See more freaks at People of Wal-Mart

Vote on which set of pictures is creepier and more disturbing.

The movie “Men in Tights” was hilarious but I feel like “Men in Thongs” is going to be more of a tragedy than a comedy…or now that I think about it, perhaps it’s both.

Let’s play “Can you find the real baby?” Don’t let that little guy going to town fool you!

I’m sure our pals over at Mugshotrow.com will get a kick out of this lady that asked the police if she could just get one more fix in before she was booked for shoplifting at Wal-mart. Hey, say what you want about Wal-mart shoppers but at least you know they are honest. Check out the story below.

A 33-year-old Minnesota woman stopped for shoplifting Monday night at a West Side Walmart found herself in bigger trouble after she asked arresting police officers if she could do some heroin, police said.

Edith Hancock, of the 3000 block of Riverwood Drive in Hastings, Minn., was charged with felony possession of a controlled substance and misdemeanor retail theft, police said.

Hancock, who told police she was three months pregnant, was seen going into a changing room at the Walmart at 4650 W. North Ave. with a pair of jeans, leggings, and a black shirt and then leave the changing area wearing those items, according to police.

After taking some cosmetics and placing them in her purse, she tried to leave the store without paying and was stopped by security, according to police. Chicago police were called and she was taken to the Grand Central District station where she was arrested at 7 p.m., according to police.

While she was being processed, she “continually asked” officers for “just one blow,” a street name for heroin, from her purse because she was “getting dopesick,” according to a police report.

Officers found multiple bags of heroin in her purse, and she continued saying that she “only wanted one” of the bags “because she had ten of them and she thought they might be more than a gram although a couple were very light because she had already used from a least a couple,” the report said.

Hancock was released on a signature bond during a hearing today before Judge Donald Panarese at the Leighton Criminal Court building. She is scheduled to appear in court next on Feb. 18.

Until I find out about my appeal, just click the link to get your Saturday dose of gross.

http://www.peopleofwalmart.com/photos/

“I was part of that strange race of people aptly described as spending their lives doing things they detest, to make money they don’t want, to buy things they don’t need, to impress people they don’t like.” ― Emile Gauvreau

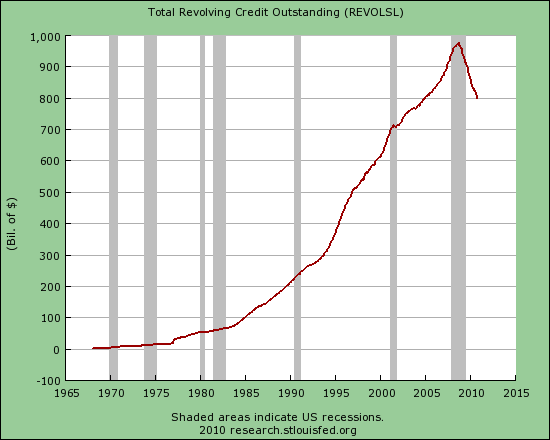

If ever a chart provided unequivocal proof the economic recovery storyline is a fraud, the one below is the smoking gun. November and December retail sales account for 20% to 40% of annual retail sales for most retailers. The number of visits to retail stores has plummeted by 50% since 2010. Please note this was during a supposed economic recovery. Also note consumer spending accounts for 70% of GDP. Also note credit card debt outstanding is 7% lower than its level in 2010 and 16% below its peak in 2008. Retailers like J.C. Penney, Best Buy, Sears, Radio Shack and Barnes & Noble continue to report appalling sales and profit results, along with listings of store closings. Even the heavyweights like Wal-Mart and Target continue to report negative comp store sales. How can the government and mainstream media be reporting an economic recovery when the industry that accounts for 70% of GDP is in free fall? The answer is that 99% of America has not had an economic recovery. Only Bernanke’s 1% owner class have benefited from his QE/ZIRP induced stock market levitation.

The entire economic recovery storyline is a sham built upon easy money funneled by the Fed to the Too Big To Trust Wall Street banks so they can use their HFT supercomputers to drive the stock market higher, buy up the millions of homes they foreclosed upon to artificially drive up home prices, and generate profits through rigging commodity, currency, and bond markets, while reducing loan loss reserves because they are free to value their toxic assets at anything they please – compliments of the spineless nerds at the FASB. GDP has been artificially propped up by the Federal government through the magic of EBT cards, SSDI for the depressed and downtrodden, never ending extensions of unemployment benefits, billions in student loans to University of Phoenix prodigies, and subprime auto loans to deadbeats from the Government Motors financing arm – Ally Financial (85% owned by you the taxpayer). The country is being kept afloat on an ocean of debt and delusional belief in the power of central bankers to steer this ship through a sea of icebergs just below the surface.

The absolute collapse in retail visitor counts is the warning siren that this country is about to collide with the reality Americans have run out of time, money, jobs, and illusions. The most amazingly delusional aspect to the chart above is retailers continued to add 44 million square feet in 2013 to the almost 15 billion existing square feet of retail space in the U.S. That is approximately 47 square feet of retail space for every person in America. Retail CEOs are not the brightest bulbs in the sale bin, as exhibited by the CEO of Target and his gross malfeasance in protecting his customers’ personal financial information. Of course, the 44 million square feet added in 2013 is down 85% from the annual increases from 2000 through 2008. The exponential growth model, built upon a never ending flow of consumer credit and an endless supply of cheap fuel, has reached its limit of growth. The titans of Wall Street and their puppets in Washington D.C. have wrung every drop of faux wealth from the dying middle class. There are nothing left but withering carcasses and bleached bones.

The impact of this retail death spiral will be vast and far reaching. A few factoids will help you understand the coming calamity:

The collapse in foot traffic to the 109,500 shopping centers that crisscross our suburban sprawl paradise of plenty is irreversible. No amount of marketing propaganda, 50% off sales, or hot new iGadgets is going to spur a dramatic turnaround. Quarter after quarter there will be more announcements of store closings. Macys just announced the closing of 5 stores and firing of 2,500 retail workers. JC Penney just announced the closing of 33 stores and firing of 2,000 retail workers. Announcements are imminent from Sears, Radio Shack and a slew of other retailers who are beginning to see the writing on the wall. The vacancy rate will be rising in strip malls, power malls and regional malls, with the largest growing sector being ghost malls. Before long it will appear that SPACE AVAILABLE is the fastest growing retailer in America.

The reason this death spiral cannot be reversed is simply a matter of arithmetic and demographics. While arrogant hubristic retail CEOs of public big box mega-retailers added 2.7 billion retail square feet to our already over saturated market, real median household income flat lined. The advancement in retail spending was attributable solely to the $1.1 trillion increase (68%) in consumer debt and the trillion dollars of home equity extracted from castles in the sky, that later crashed down to earth. Once the Wall Street created fraud collapsed and the waves of delusion subsided, retailers have been revealed to be swimming naked. Their relentless expansion, based on exponential growth, cannibalized itself, new store construction ground to a halt, sales and profits have declined, and the inevitable closing of thousands of stores has begun. With real median household income 8% lower than it was in 2008, the collapse in retail traffic is a rational reaction by the impoverished 99%. Americans are using their credit cards to pay their real estate taxes, income taxes, and monthly utilities, since their income is lower, and their living expenses rise relentlessly, thanks to Bernanke and his Fed created inflation.

