“The risk of catastrophe will be very high. The nation could erupt into insurrection or civil violence, crack up geographically, or succumb to authoritarian rule. If there is a war, it is likely to be one of maximum risk and effort – in other words, a total war. Every Fourth Turning has registered an upward ratchet in the technology of destruction, and in mankind’s willingness to use it.” – Strauss & Howe – The Fourth Turning

“In the need to develop a capacity to know what potential enemies are doing, the United States government has perfected a technological capability that enables us to monitor the messages that go through the air. Now, that is necessary and important to the United States as we look abroad at enemies or potential enemies. We must know, at the same time, that capability at any time could be turned around on the American people, and no American would have any privacy left such is the capability to monitor everything—telephone conversations, telegrams, it doesn’t matter. There would be no place to hide.

If this government ever became a tyrant, if a dictator ever took charge in this country, the technological capacity that the intelligence community has given the government could enable it to impose total tyranny, and there would be no way to fight back because the most careful effort to combine together in resistance to the government, no matter how privately it was done, is within the reach of the government to know. Such is the capability of this technology.

I don’t want to see this country ever go across the bridge. I know the capacity that is there to make tyranny total in America, and we must see to it that this agency and all agencies that possess this technology operate within the law and under proper supervision so that we never cross over that abyss. That is the abyss from which there is no return.” – Frank Church on Meet the Press regarding the NSA – 1975

Ever since Edward Snowden burst onto the worldwide stage in June 2013, I’ve been wondering how he fits into the fabric of this ongoing Fourth Turning. This period of Crisis that arrives like clockwork, 60 to 70 years after the end of the previous Fourth Turning (Civil War – 66 years after American Revolution, Great Depression/World War II – 64 years after Civil War, Global Financial Crisis – 62 years after World War II), arrived in September 2008 with the Federal Reserve created collapse of the global financial system. We are now five and a half years into this Fourth Turning, with its climax not likely until the late-2020’s. At this point in previous Fourth Turnings a regeneracy had unified sides in their cause and a grey champion or champions (Ben Franklin/Samuel Adams, Lincoln/Davis, FDR) had stepped forward to lead. Thus far, no one from the Prophet generation has been able to unify the nation and create a sense of common civic purpose. Societal trust continues to implode, as faith in political, financial, corporate, and religious institutions spirals downward. There is no sign of a unifying regeneracy on the horizon.

The core elements of this Fourth Turning continue to propel this Crisis: debt, civic decay, global disorder. Central bankers, politicians, and government bureaucrats have been able to fashion the illusion of recovery and return to normalcy, but their “solutions” are nothing more than smoke and mirrors exacerbating the next bloodier violent stage of this Fourth Turning. The emergencies will become increasingly dire, triggering unforeseen reactions and unintended consequences. The civic fabric of our society will be torn asunder.

In retrospect, the spark might seem as ominous as a financial crash, as ordinary as a national election, or as trivial as a Tea Party. The catalyst will unfold according to a basic Crisis dynamic that underlies all of these scenarios: An initial spark will trigger a chain reaction of unyielding responses and further emergencies. The core elements of these scenarios (debt, civic decay, global disorder) will matter more than the details, which the catalyst will juxtapose and connect in some unknowable way. If foreign societies are also entering a Fourth Turning, this could accelerate the chain reaction. At home and abroad, these events will reflect the tearing of the civic fabric at points of extreme vulnerability – problem areas where America will have neglected, denied, or delayed needed action.” – The Fourth Turning – Strauss & Howe

Debt

The core crisis element of debt is far worse than it was at the outset of this Crisis in September 2008. The National Debt has risen from $9.7 trillion to $17.5 trillion, an 80% increase in five and half years. It took 215 years for the country to accumulate as much debt as it has accumulated since the start of this Crisis. We continue to add $2.8 billion a day to the National debt, and the president declares it is time for this austerity to end. The total unfunded liabilities of the Federal government for Social Security, Medicare, Medicaid, government pensions and now Obamacare exceeds $200 trillion and is mathematically impossible to honor. Corporate debt stands at an all-time high. Margin debt is at record levels, as faith in the Federal Reserve’s ability to levitate the stock market borders on delusional. Consumer debt has reached new heights, as the government doles out subprime auto loans to deadbeats and subprime student loans to future University of Phoenix Einsteins. Global debt has surged by 40% since 2008 to over $100 trillion, as central bankers have attempted to cure a disease caused by debt with more debt.

