On January 8 of this year I posted my annual prediction article for this year – 2012 – The Year of Living Dangerously. Now it’s time to assess my complete and utter cluelessness when it comes to predicting things within a given time frame. Despite the fact that myself and everyone else acting like they know what lays ahead are proven wrong time and time again, we continue to make predictions about the future. It makes us feel like we have some control, when we don’t. The world is too complex, too big, too corrupt, too lost in theories and delusions, and too dependent upon too many leaders with too few brains to be able to predict what will happen next. This is the time of year when all the “experts” will be making their 2013 predictions. I haven’t seen too many of these experts going back and honestly assessing their 2012 predictions, which didn’t happen.

What I’ve learned is that “experts” usually have an agenda. Their predictions are designed to convince you to buy the stocks they recommend or purchase their newsletter. Many of these “experts” work for Wall Street, the corporate MSM, a political party or corporate interest. Half of the “experts” represent the status quo and want the masses to think everything is just fine and will steadily improve. The other half are fear mongers that want to scare you into buying their products with predictions of impending collapse at any moment. I like to read the predictions of a wide variety of pundits, bloggers, and so called journalists, while understanding they probably have an agenda.

Personally, I try to make my predictions based on the facts I observe and try to gather. My agenda is to prepare my family for whatever these facts tell me is likely to happen. My website is just a place for me to post my thoughts. I don’t depend upon it for a living and I have nothing to sell. That doesn’t mean that my biases, hopes, and desires do not color my predictions. As I reread my article yesterday, I found myself thinking, “when is this long winded gasbag going to actually make some predictions?” My article was supposed to make 2012 predictions but ended up trying to tie 2012 into the Fourth Turning Crisis paradigm. When I eventually got to the predictions, I realized that a monkey throwing darts could have done just as well. If I was one of those “experts”, I’d say that I wasn’t wrong, I was just early. Of course, that is a cop-out. Being early is the same as being wrong.

