I stopped trying to predict markets back in 2008 when the Federal Reserve, Treasury Department, Wall Street bankers, and their propaganda peddling media mouthpieces colluded to rig the markets to benefit the elite establishment players while screwing average Americans. I haven’t owned any stocks to speak of since 2006. I missed the the final blow-off, the 50% crash, and the subsequent engineered new bubble. But that doesn’t stop me from assessing our true economic situation, market valuations, and historical comparisons in order to prove the irrationality and idiocy of the current narrative.

The proof of this market being rigged and not based upon valuations, corporate earnings, discounted cash flows, or anything related to free market capitalism, was the reaction to Trump’s upset victory. The narrative was status quo Hillary was good for markets and Trump’s anti-establishment rhetoric would unnerve the markets. When the Dow futures plummeted by 800 points on election night, left wingers like Krugman cackled and predicted imminent collapse. The collapse lasted about 30 minutes, as the Dow recovered all 800 points and has subsequently advanced another 1,500 points since election day. Krugman’s predictive abilities proven stellar once again.

‘If you’re committed enough, you can make any story work. I once told a woman I was Kevin Costner, and it worked because I believed it’ – Saul Goodman – Breaking Bad

“As calamitous as the sub-prime blowup seems, it is only the beginning. The credit bubble spawned abuses throughout the system. Sub-prime lending just happened to be the most egregious of the lot, and thus the first to have the cockroaches scurrying out in plain view. The housing market will collapse. New-home construction will collapse. Consumer pocketbooks will be pinched. The consumer spending binge will be over. The U.S. economy will enter a recession.” – Eric Sprott – 2007

In Part One of this article I provided the background of how our current debt saturated economy got to this point of ludicrousness. The “crazy” bloggers, prophets of doom, and analysts who could do basic math were warning of an impending financial crisis in 2006 and 2007, which would be caused by the issuance of hundreds of billions in subprime slime by the Too Big To Trust Wall Street shysters. Subprime mortgages, auto loans, and credit card lines provided the kindling for the 2008 conflagration.

Under normal circumstances we wouldn’t have seen such irrational, reckless, greedy behavior from Wall Street for another generation. But, Wall Street didn’t have to accept the consequences of their actions. They were bailed out and further enriched by their puppets at the Federal Reserve, the lackey politicians they installed in Washington D.C., and on the backs of honest, hard-working, tax paying Americans. The lesson they learned was they could continue to take excessive, reckless, unregulated risks without concern for losses, downside, or consequences.

In reality, the Fed and government have worked in tandem with Wall Street to create the subprime economic recovery. The scheme has been to revive the bailed out auto industry by artificially boosting sales through dodgy, low interest, extended term debt. With the Feds taking over the entire student loan market, they have doled out hundreds of billions to kids who don’t have the educational skills to succeed in college, in order to keep them out of the unemployment calculation.

That’s why you have a 5.7% unemployment rate when 41% of the working age population (102 million people) is not working. The appearance of economic recovery has been much more important to the ruling class than an actual economic recovery for average Americans, because the .1% have made out like bandits anyway. Who has benefited from the $650 billion of student loan and auto debt disseminated by the oligarchs in the last four years, the borrowers or lenders?

You know we are near or at a market top when shit stains like Ally Financial are brought public by fellow shit stains – Citi, Goldman, and Morgan Stanley. You’d have to be brain dead or an Ivy League trained economist to buy this turd sandwich at $25 per share. You’d have to be retarded shit eating muppet to buy this worthless government manipulated joke of a company. This is the company that has been doling out billions in subprime auto loans to the Free Shit Army for the last three years in order to prop up General Motors auto sales. They have been doing this because Obama and his minions instructed them to do so. Now that they are loaded with hundreds of billions in loans that will never be repaid, Obama is dumping this piece of shit on the public market where the Wall Street shysters will try to convince you to buy it. Jim Cramer thinks it’s the bomb.

I decided to go to their last SEC filing to get the real scoop about this joke. Here is the link:

You need to go to page 27 & 28 of their 29 page PR presentation to find out they LOST $190 million in the 4th quarter and $910 million for all of FY13.

This is a fabulous improvement over the $1.6 billion they LOST in FY12.

These government cronies have increased their auto loans outstanding by 100% since 2009 to $108 BILLION.

Page 14 of the presentation is the smoking gun. They had $843 million of delinquent auto loans in the 1st quarter of 2013. By the 4th quarter of 2013 delinquent loans had risen to $1.325 BILLION. That is a 57% increase in one year. SHOCKING!!! Considering they have been making loans to deadbeats who can barely scratch an X on the loan document. Do you think this trend is going to reverse in the 1st quarter of 2014? Do you understand why they are doing the IPO now, before reporting 1st quarter results?

They don’t even show their balance sheet in the main presentation. You need to go to the supplemental info. It’s a doozy.

They have over $100 billion in loans with only a $1 billion loan loss reserve. Yeah that should work out real well.

They have $14 billion of equity and only $77 billion of debt. Sounds like a fantastic once in a lifetime investment opportunity.

What do you think is going to happen when the $54 billion of subprime auto loans they’ve doled out over the last four years start to really go south? What do you think will happen as interest rates on their debt ratchet upwards? If they are already losing almost a billion per year, the future will be epic.

They originally filed to go public in March 2011. I wonder what took so long. I guess they wanted to get their loss under $1 billion before allowing the masses to buy into their success story.

But I’m probably wrong. Facts don’t matter. This is a fantastic investment opportunity for the muppets. Step right up and buy some Ally Financial. You bailed them out once, why not do it again?

Ally Financial Inc. (ALLY) priced its initial public offering at $25 a share after markets closed on Wednesday. The IPO price was at the low end of the expected range. The company sold 95 million shares Thursday morning for gross proceeds of $2.38 billion.

The low-end pricing of the stock is just another poke in the eye to U.S. taxpayers. All the proceeds will be used to pay back the U.S. Treasury’s $17 billion bailout of the company known as GMAC back in 2008 when the financial crisis hit. Thursday’s sale reduces the federal government stake in the company from about 38% to around 14%.

Underwriters are Citigroup, Goldman Sachs, Morgan Stanley and Barclays Capital, which have an overallotment option on an additional 14.25 million shares.

One analyst at BTIG has already put a Buy recommendation on the bank’s stock with a price target of $31 a share, according to a report at TheStreet.com. That is arguable given that Ally failed its most recent Federal Reserve stress test and has set up a subsidiary on which the bank intends to shed all its bad loans.

Ally also has about $79 billion in remaining debt that the bank has to roll over constantly as the principal payments come due. From Ally’s point of view, if interest rates never rise about 0.25%, it is all right with the bank.

Shares opened down 3% at $24.25 and have since picked up slightly to $24.57.

Where life had no value, death, sometimes, had its price. That is why the bounty killers appeared. – For a Few Dollars More

“Tell me, isn’t a sheriff supposed to be courageous, loyal and, above all, honest?” –Man with No Name – For a Few Dollars More

Whenever I get an idea for an article I plan to keep it short and sweet. But it never seems to work out that way. Once I start typing, the articles tend to grow exponentially. It happened again with my attempt to make sense of how the United States of America managed to screw our finances up so badly, that an epic collapse is within view to people with their eyes open to facts and the truth. You don’t end up in the predicament we find ourselves in today due to a couple minor mistakes over a short time frame. It took thousands of horrible choices, colossal doses of delusion, a heaping of stupidity, and a mountain of denial over decades to put us on the brink of economic collapse. An unholy amalgamation of demographics, fiat currency, debt, taxes, power and greed have led us to this point. Next we experience collapse, revolution and ultimately, retribution.

Since I’ve identified four major rationales for our impending doom, I’ve decided to write a four part series that can be read in small doses, rather than one enormous article. I don’t want anyone to miss tonight’s episode of Dancing With the Stars, get distracted from the Royal Wedding preparations, or skip the best reality TV show ever – Ben Bernanke’s press conference, while reading an 8,000 word article about the end of America. The four part series will have a Clint Eastwood theme. For a Few Dollars Morewill address the Baby Boomer impact on America’s decline. A Fistful of Dollarswill examine how the creation of the Federal Reserve and the income tax in 1913 set us on a path to ruin. Outlaw Josey Waleswill scrutinize the looting of America by a small group of powerful, connected, super rich men lurking in the shadows, but pulling the strings on our puppet politicians. Lastly, Unforgiven will detail the impending collapse of our economic system and the retribution that will be handed out to the guilty.

