This elitist douchebag Ivy League asshole actually declares that there is no inflation and that Bernanke’s zero interest rate policy does not benefit the Wall Street banks while destroying the finances of senior citizens across the land. This is proof that ultra-liberals like Krugman and neo-con scum like Romney believe exactly the same thing. There are no differences among the ruling elite. They are circling the wagons as a small faction of critical thinking Americans reveal their cabal.

Krugman Rebutts (sic) Spitznagel, Says Bankers Are “The True Victims Of QE”, Princeton-Grade Hilarity Ensues

At first we were going to comment on this “response” by the high priest of Keynesian shamanic tautology to Mark Spitznagel’s latest WSJ opinion piece, but then we just started laughing, and kept on laughing, and kept on laughing…

As a reminder, on Thursday Universa’s Mark Spitznagel, best known recently for explaining in very vivid ways just how central planning has sown the seeds of its own destruction, wrote the following in the WSJ:

How the Fed Favors The 1%

The Fed doesn’t expand the money supply by dropping cash from helicopters. It does so through capital transfers to the largest banks.

A major issue in this year’s presidential campaign is the growing disparity between rich and poor, the 1% versus the 99%. While the president’s solutions differ from those of his likely Republican opponent, they both ignore a principal source of this growing disparity.

The source is not runaway entrepreneurial capitalism, which rewards those who best serve the consumer in product and price (Would we really want it any other way?) There is another force that has turned a natural divide into a chasm: the Federal Reserve. The relentless expansion of credit by the Fed creates artificial disparities based on political privilege and economic power.

David Hume, the 18th-century Scottish philosopher, pointed out that when money is inserted into the economy (from a government printing press or, as in Hume’s time, the importation of gold and silver), it is not distributed evenly but “confined to the coffers of a few persons, who immediately seek to employ it to advantage.”

In the 20th century, the economists of the Austrian school built upon this fact as their central monetary tenet. Ludwig von Mises and his students demonstrated how an increase in money supply is beneficial to those who get it first and is detrimental to those who get it last. Monetary inflation is a process, not a static effect. To think of it only in terms of aggregate price levels (which is all Fed Chairman Ben Bernanke seems capable of) is to ignore this pernicious process and the imbalance and economic dislocation that it creates.

As Mises protégé Murray Rothbard explained, monetary inflation is akin to counterfeiting, which necessitates that some benefit and others don’t. After all, if everyone counterfeited in proportion to their wealth, there would be no real economic benefit to anyone. Similarly, the expansion of credit is uneven in the economy, which results in wealth redistribution. To borrow a visual from another Mises student, Friedrich von Hayek, the Fed’s money creation does not flow evenly like water into a tank, but rather oozes like honey into a saucer, dolloping one area first and only then very slowly dribbling to the rest.

The Fed doesn’t expand the money supply by uniformly dropping cash from helicopters over the hapless masses. Rather, it directs capital transfers to the largest banks (whether by overpaying them for their financial assets or by lending to them on the cheap), minimizes their borrowing costs, and lowers their reserve requirements. All of these actions result in immediate handouts to the financial elite first, with the hope that they will subsequently unleash this fresh capital onto the unsuspecting markets, raising demand and prices wherever they do.

The Fed, having gone on an unprecedented credit expansion spree, has benefited the recipients who were first in line at the trough: banks (imagine borrowing for free and then buying up assets that you know the Fed is aggressively buying with you) and those favored entities and individuals deemed most creditworthy. Flush with capital, these recipients have proceeded to bid up the prices of assets and resources, while everyone else has watched their purchasing power decline.

At some point, of course, the honey flow stops—but not before much malinvestment. Such malinvestment is precisely what we saw in the historic 1990s equity and subsequent real-estate bubbles (and what we’re likely seeing again today in overheated credit and equity markets), culminating in painful liquidation.

The Fed is transferring immense wealth from the middle class to the most affluent, from the least privileged to the most privileged. This coercive redistribution has been a far more egregious source of disparity than the president’s presumption of tax unfairness (if there is anything unfair about approximately half of a population paying zero income taxes) or deregulation.

Pitting economic classes against each other is a divisive tactic that benefits no one. Yet if there is any upside, it is perhaps a closer examination of the true causes of the problem. Before we start down the path of arguing about the merits of redistributing wealth to benefit the many, why not first stop redistributing it to the most privileged?