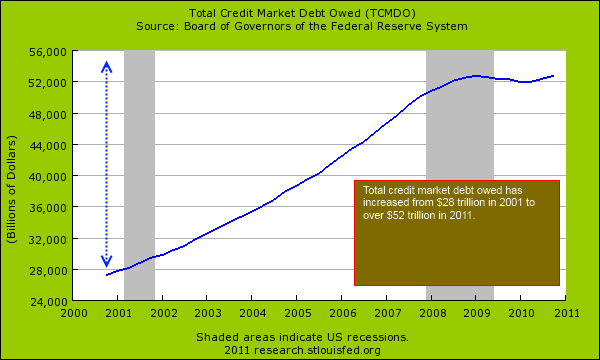

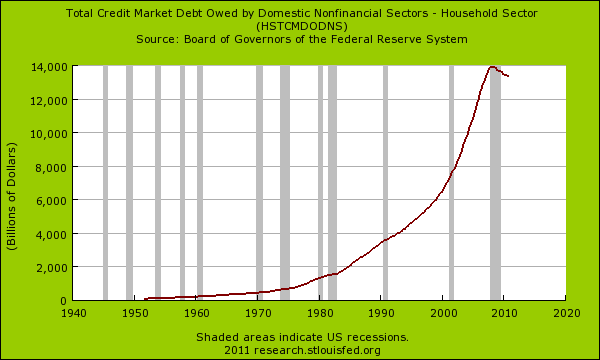

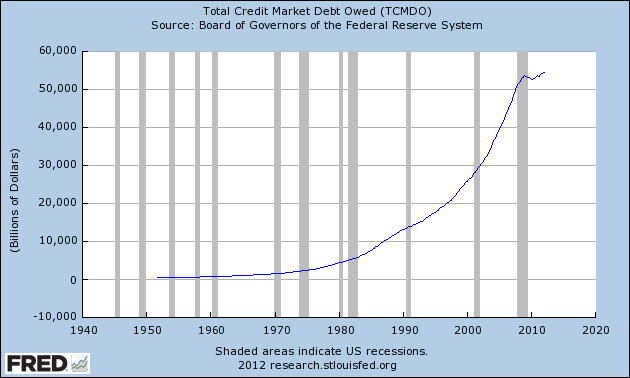

I’m more interested in why I was wrong. It seems I always underestimate the ability of sociopathic central bankers and their willingness to destroy the lives of hundreds of millions to benefit their oligarch masters. I always underestimate the rampant corruption that permeates Washington DC and the executive suites in mega-corporations across the land. And I always overestimate the intelligence, civic mindedness, and ability to understand math of the ignorant masses that pass for citizens in this country. It seems that issuing trillions of new debt to pay off trillions of bad debt, government sanctioned accounting fraud, mainstream media propaganda, government data manipulation and a populace blinded by mass delusion can stave off the inevitable consequences of an unsustainable economic system. But enough excuses. Let’s see how wrong I was:

- All the episodes which will occur in 2012 will have at their core one of the three elements described by Strauss & Howe in 1997: Debt, Civic Decay, or Global Disorder.

This was a generic prediction. Those are a lot easier to take credit for as being right. Considering the country is about to go over the fiscal cliff, I’d say that debt has had a major impact in 2012. The disgusting political campaign, the anger over efforts to ban guns, urban violence, 20% of nation on food stamps, and real unemployment rate of 23% certainly prove that civic decay is accelerating. Uprisings in Egypt, Syria and across the Middle East intensified. Israel and Iran got closer to inevitable war. Japan and China are on the verge of conflict. The U.S. is still bogged down in Afghanistan and has failed miserably in efforts to democratize the Middle East. I’d say we have had a bit of global disorder.

- At best, the excessive levels of sovereign debt will slow economic growth to zero or below in 2012. At worst, interest rates will soar as counties attempt to rollover their debt and rolling defaults across Europe will plunge the continent into a depression.

The best case scenario for European bankers and politicians came to pass in 2012. The GDP for the European Union went negative in the 3rd quarter of 2012. The southern European nations are experiencing depression level conditions with soaring unemployment, social unrest, and higher interest rates. But even Germany is experiencing a dramatic slowdown. The bankers continue to call the shots, with various debt schemes designed to keep the bankers whole, while throwing the people to the wolves. They have postponed the day of reckoning, but it is coming. They do not have a liquidity problem. They have a solvency problem. You cannot resolve a debt problem by creating more debt.

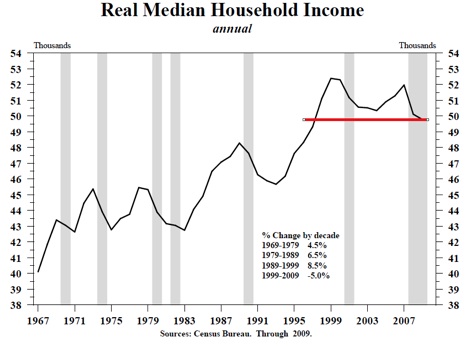

- The truth that no one wants to acknowledge is the standard of living for every person in Europe, the United States and Japan will decline. The choice is whether the decline happens rapidly by accepting debt default and restructuring or methodically through central bank created inflation that devours the wealth of the middle class. Debt default would result in rich bankers losing vast sums of wealth and politicians accepting the consequences of their phony promises. Bankers and politicians will choose inflation.

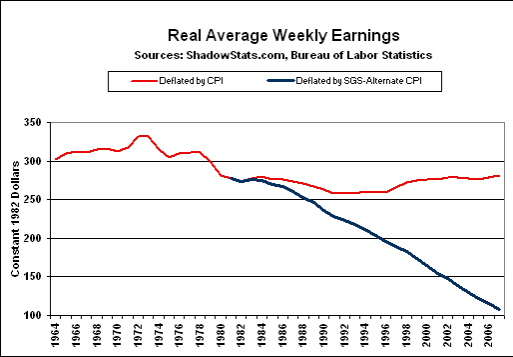

This was an easy one. Bankers and politicians will never choose pain for themselves when they can shift it to the people. Bernanke and the rest of the world’s central bankers, in cooperation with their captured politicians, have chosen to inflate the debt away by printing money. They trust in the shallowness and ignorance of the masses to not notice as their standard of living steadily declines.