Over the last few weeks there seems to be consensus among many financial bloggers, whose credibility is far more trustworthy than the corporate mainstream media, that the country is teetering on the verge of economic collapse due to the complete capture of the government, financial, regulatory, and media by a small group of oligarchs. They have also been described as the super rich, plutarchs, ruling elite, and scum sucking leeches. The bloggers that I have the utmost respect for, including Jesse, Charles Hugh Smith, Mike Shedlock, Yves Smithand Gonzalo Lirahave all come to the logical conclusion the horrific economic situation of the country is a direct result of the greed, corruption, fraud, and plundering by a powerful connected group of rich financiers operating without fear of being brought to justice by the authorities.

While pondering the ruminations of these dedicated truth tellers, I was reminded of the Clint Eastwood Spaghetti Western For a Few Dollars More. The quotes above are representative of living in the USA today. There are supposed to be courageous, loyal and honest sheriffs that protect the citizens from crime, corruption and evil doers. But, just as we saw in the Old West of Clint Eastwood movies, the sheriffs are always corrupt and bought off by the evil cattle barons. In a world where life has no value and you can’t rely on law enforcement to protect your interests, the citizens eventually will need to turn to bounty hunters to take care of the bad guys. The bounty hunters of truth reside on the internet. They reside at Zero Hedge, Jesse’s Café Americain, Of Two Minds, Mish, Chris Martenson, and dozens of other anarchist websites. When you can’t trust your government, your bankers, your church, your media, or mega-corporate CEOs, you need to seek the truth where it can be found. The insightful bloggers who courageously print the truth on a daily basis have unanimously concluded that a small band of powerful elite have accumulated undue influence and control over this country, having brought it to the verge of economic collapse. How did this happen? Who is responsible? Why were they permitted to gain this power?

Boomers Come of Age

“If those in charge of our society – politicians, corporate executives, and owners of press and television – can dominate our ideas, they will be secure in their power. They will not need soldiers patrolling the streets. We will control ourselves.” – Howard Zinn

Whenever I direct any blame for our economic woes towards the Baby Boom generation they react as expected. They blame the GI Generation for creating the welfare state. They declare that Generation X and the Millenials are just as greedy and self centered as the Boomers. Boomers are great at blaming, ridiculing and acting pompously, while taking no responsibility for their actions and more importantly their inaction. This generation cannot avoid their responsibility for the state of affairs. They like to take credit for their stand against the Vietnam War and their protests against the man during the 1960s. They don’t like to take credit for turning into materialistic, greedy, selfish, short-term focused bastards. When a generation of 76 million people decides to go in a particular direction, the country will go in that direction. While blaming FDR and the GIs who stormed the beaches of Normandy for creating the unfunded Social Security and Medicare liabilities, the Boomers have been voting since the mid-1960s and have been in control of corporate America and the levers of government since the early 1980s.

The U.S. Congress is dominated by Baby Boomers today and has been dominated by this generation since the 1990s. The Senate has 60 Boomers out of 100, while the House of Representatives has 254 Boomers out of 435 members. Boomers occupied the White House from 1992 through 2008. They have had the political power and control of the agenda for two decades and have failed miserably. Rather than do what was best for the country for the long-term, they took the expedient, easy, vote getting route. Promise more than you could ever deliver and let future generations worry about the consequences. Not one true noble statesman has arisen from this generation of myopic, self centered “Me Generation” political hacks. Even as the country nears the precipice, they continue to address the great issues of the day with talking points supplied by other Baby Boomer PR maggots from Park Avenue. These weasels care not for the country, but worry only about poll numbers and the next election cycle. An apathetic public, dominated by the Baby Boom generation, has the attention span of a gnat. As long as they can make the lease payment on their Escalade, use one of their 15 credit cards at the Mall, be entertained by 600 cable TV stations, play with the latest iSomething, live in their McMansion for two years without making a mortgage payment and consume massive quantities of fast food, then any thoughts of future generations or civic duty are unnecessary. Live for today has been the rallying cry for the Boomer generation. Pot was their drug during the 1960s. Debt has been their drug since 1980.

The drug (debt) dealer for the Baby Boom generation has been the Wall Street mega-banks, coincidentally, run by Boomers. The entire corrupt financial industry is being run by Boomers. The CEOs, CFOs, and the thousands of Harvard MBA VPs that created the fraudulent derivative scheme to bilk billions from clueless municipalities, pension funds and American taxpayers are all Boomers. It is no coincidence that the great debt delusion began in the early 1980’s. Jim Kunstler captured the essence of Boomer transformation:

“The Baby Boomers came back from the land, clipped their pony tails, discovered venture capital, real estate investment trusts, securitization of “consumer” debt, and the Hamptons. Greed was good.”

The Boomer CEO hall of scam has been built on the brilliance and financial acumen of Lloyd (god’s work) Blankfein, Charlie (keep dancing) Prince, Jamie (friend of Obama) Dimon, and the king of the Boomers, Hank (the system is sound) Paulson. These mainstays of crony capitalism led the Boomer charge of greed, greed and more greed. The Baby Boomer generation has been the proverbial pig in a python working its way through the decades as presented below. By 1985, Boomers had entered the work force in full force with the entire generation between the ages of 25 and 42. It will be a great day when the python craps this pig of a generation out the other end.

It is not a coincidence the National Debt growth has far outstripped GDP growth since 1980. Boomers had been spoiled their whole lives and felt they deserved the goodies today while passing the bill to future generations. They voted for politicians who promised them more benefits, more programs, more subsidies, more tax breaks, more military adventures, and more pleasure. And this was “paid for” with more debt. Thirty five years of government debt declining as a percentage of GDP was reversed over the next thirty years starting in 1980, pushing it past the 90% tipping point in the last year. The country is over-indebted to the tune of $9 trillion on a current basis and $100 trillion on a long term accrual basis.

There is no better picture of Boomer decadence and myopia than an historical view of the national savings rate. The parents of the Boomers understood the meaning of sacrifice and investing in the future of the country. During World War II they bought US War Bonds to support the cause. From 1950 through 1985, the savings rate consistently ranged between 7% and 12%. Americans had this odd notion that if you saved more than you spent, you actually got ahead in life. Excess savings were used to invest in new plants and equipment that were used to produce goods and employ more Americans. By 1985, the Boomers considered these notions as quaint and old fashioned. The savings rate methodically declined until it went negative in 2006, just prior to the worldwide financial conflagration. Our inspirational Boomer president George (Mission Accomplished) Bush while waging two wars of choice, asked for the ultimate sacrifice from the Boomers. He solemnly urged them to buy a GM SUV with $0 down and 0% interest for 7 years, so we could defeat the terrorists. The Boomers who ran GMAC were more than happy to make loans to people with no income so they could “purchase” a $40,000 ostentatious gas guzzling hog. They were doing their patriotic duty for the good of the nation. It brings a tear to my eye just thinking about it.

The Boomers not only heeded George’s call, but they did him proud by buying 8,000 sq ft McMansions with $0 down and negative amortization ARMs. Luckily, the executives at the mortgage origination sweatshops were Boomers. They found no good reason to verify income or assets before loaning someone $600,000, because they knew their fellow Boomers at the rating agencies would rate the bundles of these toxic shit loans as AAA so the Boomers on Wall Street could sell them to greater fools. GMAC’s exemplary subprime mortgage arm – Ditech, did a bang up job getting migrant Mexican workers into $450,000 homes in California’s inland empire. As the tsunami of bad debt swept toward shore, delusional Boomers across the land borrowed $500 billion against the inflated value of their McMansions and installed granite counter tops, stainless steel appliances, home theatres, elegant patios, Olympic sized pools, and with the excess home equity, leased a BMW or two. The first devastating tsunami wave hit in 2008 and wiped out billions in faux Boomer wealth. Instead of learning a brutal lesson and reverting back to saving and frugality, the “never say sacrifice” Boomers ventured out to where the waves had subsided looking for more trinkets and treasures.

