Guest Post by Dmitry Orlov

|

| Kelly Hensing |

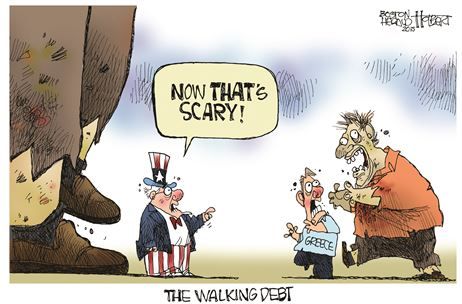

“Those whom the gods wish to destroy they first make mad” goes a quote wrongly attributed to Euripides. It seems to describe the current state of affairs with regard to the unfolding Greek imbroglio. It is a Greek tragedy all right: we have the various Eurocrats—elected, unelected, and soon-to-be-unelected—stumbling about the stage spewing forth fanciful nonsense, and we have the choir of the Greek electorate loudly announcing to the world what fanciful nonsense this is by means of a referendum.

As most of you probably know, Greece is saddled with more debt than it can possibly hope to ever repay. Documents recently released by the International Monetary Fund conceded this point. A lot of this bad debt was incurred in order to pay back German and French banks for previous bad debt. The debt was bad to begin with, because it was made based on very faulty projections of Greece’s potential for economic growth. The lenders behaved irresponsibly in offering the loans in the first place, and they deserve to lose their money.

However, Greece’s creditors refuse to consider declaring all of this bad debt null and void—not because of anything having to do with Greece, which is small enough to be forgiven much of its bad debt without causing major damage, but because of Spain, Italy and others, which, if similarly forgiven, would blow up the finances of the entire European Union. Thus, it is rather obvious that Greece is being punished to keep other countries in line. Collective punishment of a country—in the form of extracting payments for onerous debt incurred under false pretenses—is bad enough; but collective punishment of one country to have it serve as a warning to others is beyond the pale.

Janet Yellen levels her rate-hike gaze at us …

Janet Yellen levels her rate-hike gaze at us …

Medellín – city of the future

Medellín – city of the future

{kind=link}