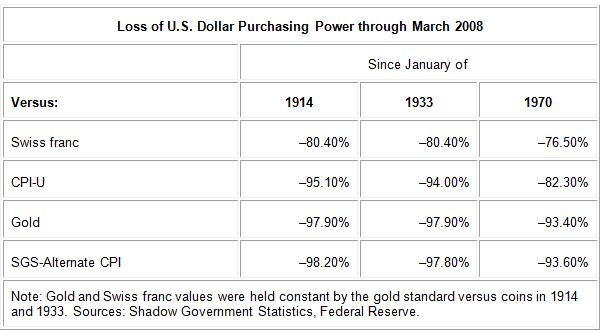

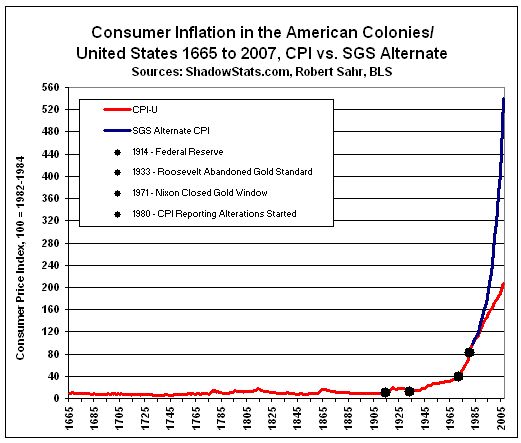

Controlling the distribution of data allows the oligarchs to falsify the true level of inflation and the corporate MSM dutifully spews the propaganda to the masses.

- The European Union will not survive 2012 in its current form. Countries are already preparing for the dissolution. Politicians and bankers will lie and print until the day they pull the plug on the doomed Euro experiment.

I was 100% wrong in this assessment. The politicians and bankers are most certainly lying, but they have succeeded in keeping the EU intact. The dissolution would imperil too many bankers. Whether they can keep it intact through 2013 is another question.

- The National Debt will be $16.5 trillion when the next president takes office in January 2013.

Barack Obama will be inaugurated on January 20, 2013. As of December 26, 2012 the National Debt stood at $16.34 trillion and according to Turbo Tax Timmy will hit the debt limit of $16.4 trillion on December 31. He will use accounting gimmicks and not fund government pensions to not exceed the limit, but the debt will continue to accumulate at a rate of $3.5 billion per day. The National Debt will be at approximately $16.47 trillion when Obama starts his 2nd term. Close enough for government work.

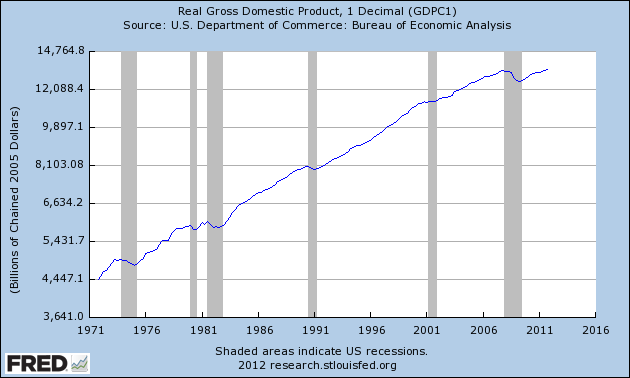

- As debt servicing grows by the day, the economy losses steam. The excessive and increasing debt levels will lead to a renewed recession in 2012.

Despite the fact that the government and corporate media continue to report economic growth and a barely positive GDP, a recession did begin this past summer. Using a true level of inflation, GDP has been negative since 2006.

The horrific Christmas retail sales and declining corporate profits reveal the truth. Fourth quarter GDP will be negative and the government will eventually adjust the prior quarters lower. Excel spreadsheet models, fake inflation figures and seasonal adjustments cannot deny reality or the facts.