The media mouthpieces for the establishment gloss over the fact average gasoline prices in 2013 were the second highest in history. The highest average price was in 2012 and the 3rd highest average price was in 2011. These prices are 150% higher than prices in the early 2000’s. This might not matter to the likes of Jamie Dimon and Jon Corzine, but for a middle class family with two parents working and making 7.5% less than they made in 2000, it has a dramatic impact on discretionary income. The fact oil prices have risen from $25 per barrel in 2003 to $100 per barrel today has not only impacted gas prices, but utility costs, food costs, and the price of any product that needs to be transported to your local Wally World. The outrageous rise in tuition prices has been aided and abetted by the Federal government and their doling out of loans so diploma mills like the University of Phoenix can bilk clueless dupes into thinking they are on their way to an exciting new career, while leaving them jobless in their parents’ basement with a loan payment for life.

The laughable jobs recovery touted by Obama, his sycophantic minions, paid off economist shills, and the discredited corporate legacy media can be viewed appropriately in the following two charts, that reveal the false storyline being peddled to the techno-narcissistic iGadget distracted masses. There are 247 million working age Americans between the ages of 18 and 64. Only 145 million of these people are employed. Of these employed, 19 million are working part-time and 9 million are self- employed. Another 20 million are employed by the government, producing nothing and being sustained by the few remaining producers with their tax dollars. The labor participation rate is the lowest it has been since women entered the workforce in large numbers during the 1980’s. We are back to levels seen during the booming Carter years. Those peddling the drivel about retiring Baby Boomers causing the decline in the labor participation rate are either math challenged or willfully ignorant because they are being paid to be so. Once you turn 65 you are no longer counted in the work force. The percentage of those over 55 in the workforce has risen dramatically to an all-time high, as the Me Generation never saved for retirement or saw their retirement savings obliterated in the Wall Street created 2008 financial implosion.

To understand the absolute idiocy of retail CEOs across the land one must parse the employment data back to 2000. In the year 2000 the working age population of the U.S. was 213 million and 136.9 million of them were working, a record level of 64.4% of the population. There were 70 million working age Americans not in the labor force. Fourteen years later the number of working age Americans is 247 million and only 144.6 million are working. The working age population has risen by 16% and the number of employed has risen by only 5.6%. That’s quite a success story. Of course, even though median household income is 7.5% lower than it was in 2000, the government expects you to believe that 22 million Americans voluntarily left the labor force because they no longer needed a job. While the number of employed grew by 5.6% over fourteen years, the number of people who left the workforce grew by 31.1%. Over this same time frame the mega-retailers that dominate the landscape added almost 3 billion square feet of selling space, a 25% increase. A critical thinking individual might wonder how this could possibly end well for the retail genius CEOs in glistening corporate office towers from coast to coast.

This entire materialistic orgy of consumerism has been sustained solely with debt peddled by the Wall Street banking syndicate. The average American consumer met their Waterloo in 2008. Bernanke’s mission was to save bankers, billionaires and politicians. It was not to save the working middle class. You’ve been sacrificed at the altar of the .1%. The 0% interest rates were for Jamie Dimon and Lloyd Blankfein. Your credit card interest rate remained between 13% and 21%. So, while you struggle to pay bills with your declining real income, the Wall Street bankers are again generating record profits and paying themselves record bonuses. Profits are so good, they can afford to pay tens of billions in fines for their criminal acts, and still be left with billions to divvy up among their non-prosecuted criminal executives.

Bernanke and his financial elite owners have been able to rig the markets to give the appearance of normalcy, but they cannot rig the demographic time bomb that will cause the death and destruction of our illusory retail paradigm. Demographics cannot be manipulated or altered by the government or mass media. The best they can do is ignore or lie about the facts. The life cycle of a human being is utterly predictable, along with their habits across time. Those under 25 years old have very little income, therefore they have very little spending. Once a job is attained and income levels rise, spending rises along with the increased income. As the person enters old age their income declines and spending on stuff declines rapidly. The media may be ignoring the fact that annual expenditures drop by 40% for those over 65 years old from the peak spending years of 45 to 54, but it doesn’t change the fact. They also cannot change the fact that 10,000 Americans will turn 65 every day for the next sixteen years. They also can’t change the fact the average Baby Boomer has less than $50,000 saved for retirement and is up to their grey eye brows in debt.

With over 15% of all 25 to 34 year olds living in their parents’ basement and those under 25 saddled with billions in student loan debt, the traditional increase in income and spending is DOA for the millennial generation. The hardest hit demographic on the job front during the 2008 through 2014 ongoing recession has been the 45 to 54 year olds in their peak earning and spending years. Combine these demographic developments and you’ve got a perfect storm for over-built retailers and their egotistical CEOs.

The media continues to peddle the storyline of on-line sales saving the ancient bricks and mortar retailers. Again, the talking head pundits are willfully ignoring basic math. On-line sales account for 6% of total retail sales. If a dying behemoth like JC Penney announces a 20% decline in same store sales and a 20% increase in on-line sales, their total change is still negative 17.6%. And they are still left with 1,100 decaying stores, 100,000 employees, lease payments, debt payments, maintenance costs, utility costs, inventory costs, and pension costs. Their future is so bright they gotta wear a toe tag.

The decades of mal-investment in retail stores was enabled by Greenspan, Bernanke, and their Federal Reserve brethren. Their easy money policies enabled Americans to live far beyond their true means through credit card debt, auto debt, mortgage debt, and home equity debt. This false illusion of wealth and foolish spending led mega-retailers to ignore facts and spread like locusts across the suburban countryside. The debt fueled orgy has run out of steam. All that is left is the largest mountain of debt in human history, a gutted and debt laden former middle class, and thousands of empty stores in future decaying ghost malls haunting the highways and byways of suburbia.

The implications of this long and winding road to ruin are far reaching. Store closings so far have only been a ripple compared to the tsunami coming to right size the industry for a future of declining spending. Over the next five to ten years, tens of thousands of stores will be shuttered. Companies like JC Penney, Sears and Radio Shack will go bankrupt and become historical footnotes. Considering retail employment is lower today than it was in 2002 before the massive retail expansion, the future will see in excess of 1 million retail workers lose their jobs. Bernanke and the Feds have allowed real estate mall owners to roll over non-performing loans and pretend they are generating enough rental income to cover their loan obligations. As more stores go dark, this little game of extend and pretend will come to an end. Real estate developers will be going belly-up and the banking sector will be taking huge losses again. I’m sure the remaining taxpayers will gladly bailout Wall Street again. The facts are not debatable. They can be ignored by the politicians, Ivy League economists, media talking heads, and the willfully ignorant masses, but they do not cease to exist.

“Facts do not cease to exist because they are ignored.” – Aldous Huxley

Is there a FUPA season? I mean, if I had to guess I’d say the springtime due to excess winter weight being gained unnoticed but I kinda have a bad “gut” feeling that we can’t limit these atrocities to just one time of year.

What’s the point of having underwear on if the world doesn’t even know you’re wearing them? These fine ladies are forward thinkers I say. I’m tired of spending my good money on some stylish undies only for them to go unnoticed. Who’s with me?!?!…nobody? Ok, nevermind then.

Attention shoppers, we have a special on parties located in every frickin’ aisle this dude goes in!!!!!

HA! Ok, when you come down from your incredible level of disbelief and disgust in humanity let me know which one you think is worse.

That will certainly deter anyone thinking about breaking into your car. I know I wouldn’t go near it now just because I’d assume you also have a bear trap on the seat cushion or something. Maybe our friends over at whitetrashrepairs.com could help let us know where this security system ranks in their books.

What’s so creepy about having a homemade shirt with multiple pictures of Winona Ryder on it? Oh, everything? Yeah that’s what I figured. Not stalkerish at all.

Who doesn’t like a classic Battle of the Sexes matchup? For this bout we’ve got a couple of over-the-top mooners. So make sure you pick a side before you hurriedly look away.