And here is how Krugman, who among other pearls of insight references … Joe Wisenthal, responds. This is seriously Princeton-grade humor. We leave it up to readers to enjoy it for themselves unobstructed by our cynical interjections. Fom the NYT (highlights ours)

Plutocrats and Printing Presses

These past few years have been lean times in many respects — but they’ve been boom years for agonizingly dumb, pound-your-head-on-the-table economic fallacies. The latest fad — illustrated by this piece in today’s WSJ — is that expansionary monetary policy is a giveaway to banks and plutocrats generally. Indeed, that WSJ screed actually claims that the whole 1 versus 99 thing should really be about reining in or maybe abolishing the Fed. And unfortunately, some good people, like Daron Agemoglu and Simon Johnson, have bought into at least some version of this story.

What’s wrong with the idea that running the printing presses is a giveaway to plutocrats? Let me count the ways.

First, as Joe Wiesenthal and Mike Konczal both point out, the actual politics is utterly the reverse of what’s being claimed. Quantitative easing isn’t being imposed on an unwitting populace by financiers and rentiers; it’s being undertaken, to the extent that it is, over howls of protest from the financial industry. I mean, where are the editorials in the WSJ demanding that the Fed raise its inflation target?

Beyond that, let’s talk about the economics.

The naive (or deliberately misleading) version of Fed policy is the claim that Ben Bernanke is “giving money” to the banks. What it actually does, of course, is buy stuff, usually short-term government debt but nowadays sometimes other stuff. It’s not a gift.

To claim that it’s effectively a gift you have to claim that the prices the Fed is paying are artificially high, or equivalently that interest rates are being pushed artificially low. And you do in fact see assertions to that effect all the time. But if you think about it for even a minute, that claim is truly bizarre.

I mean, what is the un-artificial, or if you prefer, “natural” rate of interest? As it turns out, there is actually a standard definition of the natural rate of interest, coming from Wicksell, and it’s basically defined on a PPE basis (that’s for proof of the pudding is in the eating). Roughly, the natural rate of interest is the rate that would lead to stable inflation at more or less full employment.

And we have low inflation with high unemployment, strongly suggesting that the natural rate of interest is below current levels, and that the key problem is the zero lower bound which keeps us from getting there. Under these circumstances, expansionary Fed policy isn’t some kind of giveway to the banks, it’s just an effort to give the economy what it needs.

Furthermore, Fed efforts to do this probably tend on average to hurt, not help, bankers. Banks are largely in the business of borrowing short and lending long; anything that compresses the spread between short rates and long rates is likely to be bad for their profits. And the things the Fed is trying to do are in fact largely about compressing that spread, either by persuading investors that it will keep short rates at zero for a longer time or by going out and buying long-term assets. These are actions you would expect to make bankers angry, not happy — and that’s what has actually happened.

Finally, how is expansionary monetary policy supposed to hurt the 99 percent? Think of all the people living on fixed incomes, we’re told. But who are these people? I know the picture: retirees living on the interest on their bank account and their fixed pension check — and there are no doubt some people fitting that description. But there aren’t many of them.

The typical retired American these days relies largely on Social Security — which is indexed against inflation. He or she may get some interest income from bank deposits, but not much: ordinary Americans have fewer financial assets than the elite can easily imagine. And as for pensions: yes, some people have defined-benefit pension plans that aren’t indexed for inflation. But that’s a dwindling minority — and the effect of, say, 1 or 2 percent higher inflation isn’t going to be enormous even for this minority.

No, the real victims of expansionary monetary policies are the very people who the current mythology says are pushing these policies. And that, I guess, explains why we’re hearing the opposite. It’s George Orwell’s world, and we’re just living in it.

It… just… does…. not…. compute…. is this the type of thinking of needs to exhibit to get a Nobel?

Does Krugman seriously still not understand that NIM as a business model for banks died about the time banks stopped making loans and relying exclusively on prop, pardon flow, trading and using infinite rehypothecation leverage to juice their returns into the stratosphere, using the offbalance accounting permitted by shadow banking (really read this Paul – you may finally understand how finance DOES work these days), while doing all their best to limit origination and mortgage lending exposure, thank you Bank of Countrywide Lynch (i.e. the opposite of the NIM business model)?

Well at least Krugman is right about thing: there sure aren’t many people living on fixed income anymore. Most of them have already died. And he is most certainly not referring to the $5 billion on average in capital that is weekly rotated out of stocks and into bonds.

Whatever anyone does, do not point out our previous post that it was none other than the Fed warning that monetization and excess reserves could lead to hyperinflation. Or, that none other than JPMorgan pointed out a month ago that his beloved central planning has destroyed Okun’s Law which makes all Krugman Op-Eds in the past 4 years about the same intellectual quality as one-ply Cottonelle.