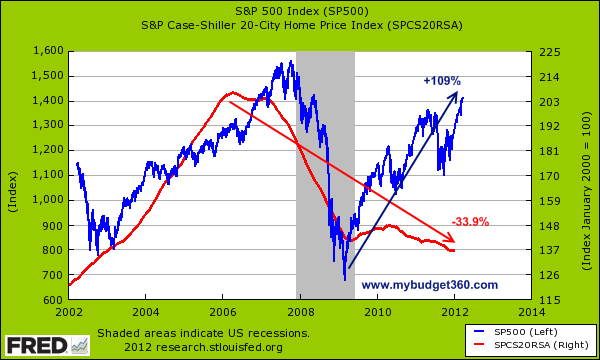

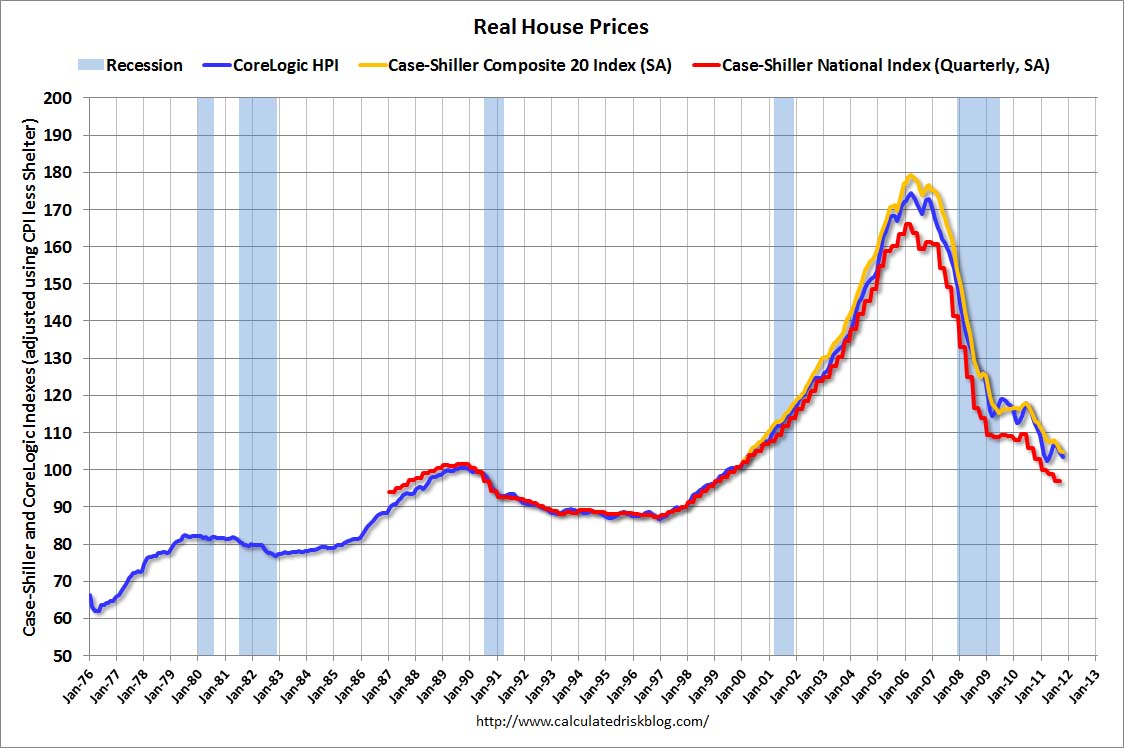

- As foreclosures rise a self-reinforcing loop will develop. Home prices will fall as banks dump houses at lower prices, pushing millions more into a negative equity position. Home prices will fall another 5% to 10% in 2012, with a couple years to go before bottoming.

