rolling in. This report is telling you what is about to happen. Book it Dano.

The classic Wall Street bullshit parade is under way. JC Penney made the dramatic announcement that same store sales during the holiday period grew by a whole 3.7%. They grew by 3.1% last year. The previous year they FELL by an astounding 31%. This year also had an extra day versus last year.

So let me give you some perspective. If their sales were $100 in 2011 and they fell by 31% in 2012, rose by 3.1% in 2013, and rose by another 3.7% in 2014, that means they are now at $74. JC Penney’s holiday sales were still 26% lower than they were in 2011 and the Wall Street shysters jacked the stock up by 20% overnight. Think about that for a moment. They are celebrating results that leave them 26% below their sales level from four years ago.

Here is what the jackoff CEO from JC Penney did not reveal in his press release. What was the customer traffic increase? I’m sure most of the increase came from on-line business and pricing. He did not reveal the tremendous profits these sales will generate. You know why? Because JC Penny used huge promotions and discounts to achieve their mammoth 3.7% increase.

JC Penney will be reporting massive losses for the fourth quarter. The Wall Street shysters will have already sold after the 20% surge, because the stock will tank again.

The proof that Christmas sucked is revealed in the chart below. Checkout the 4th quarter of 2012. There were 14 retailers who announced their earnings would be less than expected and 12 who announced better than expected earnings. Look at this year. There have been 24 retailers announce WORSE earnings than expected and 3 better than expected. Does that sound like a great Christmas season?

This destroys the economic recovery meme sold to the public by Obama, Wall Street and the captured MSM media. Profits talk. If there really was a strong jobs recovery and the “tremendous” savings from gas price declines, consumers would be spending. The proof they are not is in the chart. Don’t believe the bullshit being heaped on you every day. Nothing but lies and propaganda.

The Wall Street shysters have no morality, conscience or humanity. They are nothing but blood sucking parasites. Their sole purpose is to enrich themselves, while impoverishing their hosts (clients & customers). They destroyed the lives of millions with their fraudulent subprime housing scheme and were bailed out by the very people they screwed. Their hubris and arrogance knows no bounds. With encouragement from their captured central bank and the Obama administration, they are resorting to subprime fraud again in an effort to revive our dead economy. It worked so well the first time with houses, it will surely work a second time with automobiles. They prey upon the ignorant, stupid, and math challenged masses.

The entire engineered auto “recovery” is nothing but an easy money debt financed fraud. It will end in tears for millions and the government will insist you bail out the bankers again.

In a Subprime Bubble for Used Cars, Borrowers Pay Sky-High Rates

Rodney Durham stopped working in 1991, declared bankruptcy and lives on Social Security. Nonetheless, Wells Fargo lent him $15,197 to buy a used Mitsubishi sedan.

“I am not sure how I got the loan,” Mr. Durham, age 60, said.

Mr. Durham’s application said that he made $35,000 as a technician at Lourdes Hospital in Binghamton, N.Y., according to a copy of the loan document. But he says he told the dealer he hadn’t worked at the hospital for more than three decades. Now, after months of Wells Fargo pressing him over missed payments, the bank has repossessed his car.

This is the face of the new subprime boom. Mr. Durham is one of millions of Americans with shoddy credit who are easily obtaining auto loans from used-car dealers, including some who fabricate or ignore borrowers’ abilities to repay. The loans often come with terms that take advantage of the most desperate, least financially sophisticated customers. The surge in lending and the lack of caution resemble the frenzied subprime mortgage market before its implosion set off the 2008 financial crisis.

Auto loans to people with tarnished credit have risen more than 130 percent in the five years since the immediate aftermath of the financial crisis, with roughly one in four new auto loans last year going to borrowers considered subprime — people with credit scores at or below 640.

The explosive growth is being driven by some of the same dynamics that were at work in subprime mortgages. A wave of money is pouring into subprime autos, as the high rates and steady profits of the loans attract investors. Just as Wall Street stoked the boom in mortgages, some of the nation’s biggest banks and private equity firms are feeding the growth in subprime auto loans by investing in lenders and making money available for loans.

And, like subprime mortgages before the financial crisis, many subprime auto loans are bundled into complex bonds and sold as securities by banks to insurance companies, mutual funds and public pension funds — a process that creates ever-greater demand for loans.