I’m sure by now you’ve all heard about 49ers coach Jim Harbaugh and how his wife hates that he buys his pleated khakis for $8 at Walmart. Obviously the reason you’ve heard about that is because Sportscenter is less about sports and more about useless crap. However, we here at POWM are all about useless crap that happens at Walmart, so we’d like to say thanks to Jim for getting caught in the act and remember $8 khakis are still 1,000X better than Belichick’s awful cutoff hoodies.

Nothing says “I’m cheap as hell” like homemade bumper stickers! Also, if you need to resort to making homemade bumper stickers about people being on your ass so much, chances are good the problem is you.

Someone asked me if there is anything better than a rat tail and to be honest I was stumped. I assumed there was not. Then BOOM! Right in my face I get hit with the Siamese twin rat tail and it turns everything I thought I knew about this world upside down.

Ummm ok, couple of ladies on the prowl that might have just missed their prime hunting season by a few decades. But perhaps these cougars still got some bite left? Anyway, I’m sure there are such things as a GILF, not sure these two fit the bill but I don’t know what else to call them when I make you pick one.

Okay, yup I see it’s suppose to be ‘Ducks’ but that’s a little too close for comfort for the kiddos. However ma’am, you don’t get to use that excuse. Your shirt is clearly expressing joy over a poop.

Hey, real men wear pink capris!…not real manly men, but yes technically still male.

I’ll tell ya what buddy let me go ahead and take a worldwide vote and see who all wouldn’t want to be born a white male in America. I’m sure you and the 3 other idiots will be new best friends. Geez, this guy would hit the lottery and bitch about the taxes.

Well that’s certainly a different approach to looking foolish. Totally successful by the way, but definitely a different route there. You’re a pioneer of foolish!

You look like you messed up being a juggalo, which is about the saddest, most depressing thing I could think of saying to someone else.

Hell ya! ‘Bout time Walmart hired a real gardener to work there. I can’t wait to talk to you all about your bare white pasty tulips.

You’d figure that black hole would have sucked in that excess thigh cheese.

Is there anything sexier than Walmart selfies? I mean, they are classy, sexy and practical all rolled into one pic! Anyway, enjoy these selfies, and before I forget I wanted to point out how hot that blonde’s Adam’s apple was.

Is it weird my first thought right now is if she is willing to show some boobies at Walmart then she probably could have put that to good use and skipped some Black Friday lines? Also, boobs are the best. Just in case anyone had any doubt as to what is the best, it’s boobs. The answer has always been and will always be boobs.

I feel your pain lady. Sometimes I think Walmart has 30 lanes just to show you that it could be fast and convenient to check out but would rather make you and everyone else wait in line at the 4 lanes that are open and always seem to be manned by the slowest human beings allowed by law.

The extremely popular infatuation with Hello Kitty is something I’ll never understand. But whatever, the real issue at hand is if I were to force you to chose to pick between driving that car the rest of your life or getting that tattoo which would you choose? Also, is that a DarthVader/Hello Kitty hybrid tattoo?

In case of emergency, toss those puppies up over your shoulders and use them as a life preserver.

Pictures like these two bring a tear to my eye because I know this vicious circle of bad decision making will (unfortunately for these kids) continue through the generations. Parents set examples, kids follow examples, kid ends up on People Of Walmart. Music to my ears!

I hate it when the muffin batter spills up over the pan like that. I usually just toss ‘em out and start from scratch. Objections? Do I hear any objections? Yeah I didn’t think so.

Holy hell, I really hope that is George Carlin back from the dead because he is one of the funniest guys ever. Chances are good it’s just some guy that hates people, mainly because everyone calls him George Carlin.

My mind is blown at the amount of mullet awesomeness going on here. Which one do you guys love more? The flowing eagle locks that just majestically transform into fringe or what I assume the real meth addict Jesse Pinkman would actually look like?

It’s a battle of bottom biscuits in what I think is also a battle of the sexes? I’m not really 100% sure the one in the backpack is a dude, but let’s be real here, that outfit doesn’t work well on any human being so it doesn’t matter.

When you have bodies like this, it’s almost a crime to wear a shirt. I mean, who doesn’t love a lower back hair tramp stamp?

Ri-DONK-ulously low prices mo-fo!….Also, where is the PeopleOfWalmart donk? Let’s get on that people!

Holy mother of mercy. You just pulled off a spot-on Magda from There’s Something About Mary of epic proportions!

Because pants are for all of you caged sheep that play by society’s rules…and aren’t tripping on shrooms

I see you’re working up quite a sweat from all those kisses you’re getting. Might wanna let that sucker breathe a minute sweetheart.

More like “How the Grinch Stole My Childhood Innocence.”

Pffft amateur, my accountant does her own dreadlocks at work. So I know I’m all set. Choke on that baby!!

How do you like your public ass cracks? Over the top or a little drive-thru window action?

This lady has a toilet paper tail and yet I somehow think she looks better than those idiots running around with fur tails on. So yeah, try that one on for size weird anime kids. Also, why hasn’t someone helped her out yet? I feel like that would be too big to miss for long.

In the first three parts (Part 1, Part 2, Part 3) of this disheartening look back at a century of central banking, income taxing, military warring, energy depleting and political corrupting, I made a case for why we are in the midst of a financial, commercial, political, social and cultural collapse. In this final installment I’ll give my best estimate as to what happens next and it has a 100% probability of being wrong. There are so many variables involved that it is impossible to predict the exact path to our world’s end. Many people don’t want to hear about the intractable issues or the true reasons for our predicament. They want easy button solutions. They want someone or something to fix their problems. They pray for a technological miracle to save them from decades of irrational myopic decisions. As the domino-like collapse worsens, the feeble minded populace becomes more susceptible to the false promises of tyrants and psychopaths. There are a myriad of thugs, criminals, and autocrats in positions of power who are willing to exploit any means necessary to retain their wealth, power and control. The revelations of governmental malfeasance, un-Constitutional mass espionage of all citizens, and expansion of the Orwellian welfare/warfare surveillance state, from patriots like Julian Assange, Bradley Manning and Edward Snowden has proven beyond a doubt the corrupt establishment are zealously anxious to discard and stomp on the U.S. Constitution in their desire for authoritarian control over our society.

Anyone who denies we are in the midst of an ongoing Crisis that will lead to a collapse of the system as we know it is either a card carrying member of the corrupt establishment, dependent upon the oligarchs for their living, or just one of the willfully ignorant ostriches who choose to put their heads in the sand and hum the Star Spangled Banner as they choose obliviousness to awareness. Thinking is hard. Feeling and believing a storyline is easy.

A moral society must be inhabited by an informed, educated, aware populace and governed by honorable leaders who oversee based upon the nation’s founding principles of liberty, freedom and limited government of, by and for the people. A moral society requires trust, honor, property rights, simple just laws, and the freedom to succeed or fail on your own merits. There is one major problem in creating a true moral society where liberty, freedom, trust, honor and free markets are cherished – human beings. We are a deeply flawed species who are prone to falling prey to the depravities of lust, gluttony, greed, sloth, wrath, envy and pride. Men have always been captivated by the false idols of dominion, power and wealth. The foibles of human nature haven’t changed over the course of history. This is why we have 80 to 100 year cycles driven by the same human strengths and shortcomings revealed throughout recorded history.