The next tsunami wave is on its way. The delusional Boomers will be surprised again.

The Boomer persona has been formed over the last five decades and the country will deal with the consequences for decades to come. The clean cut Beaver Cleaver children of the 1950s turned into the pot smoking Dobie Gillis of the 1960’s, then into the slimy Gordon Gekkos of the 1980s and ultimately into the eternal wealth seeking Gollums of today.

This Boomer debt orgy over the last thirty years would have made Caligula blush. Of course, none of this could have happened without the Creature from Jekyll Island. I will address this aspect of our fate in Fistful of Dollars– Part Two.

Now for the righteous indignation from the Boomers that think I have unfairly lumped them all together as one. Their reactions are predictable. Even though they have had the means, the power and the time to reverse the course of USS Titanic, they plowed full steam ahead into the abyss. The GI Generation is dead. Generation X doesn’t hold the reins of power. The Boomer generation needs to look in the mirror to recognize who is to blame. I’m sure there are a few good Boomers out there somewhere, but as a generation they have failed this country and our unborn generations miserably.

The two stories below tell me all I need to know about the great auto recovery. I bet you didn’t know that GM and the rest of the automakers record their sales when the vehicles are shipped to their dealers. Zero Hedge has been all over the channel stuffing being done by Government Motors for the last two years as they now have 60% more vehicles sitting on dealer lots than two years ago, even though sales are up less than 20%. And now we see that Obama is doing his union bretheren a favor and buying GM cars like they’re going out of style. You the American taxpayer are subsidizing GM, just as you took the $50 billion hit when Obama screwed bondholders using your money.

Lastly, we know for a fact that Ally Financial (aka GMAC) is still 85% owned by you. It is dishing out subprime auto loans like SNAP cards in West Philly. Moody’s is already warning about the coming disastrous losses that will be experienced by YOU the taxpayer when all these crap loans go bad. But that doesn’t matter to Obama. There is an election to be won. The losses to the American taxpayer will come in 2013 and 2014. Don’t expect the MSM to fill you in on the government scam. They are part of the scam, as their ad revenue is dependent on car ads. What a great country.

GM Finds Creative New Ways To “Stuff Channels”, Get Backdoor Taxpayer Bailouts

Submitted by Tyler Durdenon 07/06/2012 12:53 -0400

Zero Hedge readers know that we have long followed channel stuffing trends at GM, whose month-end dealer inventory hit a record (for the post-reorg company which is completely different from the pre-bankruptcy entity) of 713K cars stuck in various dealer “channels” at the end of March 2012, and since then has been stagnant at just about 700K, with the most recent June number coming at 701K, an increase of 6K over May. It would be great to assume that the company has given up on cheap ways to cheat investors and the taxpaying public into believing it is doing better. It would also be wrong. As it turns out, GM has merely turned to more backdoor methods of stuffing channels, and getting money from its biggest shareholders, which still happens to be Joe Sixpack (and “superpriority” labor unions of course) by way of the US Treasury, with 32% of the common stock.

It looks like General Motors will be throwing everything in but the kitchen sink to help fluff its second quarter earnings numbers. Taxpayers continue to help with the cause as President Obama campaigns on the “success” of GM following the manipulated bankruptcy process that cost taxpayers $50 billion and another $45 billion of tax credits gifted to GM to help protect powerful UAW interests. We now learn that government purchases of GM vehicles rose a whopping 79% in June.

As a reminder, this is how GM’s general channel stuffing looked like for all its vehicles:

However there is a rather important data subset here:

According to a Bloomberg report, “GM said inventory of its full-size pickups, which will be refreshed next year, climbed to 238,194 at the end of June, a 135 days supply, up from 116 days at the end of May.” 135 days supply is huge, the accepted norm is a 60 day supply. The trick here is that GM records revenue when vehicles go into dealership inventories, not when actually sold to consumers.

This is how pickup truck channel stuffing looked in the period that the company has released the data, or since December 2011. Not pretty.

And while we all know by now that the tried and true mechanism to channel stuff is a staple when it comes to fooling the buyside as to its business efficacy, the fact that its biggest shareholder has become a key marginal client of GM should make one’s head spin at the Ponziness of the transaction:

The government’s increased spending on GM vehicle purchases presents yet another conflict of interest as Treasury refuses to sell taxpayers’ stake in GM and Obama campaigns on the auto bailouts. It does not appear that any members of Congress (from either party) are questioning the increased spending. Also ignored was the Department of Energy’s gifting of $2.7 million of taxpayer money to GM to reduce energy consumption in its door manufacturing process by 50%. The DOE seems to be one of the main conduits to funnel taxpayer funds to cronies of the Administration. The $2.7 million contribution to GM comes after additional millions of dollars were spent by the DOE on advisory fees paid to legal firms that helped smooth the way for the GM bankruptcy process (as reported here); another move that went unquestioned.

And there is more:

GM claimed that sales increases did not rely on incentive spending, which appeared to remain in check, but one analyst during GM’s sales conference call questioned whether the company’s “stair step” incentive spending was accurately depicted. This incentive spending kicks in after dealerships report final sales figures for the month and may be yet another deceptive way for GM to fudge its numbers. Not mentioned was GM card rewards programs that do not get counted as incentive spending.

Why is GM forced to succumb to such increasingly more deceptive practices? Why simple presidential election politics of course: when a failed company like GM is destined to symbolize the “success” of one’s administration, there aren’t many straws one can latch on to.

The upcoming earnings announcement by GM is, politically, the most important to date. The pressure is on Government Motors to appear financially strong as this may be the last earnings report before November elections and sets the stage for how “successful” GM is. One of GM’s past tricks to help fudge earnings numbers has been to stuff truck inventory channels. Old habits die hard at GM.

The article goes on to quote Kelley Blue Book’s Alec Gutierrez who stated “They’re (GM) likely going to have a relatively high days supply of trucks moving forward and they’re already placing some pretty aggressive cash incentives on the hood. It’s going to eat into their profit margins…”

GM’s earnings announcement comes on August 2nd. The main headwinds will be weak European operations and growing pension liabilities. The headline number for earnings should be viewed skeptically and an eye kept on the share price reaction after the conference call. Expect Government Motors to put a positive spin on its financial health as the stakes are now at their highest. The long-term health of GM remains in question and the true financial picture may not surface until well after voters decide who will be running our country. Eventually we will see just how successful GM really is.

At the end of the day, all of this is noise. If China retaliates in kind to the recen escalation by Obama vis-a-vis alleged Chinese deceptive trade practices, the GM will soon be able to kiss half of its top line, and who knows how much of its margin and bottom line goodbye. Because when half of your sales go to the one country which America’s non-existent (and unionized) manufacturing base loves to hate, the last thing you want is to bite the hand the pays the bills. Yet this is precisely what is going on as the politics of this country become so misguided that in the pursuit of a few extra votes, the administration is willing to sacrifice what little clout and momentum the recently bankrupted automaker may have generated.

In the meantime, looks for channel stuffing and direct government purchases to soar to unseen levels in the weeks and months heading into the presidential election as GM (and its 40% stock price drop since the IPO) will certainly be a key debate point between the Democrats and the GOP.

Moody’s: Hot US subprime auto lending market has parallels to the 1990s

Global Credit Research – 28 Jun 2012

New York, June 28, 2012 — The subprime auto lending market in the US is developing a resemblance to its condition in the early- and mid-1990s, when overheated competition among lenders led to poor underwriting that drove up losses, says Moody’s Investors Service in a new report. As in that earlier period, capital is pouring into the sector and the issuance of subprime auto asset-backed securities (ABS) is booming.

“It is too early to predict whether today’s subprime lending market will deteriorate as it did in the 1990s, but the early similarities between then and now suggest that losses will climb if competition intensifies,” says Moody’s Vice President Peter McNally, author of the report “US Subprime Auto Lending Market Harkens Back to 1990s.”