The New York Times examined more than 100 bankruptcy court cases, dozens of civil lawsuits against lenders and hundreds of loan documents and found that subprime auto loans can come with interest rates that can exceed 23 percent. The loans were typically at least twice the size of the value of the used cars purchased, including dozens of battered vehicles with mechanical defects hidden from borrowers. Such loans can thrust already vulnerable borrowers further into debt, even propelling some into bankruptcy, according to the court records, as well as interviews with borrowers and lawyers in 19 states.

In another echo of the mortgage boom, The Times investigation also found dozens of loans that included incorrect information about borrowers’ income and employment, leading people who had lost their jobs, were in bankruptcy or were living on Social Security to qualify for loans that they could never afford.

Photo

Credit

Many subprime auto lenders are loosening credit standards and focusing on the riskiest borrowers, according to the examination of documents and interviews with current and former executives from five large subprime auto lenders. The lending practices in the subprime auto market, recounted in interviews with the executives and in court records, demonstrate that Wall Street is again taking on very risky investments just six years after the financial crisis.

The size of the subprime auto loan market is a tiny fraction of what the subprime mortgage market was at its peak, and its implosion would not have the same far-reaching consequences. Yet some banking analysts and even credit ratings agencies that have blessed subprime auto securities have sounded warnings about potential risks to investors and to the financial system if borrowers fall behind on their bills.

Pointing to higher auto loan balances and longer repayment periods, the ratings agency Standard & Poor’s recently issued a report cautioning investors to expect “higher losses.” And a high-ranking official at the Office of the Comptroller of the Currency, which regulates some of the nation’s largest banks, has also privately expressed concerns that the banks are amassing too many risky auto loans, according to two people briefed on the matter. In a June report, the agency noted that “these early signs of easing terms and increasing risk are noteworthy.”

Despite such warnings, the volume of total subprime auto loans increased roughly 15 percent, to $145.6 billion, in the first three months of this year from a year earlier, according to Experian, a credit rating firm.

“It appears that investors have not learned the lessons of Lehman Brothers and continue to chase risky subprime-backed bonds,” said Mark T. Williams, a former bank examiner with the Federal Reserve.

In their defense, financial firms say subprime lending meets an important need: allowing borrowers with tarnished credits to buy cars vital to their livelihood.

Lenders contend that the risks are not great, saying that they have indeed heeded the lessons from the mortgage crisis. Losses on securities made up of auto loans, they add, have historically been low, even during the crisis.

Autos, of course, are very different than houses. While a foreclosure of a home can wend its way through the courts for years, a car can be quickly repossessed. And a growing number of lenders are using new technologies that can remotely disable the ignition of a car within minutes of the borrower missing a payment. Such technologies allow lenders to seize collateral and minimize losses without the cost of chasing down delinquent borrowers.

That ability to contain risk while charging fees and high interest rates has generated rich profits for the lenders and those who buy the debt. But it often comes at the expense of low-income Americans who are still trying to dig out from the depths of the recession, according to the interviews with legal aid lawyers and officials from the Federal Trade Commission and the Consumer Financial Protection Bureau, as well as state prosecutors.

While the pain from an imploding subprime auto loan market would be much less than what ensued from the housing crisis, the economy is still on relatively fragile footing, and losses could ultimately stall the broader recovery for millions of Americans.

Photo

Rodney Durham, 60, of Binghamton, N.Y., had his car repossessed.Credit Heather Ainsworth for The New York Times

The pain is far more immediate for borrowers like Mr. Durham, the unemployed car buyer from Binghamton, N.Y., who stopped making his loan payments in March, only five months after buying the 2010 Mitsubishi Galant. A spokeswoman for Wells Fargo, which declined to comment on Mr. Durham citing a confidentiality policy, emphasized that the bank’s underwriting is rigorous, adding that “we have controls in place to help identify potential fraud and take appropriate action.”

The Mitsubishi was repossessed last month, leaving Mr. Durham without a car. But his debt ordeal may not be over.

Some lenders go after borrowers like Mr. Durham for the debt that still remains after a repossessed car is sold, according to court filings. Few repossessed cars fetch enough when they are resold to cover the total loan, the court documents show. To get the remainder, some lenders pursue the borrowers, which can leave them shouldering debts for years after their cars are gone.

