Authored by Charles Hugh Smith via OfTwoMinds blog,

A world in which “we do these things because they’re easy” has one end-state: collapse.

On September 12, 1962, President John F. Kennedy gave a famous speech announcing the national goal of going to the moon by the end of the decade. ( JFK’s speech on going to the moon.) In a memorable line, Kennedy said we would pursue the many elements of the space program “not because they are easy, but because they are hard.”

Our national philosophy now is “we do these things because they’re easy”– and relying on debt to pay today’s expenses is at the top of the list. What’s easier than tapping a line of credit to buy whatever you want or need? Nothing’s easier than borrowing money, especially at super-low rates of interest.

We are now totally, completely dependent on expanding debt for the maintenance of our society and economy. Every sector of the economy–households, businesses and government–all borrow vast sums just to maintain the status quo for another year.

Compare buying a new car with easy, low-interest credit and saving up to buy the car with cash. How easy is it to borrow $23,000 for a new $24,000 car? You go to the dealership, announce all you have to put down is a trade-in vehicle worth $1,000. The salesperson puts a mirror under your nose to make sure you’re alive, makes sure you haven’t just declared bankruptcy to stiff previous lenders, and if you pass those two tests, you qualify for a 1% rate auto loan. You sign some papers and drive off in your new car. Easy-peasy!

Scrimping and saving to pay for the new car with cash is hard. You have to save $1,000 each and every month for two years to save up the $24,000, and the only way to do that is make some extra income by working longer hours, and sacrificing numerous pleasures–being a shopaholic, going out to eat frequently, $5 coffee drinks, jetting somewhere for a long weekend, etc.

The sacrifice and discipline required are hard. What’s the pay-off in avoiding debt? Not much–after all, the new auto loan payment is modest. If we take a 5-year or 7-year loan, it’s even less. By borrowing $23,000, we get to keep all our fun treats and spending pleasures, and we get the new car, too.

At the corporate level, it’s the same story: borrow a billion dollars and use it to buy back shares. Increasing the value of the corporation’s shares by increasing profit margins and actual value is hard; boosting the share price with borrowed money is easy.

It’s also the same story with politicians and the government: cutting anything is politically painful, so let’s just float a bond, i.e. borrow money to pay for what was once paid out of tax revenues: maintaining parks, repaving streets, funding pensions, etc.

This dependence on expanding debt for maintaining the status quo is a global trend. Debt is exploding in China in every sector, and the same is true in other nations, developed and developing alike.

Borrowing more money from the future is easy, painless and requires no trade-offs, sacrifices or accountability–until the debt-addicted economy collapses under its own weight of debt service and insolvency. People keep repeating various versions of the story that “debt doesn’t matter” because “future growth” will outgrow the skyrocketing debt, or inflation will make it all manageable, or that central banks will do whatever it takes to make sure everyone has enough money to service their debt burdens: negative interest rates, helicopter money, etc. etc. etc.

We want to believe in financial magic because we want things to remain easy. Borrowing from the future is easy, making sacrifices and being accountable is hard.

But eventually the cost of servicing even low interest-rate debt squeezes spending, eventually capital tires of chasing negative interest-rate bonds, eventually lenders realize that leverage has skyrocketed along with the debt and risk is piled up like dry tinder in a drought-weakened forest.

Central banks realize they can’t even limit the expansion of their balance sheets without triggering a panic that would collapse all the debt-based contraptions and manipulated markets they’ve held aloft with limitless liquidity.

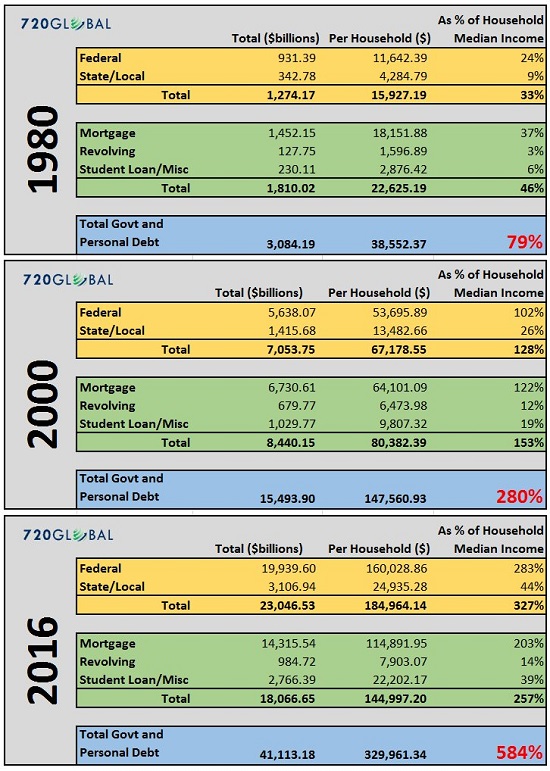

If you believe that going from a total debt burden (government and personal debt) per household being 79% of median household income to debt per household being 584% of median household income doesn’t matter and will have no consequences, you believe in magic. Unfortunately, thinking something will be easy forever and have no consequences is not the same as the real world of skyrocketing debt and leverage having no consequences.