Over the last two years, because of the sector’s profitability, a large amount of private equity investment has gone into the subprime auto lenders, many of which are relatively small, specialty finance companies, says Moody’s.

Moody’s says the interest of investors from outside the subprime auto market niche and the potential for increased competition carry the risk that losses could increase if a race for profits and market share lowers underwriting standards. The growth in the market can lead to capacity issues, says Moody’s McNally. “When losses rise quickly, inexperienced lenders have trouble servicing a loan portfolio that requires more attention.”

In the 1990s, the number of small lenders boomed, leading to intense competition for loans that in turn led to weak underwriting and high losses on securitized loans. Net losses in subprime auto ABS, according to Moody’s, jumped from under 3% in early 1995 to over 10% in December 1997.

For the past several years subprime auto loan performance has been strong, with the net loss rate currently below 4%. However, the credit quality of pools securitized in 2011 and 2012 indicate that credit has loosened since 2010, says Moody’s.

Issuance of subprime auto ABS is on pace this year to exceed the robust issuance of 2011, which comprised 24 deals, totaling $14.3 billion.

Moody’s notes several differences between today’ s market and the overheated market of the 1990s.

One credit positive for today’s market is that most lenders no longer practice gain on sale accounting, whereby lenders capitalized securitization gains and credited them to equity, which made their balance sheets look stronger than they were.

Another is that the market is not yet overcrowded with new lenders. Moody’s counts 13 active securitizers at the moment, compared with 34 issuers in 1997.

An important credit negative is that transactions are no longer backed by monoline guarantors. These bond insurers absorbed losses on transactions that would have otherwise defaulted in the 1990s and took over transaction servicing from failing lenders.

Americans have an illogical love affair with their vehicles. There are 209 million licensed drivers in the U.S. and 260 million vehicles. The U.S. has a higher number of motor vehicles per capita than every country in the world at 845 per 1,000 people. Germany has 540; Japan has 593; Britain has 525; and China has 37. The population of the United States has risen from 203 million in 1970 to 311 million today, an increase of 108 million in 42 years. Over this same time frame, the number of motor vehicles on our crumbling highways has grown by 150 million. This might explain why a country that has 4.5% of the world’s population consumes 22% of the world’s daily oil supply. This might also further explain the Iraq War, the Afghanistan occupation, the Libyan “intervention”, and the coming war with Iran.

Automobiles have been a vital component in the financial Ponzi scheme that has passed for our economic system over the last thirty years. For most of the past thirty years annual vehicle sales have ranged between 15 million and 20 million, with only occasional drops below that level during recessions. They actually surged during the 2001-2002 recession as Americans dutifully obeyed their moron President and bought millions of monster SUVs, Hummers, and Silverado pickups with 0% financing from GM to defeat terrorism. Alan Greenspan provided the fuel, with ridiculously low interest rates. The Madison Avenue media maggots provided the transmission fluid by convincing millions of willfully ignorant Americans to buy or lease vehicles they couldn’t afford. And the financially clueless dupes pushed the pedal to the metal, until everyone went off the cliff in 2008.

America is proving itself to be insane as described by Albert Einstein:

“Insanity: doing the same thing over and over again and expecting different results.”

The 2008 cataclysm was created by the voracious greed and avarice of Wall Street, sustained by corrupt politicians in Washington, non-existent regulation by banking regulators, Federal Reserve easy money policies, unspoken guarantees of Fed bailouts if Wall Street excess risk taking blew up, and millions of delusional Americans with an unlimited credit line. Excessive debt created the problem. Adding debt is the present solution to the problem. And the accumulation of debt will lead to a tipping point that destroys the U.S. dollar and topples the Great American Empire.

This spiral of government sponsored debt financed debacles has shockingly accelerated as we have supposedly been experiencing an economic recovery for the last two years. The 2008 financial meltdown was the result of too much debt peddled to too many people who never had the means or intentions to repay the debt. The Wall Street peddlers of debt didn’t care if it got repaid because they had already packaged it, bribed Moodys and S&P to rate the toxic garbage as AAA, and sold it to their “clients”. Then they made derivatives bets that it wouldn’t be repaid and raked in billions more as their Ponzi scheme unwound. There was just one problem with their master plan. The Wall Street titans made their derivate weapons of mass destruction so complicated and confusing that their own evil organizations of Harvard MBAs didn’t understand them. Enough hubristic CEOs existed at enough financial firms (AIG, Lehman, Bear Stearns, Citicorp) to bring the entire system crashing down as the toxic derivatives intertwined every major institution in the worldwide banking cabal.

What has happened since those dark days of 2008 is mind blowing in its epic proportions and epic stupidity. To quote Doug Casey, “Not only haven’t we done the right thing, we’ve done the exact opposite of the right thing.” It is absurd and ultimately suicidal to cure a debt disease by administering massive doses of more debt. But that is exactly what those in power have done. The National Debt has risen from a $9.7 trillion to $15.6 trillion, a 61% increase in three and a half years, while our real GDP has grown by $244 billion, a 1.9% increase. Not exactly a fabulous return on investment. But at least there are 7 million less people employed today than there were at the peak in 2008. Plus, senior citizens and middle class savers have seen $450 billion of annual interest income they were earning in 2008 pilfered from their savings accounts and handed to the Wall Street banking elite through Ben Bernanke’s ZIRP.

The Federal Reserve has tripled their balance sheet (actually your liability) from $950 billion to $2.9 trillion. Various other Federal government controlled bureaucracies (Fannie Mae, Freddie Mac, FHA) have stealthily subsidized hundreds of billions in losses on behalf of the criminal Wall Street banks. Other Federal government run agencies (BLS, BEA, CBO) exist solely to massage, manipulate, misuse, and malign economic data and financial projections in order to muddle, misinform and mislead the American people about the true nature of our ongoing economic calamity. Propaganda and obfuscation are the scheme of choice by the powers that be. They are counting on decades of government run public education to insure that millions of non-critical thinking dullards will be unqualified or uninterested in the truth about our grim economic prospects. The oligarchy’s master plan has centered on houses, automobiles, and the illusion of a jobs recovery.

Whenever I’m trying to understand the motivations of the sociopathic Washington politicians, Wall Street bankers and mega-corporation CEOs, I always come back to the words of master manipulator Edward Bernays:

“The conscious and intelligent manipulation of the organized habits and opinions of the masses is an important element in democratic society. Those who manipulate this unseen mechanism of society constitute an invisible government which is the true ruling power of our country. …We are governed, our minds are molded, our tastes formed, our ideas suggested, largely by men we have never heard of. This is a logical result of the way in which our democratic society is organized. Vast numbers of human beings must cooperate in this manner if they are to live together as a smoothly functioning society. In almost every act of our daily lives, whether in the sphere of politics or business, in our social conduct or our ethical thinking, we are dominated by the relatively small number of persons…who understand the mental processes and social patterns of the masses. It is they who pull the wires which control the public mind.”– Edward Bernays, Propaganda, 1928

The relatively small number of wealthy men thinks they are smarter than the masses and can manipulate them through their control of the government, the financial system and the media. The players in this game remain the same, but they have switched positions. The debt accumulation which led to the 2008 collapse was heavily concentrated on the books of the ruthless Wall Street psychopathic banks and on the backs of a readily pliable public. Today, the Federal government and the Federal Reserve have switched positions with their banker puppet masters, essentially shifting all past and future debt onto the backs of the American middle class. The Federal Reserve Flow of Funds Report, issued two weeks ago, reveals the extent of this blatant scheme to screw the American people in order to save and further enrich the Wall Street psychopaths who won’t be satisfied until their looting and pillaging leads to complete collapse and the world erupting into a world war. The despicable facts are as follows:

Total U.S. credit market debt has RISEN from $50.9 trillion in 2007 to $54.1 trillion as of 12/31/11, a $3.2 trillion increase.

Household debt has declined from $13.8 trillion in 2007 to $13.2 trillion as of 12/31/11. The mainstream media would point to this $600 billion decline as proof that Americans have embraced austerity and have learned their lesson. Of course that would be a lie. The Wall Street banks have written off $200 billion of credit card debt and the 5 million completed foreclosures extinguished another $800 billion of mortgage debt. The truth is that consumers have continued to pile up debt.