But for now, Mr. Durham, who is disabled, has a more immediate problem.

“I just can’t get around without my car,” he said.

The Brokers

Outside, the banner proclaimed: “No Credit. Bad Credit. All Credit. 100 percent approval.” Inside the used-car dealership in Queens, N.Y., Julio Estrada perfected his sales pitches for the borrowers, including some immigrants who spoke little English.

Sure, the double-digit interest rates might seem steep, Mr. Estrada told potential customers, but with regular payments, they would quickly fall. Mr. Estrada, who sometimes went by John, and sometimes by Jay, promised others cash rebates.

If the soft sell did not work, he played hardball, threatening to keep the down payments of buyers who backed out, according to court documents and interviews with customers.

The salesman was ultimately indicted by the Queens district attorney on grand larceny charges that he defrauded more than 23 car buyers with refinancing schemes.

Relatively few used-car dealers are charged with fraud. Yet the extreme example of Mr. Estrada comes as some used-car dealers — a business that has long had a reputation for aggressive pitches — are pushing sales tactics too far, according to state prosecutors and federal regulators.

And these are among the thousands of used-car dealers who are working hand-in-hand with Wall Street to sell cars. Court records show that Capital One and Santander Consumer USA all bought loans arranged by Mr. Estrada, who pleaded guilty last year. Since then, Mr. Estrada was indicted on separate fraud charges in March by Richard A. Brown, the Queens district attorney. That case is still pending.

To guard against fraud, the banks say, they vet their dealer partners and routinely investigate complaints. Capital One has “rigorous controls in place to identify any potential issues,” said Tatiana Stead, a bank spokeswoman, adding that last year “we terminated our relationship with the dealership” where Mr. Estrada worked. Dawn Martin Harp, head of Wells Fargo Dealer Services, said that “it’s important to note that not all claims of dealer fraud turn out to be fraud.”

James Kousouros, Mr. Estrada’s lawyer, said that “for those individuals for whom Mr. Estrada bore responsibility, he accepted this and is committed to the restitution agreed to.” Some civil lawsuits filed by borrowers were found to be without merit, he said.

For their part, car dealers note that like any industry they sometimes have rogue employees, but add that customers are overwhelmingly treated fairly.

“There is no place for fraud or any other nefarious activities in the industry, especially tactics that seek to take advantage of vulnerable consumers,” said Steve Jordan, executive vice president of the National Independent Automobile Dealers Association.

In their role as matchmaker between borrowers and lenders, used-car dealers wield tremendous power. They make the pitch to customers, including many troubled borrowers who often believe that their options are limited. And the dealers outline the terms and rates of the loans.

In interviews, more than 40 low-income borrowers described how they were worn down by used car dealers who kept them in suspense for hours before disclosing whether they even qualified for a loan. The seemingly interminable wait, the borrowers said, left them with the impression that the loan — no matter how onerous the terms — was their only chance.

The loans also came with other costs, according to interviews and an examination of the loan documents, including add-on products like unusual insurance policies. In many cases, the examination by The Times found, borrowers ended up shouldering loans that far exceeded the resale value of the car. A reason for that disparity is that some borrowers still owe money on cars that they are trading in when they purchase a new one. That debt is then rolled over into the new loan.

“By the end, they are paying $600 a month for a piece of junk,” said Charles Juntikka, a bankruptcy lawyer in Manhattan.

The dealers have an incentive to increase both the size and the interest rate of the loans.

The arithmetic is simple. The bigger size and rate of the loan, the bigger the dealers’ profit, or so-called markup — the difference between the rate charged by the lenders and the one ultimately offered to the borrowers. Under federal law, dealers do not have to disclose the size of the markup.

Photo

Dolores Blaylock, 51, of Austin, Tex., and her father, Fidencio Muñiz, 84. Like many buyers, she found she had unwittingly purchased an add-on — in her case, a life insurance policy.Credit Erich Schlegel for The New York Times

To buy her 2004 Mazda van, Dolores Blaylock, 51, a home health care aide in Austin, Tex., said she unwittingly paid for a life insurance policy that would cover her loan payments if she died.

Her loan totaled $13,778 — nearly three times the value of the van that she uses to shuttle her father, who uses a wheelchair, to his doctor’s appointments.