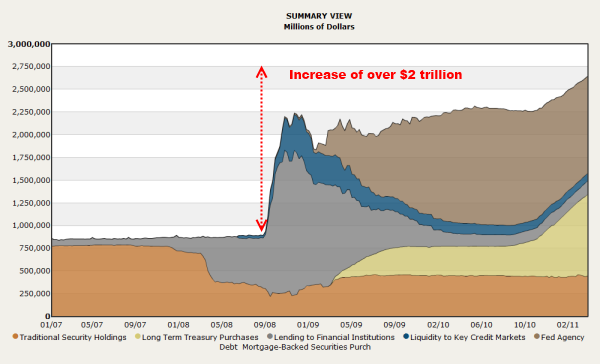

Another 100% wrong prediction. I again underestimated the willingness of corrupt Wall Street bankers, in cahoots with the Federal government, to fraudulently boost home prices by withholding foreclosures from the market and creating a fake housing shortage. The Feds have willingly used Fannie, Freddie and the FHA to guarantee more bad mortgage loans and put the taxpayer further on the hook for the billions of bad debt. Bennie has swooped in and bought up billions of toxic mortgage debt from the criminal Wall Street banks, while driving mortgage rates to record low levels. With this massive intervention, they have managed to increase home prices by 4% and increase home sales to levels 60% below the peak. Job well done.

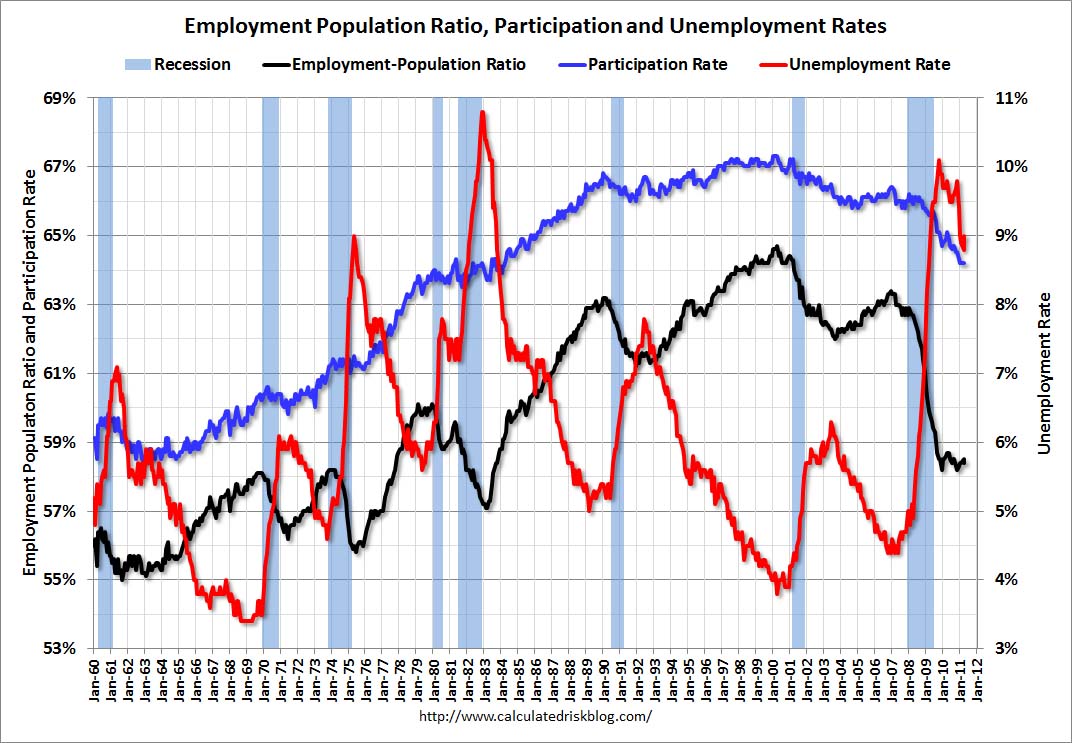

- The working age population will increase by 1.7 million, the number of people employed will go up by 1 million, but the official unemployment rate will drop to 7% as the BLS reveals that 10 million people decided to relax and leave the workforce. Surely I jest. The government manipulated unemployment rate will rise above 9%, while the real rate will surpass 25%.

I made what I thought was an outrageous prediction as an attempt at humor, but my outrageous prediction was closer to the truth. The working age population has grown by 3.7 million people, the number of employed people has gone up by only 2.7 million, 2.4 million people decided to kick back and leave the workforce, resulting in the unemployment rate “plunging” from 8.7% to 7.7%.

Measuring unemployment on par with the method used during the 1930s would put the level at 23% today. But you should trust the BLS. Why would they lie?