Much has been made of corporate America being flush with cash. If they are so flush, why have they added $900 billion of debt since 2007, an increase of 13% to an all-time high of $7.8 trillion?

The revealing data shows up in the financial company data. These Wall Street national treasures have reduced their debt from $17.1 trillion in 2008 to $13.6 trillion as of 12/31/11. How were they able to do this, while writing off $1 trillion of consumer debt?

You guessed it. They dumped it on the American taxpayer. The Federal government increased their debt from $5.1 trillion to $10.5 trillion. And our old friends called government sponsored enterprises (Fannie, Freddie, Student loans) increased their debt from $2.9 trillion to $6.2 trillion. Wall Street banks and millions of deadbeats who chose to game the system and live the good life have effectively foisted their $4.5 trillion of debt upon the backs of middle class taxpayers who lived within their means. Another $4.2 trillion has been pissed down the toilet by Obama with his $800 billion Keynesian porkulus program, home buyer tax credits, cash for clunkers, green energy boondoggles, 47 million people on food stamps success story, 99 weeks of unemployment, doubling of SSDI membership, and his multiple wars of choice in the Middle East.

The average hard working, taxpaying American has been enslaved in debt of such proportions that they will never be able pay it off. Your share of the $15.6 trillion National Debt is now $50,000, and growing by $4,500 per year. Your share of the future unfunded liabilities, created by the people you elected, is approximately $350,000. This crushing burden is in addition to the $13.8 trillion of mortgage, credit card, student loan, and auto loan debt Americans have accumulated in the last three decades of delusion. Forty percent of all credit card users do not pay-off their credit card every month and carry an average balance of $16,000 at an average interest rate of 15%. Good to see the Wall Street banks passing along some of their 0% borrowing windfall to their “customers”.

Source: TF Metals Report

Pedal to the Metal

You may have noticed the corporate mainstream media, crooked politicians and lying Wall Street shills attempting to pound the economic recovery storyline into the consciousness of a terminally distracted populace. This is part of the Bernays inspired master plan of a small cabal of powerful men to control the public mind and keep our mass consumer society functioning smoothly so these corporate fascists can continue to gorge upon the carcass of a once vital republic. Decades of mass media consumer indoctrination, dumbing down of children through public school education and the conscious manipulation of attitudes and opinions of the malleable masses has succeeded. The invisible government of the rich and powerful has effectively converted responsible citizens into mindless consumers of products, bought with debt, peddled by associates of the invisible government. The crowded shopping malls, automobile showrooms, and restaurants are a testament to the power of propaganda and the intellectual bankruptcy of a vast swath of the American population.

Only psychopaths would encourage and condone behavior that would financially enrich themselves while destroying the lives and personal wealth of millions. The invisible government (Wall Street bankers, D.C. political hacks, mega-corporate executives, mass media titans) exhibits all the traits of a psychopath as described in a recent Harvard Business Review article:

Glibness and superficial charm

Lack of empathy

Consistent decisions in their self-interest, even where it is ethically questionable

Chronic, sometimes transparent lies, even with regard to minor things

Lack of remorse

Failure to take responsibility for their actions, and instead blaming others

Shallow emotions

Ignoring responsibilities

Persistent focus on gratifying their own needs at the expense of others

Conning and manipulative behavior

Do you recognize any of these traits in our president (Obama), congressmen (Weiner, McCain) Wall Street bankers (Dimon, Blankfein), corporate CEOs (Immelt), and mass media titans (Murdoch)? These people and many more like them will stop at nothing to further their self-serving agenda. They are intelligent and highly skilled at lying and manipulation. They lack empathy and don’t care what others think as they relentlessly pursue riches and power no matter the damage they inflict upon the people they so casually abuse, scorn and look down on. These are the people attempting to convince you that the path to economic recovery is through increased spending by consumers, utilizing debt supplied by them.

The entire recovery theme is a sham, financed by the Federal government with your tax dollars and the tax dollars of future unborn generations. I’ve arrived at this conclusion after pondering what I’ve been seeing with my own two eyes and through the insightful analysis found in the non-mainstream media (Zero Hedge, Jesse, Mish and many others). The mantra being pounded relentlessly by the mainstream media is that retail sales are booming and the unemployment rate has declined significantly, therefore an economic recovery is at hand. The chart below reveals the dramatic surge in vehicle “sales”. The annual pace is all the way back to 15 million, from the low below 10 million in 2009. The brief surge in mid-2009 was due to Obama’s highly successful Cash for Clunkers program that cost taxpayers $2.8 billion or $24,000 per car sold. It was highly successful for Government Motors (GM) and their union workers (Obama voters).

This rapid surge in auto sales has also resulted in a boost to overall retail sales, which have reached an all-time high. Automobile “sales” make up 18% of the retail sales number, by far the largest segment. The “record” retail sales are the result of surging gasoline sales, swelling food inflation, and a somewhat confusing cascade of car sales. It’s somewhat confusing until you realize how and why the 50% rise in vehicle sales has been accomplished by our Bernaysian masters. Retail sales in the first two months of 2012 are up 8.2%, led by a 9.2% wave of motor vehicle sales. Auto sales are at levels last seen in early 2008. This seems peculiar, since there are still 7 million less employed people in the country than in early 2008 and the real median household income is 9% lower than it was in early 2008. Real average hourly earnings have fallen for the last three months and are 1.2% lower than they were in October, 2010. A critical thinking person might ask himself, how could American households with less jobs and lower wages increase their purchases of automobiles by 50% in the last two years?

The answer is just what you expected. A phenomenal amount of debt peddled to people without the means or intent to ever repay the debt by the usual suspects: Ally Financial, Capital One, Wells Fargo, JP Morgan and Bank of America. These fine upstanding institutions control 25% of the auto loan market. They doled out $24 billion of new car loans in the 4th quarter of 2011, with an outpouring of loans to those downtrodden subprime borrowers and an extension in the average loan length beyond 6 years. Subprime borrowers now account for 45% of all auto loans. As a refresher, subprime borrowers generally have little or no assets, have a history of late payments or defaulting on obligations, and have low incomes. No worries there. When has making hundreds of billions in subprime loans ever caused a problem before. Ally Financial CEO Michael Carpenter had this to say about the market:

“We have seen crazy, irrational competition in the subprime end of the marketplace, which is one reason why more banks are targeting the lower end of the market.”

Bank of America and Capital One increased their market shares of the auto loan market by 40% in the 4th quarter as they attempt to keep up with Ally Financial in reckless lending to deadbeats. If you aren’t familiar with Ally Financial, then you should be. You own 74% of this POS. Here is a brief summary:

GMAC, after contributing mightily to the financial crash of 2008 through their reckless subprime mortgage (Ditech) and auto lending and requiring a $16 billion bailout from American taxpayers, changed its name to Ally Financial in 2009. It’s sort of like John Dillinger using acid to try and change his fingerprints.

Ally Financial provides financing for all GM and Chrysler customers and dealers and is the market share leader in auto lending.

Ally Financial still owes the American taxpayers $12 billion.

Ally Financial is a ward of the Federal government and will do anything it is told to do by Obama. The recent foreclosure fraud settlement required Ally to pay $250 million to the customers it defrauded. They will only pay $110 million based on their inability to pay $250 million. Sounds like a company that should be increasing their subprime loan portfolio. Obama and his minions instead received a commitment from a lender they own and control to cut principal for delinquent borrowers and refinance underwater borrowers. And Obama didn’t even offer us a cigarette afterwards.

Ally Financial, along with Capital One, failed the Federal Reserve stress test last week. Ally, Capital One, Bank of America, and Citicorp are dead banks walking. Brilliant bank analyst Chris Whelan succinctly sums up their fate after analyzing the Federal Reserve stress test results:

“When you get to junior liens and HELOCs you will understand why I have been saying that Ally Financial and BAC need to be restructured. With a plus 20% loss rate on second liens, Ally has substantial capital issues to put it mildly. But look at C right behind them with a loss rate in the mid-teens followed by BAC. Yikes. This type of loss rate is typical for credit cards and both of these second lien portfolios are > $100 billion.