Now, Ms. Blaylock says she regrets ever buying the van, which frequently breaks down. “I am afraid to drive it out of town,” she said.

In some cases, though, the tactics veer toward outright fraud. The Times’s scrutiny of loan documents, including some produced in litigation, found that some used-car dealers submitted loan applications to lenders that contained incorrect income and employment information. As was the case in the subprime mortgage boom, it is unclear whether borrowers provided incorrect information to qualify for loans or whether the dealers falsified loan applications. Whatever the cause, the result is the same: Borrowers with scant income qualified for loans.

Mary Bridges, a retired grocery store employee in Syracuse, N.Y., said she repeatedly explained to a car salesman that her only monthly income was about $1,200 in Social Security. Still, Ms. Bridges said that the salesman falsely listed her monthly income as $2,500 on the application for a car loan submitted by a local dealer to Wells Fargo and reviewed by The Times.

As a result, she got a loan of $12,473 to buy a 2004 used Buick LeSabre, currently valued by Kelley Blue Book at around half that much. She tried to keep up with the payments — even going on food stamps for the first time in her life — but ultimately the car was repossessed in 2012, just two years after she bought it.

“I have always been told to do the responsible thing, but I said, ‘This is too much,’ ” the 76-year-old widow said.

The dealer agreed to pay Ms. Bridges $1,000 after Syracuse University law students threatened to file a lawsuit accusing the company of violating state and federal consumer protection laws.

But Wells Fargo, which resold the car for $4,500 last July, is still pursuing Ms. Bridges for $2,900 — a total that includes her remaining loan balance and an $835 fee for “cost of repossession and sale,” according to a copy of a letter that Wells Fargo sent to Ms. Bridges last August. (Wells Fargo declined to comment on Ms. Bridges.)

Photo

Shahadat Tuhin, 42, with his daughter Sadia Oishika, 10. He says his auto dealer used deceptive practices.Credit Hiroko Masuike/The New York Times

Even when authorities have cracked down on dealers, borrowers are still vulnerable to fraud. Last June, Shahadat Tuhin, a New York City taxi driver, bought a car from Mr. Estrada, the salesman in Queens who less than a year earlier had been indicted.

The charge by the Queens district attorney didn’t keep him out of the business. While his criminal case was pending, the salesman persuaded Mr. Tuhin to buy a used car for 90 percent more than the price he agreed upon. Needing the car to take his daughter, who has a heart condition, to the doctor, Mr. Tuhin said he unwittingly signed for a $26,209 loan with completely different terms than the ones he had reviewed.

Immediately after discovering the discrepancies, Mr. Tuhin, 42, said he tried to return the car to the dealership and called the lender, M&T Bank, to notify them of the fraud.

The bank told him to take up the issue with the dealer, Mr. Tuhin said.

M&T declined to comment on Mr. Tuhin, but said it no longer does business with that dealership.

The Money

Investors, seeking a higher return when interest rates are low, recently flocked to buy a bond issue from Prestige Financial Services of Utah. Orders to invest in the $390 million debt deal were four times greater than the amount of available securities.

What is backing many of these securities? Auto loans made to people who have been in bankruptcy.

An affiliate of the Larry H. Miller Group of Companies, Prestige specializes in making the loans to people in bankruptcy, packaging them into securities and then selling them to investors.

“It’s been a hot space,” Richard L. Hyde, the firm’s chief operating officer, said during an interview in March. Investors are betting on risky borrowers. The average interest rate on loans bundled into Prestige’s latest offering, for example, is 18.6 percent, up slightly from a similar offering rolled out a year earlier. Since 2009, total auto loan securitizations have surged 150 percent, to $17.6 billion last year, though some estimates have put the total volume even higher. To meet that rising demand, Wall Street snatches up more and more loans to package into the complex investments.

Much like mortgages, subprime auto loans go through Wall Street’s securitization machine: Once lenders make the loans, they pool thousands of them into bonds that are sold in slices to investors like mutual funds, pensions and hedge funds. The slices that include loans to the riskiest borrowers offer the highest returns.

Rating agencies, which assess the quality of the bonds, are helping fuel the boom. They are giving many of these securities top ratings, which clears the way for major investors, from pension funds to employee retirement accounts, to buy the bonds. In March, for example, Standard & Poor’s blessed most of Prestige’s bond with a triple-A rating. Slices of a similar bond that Prestige sold last year also fetched the highest rating from S.&P. A large slice of that bond is held in mutual funds managed by BlackRock, one of the world’s largest money managers.