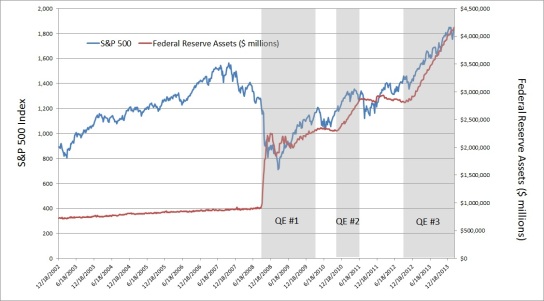

All of this debt accumulation is compliments of Bernanke/Yellen and the Federal Reserve, who have produced this new debt bubble with their zero interest rate policy and quantitative easing that has driven their balance sheet from $935 billion of mostly Treasury bonds in September 2008 to $4.2 trillion of toxic mortgage garbage acquired from their owners – the insolvent Too Big To Trust Wall Street banks. This entire house of cards is reliant upon permanently low interest rates, the faith of foreigners in our lies, and trust in Ivy League educated economists captured by Wall Street. This debt laden house of cards sits atop hundreds of trillions of derivatives of mass destruction used by the Wall Street casinos to generate “riskless” profits. When, not if, a trigger ignites this explosive concoction of debt, the collapse will be epic and the violent phase of this Fourth Turning will commence.

Civic Decay

The core crisis element of civic decay is evident everywhere you turn. Our failed public educational system is responsible for much of the civic decay, as a highly educated critical thinking populace is our only defense against a small cabal of bankers and billionaires acquiring unwarranted influence and control over our country. Our children have been taught how to feel and to believe government propaganda. The atrocious educational system is not a mistake. It has been designed and manipulated by your owners to produce the results they desire, as explained bluntly by George Carlin.

“There’s a reason that education sucks, and it’s the same reason it will never ever ever be fixed. It’s never going to get any better, don’t look for it. Be happy with what you’ve got. Because the owners of this country don’t want that. I’m talking about the real owners now, the big, wealthy, business interests that control all things and make the big decisions. They spend billions of dollars every year lobbying to get what they want. Well, we know what they want; they want more for themselves and less for everybody else. But I’ll tell you what they don’t want—they don’t want a population of citizens capable of critical thinking. They don’t want well informed, well educated people capable of critical thinking. They’re not interested in that. That doesn’t help them. That’s against their interest.”

The urban ghettos become more dangerous and uninhabitable by the day. The inner cities are crumbling under the weight of welfare spending and declining tax revenues. The very welfare policies begun fifty years ago to alleviate poverty have hopelessly enslaved the poor and ignorant in permanent squalor and destitution. The four decade old drug war has done nothing to reduce the use of drugs. It has benefited the corporate prison industry, as millions have been thrown into prison for minor drug offenses. Meanwhile, millions more have been legally addicted to drugs peddled by the corporate healthcare complex. The culture warriors and advocates of new rights for every special interest group continue their never ending battles which receive an inordinate amount of publicity from the corporate media. Class warfare is simmering and being inflamed by politicians pushing their particular agendas. Violence provoked by race and religion is growing by the day. The fault lines are visible and the imminent financial earthquake will push distress levels beyond the breaking point. Once the EBT cards stop working, all hell will break loose. Three days of panic will empty grocery store shelves and the National Guard will be called out to try and restore control.

Global Disorder

The core crisis element of global disorder is evident everywhere you turn. The false flag revolution in the Ukraine, initiated by the U.S. and EU in order to blunt Russia’s control of natural gas to Europe, has the potential to erupt into a full blown shooting war at any moment. The attempt by Saudi Arabia, Israel and the U.S. to overthrow the Syrian dictator in order to run a natural gas pipeline across their land into Europe was blunted by Russia. Iraq is roiled in a civil war, after the U.S. invaded, occupied and destabilized the country. After 12 years of occupation, Afghanistan is more dysfunctional and dangerous than it was before the U.S. saved them from the evil Taliban. Unrest, violent protests, and brutal measures by rulers continue in Egypt, Turkey, Thailand, Venezuela, Bahrain, Brazil, and throughout Africa. American predator drones roam the skies of the world murdering suspected terrorists. The European Union is insolvent, with Greece, Spain, Italy and Portugal propped up with newly created debt. Austerity for the people and prosperity for the bankers is creating tremendous distress and tension across the continent. A global volcanic eruption is in the offing.