And the real lesson, dead friends, is that the good old USA is a subprime nation, a society of individuals whose aggregate probability of default is probably around a “B” to “CCC.” Convert the loss rates in the stress tests to bond ratings using the break points from Moody’s or S&P and tell me what you see.

Last point on Ally Financial: Yikes. Probably the weakest results of the whole group. Memo to POTUS: File Ch. 11, sell auto biz and bank to GM in 365 sale. Liquidate ResCap. Declare success. But do not be surprised if BAC follows if Ally goes into bankruptcy. The one thing that the Fed almost completely ignores is the vast financial risk facing BAC and Ally, and to a lesser degree, WFC, JPM and C.”

When you understand this background, anecdotal evidence that seems absurd starts to make sense. I spend two hours per day on the road and have plenty of time to observe my surroundings. I drive through the Mantua section of West Philadelphia every day. The average household income in this neighborhood is $16,000. The average home value is $25,000. The true unemployment rate exceeds 40%. At least 20% of the properties are vacant and the neighborhood resembles Baghdad. Last week, I counted six brand new vehicles with registration tags in their back windows in a one block radius of this neighborhood. Every block has newer model Ford Expeditions, GMC Sierras, BMWs, Acuras, Cadillacs, and Mercedes sprinkled among the squalor. Someone is loaning these people the money to buy these $40,000 vehicles or approving them for leases. This neighborhood puts the SUB in subprime. No financial firm worth spit would make a six year $35,000 auto loan to someone in this neighborhood unless they were instructed to do so by the Federal government or were guaranteed that the future loss would be borne by someone else – YOU.

The GM, Chevy and Chrysler car dealer ads in my local paper actually have the following headline in bold:

Have credit problems? NO PROBLEM

Most of the ads don’t even list the prices of the vehicles. They either tout the 72 month 0% financing or they list the monthly lease cost. It seems that virtually any vehicle can be leased for $300 per month or less these days. This might explain why 25% of all vehicles are leased today. In reality, 25% of the cars being “sold” today are really just being rented for three years. Both the lessors and lessees are basing these transactions upon delusions and assumptions which will likely blow up in their faces and again cost – YOU.

An auto lease payment is based upon interest rates, the cost of the car, subsidies from the auto makers, and the expected residual value of the vehicle at the end of the three year lease. When have financial companies ever miscalculated any of these assumptions? How about 2001-2002 and 2008-2009? The reason auto leases are ridiculously low is because Ben Bernanke’s zero interest rate policy is providing free money to Ally Financial and the rest of the Wall Street zombie banks and creating huge mal-investment – Again. The auto makers see no risks, as the used car market has been extremely strong for the last year and they anticipate continued strong demand for cars as they come off their three year leases. Therefore, they have estimated the residual values three years out at a very high level. The strong used car market may have been slightly impacted by the destruction of 700,000 vehicles under Obama’s Cash for Clunkers debacle. The combination of excessively low interest rates and excessively high residual value estimates leads to ridiculously low lease rates. The sales statistics for the first two months of 2012 reveal why this will blow up in the faces of lessors and the predictably incompetent financial drug dealers.

Feb-12

% Chg Feb’11

YTD 2012

Cars

612,145

23.9

1,080,466

Midsize

304,601

25.6

532,818

Small

225,061

26.5

397,838

Luxury

81,476

22.7

147,647

Large

1,007

-85.8

2,163

Light-duty trucks

537,251

7.6

982,217

Pickup

148,956

13.8

273,430

Cross-over

225,621

0.4

412,974

Minivan

64,849

15.3

111,764

Midsize SUV

54,827

15.3

101,813

Large SUV

16,783

-5.4

31,566

Small SUV

13,926

24

25,951

Luxury SUV

12,289

12.4

24,719

It seems the delusional American public and their love affair with big SUVs, pickups, and their 8 cylinder luxury wheels will continue until they are hit over the head with the baseball bat of $5 a gallon gas. The Madison Avenue Bernays disciples have molded the minds and formed the opinions of millions of easily influenced, financially ignorant superficial Americans into believing the vehicle they drive is a true measurement of success. These people choose being up to their eyeballs in auto debt or perennial renters of luxury vehicles to appear prosperous to their neighbors and coworkers rather than actually achieving real success through the time honored tradition of earning more than you spend and saving the difference. The fact is that 80% of all the vehicles being sold in the U.S. are SUVs, pickups, crossovers, minivans, and larger cars that get 25 mpg or less.

As gas prices continue to rise towards $5 per gallon, a war with Iran looming in the near future, interest rates beginning to rise, and the country headed back into recession (MSM is wrong about the recovery), the car makers are poised to again experience enormous losses. Auto makers will have a sense of déjà vu as they have committed an epic blunder by overestimating the future value of the gas guzzlers they have been leasing. As a result, when the leases expire and auto makers take back the SUVs and pickups that get 15 mpg and attempt to resell them, the losses will run into the billions of dollars. There will be no one buying used gas guzzlers, with gas costing $5 per gallon. As the millions of subprime borrowers realize they can’t afford car payments, paying 40% more for gas, and trying to put food on the table, auto loan delinquencies will soar. This is as predictable as the housing market collapse in 2005. None of this matters to the psychotic governing elite who only care about the illusion of recovery today. These vampire squids will not be satisfied until every drop of blood is sucked out of the national carcass.

Ally Financial is part of the Federal Government and is being used to promote the agenda of the governing elite. They join Fannie Mae, Freddie Mac, and the Federal student loan peddlers as the primary tools of the corporate fascist powers that control this country. The nominal private ownership of these companies is a sham, as the state dictates how they will be run and who they will benefit. This corporate fascist empire is built upon an unholy alliance between big banks, big business, big media and big government, with each protecting and enriching each other. The psychopaths who are drawn to these organizations want to control people. They desire power, wealth, and the ability to manipulate public opinion. Their tactics include spreading fear and an atmosphere of paranoia in order to convince the populace that more government action will improve their lives. We are headed towards economic and financial collapse as these psychopaths will never willingly reverse course and the majority of our population has become so degraded (have you been to a Wal-Mart lately) that they are incapable or unwilling to confront the psychopaths.

Doug Casey in the latest Casey Report explains how evil and stupidity are a deadly combination:

“I would like to suggest that what really distinguishes political elites from normal people is not just a predilection for stupidity but a real capacity for evil. Evil might best be defined as the intentional and usually gratuitous commission of acts that are cruel or unjust. A person who commits many evil acts is a sociopath. The sociopaths who are naturally drawn to government eventually come to dominate it. They’re very dangerous people. They reset the social mores of the country they control. After a certain point, a critical mass is reached, and it’s GAME OVER. I suspect we’re approaching that point.”

The next time you hear a government drone, Wall Street shyster, or corporate mainstream media whore declare we are experiencing an economic recovery try not to laugh out loud. Their agenda doesn’t include making your life better. You are not in the club. Prepare accordingly.

I wrote this back in September 2009 before I had a website. I was reminded of it this morning as Weezer blared from my radio on the way to work.

For the last three decades millions of Americans have been living in Beverly Hills. How can this be? Only 35,000 people reside in Beverly Hills, California. Millions have acted like they live in Beverly Hills, where the median household income is $125,000. The median household income in the United States is $50,000. There are 116 million households in the United States. Only 12 million households have income of $125,000 or more. There are 60 million households making less than $50,000.

Why shouldn’t the 60 million households be entitled to live like the top 10%? This is America, where the American Dream of wealth and riches is achievable. Just one small problem. Millions chose to live like the privileged Beverly Hills elite without doing the difficult work to earn their way into the top 10%. They made these dreadful decisions of their own free will. No one forced millions of Americans to borrow and spend like drunken soldiers.

It appears that the psychology of the nation transformed in the early 1980’s. Was it the optimistic message of “Morning in America” preached to the country by Ronald Reagan? Was it the fact that the youngest Baby Boomers were turning 35, entering their prime spending years? Or, was it the long-term decline in interest rates from 18% to 1% over two decades? Whatever the rationale, millions are now drowning in deep pool of debt.