Private equity firms have also seen the opportunity in auto subprime lending. A $1 billion investment by Kohlberg Kravis Roberts & Co., Centerbridge Partners and Warburg Pincus in a large subprime lender roughly doubled in about two years. Typically, it takes private equity firms three to five years to reap significant profit on their investments.

It is not just the private equity firms and large banks that are fanning the lending boom. Major insurance companies and mutual funds, which manage money on behalf of mom-and-pop investors, are also snapping up securities backed by subprime auto loans.

While there are no exact measures of how many of these loans end up on banks’ balance sheets, interviews with consumer lawyers and analysts suggest the problem is spreading, propelled by the very structure of the subprime auto market.

The vast majority of banks largely rely on dealers to screen potential borrowers. The arrangement, which means the banks rarely meet customers face to face, mirrors how banks relied on brokers to make mortgages.

In some cases, consumer lawyers say, the banks actually ignore complaints by borrowers who accuse dealers of fabricating their income or even forging their signatures.

“Even when they are presented with clear evidence of fraud, the banks ignore it,” said Peter T. Lane, a consumer lawyer in New York. “The typical refrain is, ‘It’s not our problem, take it up with the dealer.’ ”

It could quickly become the banks’ problem, analysts say, if questionable loans sour, causing losses to multiply.

For now, the banks are not pulling back. Many are barreling further into the auto loan market to help recoup the billions in revenue wiped out by regulations passed after the 2008 financial crisis.

Wells Fargo, for example, made $7.8 billion in auto loans in the second quarter, up 9 percent from a year earlier. At a presentation to investors in May, Wells Fargo said it had $52.6 billion in outstanding car loans. The majority of those loans are made through dealerships. The bank also said that as of the end of last year, 17 percent of the total auto loans went to borrowers with credit scores of 600 or less. The bank currently ranks as the nation’s second-largest subprime auto lender, behind Capital One, according to J. D. Power & Associates.

Wells Fargo executives say that despite the surge, the credit quality of its loans has not slipped. At the May presentation, Thomas A. Wolfe, the head of Wells Fargo Consumer Credit Solutions, emphasized that the overall quality of its auto loans was improving. And Tatiana Stead, the Capital One spokeswoman, said that Capital One worked “to ensure we do not follow the market to pursue growth for growth’s sake.”

Prestige says its loans experience relatively low losses because borrowers have discharged many of their other debts in bankruptcy, freeing up more cash for their car payments. Another advantage for the lender: No matter how tough things get for troubled borrowers, federal law prevents them from escaping their bills through bankruptcy for at least another seven years.

“The vast majority of our customers have been successful with their loans and leave us with a much higher credit score,” said Mr. Hyde, Prestige’s chief operating officer.

The Risks

All it took was three months.

Dolores Jackson, a teacher’s aide in Jersey City, says she thought she could handle the $540 a month on the 2012 Chevy Malibu she bought in January 2013.

But the payments on the $27,140 loan from Exeter Finance, which is owned by Blackstone, quickly overwhelmed her, and she prepared to declare bankruptcy in April.

“I was drowning,” she said.

Other borrowers have also found themselves quickly overwhelmed by car loan payments.

Even after getting a second job at Staples, Alicia Saffold, 24, a supply technician at the Fort Benning military base in Georgia, could not afford the monthly payments on her $14,288.75 loan from Exeter. The loan, according to a copy of her loan document reviewed by The Times, came with an interest rate of nearly 24 percent. Less than a year after she bought the gray Pontiac G6, it was repossessed.

Photo

Marcelina and Jonathan Mojica, and their dog, Lilly. “The car gets more money than what we put in our fridge,” Mr. Mojica said.Credit Damon Winter/The New York Times

In the case of Marcelina Mojica and her husband, Jonathan, they are keeping up with their payments on their $19,313.45 Wells Fargo auto loan — but just barely. They are currently living in a homeless shelter in the Bronx.

“The car gets more money than what we put in our fridge,” said Mr. Mojica, 28. Such examples of distress underscore the broader strains within the subprime auto loan market.