Empires rise and fall due to the humanness of their leaders and citizens. The great American Empire is no different. It was created a mere 224 years ago by courageous patriots who risked their wealth and their lives to create a Republic founded upon the principles of freedom, liberty, and the pursuit of happiness; took a dreadful wrong turn in 1913 with the creation of a privately held central bank to control its currency and introduction of an income tax; devolved into an empire after World War II, setting it on a course towards bankruptcy; sealed its fate in 1971 by unleashing power hungry psychopathic elitists to manipulate the monetary and fiscal policies of the nation to enrich themselves; and has now entered the final frenzied phase of pillaging, currency debasement, war mongering, and ransacking of civil liberties. Despite the frantic efforts of the financial elite, their politician puppets, and their media propaganda outlets, collapse of this aristocracy of the moneyed is a mathematical certainty. Faith in the system is rapidly diminishing, as the issuance of debt to create the appearance of growth has reached the point of diminishing returns.

“At the root of America’s economic crisis lies a moral crisis: the decline of civic virtue among America’s political and economic elite. A society of markets, laws, and elections is not enough if the rich and powerful fail to behave with respect, honesty, and compassion toward the rest of society and toward the world.” – Jeffrey Sachs

The day of reckoning for a century of putting our faith in the wrong people with wrong ideas and evil intentions is upon us. Dmitry Orlov provides a blueprint for the collapse in his book – The Five Stages of Collapse – Survivors’ Toolkit:

Stage 1: Financial Collapse. Faith in “business as usual” is lost. The future is no longer assumed to resemble the past in any way that allows risk to be assessed and financial assets to be guaranteed. Financial institutions become insolvent; savings wiped out and access to capital is lost.

Stage 2: Commercial Collapse. Faith that “the market shall provide” is lost. Money is devalued and/or becomes scarce, commodities are hoarded, import and retail chains break down and widespread shortages of survival necessities become the norm.

Stage 3: Political Collapse. Faith that “the government will take care of you” is lost. As official attempts to mitigate widespread loss of access to commercial sources of survival necessities fail to make a difference, the political establishment loses legitimacy and relevance.

Stage 4: Social Collapse. Faith that “your people will take care of you” is lost, as social institutions, be they charities or other groups that rush to fill the power vacuum, run out of resources or fail through internal conflict.

Stage 5: Cultural Collapse. Faith in the goodness of humanity is lost. People lose their capacity for “kindness, generosity, consideration, affection, honesty, hospitality, compassion, charity.” Families disband and compete as individuals for scarce resources. The new motto becomes “May you die today so that I can die tomorrow.”

The collapse is occurring in fits and starts. The stages of collapse do not necessarily have to occur in order. You can recognize various elements of the first three stages in the United States today. Stage 1 commenced in September 2008 when this Crisis period was catalyzed by the disintegration of the worldwide financial system caused by Wall Street intentionally creating the largest control fraud in world history, with easy money provided by Greenspan/Bernanke, fraudulent mortgage products, fake appraisals, bribing rating agencies to provide AAA ratings to derivatives filled with feces, and having their puppets in the media and political arena provide the propaganda to herd the sheep into the slaughterhouse.

The American people neglected their civic duty to elect leaders who would tell them the truth and represent current and future generations equally. They have neglected the increasing lawlessness of Wall Street, K Street and the corporate suite. The American people have lived in denial about their responsibility for their own financial well-being, willingly delegating it to a government of math challenged politicians who promised trillions more than they could ever deliver. The American people have delayed tackling the dire issues confronting our nation, including: $200 trillion of unfunded liabilities, the military industrial complex creating wars across the globe, militarization of our local police forces, domestic spying on every citizen, allowing mega-corporations and the financial elite to turn our nation from savings based production to debt based consumption, and allowing corporations, the military industrial complex, Wall Street, and shadowy billionaires to pick and control our elected officials. The civic fabric of the country is being torn at the points of extreme vulnerability.

“At home and abroad, these events will reflect the tearing of the civic fabric at points of extreme vulnerability – problem areas where, during the Unraveling, America will have neglected, denied, or delayed needed action. Anger at “mistakes we made” will translate into calls for action, regardless of the heightened public risk. It is unlikely that the catalyst will worsen into a full-fledged catastrophe, since the nation will probably find a way to avert the initial danger and stabilize the situation for a while. Yet even if dire consequences are temporarily averted, America will have entered the Fourth Turning.” – The Fourth Turning – Strauss & Howe – 1997

Our Brave New World controllers (bankers, politicians, corporate titans, media moguls, shadowy billionaires) were able to avert a full-fledged catastrophe in the fall of 2008 and spring of 2009 which would have put an end to their reign of destruction. To accept the rightful consequences of their foul actions was intolerable to these obscenely wealthy, despicable men. Their loathsome and vile solutions to a crisis they created have done nothing to relieve the pain and suffering of the average person, while further enriching them, as they continue to gorge on the dying carcass of a once thriving nation. Despite overwhelming public outrage, Congress did as they were instructed by their Wall Street masters and handed over $700 billion of taxpayer funds into Wall Street vaults, under the false threat of systematic collapse. The $800 billion of pork stimulus was injected directly into the veins of corporate campaign contributors. The $3 billion Cash for Clunkers scheme resulted in pumping taxpayer dollars into the government owned union car companies, while driving up the prices of used cars and hurting lower income folks.

Ben Bernanke has peddled the false paradigm of quantitative easing (code for printing money and airlifting it to Wall Street) as benefitting Main Street. Nothing could be further from the truth. He bought $1.3 trillion of toxic mortgage backed securities from his Wall Street owners. He has pumped a total of $2.8 trillion into the hands of Wall Street since September 2008, and is singlehandedly generating $5 billion of risk free profits for these deadbeats by paying them .25% on their reserves. Drug dealer Ben continues to pump $2.8 billion per day into the veins of Wall Street addicts and any hint of tapering the heroin causes the addicts to flail about. Ben should be so proud. He should hang a Mission Accomplished banner whenever he gives a speech. Bank profits reached an all-time record in the 2nd quarter, at $42.2 billion, with 80% of those profits going to the 2% Too Big To Trust Wall Street Mega-Goliath Banks. It’s enough to make a soon to retire, and take a Wall Street job, central banker smile.

“The money rate can, indeed, be kept artificially low only by continuous new injections of currency or bank credit in place of real savings. This can create the illusion of more capital just as the addition of water can create the illusion of more milk. But it is a policy of continuous inflation. It is obviously a process involving cumulative danger. The money rate will rise and a crisis will develop if the inflation is reversed, or merely brought to a halt, or even continued at a diminished rate. Cheap money policies, in short, eventually bring about far more violent oscillations in business than those they are designed to remedy or prevent.” – Henry Hazlitt – 1946

Any serious minded person knew Wall Street had too much power, too much control, and too much influence in 2008 when they crashed our economic system. When something is too big to fail because it will create systematic collapse, you make it smaller. Instead we have allowed our sociopathic rulers to allow these parasitic institutions to get even larger. Just 12 mega-banks control 70% of all the banking assets in the country, with 90% controlled by the top 86 banks. There are approximately 8,000 financial institutions in this country. Wall Street will be congratulating themselves with record compensation of $127 billion and record bonuses of $23 billion for a job well done. It is dangerous work making journal entries relieving loan loss reserves, committing foreclosure fraud, marking your assets to unicorn, making deposits at the Fed, and counting on the Bernanke Put to keep stocks rising. During a supposed recovery from 2009 to 2011, average real income per household grew pitifully by 1.7%, but all the gains accrued to Bernanke’s minions. Top 1% incomes grew by 11.2% while bottom 99% incomes shrunk by 0.4%. Therefore, the top 1% captured 121% of the income gains in the first two years of the recovery. This warped trend has only accelerated since 2011.

