Huxley wrote that the only lesson of history is that we never heed the lessons of history. If you don’t think history matters anymore, don’t read Hussman’s commentary. If you think record level corporate profits will never fall (they are already falling) then don’t read the next two paragraphs.

We also observe the very regular tendency for profit margins to increase during economic expansions (presently corporate profits are close to 11% of GDP), and to contract during softer periods. Corporate profits as a share of GDP have always retreated to less than 5.5% in every economic cycle on record, even in recent decades.

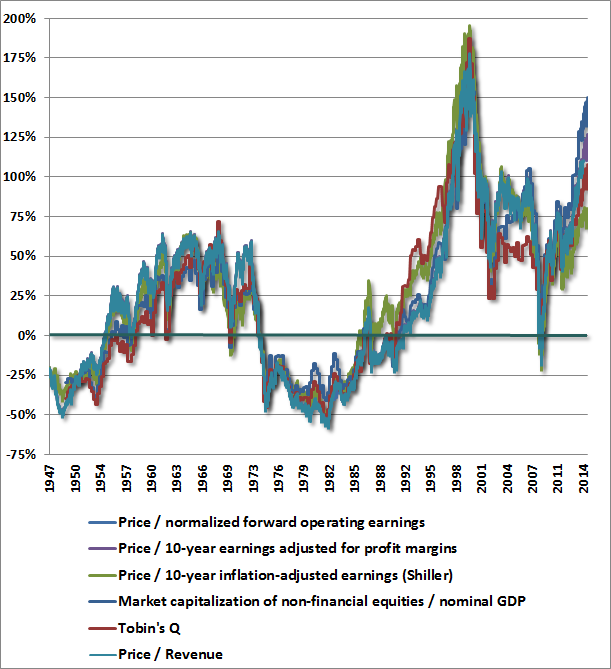

Our valuation concerns don’t rely on any requirement for earnings or profit margins to turn down in the near term. Valuations are a long-term proposition that link the price being paid today to a stream of cash flows that, for the S&P 500, have an effective duration of about 50 years. In evaluating whether “this time is different,” it should be understood that current valuations are “justified” only if 1) the wide historical cyclicality of profits over the economic cycle has been eliminated, 2) the average level of profit margins over the next five decades will be permanently elevated at nearly twice the historical norm, 3) the strong historical advantage of smoothed or margin-adjusted valuation measures over single-year price/earnings measures has vanished, and 4) zero interest rate policies will persist not just for 3 or 4 more years, but for decades while economic growth proceeds at historically normal rates nonetheless. Believe all of that if you wish. Without permanent changes in the way the world works, on valuation measures that are best correlated with actual subsequent market returns, stocks are wickedly overvalued here.

If you believe that six different valuation methods that have been valid for the last one hundred years in assessing stock market valuations are no longer valid then ignore the fact that today’s market is now 100% overvalued, and more overvalued than 1929, 1987, and 2007. History and facts no longer matter. Right?

While it’s easy to lose sight of the extremity of the present situation, these measures are well over 100% above their respective norms, on average. On the most reliable measures, we estimate that S&P 500 valuations are now only about 15-20% short of the 2000 extreme, and are clearly above every other extreme in history including 1901, 1929, 1937, 1972, 1987, and 2007.

If you believe central bankers have figured out how to permanently keep stock markets elevated through easy money and low interest rates, then ignore the fact the stock market will provide negative returns over the next 8 years. You will surely get out before the collapse because you’re smarter than the average schmuck. Right?

As of last week, based on a variety of methods, we estimate likely S&P 500 10-year nominal total returns averaging just 1.5% annually over the coming decade, with negative expected returns on every horizon shorter than about 8 years. In the current cycle, central banks have stuffed the ballot box. That doesn’t make long-term prospects any better, but it has induced substantial yield-seeking speculation for several years running.

What does all of this mean for the market at present? Since the initial “air-pocket” in stocks a few weeks ago, I’ve been careful to emphasize that I’ve had no opinion regarding near-term direction, and that we could observe either a corrective short-squeeze or a fresh market plunge. There was quite simply very little evidence that supported any directional view besides the expectation of continued volatility. Last week, however, the market re-established conditions extreme enough to place the present instance among what I’ve often called the “who’s who of awful times to invest.” Importantly, and in contrast to a few similarly extreme conditions we’ve seen in recent years, we presently observe both widening credit spreads and – at least for now – deteriorating internals and unfavorable trend uniformity on our measures of market action.

If you think John Hussman is just a perma-bear and his been discredited over the last five years, than leverage up and buy stocks. Amazon, Twitter, Go-Pro, and Alibaba are can’t miss opportunities of a lifetime. I hear Sears and JC Penney have turned the corner and will be rolling in profits over the next few years. It’s the best time to buy.

In short, our views will shift as the evidence shifts, but here and now, the market has re-established overvalued, overbought, overbullish conditions that mirror some of the most precarious points in the historical record such as 1929, 1937, 1974, 1987, 2000 and 2007. That syndrome is now coupled with continued evidence of a subtle shift toward more risk-averse investor psychology, primarily reflected by internal dispersion and widening credit spreads. I’ve often emphasized that the worst market outcomes have historically been associated with compressed risk premiums coupled with a shift toward risk aversion among investors. In those environments, risk premiums typically don’t normalize gradually – they do so in abrupt spikes. We’ll continue to respond as the evidence changes, but under current conditions, we view the investment environment for stocks as being among a handful of the most hostile points in history.