Exeter Finance declined to comment on Ms. Saffold or Ms. Jackson, but Blackstone, its parent company, emphasized that the credit quality of its lender’s loans was improving and that it worked hard to ensure its customers received the best rates. To ensure the accuracy of loan documents, Blackstone said, employees vet both dealers and borrowers.

“Exeter Finance believes it’s important to provide people with the option to finance transportation essential to their livelihood,” said Mark Floyd, the company’s chief executive.

Still, financial firms are beginning to see signs of strain. In the first three months of this year, banks had to write off as entirely uncollectable an average of $8,541 of each delinquent auto loan, up about 15 percent from a year earlier, according to Experian.

Some investors think the time is right to start selling their holdings. Earlier this year, for example, private equity firms, including K.K.R., sold most of their stake in the subprime auto lender, Santander Consumer USA, when the lender went public. Since the company’s initial public offering, the stock has fallen more than 16 percent.

While losses from soured car loans would be far less than those on subprime mortgages, the red ink could still deal a blow to the banks not long after they recovered from the housing bust. Losses from auto loans might also cause the banks to further retrench from making other loans vital to the economic recovery, like those to small business and would-be homeowners.

In another sign of trouble ahead, repossessions, while still relatively low, increased nearly 78 percent to an estimated 388,000 cars in the first three months of the year from the same period a year earlier, according to the latest data provided by Experian. The number of borrowers who are more than 60 days late on their car payments also jumped in 22 states during that period.

As a result, some rating agencies, even those that had blessed auto loan securitizations with high ratings, are starting to question the quality of the loans backing those securities, and warn of losses that investors could suffer if the bonds start to sour. Describing the potential trouble ahead, Kevin Cole, an analyst with Standard & Poor’s, said, “We believe these trends could lead to higher losses and weakened profitability in a few years.”

If those losses materialize, they could pummel a wide range of investors, from pension funds to insurance companies to mutual funds held by Americans preparing for retirement. For the huge baby-boomer generation, including many whose savings were sapped by the 2008 crisis and the ensuing recession, any losses from the auto loan securities could deal them another setback.

“Borrowers are haunted by this debt, and it can crater their credit scores, prevent them from getting other loans and thrust them even further onto the financial margins,” said Ahmad Keshavarz, a consumer lawyer in New York.

Some borrowers are stuck making payments on loans that were fraudulently made by dealers, according to an examination of dozens of lawsuits against dealers. There are no exact measures of just how many people whose cars have been repossessed end up in this predicament, but lawyers for borrowers say that it is a growing problem, and one that points to another element of subprime auto lending.

Thanks to an amendment to the Dodd-Frank financial overhaul, the vast majority of dealers are not overseen by the Consumer Financial Protection Bureau. Since its start in 2010, the agency has earned a reputation for aggressively penalizing lenders, but it has limited authority over dealers.

The Federal Trade Commission, the agency that does oversee the dealers, has cracked down on certain questionable practices. And although the agency has won a number of cases against dealers for failing to accurately disclose car costs and other abuses, it has not taken aim at them for falsifying borrowers’ incomes, for example.

Photo

Alicia Saffold, 24, received a loan with an interest rate of nearly 24 percent. Her car was soon repossessed.Credit Tami Chappell for The New York Times

And the help is not coming fast enough for borrowers like Mr. Durham, the retiree in Binghamton; Mr. Tuhin, the taxi driver in Queens; or Ms. Saffold, the technician in Georgia.

“Buying the car was the worst decision I have ever made,” Ms. Saffold said.

Another Obama success story. Have the government take over the entire student loan industry in one fell swoop. Utilize the program as a way to artificially reduce the unemployment rate and to provide Keynesian stimulus to the economy as the “student” borrowers don’t actually go to class, but spend the borrowed money on iGadgets, Xboxes, and nights out at Applebees. Dole out $400 billion in NEW student loan debt in the last four years, bringing the total outstanding to $1.23 billion. This was all done with taxpayer money. When you realize the functional illiterates who got the loans will never be able to pay them back, you start reducing the interest rates, reducing monthly payments and create a brand new loan forgiveness program. Loan forgiveness is a clever name for FUCK THE TAXPAYER.