The median household income has fallen by $2,400 to $52,100 since the government proclaimed the end of the recession in 2009. Real wages for real people continue to fall. A record 23.1 million households (20% of all households) are receiving food stamps. After four years of “recovery” propaganda, we are left with 2.2 million less people employed (5 million less full time jobs) and 22 million more people on SNAP and SSDI. A record 90.5 million working age Americans are not working, with labor participation at a 35 year low. Ben’s money has not trickled down, but his inflation has fallen like a load of bricks on the heads of the middle class. Bernanke’s QE to infinity constitutes a transfer of purchasing power away from the middle class to the bankers, mega-corporations and .1%. This Cantillon effect means that newly created money is neither distributed evenly nor simultaneously among the population. Some users of money profit from rising prices, and others suffer from them. This results in a transfer of wealth (a hidden tax) from later receivers to earlier receivers of new money. This is why the largest banks and largest corporations are generating the highest profits in history, while the average person sinks further into debt as their real income declines and real living expenses (energy, food, clothing, healthcare, tuition) rise.

Ben works for your owners. Real GDP (using the fake government inflation adjustment) since July 2009 is up by a wretched 5.6%. Revenue growth of the biggest corporations in the world is up by a pathetic 12%. One might wonder how corporate profits could be at record levels with such doleful economic performance. One needs to look no further than Ben’s balance sheet, which has increased by 174%. There appears to be a slight correlation between Ben’s money printing and the 162% increase in the S&P 500 index. With the top 1% owning 42.1% of all financial assets (top .1% own most of this) and the bottom 80% owning only 4.7% of all financial assets, one can clearly see who benefits from QE to infinity.

The key take away from what the ruling class has done since 2008 is they have only temporarily delayed the endgame. Their self-serving exploits have guaranteed that round two of the financial collapse will be epic in proportion and intensity. This Fourth Turning Crisis is ongoing. The linear thinkers who control the levers of power keep promising a return to normalcy and resumption of growth. This is an impossibility – mathematically & socially. Fourth Turnings do not end without the existing social order being swept away in a tsunami of turmoil, violence, suffering and war. Orlov’s stages of collapse will likely occur during the remaining fifteen years of this Crisis. We are deep into Stage 1 as our national Detroitification progresses towards bankruptcy, with an added impetus from our trillion dollar wars of choice in the Middle East. Commercial collapse has begun, as faith in the fantasy of free market capitalism is waning. The race to the bottom with currency debasement around the globe is reaching a tipping point, and the true eternal currencies of gold and silver are being hoarded and shipped from the West to the Far East.

When the financial collapse reaches its crescendo, the just in time supply chain, that keeps cheese doodles and cheese whiz on your grocery store shelves, Chinese produced iGadgets in your local Wal-Mart Supercenter, and gasoline flowing out of gas station hoses into your leased Cadillac Escalade, will break down rapidly. The strain of $110 oil is already evident. The fireworks will really get going when ATM machines run dry and the EBT cards stop functioning. Within a week riots and panic will engulf the country.

“At some point we are bound to hear, from across two oceans, the shocking words “Your money is no good here.” Fast forward to a week later: banks are closed, ATMs are out of cash, supermarket shelves are bare and gas stations are starting to run out of fuel. And then something happens: the government announces they have formed a crisis task force, and will nationalize, recapitalize and reopen banks, restoring confidence. The banks reopen, under heavy guard, and thousands of people get arrested for attempting to withdraw their savings. Banks close, riots begin. Next, the government decides that, to jump-start commerce, it will honor deposit guarantees and simply hand out cash. They print and arrange for the cash to be handed out. Now everyone has plenty of cash, but there is still no food in the supermarkets or gasoline at the gas stations because by now the international supply chains have broken down and the delivery pipelines are empty.” – Dmitry Orlov – The Five Stages of Collapse

We are witnessing the beginning stages of political collapse. The government and its leaders are being discredited on a daily basis. The mismanagement of fiscal policy, foreign policy and domestic policy, along with the revelations of the NSA conducting mass surveillance against all Americans has led critical thinking Americans to question the legitimacy of the politicians running the show on behalf of the bankers, corporations and arms dealers. The Gestapo like tactics used by the government in Boston was an early warning sign of what is to come. Government entitlement promises will vaporize, as they did in Detroit, with pension promises worth only ten cents on the dollar. Total social and cultural collapse could resemble the chaotic civil war scenarios playing out in Libya and Syria. The best case scenario would be for a collapse similar to the Soviet Union’s relatively peaceful disintegration into impotent republics. I don’t believe we’ll be this fortunate. The most powerful military empire in world history will not fade away. It will go out in a blaze of glory with a currency collapse, hyper-inflation, and war on a grand scale.

“History offers even more sobering warnings: Armed confrontation usually occurs around the climax of Crisis. If there is confrontation, it is likely to lead to war. This could be any kind of war – class war, sectional war, war against global anarchists or terrorists, or superpower war. If there is war, it is likely to culminate in total war, fought until the losing side has been rendered nil – its will broken, territory taken, and leaders captured.” – The Fourth Turning – Strauss & Howe – 1997

“Use of money concentrates trust in a single central authority – the central bank – and, over extended periods of time, central banks always tend to misbehave. Eventually the “print” button on the central banker’s emergency console becomes stuck in the depressed position, flooding the world with worthless notes. People trust that money will remain a store of value, and once the trust is violated a gigantic black hole appears at the very center of society, sucking in peoples’ savings and aspirations along with their sense of self-worth. When those who have become psychologically dependent on money as a yardstick, to be applied to everything and everyone, suddenly find themselves in a world where money means nothing, it is as if they have gone blind; they see shapes but can no longer resolve them into objects. The result is anomie – a sense of unreality – accompanied by deep depression. Money is an addiction – substance-less and unreal, and sets itself up for a severe and lengthy withdrawal.” – Dmitry Orlov – The Five Stages of Collapse

Our modern world revolves around wealth, the appearance of wealth, the false creation of wealth through the issuance of debt, and trust in the bankers and politicians pulling the levers behind the curtain. The entire world economic system is dependent on trusting central bankers whose only response to any crisis is to create more debt. The death knell is ringing loud and clear, but people around the globe are desperately clinging to their normalcy biases and praying to the gods of cognitive dissonance. It seems the only things that matter to our controllers are stock market levels, the continued flow of debt to the plebs, continued doling out of hush money to those on the dole, and of course an endless supply of brown skinned enemies to attack. With every country in the world attempting to the same solution of debasing their currencies, we are rapidly approaching the tipping point. India is the canary in the coal mine.

An exponential growth model built upon cheap plentiful energy and debt creation has its limits, and we’ve reached them. With the depletion of inexpensive, easily accessible energy resources, higher prices will continue to slow world economies. Demographics in the developed world are slowing the global economy as millions approach their old age with little savings due to over consuming during their peak earnings years. Bernanke has already quadrupled his balance sheet with no meaningful benefit to the economy or the financial well-being of the average middle class American. Financial manipulation that creates nothing has masked the rot consuming our economic system. The game has been rigged in favor of the owners, but even a rigged game eventually comes to an end. Americans and Europeans can no longer maintain a façade of wealth by buying knickknacks from China with money they don’t have. The US and Europe are finding that their credit is no longer good in the exporting Far East countries. This is a perilous development, as the West has depended upon foreigners to accommodate its never ending expansion of credit. Without that continual expansion of debt, the Ponzi scheme comes crashing down. As China, Japan and the rest of Asia have balked at buying U.S. Treasuries with negative real yields, the only recourse for Ben has been to monetize the debt through QE and inflation. The doubling of ten year Treasury rates in a matter of three months due to just talk of possibly slowing QE should send shivers down your spine.