- Ben Bernanke, Wall Street shysters and Barack Obama want you to be drawn in by the allure of short-term gains based on hopes of QE3. The stock market will be volatile in 2012 with stocks falling 20% when it becomes evident the country is going back into recession. Ben will try to ride to the rescue with QE3 as he buys up more toxic mortgage debt. Wall Street will do their usual touchdown dance celebration, but the bloom will fall off this rose fast, as quantitative easing has proven to be a failure in stimulating economic growth.Gridlock in Washington D.C., chaotic national conventions, and the implosion of Europe will contribute to the market finishing down by at least 15% for the year.

I hope you didn’t follow my stock market advice as it looks like I missed by only 25% or 30% with this prediction. It is amazing what zero interest rates for Wall Street banks, QE to infinity, high frequency trading supercomputers, and fake Wall Street earnings can do for a stock market. Since the recession has not been acknowledged and rigged corporate profits still sit near their peak, the stock market has continued to rise. I applaud the oligarchs for their ability to extract every last dime from the pockets of the middle class in their avaricious plundering of America. Bernie Madoff is proudly admiring their work from his prison cell.

- The average price of oil will exceed $100 during 2012 resulting in the highest average gas price in history for American drivers. These high prices, along with various weather related issues will keep food prices elevated, with 5% or higher increases likely. This should spur a few more peasant revolutions around the globe.

I nailed this prediction. Americans paid the highest average price for a gallon of gasoline in history during 2012. Agricultural commodities like corn, wheat and soybeans soared by 7% to 20%, as the high oil prices and drought drove food prices higher. Meat prices will rise in 2013 as herds had to be thinned in 2012 because of the high feed costs. But don’t worry. The BLS will just adjust the food inflation away as they assume you switch from hamburger to cat food.

- Gold will finish the year higher. As always, it will be volatile and manipulated by the powers that be. A drop below $1,500 in the beginning of the year is possible, but when Ben announces QE3, it will be off to the races. I expect gold to reach $1,900 by year end. Silver will be more volatile, but will likely reach $40 by year end.

Gold will finish the year higher for the twelfth consecutive year. It was volatile, with a high of $1,796 and a low of $1,527. It will finish the year in the mid $1,600s. Silver was equally volatile, but also up for the year. It ranged between $37.50 and $26. It will finish the year in the $30 range. The powers that be know that rising gold and silver prices reveal their deceitful inflationary master plan, so they use all of their market manipulative powers to suppress the prices of these metals. The higher our debt, the higher their prices will go. When the confidence game is revealed to be a Ponzi scheme, the prices of gold and silver will be unleashed.

- Old line mall based retailers like Sears and J.C. Penney die a slow agonizing death as they stagger into the sunset like Montgomery Ward, Circuit City and thousands before them.

I was wrong about JC Penney. They are dying a fast agonizing death as the idiot savant from Apple has driven them straight into the ground, with sales plunging by 26% versus last year. It isn’t a matter of if, but when this employer of 159,000 declares bankruptcy. The “brilliant” (Jim Cramer says so) Eddie Lampert has Sears on a glide path to liquidation. This Christmas season will reveal these CEOs to be frauds.

- The Occupy Movement will become more extreme with more disruptions of the economic system with less warning so the authorities don’t have time to prepare. I expect more cyber hacking into Wall Street, government, and media computer networks, causing disarray and uncertainty regarding financial information. I expect the Democratic and Republican presidential conventions to be overrun by protestors. The authorities will respond with excessive force, resulting in further violent protests in other cities.

Another 100% miss. The Occupy Movement splintered and petered out after being brutally dismantled by the armed mercenaries of the status quo. There were some cyber-attacks, but they caused minimal disruption. The masses are satiated with their techno-gadgets and reality TV shows. No one protested. No one cared.

- The Federal government grows ever more panicked by the knowledge that its Ponzi scheme economy is going to collapse. This is why passage of the NDAA and the future passage of SOPA are so important to them. Imprisonment of citizens without charge and shutting down the only remaining means of truth – the Internet – are essential to retaining their power and control over the masses. At the same time, gun sales are at record levels. Critical thinking Americans can see the writing on the wall and no longer trust corrupt politicians of either party. Arming yourself and buying physical gold and silver is a prudent act in today’s world.