It is clear to me the American Empire is in terminal decline. Hubris, delusion, corruption, foolish disregard for future generations and endless foreign follies have set in motion a chain of events that will lead to a cascading sequence of debt defaults, mass poverty, collapsing financial markets, and hyperinflation or deflation, depending on the actions of feckless bankers and politicians. There is no avoiding the tragic outcome brought on by decades of bad choices and a century of allowing private banking interests to control our currency. The “emergency” QE and ZIRP responses by the Federal Reserve to the Federal Reserve created 2008 financial collapse continue, even though the propaganda peddled by the Deep State tries to convince the public we have fully recovered. This grand fraud cannot go on forever. Ponzi schemes no longer work once you run out of dupes. With societal trust levels approaching all-time lows and foreign countries beginning to understand they are the dupes, another global financial crisis is a lock.

The Snowden Factor

With ten to fifteen years likely remaining in this Fourth Turning Crisis, people familiar with generational turnings can’t help but ponder what will happen next. Linear thinkers, who constitute the majority, mistakenly believe things will magically return to normal and we’ll continue our never ending forward human progress. Their ignorance of history and generational turnings that recur like the four seasons will bite them in the ass. We are being flung forward across the vast chaos of time and our existing social order will be transformed beyond recognition into something far better or far worse. The actual events over the coming decade are unknowable in advance, but the mood and reactions of the generational archetypes to these events are predictable. The actions of individuals will matter during this Fourth Turning. The majority are trapped in their propaganda induced, techno distracted stupor of willful ignorance. It will take a minority of liberty minded individuals, who honor the principles of the U.S. Constitution and are willing to sacrifice their lives, to prevail in the coming struggle.

Despite fog engulfing the path of future events, we know they will be propelled by debt, civic decay, and global disorder. Finding a unifying grey champion figure seems unlikely at this point. I believe the revelations by Edward Snowden have set the course for future events during this Fourth Turning. The choices of private citizens, like Snowden, Assange, and Manning, have made a difference. The choices we all make over the next ten years will make a difference. A battle for the soul of this country is underway. The Deep State is firmly ingrained, controlling the financial, political and educational systems, while using their vast wealth to perpetuate endless war, and domination of the media to manipulate the masses with propaganda and triviality. They are powerful and malevolent. They will not relinquish their supremacy and wealth willingly.

Snowden has revealed the evil intent of the ruling class and their willingness to trash the Constitution in their psychopathic pursuit of mammon. The mass surveillance of the entire population, locking down of an entire city in pursuit of two teenagers, military training exercises in major metropolitan areas, militarization of local police forces by DHS, crushing peaceful demonstrations with brute force, attempting to restrict and confiscate guns, molesting innocent airline passengers, executive orders utilized on a regular basis by the president, and treating all citizens like suspects has set the stage for the coming conflict. Strauss & Howe warned that history has shown armed conflict is always a major ingredient during a Fourth Turning.

“History offers even more sobering warnings: Armed confrontation usually occurs around the climax of Crisis. If there is confrontation, it is likely to lead to war. This could be any kind of war – class war, sectional war, war against global anarchists or terrorists, or superpower war. If there is war, it is likely to culminate in total war, fought until the losing side has been rendered nil – its will broken, territory taken, and leaders captured.” – The Fourth Turning – Strauss & Howe -1997

It appears to me the Deep State is preparing for armed conflict with the people. Why else would they be utilizing Big Brother methods of surveillance, militarization of police forces and Gestapo like tactics of intimidation to control the masses? This doesn’t happen in a democratic republic where private individuals are supposed to know everything done by public government servants, not vice versa. They know the cheap, easy to access energy resources are essentially depleted. They know the system they have built upon a foundation of cheap energy and cheap debt is unsustainable and will crash in the near future. They know their fiat currency scheme is failing.They know it is going to come crashing down.