We may get a scene straight out of Scanners. And we don’t want that – we just want more Krugman humor and more LSAP, aka Large Scale Asshat Publications. In fact, it is time for the Fed to stop printing money and just print Krugman Op-Eds. Following the laughter-induced genocide, unemployment will indeed finally drop for once naturally, instead of as a result of millions of people dropping out of the labor force on a monthly basis.

Nobody ever talks about generational conflict. Who wants to bring up that the old are eating the young at the dinner table? How are you going to mention that to your boss? If you’re a politician, how are you going to tell your donors? Even the Occupy Wall Street crowd, while rejecting the modes and rhetoric and institutional support of Boomer progressives, shied away from articulating the fundamental distinction that fills their spaces with crowds: young against old.

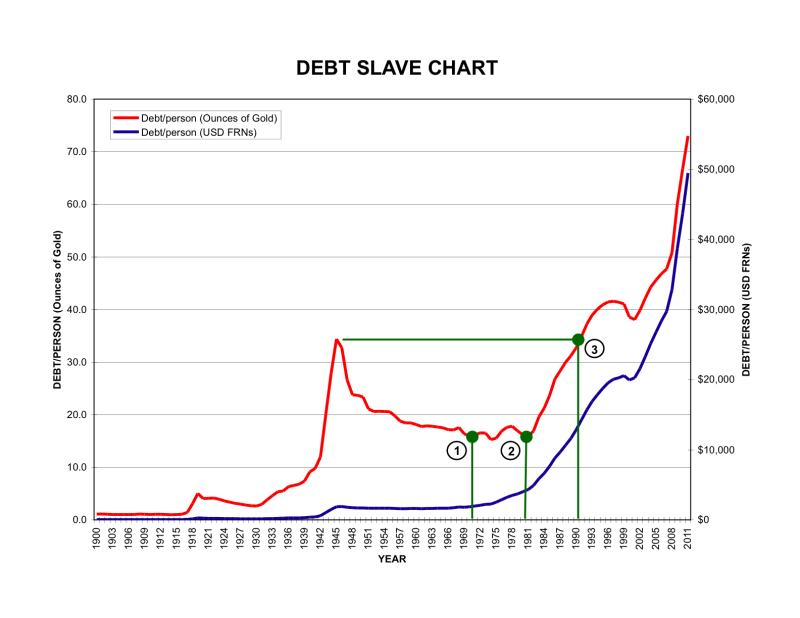

Nobody ever talks about generational conflict. Who wants to bring up that the old are eating the young at the dinner table? How are you going to mention that to your boss? If you’re a politician, how are you going to tell your donors? Even the Occupy Wall Street crowd, while rejecting the modes and rhetoric and institutional support of Boomer progressives, shied away from articulating the fundamental distinction that fills their spaces with crowds: young against old. Only 58 percent of Boomers have more than $25,000 put aside for retirement, so the rest will either starve or the government will have to pay for them. But the government’s future ability to pay is decreasing rapidly precisely because the Boomers splurged so heavily during the Bush and Clinton years. Public debt per person in the United States currently stands at $33,777. George W. Bush inherited a public-debt-to-GDP ratio of 32.5 percent and brought it up to 54.1 percent during a period of economic growth. (The money borrowed from the future paid for massive tax cuts, with no serious reductions in domestic spending, two expensive wars, and a prescription-drug benefit added to Medicare.) Under Obama, the debt-to-GDP ratio has risen to 67.7 percent and is projected to rise to 74.2 percent this year.

Only 58 percent of Boomers have more than $25,000 put aside for retirement, so the rest will either starve or the government will have to pay for them. But the government’s future ability to pay is decreasing rapidly precisely because the Boomers splurged so heavily during the Bush and Clinton years. Public debt per person in the United States currently stands at $33,777. George W. Bush inherited a public-debt-to-GDP ratio of 32.5 percent and brought it up to 54.1 percent during a period of economic growth. (The money borrowed from the future paid for massive tax cuts, with no serious reductions in domestic spending, two expensive wars, and a prescription-drug benefit added to Medicare.) Under Obama, the debt-to-GDP ratio has risen to 67.7 percent and is projected to rise to 74.2 percent this year.

![[ken+lay+i+els+bush]](https://1.bp.blogspot.com/_XyZ8CYMrrFg/ShxdAK9e_XI/AAAAAAAAAhI/nsvDQbZXqLE/s1600/ken%2Blay%2Bi%2Bels%2Bbush)