We are supposedly five years past the great crisis. Magazine covers proclaimed Bernanke a hero. If we are well past the crisis, why are the extreme emergency measures still in effect? If the economy is growing and jobs are being created, why do we need $85 billion of government debt to be monetized each and every month? Why are the EU, Japan, and China printing even faster than the Fed? The answer is simple. If the debt was not being monetized, it would have to be purchased out in the free market. Purchasers would require an interest rate far above the 2.9% being paid today. The debt levels in the U.S., Europe and Japan are so large that a rise in interest rates of just a few points would explode budget deficits and lead to a worldwide financial collapse. This is why Bernanke and the rest of his central banker brethren are trapped by their own ideology of bubble production. Just the slowing of debt creation will lead to collapse. Bernanke needs a Syrian crisis to postpone the taper talk. Those in control need an endless number of real or false flag crises to provide cover for their printing presses to keep rolling.

There are a couple analogies that apply to our impending doom. The country is like a 224 year old oak tree that has been slowly rotting on the inside due to the insidious diseases of hubris, apathy, selfishness, dependence, delusion, and debasement. The old oak gives an outward appearance of health and stability. Winter has arrived and gale force winds are in the forecast. One gust of wind and the mighty aged oak will topple and come crashing to earth. I think an even more fitting analogy is the sandpile with grains of sand being added day after day. Seven out of ten Americans receive more in government benefits than they pay in taxes. Goliath corporations and the uber-wealthy use the tax code and legislation to syphon hundreds of billions from the national treasury every year. We spend $1 trillion per year on past, current and future wars of choice. Annual interest on the debt we’ve racked up in the last few decades already approaches $400 billion per year. The entire Federal budget totaled $400 billion in 1977. The sandpile grows ever higher, while its instability expands exponentially. One seemingly innocuous grain of sand will ultimately cause the pile to collapse catastrophically. Will it be an unintended consequence of a missile launch into Syria? Will it be a spike in oil prices? Will it be the collapse of one of the EU PIIGS? Will it be an assassination of a political figure or banker? No one knows. But that innocuous grain of sand will trigger the collapse of the entire pile.

Worried people are looking for solutions. They often get angry at me because they don’t think I provide answers to the issues I raise about our corrupt failing system. They want easy answers to intractable problems. Sadly, I’ve come to the conclusion that our system and majority of citizens are too corrupted to change our course through the ballot box or instituting policies along the lines of those proposed by Ron Paul and many other thoughtful liberty minded people. We are experiencing the downside of a representative democracy. Once a person is democratically elected a gulf is created between the electors and the person they elected, as the representative becomes corrupted and bought by moneyed interests. Elected officials become a class unto themselves. The political class grows to be puppets that resemble human beings but are nothing but cogs in a vast corporate run machine, pawns in an enormous game of chess played by powerful vindictive immoral men.

There are no cures for our disease. It’s terminal. Anyone telling you they have the answers is either lying or trying to sell you something. More people and organizations are on the take than are playing by the rules. The producers are being overrun by the parasites. The barbarians are at the gate. An implosion of societal trust is underway. The next stage of this crisis, which I believe will materialize within the next twelve months will try the souls of the weary.

“As the Crisis catalyzes, these fears will rush to the surface, jagged and exposed. Distrustful of some things, individuals will feel that their survival requires them to distrust more things. This behavior could cascade into a sudden downward spiral, an implosion of societal trust. This might result in a Great Devaluation, a severe drop in the market price of most financial and real assets. This devaluation could be a short but horrific panic, a free-falling price in a market with no buyers. Or it could be a series of downward ratchets linked to political events that sequentially knock the supports out from under the residual popular trust in the system. As assets devalue, trust will further disintegrate, which will cause assets to devalue further, and so on.” – The Fourth Turning – Strauss & Howe – 1997

As a nation we have squandered our inheritance, born of the blood of patriots. A freedom loving, liberty minded, self-responsible, courageous people have allowed ourselves to fall prey to selfishness, apathy, complacency and dependency. Once we allowed our human appetites of greed, power seeking, and control to override the moral responsibility for our own lives and the lives of future unborn generations, collapse was inevitable. The danger now is what happens after the unavoidable collapse. Will the millions of dependency zombies beg for a strong dictator to protect them, provide for them and lead them into further bondage? Or will the spark of liberty and freedom reignite, allowing citizens to throw off the shackles of banker and corporate control? I believe most of the people in this country are good hearted. We are merely pawns in this game of Risk being played by those seeking power, wealth and world domination. We are all trapped in our own forms of normalcy bias. Have I cashed out my retirement funds, sold my suburban house and built a doomstead in the mountains? No I haven’t. Do I second guess myself sometimes? Yes I do. But even the aware have families to support, jobs to go to, bills to pay, laundry to do, lawns to mow, and lives to live. I can’t live in constant fear of what might happen. We only get 80 or so years on this earth, if we’re lucky. The best we can do is leave a positive legacy for our children and their children. A drastic change to our way of life is coming, but most of us are trapped in a cage of our own making.

Each living generation will need to do their part during this Crisis if we are to survive the coming storm. Since no one knows the nature of how the next fifteen years will unfold, it would be wise to at least make basic preparations for food, water, heat and protection. This is easier for some than others, but you don’t have to star on Doomsday Preppers in order to stock up on items that can be purchased at Wal-Mart today, but won’t be available when the global supply chain breaks down. Make sure you have neighbors and family you can rely upon. A small community of like-minded people with varied skills is more likely to succeed in our brave old world than rugged individualists. With no financial means to maintain our globalized world, living locally will take on a new meaning. After much turmoil, chaos, violence, and likely mass casualties the best outcome would be for the Great American Empire to break into regional republics, incapable of waging global war, led by law abiding moral liberty minded individuals, and willing to trade freely and honestly with their fellow republics. Daily life would revert back to a simpler Amish like time. Would that be so bad?

This Fourth Turning could end with a whimper or a bang. There are enough nuclear arms to obliterate the world ten times over. There are enough hubristic egomaniacal psychopathic men in power, that the use of those weapons has a high likelihood of happening. It will be up to the people to not allow this horrific result. I love my country and despise my government. The Declaration of Independence clearly states that when a long train of abuses and usurpations lead toward despotism, it is our right and duty to throw off that government and provide new guards of liberty. My family comes first with my country a close second. I will fight with whatever means necessary to protect my family and do what I can to influence the future course of our country. Time is running out. Will we have the courage, fortitude and wisdom to make the right decisions over the next fifteen years? Will we choose glory or destruction? The fate of our nation hangs in the balance. Are you prepared? Are you ready to fight for your family and your rights?

The Fourth Turning could spare modernity but mark the end of our nation. It could close the book on the political constitution, popular culture, and moral standing that the word America has come to signify. The nation has endured for three saecula; Rome lasted twelve, the Soviet Union only one. Fourth Turnings are critical thresholds for national survival. Each of the last three American Crises produced moments of extreme danger: In the Revolution, the very birth of the republic hung by a thread in more than one battle. In the Civil War, the union barely survived a four-year slaughter that in its own time was regarded as the most lethal war in history. In World War II, the nation destroyed an enemy of democracy that for a time was winning; had the enemy won, America might have itself been destroyed. In all likelihood, the next Crisis will present the nation with a threat and a consequence on a similar scale. – The Fourth Turning – Strauss & Howe – 1997

Heritage or hate argument aside, this seems like enough of a reason to convince me the stars and bars needs to be hidden from everyone!

Hey hey hey hey hey! I absolutely did NOT order my bottom biscuits with sausage. I specifically said NO sausage!

Wow! Just wow! I mean, don’t get me wrong I’m relieved you hand pockets are conveniently located low enough that they cover your nipples but for the love of all that is good in this world put on a f*cking bra lady! I don’t mind seeing Kate Upton in a see through mesh top, that’s cool. Are you Kate Upton? No? Well then take those old ass water balloons and get the hell out of here.