Read John Hussman’s Full Weekly Letter

Alibaba Closing In On 6th Largest Company In The US

Submitted by Tyler Durden on 11/10/2014 12:46 -0500

Alibaba is now the 6th largest company of all US-traded entities… and is the biggest non-US-domiciled corporation in the world (having added $80 billion in market cap in the last 3 weeks alone)

[img [/img]

[/img]

Just sitting with my bag of popcorn watching the show

Of course the bucket shop is overvalued when CEO’s use profits to buy back stocks.

KB, do you still refer to the fridge as ‘ice box’?

Avoid This Accident Waiting To Happen In Investment Markets

Submitted by Tim Price via Sovereign Man blog,

In 1975, Charles Ellis, the founder of Greenwich Associates, wrote one of the most powerful and memorable metaphors in the history of finance.

His essay is titled ‘The loser’s game’, which in his view is what the ‘sport’ of investing had become by the time he wrote it. His thesis runs as follows:

Whereas the game of tennis is won by professionals, the game of investing is ‘lost’ by professionals and amateurs alike.

Whereas professional sportspeople win their matches through natural talent honed by long practice, investors tend to lose (in relative, if not necessarily absolute terms) through unforced errors.

Success in investing, in other words, comes not from over-reach, in straining to make the winning shot, but simply through the avoidance of easy errors.

Ellis was making another point. As far back as the 1970s, investment managers were not beating the market; rather, the market was beating them.

This was a mathematical inevitability given the over-crowded nature of the institutional fund marketplace, the fact that every buyer requires a seller, and the impact of management fees on returns from an index.

Ben W. Heineman, Jr. and Stephen Davis of the Yale School of Management asked in their report of October 2011, ‘Are institutional investors part of the problem or part of the solution?’

By their analysis, in 1987, some 12 years after Ellis’ earlier piece, institutional investors accounted for the ownership of 46.6% of the top 1000 listed companies in the US. By 2009 that figure had risen to 73%.

That percentage is itself likely understated because it takes no account of the role of hedge funds.

Also by 2009 the US institutional landscape contained more than 700,000 pension funds; 8,600 mutual funds (almost all of which were not mutual funds in the strict sense of the term, but rather for-profit entities); 7,900 insurance companies; and 6,800 hedge funds.

Perhaps the most pernicious characteristic of active fund management is the tendency towards benchmarking (whether closet or overt).

Since a capitalisation benchmark assigns the heaviest weightings in a bond index to the largest bond markets by asset size, and since the largest bond markets by asset size represent the most heavily indebted issuers – whether sovereign or corporate – a bond-indexed manager is compelled to have the highest exposure to the most heavily indebted issuers.

All things equal, therefore, it is likely that the bond index-tracking manager is by definition heavily exposed to objectively poor quality (most heavily indebted) credits.

There is now a grave risk that an overzealous commitment to benchmarking is about to lead hundreds of billions of dollars of invested capital off a cliff.

Why? To begin with, trillions of dollars’ worth of equities and bonds now sport prices that can no longer be trusted in any way, having been roundly boosted, squeezed, coaxed and manipulated for the dubious ends of quantitative easing.

The most important characteristic of any investment is the price at which it is bought, which will ultimately determine whether that investment falls into the camp of ‘success’ or ‘failure’.

At some point, enough elephantine funds will come to appreciate that the assets they have been so blithely accumulating may end up being vulnerable to the last bid – or lack thereof – on an exchange.

When a sufficient number of elephants start charging inelegantly towards the door, not all of them will make it through unscathed.

Corporate bonds, in particular, thanks to heightened regulatory oversight, are not so much a wonderland of infinite liquidity, but an accident in the secondary market waiting to happen.

We recall words we last heard in the dark days of 2008: “When you’re a distressed seller of an illiquid asset in a market panic, it’s not even like being in a crowded theatre that’s on fire. It’s like being in a crowded theatre that’s on fire and the only way you can get out is by persuading somebody outside to swap places with you.”

The beatings will continue until morale improves – and until bondholders have been largely destroyed. When will the elephants start thinking about banking profits and shuffling nervously towards the door?

Meanwhile, central bankers continue to waltz effetely in the policy vacuum left by politicians.

As Paul Singer of Elliott Management recently wrote, we inhabit a world of “fake growth, fake money, fake jobs, fake stability, fake inflation numbers”.

Top down macro-economic analysis is all well and good, but in an investment world beset by such profound fakery, only bottom-up analysis can offer anything approaching tangible value.

In the words of one Asian fund manager, “The owner of a[n Asian] biscuit company doesn’t sit fretting about Portuguese debt but worries about selling more biscuits than the guy down the road.”

So there is hope of a sort for the survival of true capitalism, albeit from Asian biscuit makers. Perhaps even from the shares of biscuit makers in Europe – at the right price.