A world in which “we do these things because they’re easy” has one end-state: collapse. Believing that debt has no consequence, that the status quo is permanent, that all the promises based on soaring debt can be paid–it’s all an appealing fantasy, magical thinking at its most enchanting. Believe these fantasies at your own risk.

Could’nt have said it better myself!! And while some debt is un-avoidable (house mortgage), the majority of debt, is for all intents and purposes for non essential things. Even governments are starting to realize that debt burdens are coming up against an impenetrable wall. I absolutely love smug fellow Canuckistan’s belief that we are OK and the debt problem is only south of the border. WRONG!!!

1.4 Trillion total debt on a working class of 15 million, equals disaster down the road and most of those are minimum wage jobs or on the government dole!

This won’t end well……….

A mortgage is only unavoidable because mortgage availability has driven the price of homes up to the point where paying cash for a house (from your own earned money, not inherited wealth or a windfall, like a lottery win) is not feasible on a middle class income.

My grandfather was just a CPA who never made more than $24k (he retired in 1988), but he never held a mortgage in his life.

Just like the availability of subsidized student loans drove the cost of college to the point where you can no longer go without getting loans, the same happened to housing when subsidized mortgages became universally used.

I thought I would be able to count on Big Injun Chief and Stucky during the coming storms .Big Injun Chief moved away and only God knows what happened to Stucky.I have been abandoned.

He is right about saving up to buy a new car.Try savings up to buy a Brand new commercial truck.It took me about two years to save up for the down payment(20,000 thousand )

All that debt is just somebody else’s “savings”, that was not spent.

The total economic product is always consumed in consumer goods or investment goods. In the same light, when a person saves, it gets lent out for someone to spend or it is invested.

The people who did not consume all of their personal product, but instead lent it out are the people who will take it on the chin since the won’t get equal value in goods/services bad.

It is like the Germans. They have a credit of a least 700 billion in Tier 2 balances at the ECB. All those Germans think they have something there, maybe for their retirement. All those other countries with negative Tier two balances will never be in a position to supply Germany with 700 billion in goods and services to make good on it When the Germans call on that money, the people who owe it will not be able to supply goods and services the Germans want.

Basically the Germans have donated all those Mercedes and BMWs. The Germans go to work everyday so they can make free cars for the rest of the world. They might was well write it off now, because it will never be paid off in the return of equal goods and services in the future either.

“All that debt is just somebody else’s “savings”, that was not spent.”

Most, if not all, of the credit (and hence debt) created since 2008, has been created by the central banking cartel, and unbacked by any savings. It is quite possible that there is no net savings left whatsoever. When the real savings pool is gone, it’s only a matter of time before the whole Ponzi comes down.

You can’t consume something you or someone else did not produce is really the main theme. If someone else consumes more than they produce, they are borrowing it from someone else who has a personal surplus. In theory if everyone consumed 100 % of their personal product there would be no debt. If someone consumes less than what they produced they can loan the difference it to someone else who will consume it. Goods and services are real things in limited quantities. You would be stupid to take on debt without consuming some sort of goods/service.

Yes the central banks print money, and there is a money multiplier in fraction reserve lending, but in the end only what is produced is consumed as consumption or as investment good. All those things do is distort the price of consuming someone else’s personal product. Someone had to not consume some portion of their personal product to lend that to someone else to go in debt and consume what the other did not consume.

It may seems strange to have a clip from Scrubs in a comment on this article, but it was actually, for a while at least, a fairly nuanced, well-balanced and genuinely funny show:

I believe.

The middle cannot hold forever. John

The comments on the video below (Catherine Austin Fitts) are certainly interesting and worth listening to, but it is just more of the same commentary about what to do about the situation that is going to cause our country/economy/system/insert term here…

Do I think living debt free is worthwhile? Yes.

Do I think the national debt can be repaid? No.

Do I think most Americans can repay their own debt? No.

Do I have a fucking clue when the shit really hits the fan? No.

https://www.youtube.com/watch?v=0TkYa34hEpk

+100 Maggie.