Good thing you laid that out for me, I wasn’t sure if I’d have time to write that answer to life’s question down or not. Should I do everything in that order too or is it cool if I hail Satan before I chow down on some pussy?

Seriously, when will Elvis leave the building for good?

Whoa Whoa Whoa Whoa Whoa. Don’t you try to put that on me!

Here is something I just realized, even with that masked face I love boobies and I’d still hit it. What’s up guy standards? *high-fives nearest dude*

Let’s be honest, it was only a matter of time before someone from Duck Dynasty showed up here. Willie Robertson & his wife know they are PoWM royalty.

Yo son, I heard you like cars. So I put cars on your car! Xzibit style homie!

Is there anything better in the world than bro titties? Oh there is? Like a billion things? Really a billion? Ohh, ok. Well then, ignore that statement and when you’re done with all those other things then maybe you can circle back and enjoy some bro titties.

Because if she didn’t get enough of your attention with her dirty dreads/afro puff combo or a Geisha fan then she’ll make sure you turn your focus to her with the bull horn. Basically, do yourself a favor and just look for a minute then run.

It must be that time of year when the People of Walmart bust out their favorite backless shirts that look like moths destroyed since the previous summer. We are gonna throw a little curveball at you on this one. One of these fine specimens is a dude. Can you guess which one? Yeah probably, it’s really not that difficult. It was fun playing though, right? No? We are morons? Well, yes, yes we are.

To be fair, I basically say those women bodybuilders look like men anyway so I suppose a muscle man with some femininity is basically the same thing. Wonder if GirlsInYogaPants.com agrees?

Cheetah biscuits. They’re like bottom biscuits, but they’ve got a more wild smokey flavor. I mean, they still taste like shit, but a wild smokier shit.

La Bella Vita, hmmm I didn’t know the Italians decided to change its meaning from “the beautiful life” to “skeezers gonna twerk it”. Thanks for keeping me updated Rosetta Stone.

I don’t know what this is but I do know that it is wrong. Whatever you were going for you failed at. If you think this is right, you are mistaken. I’m not really sure how else to say this but if I haven’t been clear enough let me know and i’ll see what else I can come up with.

Look at these two sex symbols! Okay, maybe it’s more like symbols for abstinence, but whatever. The important question here is “Who Would You Do?”

What did I tell you guys? Huh? Who called that it was time for some crazy-ass asses in white! This guy did. So I told you that, now you tell me which is worse, loose and see through or tight and tighter.

Dear Walmart, thanks for scaring the living hell out of everyone today. However, we’d also like to point out that she might be the hottest chick we’ve seen in there for quite some time.

Of course Jesus would park his van at Walmart, because he probably saw our site and realized he could cut down on time and save soooo many souls in one place!

You haven’t lived until you have walked around Walmart with a monkey’s vagina touching you neck. Yeah, it’s gross, but you people need to think about that so people stop doing this crap. They aren’t birds, you’ve got monkey genitals all up on your face!

Some pirates looking for booty are gonna be in for quite the surprise when they find these black spots marked for a pirate’s death! (Shout out to Muppets Treasure Island for that bit of knowledge.)

Are me and Eric Cartman the only ones that get annoyed by modern day hippies? There truly is no point to them whatsoever, unless the point is to look weird and smell all sorts of funny.

I guess this isn’t technically a “Who Wears It Better?” unless I suppose I ask you which cart wears it’s lazy bitch better? Yeah, I guess that could work. Who wears it better?

Ahh yes, #3 in the pervert playbook: The Upskirt! So which under booty bottom biscuit would you put on the books?

This guy couldn’t look anymore like a rat if he was in the middle of narcing on John Gotti.

Hey people, just a quick reminder, patterns don’t typically go together very well. Just because it’s a nice shirt and those are nice pants does not automatically let them combine to make a nice outfit. I mean, nothing in here is working on its own, but even if it did that would apply. That’s all I’m saying. Anywho, I’d like you guys to pick which one of these screwed the pooch the least.

Looks like we got ourselves a couple of bitches here that just love to bitch about other bitches. Also, my dog is a bitch and I can’t really think of any other ways to use the word bitch…bitch.

Alright people, we haven’t given anything away for a while so let’s change that. Funniest pickup line wins either a copy of our new book or calendar, your choice. GOOOOOOOO!

No use actually buying toilet paper when you’re just gonna let it air dry. Either have poor hygiene or poor fiscal responsibility, not both.

Everyone say hello to Brandon from MTV’s True Life: “Addicted to Porn”. *This is where you all say hello in unison like an intervention* Anyway, not sure whether or not Brandon is still addicted to porn or not because I haven’t watched anything on MTV since 1998. Do we have any porn addicts out there who just happen to be browsing our site during a down time?

Remember guys, if you ever find yourself terribly lost in this horrific neck of the woods you can always find your way out by following the North Star.

Plot: Smokey meets a VW bug, accidentally knocks her up, gets behind on child support, gets some gambling debt and then his sciatica starts acting up.

I was gonna yell at this dude for his complete disregard for personal space but then I realized any girl that wears see-through lace pants doesn’t really have “personal space”.

Don’t worry, your ass in white yoga pants definitely does not look like mashed potatoes. Nope. Not at all. I don’t know what to tell you, I’m not sure why that girl has a bowl of gravy.

Your hair looks like something they find buried under a hoarder’s couch.

Is it just me, or are the signs of consumer collapse as clear as a Lowes parking lot on a Saturday afternoon? Sometimes I wonder if I’m just seeing the world through my pessimistic lens, skewing my point of view. My daily commute through West Philadelphia is not very enlightening, as the squalor, filth and lack of legal commerce remain consistent from year to year. This community is sustained by taxpayer subsidized low income housing, taxpayer subsidized food stamps, welfare payments, and illegal drug dealing. The dependency attitude, lifestyles of slothfulness and total lack of commerce has remained constant for decades in West Philly. It is on the weekends, cruising around a once thriving suburbia, where you perceive the persistent deterioration and decay of our debt fixated consumer spending based society.

The last two weekends I’ve needed to travel the highways of Montgomery County, PA going to a family party and purchasing a garbage disposal for my sink at my local Lowes store. Montgomery County is the typical white upper middle class suburb, with tracts of McMansions dotting the landscape. The population of 800,000 is spread over a 500 square mile area. Over 81% of the population is white, with the 9% black population confined to the urban enclaves of Norristown and Pottstown.

The median age is 38 and the median household income is $75,000, 50% above the national average. The employers are well diversified with an even distribution between education, health care, manufacturing, retail, professional services, finance and real estate. The median home price is $300,000, also 50% above the national average. The county leans Democrat, with Obama winning 60% of the vote in 2008. The 300,000 households were occupied by college educated white collar professionals. From a strictly demographic standpoint, Montgomery County appears to be a prosperous flourishing community where the residents are living lives of relative affluence. But, if you look closer and connect the dots, you see fissures in this façade of affluence that spread more expansively by the day. The cheap oil based, automobile dependent, mall centric, suburban sprawl, sanctuary of consumerism lifestyle is showing distinct signs of erosion. The clues are there for all to see and portend a bleak future for those mentally trapped in the delusions of a debt dependent suburban oasis of retail outlets, chain restaurants, office parks and enclaves of cookie cutter McMansions. An unsustainable paradigm can’t be sustained.