You then make ridiculous assumptions about the number of participants and the loan amounts to make it seem like a perfectly reasonable government program. Tell the dykes on MSNBC to rave about the wonderful plan and tell them it’s for the chilrun. Then you hire a bunch of unemployed liberal douchebags to market the plan to dumbass students getting degrees in African history and Mural art appreciation. Then you send emails to every indebted student in the country encouraging them to default on their student loans. And guess what? Huge success. Millions of students with no brains or hope for a job are stampeding into this wonderful program.

You the taxpayer are fucked at the rate of $72 billion so far. Obama’s brilliant strategy in controlling the student loan market will now cost you $14 billion per year in loan losses. And this is just the beginning. The losses will run into the hundreds of billions. It’s called math – something these students and Barack Obama have failed miserably.

Do you think Obama’s cost estimates for Obamacare will be this good? I can’t wait to find out.

Flood Of Students Demanding Loan Forgiveness Forces Administration Scramble

Submitted by Tyler Durden on 04/22/2014 14:22 -0400

“Loan forgiveness creates incentives for students to borrow too much to attend college, potentially contributing to rising college prices for everyone,” is a study’s warning over government plans that allow students to rack up big debts and then forgive the unpaid balance after a set period. As WSJ reports, enrollment in student debt forgiveness plans have surged nearly 40% in just six months, to include at least 1.3 million Americans owing around $72 billion. The administration is looking to cap debt eligible for forgiveness, as President Obama’s revamped Pay As You Earn scheme has seen applications soar and is estimated to cost taxpayers $14bn a year. The ‘popularity’ of the student loan bailout plan surged after Obama promoted it in 2012, and now the administration must back-track as costs have massively outpaced government predictions.

We have been aggresively focused on the government’s blowing of the student loan bubble…

Student debt has nearly doubled since 2007 to $1.1 trillion, disproportionately driven by the growth in graduate-school debt.

And questioned the need to incur such massive credit-fueled costs of tuition only to gain a low-paying job…

there is no point in trying to preserve the old regime. Today’s emphasis on measuring college education in terms of future earnings and employability may strike some as philistine, but most students have little choice. When you could pay your way through college by waiting tables, the idea that you should “study what interests you” was more viable than it is today, when the cost of a four-year degree often runs to six figures. For an 18-year-old, investing such a sum in an education without a payoff makes no more sense than buying a Ferrari on credit.

And while government plans are nothing new, Obama has aggressively promoted them…

The government has offered some form of income-based repayment since the early 1990s, but few studentsfound the terms enticing. But in 2007, Congress allowed borrowers working in nonprofit and government jobs to have unpaid debt forgiven after 10 years, and cut monthly payments for new borrowers to 15% of discretionary income.

In 2010, it cut those payments to 10% for borrowers who took out loans from 2014. A year later, Mr. Obama, through executive action, moved up the date when borrowers could qualify for the new terms, creating a program for those who took out loans from 2011. The White House this year has proposed making the program available to all student borrowers, regardless of when they signed their loans.

The popularity of the programs surged after the Obama administration began to promote them, starting in 2012, on the Internet and later through email to borrowers.

And it seems they are ripe for abuse…

“Income-based repayment can be a way for students responsibly to manage debt, but it should not be a bailout for students who borrow too much or for schools who charge too much,” said Sen. Lamar Alexander of Tennessee, the ranking Republican on the Senate Education Committee.

But, as usual, the government screwed up…

The plans’ long-term costs have greatly outpaced the government’s predictions. In the last fiscal year, debt absorbed by the repayment plans from the most widely used student-loan program—Stafford loans—exceeded government expectations from a year earlier by 90%.

…

A report Monday last week from the Brookings Institution, a centrist think tank, offered one of the few preliminary examinations of the programs’ impact. The most popular plan could cost taxpayers $14 billion a year if it becomes available to all borrowers as Mr. Obama has proposed, while fueling tuition inflation, it said.

“Loan forgiveness creates incentives for students to borrow too much to attend college, potentially contributing to rising college prices for everyone,” the study said. The authors recommend scrapping the forgiveness provisions.

Sure enough everyone piled in looking for their handout…

Enrollment in the plans—which allow students to rack up big debts and then forgive the unpaid balance after a set period—has surged nearly 40% in just six months, to include at least 1.3 million Americans owing around $72 billion, U.S. Education Department records show.