Auto Nation

Where I come from isn’t all that great

My automobile is a piece of crap My fashion sense is a little whack

And my friends are just as screwy as me Living in Beverly Hills – Weezer

I spend 500 hours per year in my car commuting on the Schuykill Expressway to and from work. In my spare time, I’ve calculated that I will spend at least a year of my life in traffic before I retire. While commuting at 5 mph on the Schuykill, I can’t help but survey the cars I’m sharing the road with. There are thousands jamming the highways in the Philadelphia area. There are 230 million cars in the U.S. and approximately 200 million drivers. We are a car crazed nation, with the number of cars per person 40% higher than Europe, 500% higher than China and 6,200% more than India. In 1970, when I was seven years old, the number of cars per 1,000 people was 529. Today it is 765, a 45% increase in three decades. Suburban dwellers have a love affair with their cars.

The average price of a new car exceeds $30,000 today. That is a nice chunk of change. I have a mental block paying that much money for an asset, that losses 20% of its value in the 1st year of ownership. My price limit is $20,000. I finance my cars over 4 years and try to get 10 years out of them. The 6 years of no payments goes directly into savings. My frugality regarding cars probably harks back to my father buying used cars during my entire childhood. Cars were a means of transportation, not a symbol of success. It appears to me that expensive luxury cars are an attempt at filling a psychological or emotional void in people’s lives. We spend half our lives in cubicles or offices and the other half in our shielded houses with gates and fences to keep people at a distance. The only time we are seen by others is on the highways and byways. An expensive sports car tells the world you are a success. A luxury car is a futile attempt at increasing your perceived happiness. Your fashion sense may be a little whack, but your car isn’t a piece of crap.

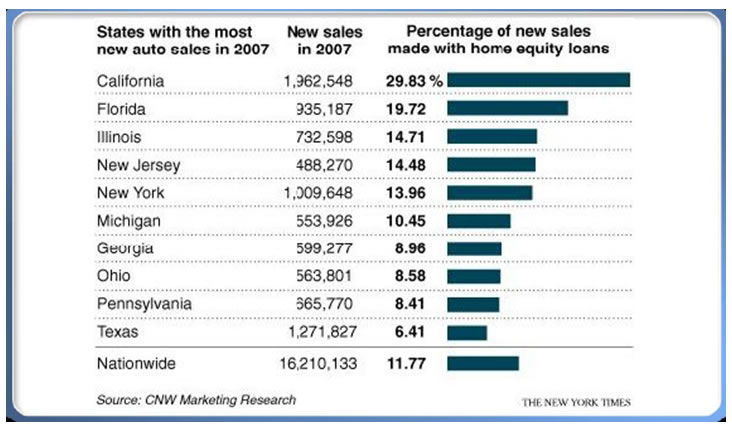

This brings me to the conundrum that has confounded me as I drive to work each day. There appears to be many more BMW and Mercedes vehicles on the road than people with enough income to own one of these vehicles. How can this be? I was befuddled. After a little research it became quite clear. The graphs below tell the whole sordid story. Borrow today, live like a Beverly Hills hotshot, roll the loan or lease into the next loan or lease in 3 years, and don’t be troubled about the future. According to the Federal Reserve, consumer non-revolving debt grew from $300 billion in 1980 to $1.6 trillion today. About $1 trilion of this is auto loans. The average automobile loan today is for 63 months, with some going as high as 84 months, compared with an average of less than 48 months in the early 1990s. In 1997 banks financed an average 89% of a new vehicle’s price. The average loan amount was $17,000. In 2007 banks financed 101% of a new vehicle’s price, since consumers borrowed to cover the amount they were upside down on their trade-in. The average loan amount is now $29,000. A full 40% of all trade-ins involve upside-down car loans. The average American car “owner” is in debt up to their eyeballs and upside down on their loan, but at least they look like a million bucks in the eyes of their neighbors and co-workers. Looking marvelous is what passes for achievement today.

Of course, it takes two to tango. A car buyer with no money wouldn’t be able to drive that beautiful BMW X5 or that Mercedes ML350 unless someone loans them the money to do so. This is where the creative geniuses from Wall Street entered the picture. Auto loans were securitized into packages and sold off to investors. The banks and finance companies who initiated the loans did not care if the loans went bad. Their sole intent was to move cars off the lots, not lose sleep about silly details like credit scores, income, or ability to pay back the loan. It worked wonders for the car companies. Annual sales rolled along at a 16 million per year clip. Car executives and bankers made ungodly salaries and bonuses. Then reality set in. Many borrowers couldn’t really afford their loans. Delinquency rates have soared to all time highs in the 10% range and are headed higher. The securitization market froze and annual sales have plunged below 10 million units. Another Wall Street success story.

The ability of car companies to make payments extremely low through long-term loans and leases is the reason an average Joe making $50,000 per year can drive a BMW and resemble someone making $150,000 per year. Chrysler and Ford generated 20% of their car sales through leases, while GM led the pack at 40% of their sales. Many of these leases were for SUVs and other giant gas guzzlers. When gas prices soared in 2008, the residual value of these gas guzzlers plummeted as the resale market disappeared. Ford and Chrysler have written off billions. The king of the hill, GMAC accumulated $33 billion of lease assets and is slowly but surely writting off $14 million of these “assets”, while the taxpayer funds their future bad leases.

Leases have made it possible for millions of Americans to drive the hottest luxurious wheels their limited cash budgets would not permit them to buy. Auto makers loved leases because they could sell higher-priced vehicles, which generate a gusher of profits in the short-term. By piling on inducements of their own, such as rebates or 0% financing deals, auto makers were able to subsidize consumers’ lease payments further. As a result, Americans have been able to have access to vehicles their parents never envisioned driving. Leases allowed anyone to look like a rock-star, driving luxury sedans, sports cars and Hummers costing $40,000 to $60,000. The Wall Street Journal describes a common scenario:

For Richelle Babcock, a mother of two young boys in Ann Arbor, Mich., leasing has made it possible to get new cars every couple of years. A few years ago, she took advantage of a trade-in deal and other incentives Chrysler was offering and got a $180-a-month lease on a 2006 Jeep Commander with a sticker price of about $35,000. There’s “no way,” Ms. Babcock says, that she would have bought the Commander outright. “I don’t want to have to own it and drive it forever.” Indeed, in December she turned it in and instead leased a new 2008 Commander. Her payment roughly doubled, but that’s mainly because the lease is much less restrictive about her annual mileage.

I’d like to ask Ms. Babcock a couple questions. Does she have college education funds set up for her two young boys? Does she have an emergency fund of 6 months of living expenses? How much does she have in her retirement account? I’m sure she would be offended by such questions. It’s her right to get a brand new car every two years. These are the people who can’t distinguish a need from a want.

This brings me to the chapter in this horror story that really sticks in my craw. I drive through West Philadelphia every day. The neighborhoods are decrepit, with boarded up houses, trash strewn vacant lots, grade schools that resemble prisons, and a substantial number of unemployed folks shuffling about from morning to night. These neighborhoods appear to have five times as many BMWs and Mercedes as my suburban upper middle class neighborhood. According to the U.S. Census, West Philly is a predominantly Black neighborhood, with a large proportion of unmarried high school dropouts living in poverty, occupying dilapidated houses with Direct TV dishes on their roofs. According to the U.S. Census, my neighborhood is occupied by people who are five times higher on the income scale.

The August unemployment figures from the BLS show that the unemployment rate for Black men is 17.0% versus 10.6% last August and versus 9.3% for White men. The unemployment rate for Black teenagers is 34.7%. With these figures, you would expect unrest, looting, and riots in West Philly. The civil unrest hasn’t happened in West Philly or anywhere else. I think I’ve figured out why. Just picture a 20 year old unemployed Black man calling his homies on his iPhone urging them to drag themselves away from staring at their 52 inch HDTVs with 600 stations on their Direct TV network, hop into their BMW X5, and drive over to the comprehensive healthcare riots. It’s not happening. Our elected officials, Federal Reserve and banking cartel have chosen to buy off the poor at the expense of the middle class, so the rich can get richer.