EDIT: Fucking WordPress logged me out! Anon is Indentured_Servant

“Scrimping and saving to pay for the new car with cash is hard.”

Not true. If you can manage to avoid debt and pay off any debt you do have it becomes very easy. Now I’ll admit that avoiding/paying off debt can be arduous but once done, saving becomes as easy as going to work, cashing your paycheck and not spending it.

“The sacrifice and discipline required are hard. What’s the pay-off in avoiding debt? Not much–after all,…”

The sacrifice and discipline may be hard but anything worthwhile usually involves sacrifice and discipline right?

What’s the pay-off in avoiding debt? The pay-off is huge and the author is too short sighted. For most, debt becomes a way of life…..a way of life that enslaves the borrower. Sure, a single 1% interest loan is no big deal but most have a single 1% car loan plus a 4% mortgage plus 5% student loans plus numerous 20% or higher interest credit cards and that makes them slaves.

The biggest payoff comes in YOU being in control of YOUR money. Being in debt means you are a slave that is required to send your paycheck to every Tom, Dick and Harry each month. For those of you currently in debt, quickly add up the total of your monthly debt payments in your head. Now imagine all that money going to your savings instead. See the difference? Being debt free is not easy but the hardship gives you discipline to discern between needs and wants. That hardship will cause you to value what you already have and make better spending decisions going forward.

Barring any inheritance or big lottery winnings your paycheck is the only tool you have to build wealth. If you’re busy spending it to service debt, no wealth will be built. If you’re busy avoiding debt and making smart spending decisions, wealth can easily be built.

It took my wife and I some time to have our own epiphany regarding debt but here it is: We are the ones who have to get out of our nice warm beds every day, go someplace we’d rather not go to do a bunch of stuff we’d rather not do with people we’d rather not be with. In other words: WORK. Since we HAVE to work then in our opinion we deserve a reward for doing so. Getting out of debt allows us to keep and manage the fruits of our labor. Being in debt does not.

Avoiding debt frees you in other ways too. Being in debt means that most slave away at jobs they hate in order to just keep their heads above water. Being debt free with a nice fat savings account frees you up to seek more rewarding jobs without the fear of losing your home, car etc.

Getting out of debt only requires a short period of extreme sacrifice that can be done by just about anyone. Step 1. Make a list of bare minimum NEEDS. This would be food, water, shelter, transportation (think hoopty instead of anything that requires payments) and a few others. Step 2. STOP spending on all wants. This would be dining out, that morning latte, vacations, car payments, electronics including cell phones, food beyond the basics and all that other crap that does not contribute DIRECTLY to keeping you alive or earning a paycheck. Step 3. Take EVERY spare penny not required for NEEDS and use it to pay down debt EVERY month. Step 4. Start selling all that crap that is cluttering up your house and garage that you bought with money you didn’t have and just sits around gathering dust. Again, this will include everything that does not DIRECTLY contribute to keeping you alive or employed. Another part of this step is to get a second job or generate a second income with every penny going to pay off debt. Also use all pay raises and bonuses to pay off debt. Step 5. Repeat steps two, three and four EVERY month until you are out of debt. Step 6. Avoid all future debt and build wealth by spending less than you earn.

For most people this will take between one and five years but the bigger the sacrifice, the quicker debt goes away. It my not be easy but it IS simple and very effective.

I never even considered the following until we were out of debt.

My wife makes less than one third of what I make each month. Being debt free means I could quit my job and we could get by on her pay check alone with money to spare.

FREEDOM can truly be spelled D-E-B-T-F-R-E-E.

Debt Free is the closest thing to genuine freedom we working stiffs in the industrialized world have 100% within our control.

Yep and the sacrifice it takes to become debt free will give birth to all manner of good things that are not readily apparent when considering whether to make the sacrifice.

I experienced numerous small epiphanies along the way but the one that truly amazed me was the change I witnessed in my wife one day when she declared that she preferred having a fat savings account to pissing money away on crap. This came after I delivered one of my infrequent State of the Household updates. She was blown away when she saw the benefits of the sacrifices we had made. Her mind began to reel at the possibilities and she was hooked on the mission after that.

Become debt free is like waiting for Collapse……it happens very slowly for a while then it happens all at once, the difference being that you win in the end!

In a nutshell it comes down to what your Mama always taught you….there is no free lunch and if it sounds too good to be true, it is too good to be true. Those basic life tenets have and always will be your best guidance for managing your money and your life in general.

Peaknic- excellent point.

My 28 year son is always concerned about his green foot print. Not the environmental kind. He has no debt and has saved $70K.