Which means costs are soaring and the administration feels the need to do something to fix what it had broken by intervening once again…

The Obama administration has proposed in its latest budget released last month to cap debt eligible for forgiveness at $57,500 per student. There is currently no limit on such debt.

The move reflects concerns in the administration not just about the hit to the government, but over the risk that promising huge debt forgiveness could make borrowers and schools less disciplined about costs. Colleges might charge more than they would otherwise, leading students to borrow more.

And so is the government about to pop the student loan bubble by spoiling a good thing – unlimited debt forgiveness – for students and trickling down that credit tightening impact on colleges only to happy to raise tuition costs to reflect the credit-forgiveness-adjusted amount of money on the table?

You know we are near or at a market top when shit stains like Ally Financial are brought public by fellow shit stains – Citi, Goldman, and Morgan Stanley. You’d have to be brain dead or an Ivy League trained economist to buy this turd sandwich at $25 per share. You’d have to be retarded shit eating muppet to buy this worthless government manipulated joke of a company. This is the company that has been doling out billions in subprime auto loans to the Free Shit Army for the last three years in order to prop up General Motors auto sales. They have been doing this because Obama and his minions instructed them to do so. Now that they are loaded with hundreds of billions in loans that will never be repaid, Obama is dumping this piece of shit on the public market where the Wall Street shysters will try to convince you to buy it. Jim Cramer thinks it’s the bomb.

I decided to go to their last SEC filing to get the real scoop about this joke. Here is the link:

You need to go to page 27 & 28 of their 29 page PR presentation to find out they LOST $190 million in the 4th quarter and $910 million for all of FY13.

This is a fabulous improvement over the $1.6 billion they LOST in FY12.

These government cronies have increased their auto loans outstanding by 100% since 2009 to $108 BILLION.

Page 14 of the presentation is the smoking gun. They had $843 million of delinquent auto loans in the 1st quarter of 2013. By the 4th quarter of 2013 delinquent loans had risen to $1.325 BILLION. That is a 57% increase in one year. SHOCKING!!! Considering they have been making loans to deadbeats who can barely scratch an X on the loan document. Do you think this trend is going to reverse in the 1st quarter of 2014? Do you understand why they are doing the IPO now, before reporting 1st quarter results?

They don’t even show their balance sheet in the main presentation. You need to go to the supplemental info. It’s a doozy.

They have over $100 billion in loans with only a $1 billion loan loss reserve. Yeah that should work out real well.

They have $14 billion of equity and only $77 billion of debt. Sounds like a fantastic once in a lifetime investment opportunity.

What do you think is going to happen when the $54 billion of subprime auto loans they’ve doled out over the last four years start to really go south? What do you think will happen as interest rates on their debt ratchet upwards? If they are already losing almost a billion per year, the future will be epic.

They originally filed to go public in March 2011. I wonder what took so long. I guess they wanted to get their loss under $1 billion before allowing the masses to buy into their success story.

But I’m probably wrong. Facts don’t matter. This is a fantastic investment opportunity for the muppets. Step right up and buy some Ally Financial. You bailed them out once, why not do it again?

Ally Financial Inc. (ALLY) priced its initial public offering at $25 a share after markets closed on Wednesday. The IPO price was at the low end of the expected range. The company sold 95 million shares Thursday morning for gross proceeds of $2.38 billion.

The low-end pricing of the stock is just another poke in the eye to U.S. taxpayers. All the proceeds will be used to pay back the U.S. Treasury’s $17 billion bailout of the company known as GMAC back in 2008 when the financial crisis hit. Thursday’s sale reduces the federal government stake in the company from about 38% to around 14%.

Underwriters are Citigroup, Goldman Sachs, Morgan Stanley and Barclays Capital, which have an overallotment option on an additional 14.25 million shares.

One analyst at BTIG has already put a Buy recommendation on the bank’s stock with a price target of $31 a share, according to a report at TheStreet.com. That is arguable given that Ally failed its most recent Federal Reserve stress test and has set up a subsidiary on which the bank intends to shed all its bad loans.

Ally also has about $79 billion in remaining debt that the bank has to roll over constantly as the principal payments come due. From Ally’s point of view, if interest rates never rise about 0.25%, it is all right with the bank.

Shares opened down 3% at $24.25 and have since picked up slightly to $24.57.

Getty Images

Getty Images

")