The outrage over SOPA, led by the alternative online media, stopped it from being passed. The tyrants continue their efforts to suppress free speech on the internet, as Facebook shuts down pages that do not conform to the corporate fascist government agenda. Gun sales are off the charts, as critical thinking people no longer trust the corrupt government. Physical gold and silver sales are soaring as critical thinking people no longer trust our corrupt economic system.

- The ruling elite hand selected puppets for the 2012 presidential election are Obama and Romney. They are virtually interchangeable and both are acceptable to the Wall Street oligarchs. The monkey wrench in the gears is Ron Paul. He will run as a 3rd Party candidate and focus a light on the crony capitalism that passes for free markets in America today. He will be vilified by both parties and their media mouthpieces, but if he gains traction I fear an unfortunate accident will befall him. Either way, he will have a dramatic impact on the debate and the outcome of the 2012 election.

With this prediction I allowed my hope to overcome reason. The oligarchs are too powerful. Ron Paul’s grassroots campaign made the oligarchs extremely uncomfortable. He drew huge crowds of young people on college campuses across the country. His message of liberty and freedom resonated with millions, but he was no match for the billionaires that call the shots in this country. He was silenced by the Republican establishment and chose not to run as a 3rd party candidate. The puppet on the left won the election. The puppet on the right retreated to one of his six mansions. Ron Paul rode off into the sunset knowing he gave it his best shot.

- It seems more likely by the day that someone will do something stupid in or around Iran and the Persian Gulf will explode into a virtual hell on earth. The unintended consequences of such a development will far outweigh the intended consequences. The revolutions, protests, and brewing civil wars in Egypt, Syria, Libya and Iraq will flare up even if Iran doesn’t explode into a shooting war. The tensions in the Middle East will keep oil prices above $100, despite a world plunging into recession.

The showdown between Israel and Iran did not happen in 2012, despite increasingly angry rhetoric. The stealth war with Iran began, as economic sanctions and cyber warfare have begun to destroy their economy and impoverish their people. Revolutions, riots, protests and civil war spread across the Middle East throughout 2012 resulting in high oil prices and a worldwide economic contraction which is picking up speed as 2012 comes to a conclusion.

- China’s hard landing will arrive in 2012. Keynesianism on steroids has failed as they’ve built more than enough vacant malls, vacant cities, vacant condo towers, and bridges to nowhere. Property prices will plunge, exports will decline, and peasants will revolt as food and energy prices push them over the edge.

China has come in for a hard landing. With a government more corrupt than even ours, their reported economic data would make a BLS drone blush with pride. Property prices are falling. Exports are falling. But somehow they report economic growth of 7%. And the MSM dutifully reports this gibberish as truth. Unrest and protests are a daily occurrence in China, but they are immediately crushed. The Chinese authorities continue to clamp down on the internet and media. China’s economic system is a rotting Keynesian nightmare.

I also raised the generic possibilities of earthquakes, hurricanes, pandemics and terrorist attacks. I noted that a terrorist attack in a public venue might cause a government over-reaction. Even though the slaughter of young school children by a deranged mental defective doesn’t constitute a terrorist attack, the reaction by government officials and their liberal control freak allies in the mainstream media are exactly what I feared. Every tragedy is used to gain more control over our lives and take away our Constitutional rights in the name of safety and security. The ignorant masses willingly give up their freedom and liberty, believing their Orwellian government protectors will look out for them. As we enter 2013, time grows shorter. The power hungry psychopaths continue to pillage and plunder. Our unsustainable economic system struggles under the weight of debt, despair and delusion as the endgame approaches. The willfully ignorant populace is lost in their techno-narcissistic dream world.

Will 2013 be the year it all collapses in a flaming heap of rubble? I don’t know. Maybe you should ask an “expert”.

It guarantees to be an interesting year. I’ll be hiring Bonzo the chimp to help me make my 2013 predictions in the next week or so.