They know America and the world will plunge into an era of depression, violence, and war. They also know they want to retain their wealth, power and control. There is no possibility the existing establishment can be purged through the ballot box. It’s a one party Big Brother system that provides the illusion of choice to the Proles. Like it or not, the only way this country can cast off the shackles of the banking, corporate, fascist elites, and the government surveillance state is through an armed revolution. The alternative is to allow an authoritarian regime, on par with Hitler, Stalin and Mao, to rise from the ashes of our financial collapse. This is a distinct possibility, given the ignorance and helplessness of most Americans after decades of government education and propaganda.

The average mentally asleep American cannot conceive of armed conflict within the borders of the U.S. War, violence and dead bodies are something they see on their 52 inch HDTVs while gobbling chicken wings and cheetos in their Barcalounger. We’ve allowed a banking cartel and their central bank puppets to warp and deform our financial system into a hideous façade, sold to the masses as free market capitalism. We’ve allowed corporate interests to capture our political system through bribery and corruption.

We’ve allowed the rise of a surveillance state that has stripped us of our privacy, freedom, liberty and individuality in a futile pursuit of safety and security. We’ve allowed a military industrial complex to exercise undue influence in Washington DC, leading to endless undeclared wars designed to enrich the arms makers. We’ve allowed the corporate media and the government education complex to use propaganda, misinformation and social engineering techniques to dumb down the masses and make them compliant consumers. These delusions will be shattered when our financial and economic system no longer functions. The end is approaching rapidly and very few see it coming.

Glory or Ruin?

The scenario I envision is a collapse of our debt saturated financial system, with a domino effect of corporate, personal, and governmental defaults, exacerbated by the trillions of currency, interest rate, and stock derivatives. Global stock markets will crash. Trillions in paper wealth will evaporate into thin air. The Greater Depression will gain a choke-hold around the world. Mass bankruptcies, unemployment and poverty will sweep across the land. The social safety net will tear under the weight of un-payable entitlements. Riots and unrest will breakout in urban areas. Armed citizens in rural areas will begin to assemble in small units. The police and National Guard will be unable to regain control. The military will be called on to suppress any and all resistance to the Federal government. This act of war will spur further resistance from liberty minded armed patriots. The new American Revolution will have begun. Leaders will arise in the name of freedom. Regional and local bands of fighters will use guerilla tactics to defeat a slow top heavy military dependent upon technology and vast quantities of oil. A dictatorial regime may assume power on a Federal level. A breakup of the nation into regional states is a distinct possibility.

With the American Empire crumbling from within, our international influence will wane. With China also in the midst of a Fourth Turning, their debt bubble will burst and social unrest will explode into civil war. Global disorder, wars, terrorism, and financial collapse will lead to a dramatic decrease in oil production, further sinking the world into depression. The tensions caused by worldwide recession will lead to the rise of authoritarian regimes and global warfare. With “advances” in technological warfare and the proliferation of nuclear warheads, this scenario has the potential to end life on earth as we know it. The modern world could be set back into the stone-age with the push of a button. There are no guarantees of a happy ending for humanity.

The outcome of this Fourth Turning is dependent upon the actions of a minority of critical thinking Americans who decide to act. No one can avoid the trials and tribulations that lie ahead. We will be faced with immense challenges. Courage and sacrifice will be required in large doses. Elders will need to lead and millennials will need to carry a heavy load, doing most of the dying. The very survival of our society hangs in the balance. Edward Snowden has provided an example of the sacrifice required during this Fourth Turning. How we respond and the choices we make over the next decade will determine whether this Fourth Turning will result in glory or ruin for our nation.

“Eventually, all of America’s lesser problems will combine into one giant problem. The very survival of the society will feel at stake, as leaders lead and people follow. The emergent society may be something better, a nation that sustains its Framers’ visions with a robust new pride. Or it may be something unspeakably worse. The Fourth Turning will be a time of glory or ruin.” – Strauss & Howe – The Fourth Turning

Click these links to read the first two parts of this three part series:

Do No Evil Google – Censor & Snitch for the State

Google, China, the NSA and the Fourth Turning