Easy money allows the poor to live like the rich. This explains why people in West Philly are able to drive $50,000 one year old BMWs, while I choose to drive an 8 year old CRV with 130,000 miles. My choice was to finance my $20,000 car over 4 years at 7%. I had a $500 monthly payment for 4 years and then was able to save $500 per month for the next 6 years, banking $36,000 in savings. The auto financing companies GMAC, Ford Credit, and Chrysler Credit offer rebate incentives, 7 year loans, and 0% interest to entice everyone to drive BMWs and Mercedes for a monthly payment below $500. The poor are more likely drawn to three year leases with even lower monthly payments. You can lease a BMW for $399 per month or lower. Once you are lured into 3 year leases or 7 year loans, you are ensnared in a lifetime car payment, never saving a dime. Over 4 decades, my method will leave me with $200,000 of savings. A perpetual car payment will leave you with $0 of savings. Millions have chosen this negligent path. Not only did they pursue this path, they hurtled themselves down the path with gusto by borrowing against their houses to buy cars. The numb-nuts in California and Florida were the worst offenders.

A drug addict still needs a dealer to get their fix. Politicians in Washington with their cohorts in crime, the Federal Reserve and the banking cartel, provided the drug of easy money. The unholy combination of a psychological need to appear successful and easy money has created a deadly recipe for those in the middle class who drive their modest cars for 10 years and save for the future. The black magic of securitization has allowed banks and finance companies to bestow credit card cards and car loans to high school dropouts making $20,000 per year in West Philly with no concern about getting repaid. They packaged this future bad debt, paid off Moody’s and S&P to rate it AAA, and dumped it on suckers throughout the world. Now, auto loan delinquency rates are at all time highs, 1.7 million cars were repossessed in 2008, with another 2 million likely to be repossessed in 2009.

The underprivileged people in West Philadelphia don’t comprehend that politicians and bankers are actually keeping them entrapped in poverty by providing them with easy credit and persuading them that making perpetual payments for cars, TVs, and other material goods is a normal lifestyle. When reality sets in and these people stop making their payments, no trouble for them. As the financial system came crashing down due to the millions of bad loans made by the banking cartel, their protectors Hank (Goldman) Paulson and Ben (Helicopter) Bernanke funneled TRILLIONS of your tax dollars and your children’s tax dollars and their children’s tax dollars to the banks that committed these crimes. The poor people in West Philly don’t pay taxes, so they got to drive BMWs and watch 52 inch TVs for awhile, and are left relatively unscathed. The middle class is paying the bill, losing millions of jobs, while seeing their 401ks drop by 40% and they are still driving their 10 year old cars. Government now wants you to pay more so the poor will have health insurance when they get injured in a BMW accident.

What’s My Payment?

I didn’t go to boarding schools

Preppy girls never looked at me Why should they, I ain’t nobody

Got nothing in my pocket

Living in Beverly Hills – Weezer

For the last three decades you didn’t need anything in your pocket to attract a preppy girl. You just needed to whip out one of your 10 credit cards and act like a Beverly Hills hotshot. Cash was for suckers. Credit cards are so easy to use. You just pull it out, buy whatever you desire at that moment and make a minimum payment every month until infinity. We’ve become a minimum payment nation. If you can handle the minimum payment, it’s yours. In 2006, the Census Bureau determined that there were nearly 1.5 billion credit cards in use in the U.S. A stack of all those credit cards would reach more than 70 miles into space — and be almost as tall as 13 Mount Everests. Consumer credit debt has risen from $400 billion in 1980 to $2.5 trillion today. Consumers have an average of 5.4 credit cards with $973 billion outstanding. The average outstanding credit card debt for households that have a credit card was $10,679 at the end of 2008. The average American with a credit file is responsible for $16,635 in debt, excluding mortgages, according to Experian. The most fascinating fact is that the top 10 U.S. credit card issuers held an 87.55% market share of $973 billion in general purpose card outstanding in 2008. These 10 banks are coincidently the same banks that brought down the financial system (Bank of America, Citicorp, JP Morgan Chase, Wells Fargo, Capital One, HSBC, American Express, Discover, US Bank, USAA).

Consumer Credit Debt

It has taken Americans three decades of overspending and under-saving to get into this pickle. As you may notice, consumer credit debt is $2.5 trillion and has barely budged downward. The pundits and economists predicting a strong economic recovery are blind to the truths of consumer debt. With actual unemployment exceeding 16.8%, 9 million people forced to work part-time wanting to work full-time, the work week at all time lows, and banks shutting down credit lines, consumers will be reducing or defaulting on their debt for years. With 70% of the economy dependent on consumer spending, there is absolutely no chance of a strong recovery. Household debt service payments as a percentage of disposable income reached a peak of 14.2% in 2007 and have plunged all the way to 13.5% today. Disposable income is plunging as people without jobs don’t have anything to dispose of.

A paradigm shift is occurring and the mainstream media, mainstream economists, and clueless politicians running this country do not understand the implications. Three decades of debt accumulation is not resolved in two years. It will take decades of reduced spending, paying down debt, and writing off debt. The Federal Reserve, banking cartel, and politicians are franticly attempting to make consumers borrow and spend with TARP, TALF, Cash for Clunkers, and numerous other debt increasing gimmicks. The consumer is tapped out. The median 401k balance in the U.S. is $26,000. Boomers realize they are 60 years old and have $50,000 of retirement savings and $30,000 of credit card debt. They are learning the brutal lesson of needs versus wants. The implications are disastrous for those dependent on a consumer spending society (i.e. retailers, restaurants, hotels, car makers, homebuilders).

There are 25% of households in the U.S. with no credit cards. Of those with a credit card, 30% pay off their balances each month. These are the people that have chosen to live within their means. They understand the difference between needs and wants. They appreciate the notion of delayed gratification. You buy things when you can afford them. You live a life of thrift and frugality, save for your family’s future, and live within the parameters of a budget. What a concept. The TARP accepting banks that control 87% of the credit card market are recording losses on an unprecedented scale. But no need to worry, the middle class tax payers come to the rescue again. Orwell must be rolling in his grave at the government originated Troubled Asset Relief Program. “Troubled” is an Orwellian word to describe debt that was knowingly issued by banks to people who would never pay it back in order to generate outrageous fees and bonuses for the executives issuing the debt. When the debt predictably went bad, “Relief” was provided to the criminal bankers on the backs of the taxpaying middle class. Bank of America, Wells Fargo and JP Morgan are bigger than they were before the financial crisis, their executives are still making millions, their “assets” are still “troubled”, and we continue to pay the bill, as will our children and grandchildren. Don’t worry. Ken Lewis, Vikram Pandit and Jamie Dimon’s grandchildren will inherit hundreds of millions of your tax dollars from their banker grandpas.

I Wanna Be Just Like A King

Beverly Hills… That’s where I want to be! (gimme, gimme)

Living in Beverly Hills… Beverly Hills… Rolling like a celebrity! (gimme, gimme)

Living in Beverly Hills…

Look at all those movie stars

They’re all so beautiful and clean When the housemaids scrub the floors

They get the spaces in between

I wanna live a life like that

I wanna be just like a king Take my picture by the pool

Cause I’m the next big thing Living in Beverly Hills – Weezer

The 8,000 square foot castle-like McMansions are the symbol of extravagance and excess that represent the worst of America’s hyper-consumerism culture. Even though the family unit has gotten smaller since 1970, the average home size has grown from 1,400 sq ft to 2,500 sq ft. McMansions are clearly not necessary due to family size. Essentially, it is another example of Boomers attempting to show the world they are successful. The bigger and gaudier the house the more flourishing you appear. This psychological need for approval combined with the big lie pushed by the National Association of Realtors that a house is always a great investment to generate the biggest housing bubble in history. One glance at Robert Shiller’s chart showing home prices versus population growth and CPI, proves beyond a shadow of a doubt that we have experienced a manic increase in house prices. It is also unambiguous that the downward spiral is not nearly complete. The housing cheerleaders continue to forecast a housing recovery that is still 5 years in the future.