The Wall Street shysters were scorning John Hussman in 2007 and 2001 when he was using historical tried and true measures of stock market valuation to warn people of a coming crash. He wasn’t heeded then and he won’t be heeded now. So it goes.

“Remember how these things unwound after 1929 (even before the add-on policy mistakes that created the Depression), 1972, 1987, 2000 and 2007 – all market peaks that uniquely shared the same extreme overvalued, overbought, overbullish syndromes that have been sustained even longer in the present half-cycle. These speculative episodes don’t unwind slowly once risk perceptions change. The shift in risk perceptions is often accompanied by deteriorating market internals and widening credit spreads slightly before the major indices are in full retreat, but not always.”

Yes, This is an Equity Bubble, Hussman Weekly Market Comment, July 2014

“Normally, market internals deteriorate in a way that provides more time to establish a defensive position – market breadth lags, divergences develop across various industries and security types, price/volume action shows signs of distribution and so forth. The overvalued, overbought, overbullish syndrome may present none of those warnings, particularly when there is even modest upward movement in Treasury yields.

“So while I recognize that my insistence on defensiveness may appear to be interminably stubborn and at odds with ‘obvious’ trends, it is precisely the apparent obviousness of those trends that contributes to my uneasiness. At the late 1972 – early 1973 peak market listed above, Barron’s annual investment ‘roundtable’ was accompanied by the title ‘Not a Bear Among Them.’ It’s notable that the latest roundtable just published by Barron’s reflects an identical uniformity of optimism.”

Hazardous Ovoboby! Hussman Weekly Market Comment, January 2007

“Abrupt market weakness is generally the result of low risk premiums being pressed higher. There need not be any collapse in earnings for a deep market decline to occur. The stock market dropped by half in 1973-74 even while S&P 500 earnings grew by over 50%. The 1987 crash was associated with no loss in earnings. Fundamentals don’t have to change overnight. There is in fact zero correlation between year-over-year changes in earnings and year-over-year changes in the S&P 500. Rather, low and expanding risk premiums are at the root of nearly every abrupt market loss. One of the best indications of the speculative willingness of investors is the ‘uniformity’ of positive market action across a broad range of internals. Probably the most important aspect of last week’s decline was the decisive negative shift in these measures.”

Market Internals Go Negative, Hussman Weekly Market Comment, July 2007

Here is what he is saying this week:

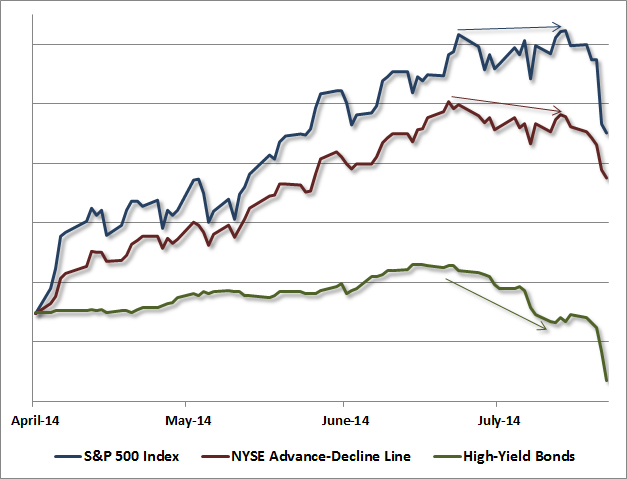

We don’t take any single divergence as serious in itself, but the accumulation of divergences in recent weeks should not be ignored. Notably, the majority of NYSE stocks are now below their respective 200-day moving averages (which again, isn’t serious in itself, but feeds into a larger syndrome of internal breakdowns in a market that remains strenuously overvalued).

The key point is this: after an extended and extreme compression of risk premiums, we’re now observing increasing divergences across a variety of market internals and security types (e.g. breadth, leadership, momentum stocks, small caps, junk bonds). We’ve come to avoid pointed warnings in this market, because speculative conditions have extended much longer than in other cycles.

Whatever the crowd wishes to do about it, historically-minded investors should think carefully about whether a strenuously overvalued market with deteriorating market internals is a desirable environment for risk taking. For our part, the answer is a resounding “No.”

Ignoring John Hussman’s warnings for the last two years has been beneficial to someone fully invested in the market. Faith in the Fed is at an all-time high and rigging the game has worked wonders for the muppet slayers. Are you feeling lucky? Then borrow on margin and buy some Twitter stock. It’s a can’t miss plan. I hear Amazon plans to double their losses next quarter by selling more shit for a loss. That should drive their stock price to $600.

Read the rest of John Hussman’s Weekly Letter

Hey, if Amazon goes to $600.00 just imagine how many people will BTFATH!!!!!!!!!!!!!!John

But it’s different now, isn’t it?

Last October I thought it would come crashing down when Bernanke was indicating the Fed would start tapering off QE. Then he did no such thing, and the markets came roaring back. People told me I was a fool.

This time the markets appear to be dipping dramatically, in a much bigger way than last october.

“Somebody told me wall street fell / But we were so poor that we couldn’t tell.”

It will be considered a major sign of the US decline.

Not the failing educational system. Not the declining physical and mental health of the populace. Not the falling take home pay for your average joe.

Nope, THIS will be touted as the leading indicator of the decline of US power. What a fucking joke.