The first weekend had me driving along Ridge Pike, from Collegeville to Pottstown. Ridge Pike is a meandering two lane road that extends from Philadelphia, winds through Conshohocken, Plymouth Meeting, Norristown, past Ursinus College in Collegeville, to the farthest reaches of Montgomery County, at least 50 miles in length. It served as a main artery prior to the introduction of the interstates and superhighways that now connect the larger cities in eastern PA. Except for morning and evening rush hours, this road is fairly sedate. Like many primary routes in suburbia, the landscape is engulfed by strip malls, gas stations, automobile dealerships, office buildings, fast food joints, once thriving manufacturing facilities sitting vacant and older homes that preceded the proliferation of cookie cutter communities that now dominate what was once farmland.

I should probably be keeping my eyes on the road, but I can’t help but notice the telltale signs of an economic system gone haywire. As you drive along, the number of For Sale signs in front of homes stands out. When you consider how bad the housing market has been, the 40% decline in national home prices since 2007, the 30% of home dwellers underwater on their mortgage, and declining household income, you realize how desperate a home seller must be to try and unload a home in this market. The reality of the number of For Sale signs does not match the rhetoric coming from the NAR, government mouthpieces, CNBC pundits, and other housing recovery shills about record low inventory and home price increases.

The Federal Reserve/Wall Street/U.S. Treasury charade of foreclosure delaying tactics and selling thousands of properties in bulk to their crony capitalist buddies at a discount is designed to misinform the public. My local paper lists foreclosures in the community every Monday morning. In 2009 it would extend for four full pages. Today, it still extends four full pages. The fact that Wall Street bankers have criminally forged mortgage documents, people are living in houses for two years without making mortgage payments, and the Federal Government backing 97% of all mortgages while encouraging 3.5% down financing does not constitute a true housing recovery. Show me the housing recovery in these charts.

Existing home sales are at 1998 levels, with 45 million more people living in the country today.

New single family homes under construction are below levels in 1969, when there were 112 million less people in the country.

Another observation that can be made as you cruise through this suburban mecca of malaise is the overall decay of the infrastructure, appearances and disinterest or inability to maintain properties. The roadways are potholed with fading traffic lines, utility poles leaning and rotting, and signage corroding and antiquated. Houses are missing roof tiles, siding is cracked, gutters astray, porches sagging, windows cracked, a paint brush hasn’t been utilized in decades, and yards are inundated with debris and weeds. Not every house looks this way, but far more than you would think when viewing the overall demographics for Montgomery County. You wonder how many number among the 10 million vacant houses in the country today. The number of dilapidated run down properties paints a picture of the silent, barely perceptible Depression that grips the country today. With such little sense of community in the suburbs, most people don’t even know their neighbors. With the electronic transfer of food stamps, unemployment compensation, and other welfare benefits you would never know that your neighbor is unemployed and hasn’t made the mortgage payment on his house in 30 months. The corporate fascist ruling plutocracy uses their propaganda mouthpieces in the mainstream corporate media and government agency drones to misinform and obscure the truth, but the data and anecdotal observational evidence reveal the true nature of our societal implosion.

A report by the Census Bureau this past week inadvertently reveals data that confirms my observations on the roadways of my suburban existence. Annual household income fell in 2011 for the fourth straight year, to an inflation-adjusted $50,054. The median income — meaning half earned more, half less — now stands 8.9% lower than the all-time peak of $54,932 in 1999. It is far worse than even that dreadful result. Real median household income is lower than it was in 1989. When you understand that real household income hasn’t risen in 23 years, you can connect the dots with the decay and deterioration of properties in suburbia. A vast swath of Americans cannot afford to maintain their residences. If the choice is feeding your kids and keeping the heat on versus repairing the porch, replacing the windows or getting a new roof, the only option is survival.

All races have seen their income fall, with educational achievement reflected in the much higher incomes of Whites and Asians. It is interesting to note that after a 45 year War on Poverty the median household income for black families is only up 19% since 1968.

Now for the really bad news. Any critical thinking person should realize the Federal Government has been systematically under-reporting inflation since the early 1980’s in an effort to obscure the fact they are debasing the currency and methodically destroying the lives of middle class Americans. If inflation was calculated exactly as it was in 1980, the GDP figures would be substantially lower and inflation would be reported 5% higher than it is today. Faking the numbers does not change reality, only the perception of reality. Calculating real median household income with the true level of inflation exposes the true picture for middle class America. Real median household income is lower than it was in 1970, just prior to Nixon closing the gold window and unleashing the full fury of a Federal Reserve able to print fiat currency and politicians to promise the earth, moon and the sun to voters. With incomes not rising over the last four decades is it any wonder many of our 115 million households slowly rot and decay from within like an old diseased oak tree. The slightest gust of wind can lead to disaster.

Eliminating the last remnants of fiscal discipline on bankers and politicians in 1971 accomplished the desired result of enriching the top 0.1% while leaving the bottom 90% in debt and desolation. The Wall Street debt peddlers, Military Industrial arms dealers, and job destroying corporate goliaths have reaped the benefits of financialization (money printing) while shoveling the costs, their gambling losses, trillions of consumer debt, and relentless inflation upon the working tax paying middle class. The creation of the Federal Reserve and implementation of the individual income tax in 1913, along with leaving the gold standard has rewarded the cabal of private banking interests who have captured our economic and political systems with obscene levels of wealth, while senior citizens are left with no interest earnings ($400 billion per year has been absconded from savers and doled out to bankers since 2008 by Ben Bernanke) and the middle class has gone decades seeing their earnings stagnate and their purchasing power fall precipitously.

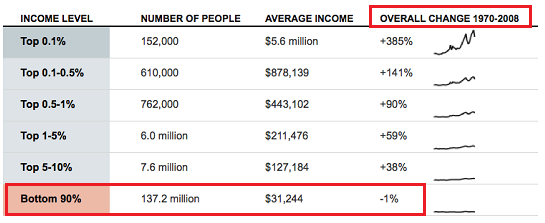

The facts exposed in the chart above didn’t happen by accident. The system has been rigged by those in power to enrich them, while impoverishing the masses. When you gain control over the issuance of currency, issuance of debt, tax system, political system and legal apparatus, you’ve essentially hijacked the country and can funnel all the benefits to yourself and costs to the math challenged, government educated, brainwashed dupes, known as the masses. But there is a problem for the 0.1%. Their sociopathic personalities never allow them to stop plundering and preying upon the sheep. They have left nothing but carcasses of the once proud hard working middle class across the country side. There are only so many Lear jets, estates in the Hamptons, Jaguars, and Rolexes the 0.1% can buy. There are only 152,000 of them. Their sociopathic looting and pillaging of the national wealth has destroyed the host. When 90% of the population can barely subsist, collapse and revolution beckon.

As I drove further along Ridge Pike we passed the endless monuments to our spiral into the depths of materialism, consumerism, and the illusion that goods purchased on credit represented true wealth. Mile after mile of strip malls, restaurants, gas stations, and office buildings rolled by my window. Anyone who lives in the suburbs knows what I’m talking about. You can’t travel three miles in any direction without passing a Dunkin Donuts, KFC, McDonalds, Subway, 7-11, Dairy Queen, Supercuts, Jiffy Lube or Exxon Station. The proliferation of office parks to accommodate the millions of paper pushers that make our service economy hum has been unprecedented in human history. Never have so many done so little in so many places. Everyone knows what a standard American strip mall consists of – a pizza place, a Chinese takeout, beer store, a tanning, salon, a weight loss center, a nail salon, a Curves, karate studio, Gamestop, Radioshack, Dollar Store, H&R Block, and a debt counseling service. They are a reflection of who we’ve become – an obese drunken species with excessive narcissistic tendencies that prefers to play video games while texting on our iGadgets as our debt financed lifestyles ultimately require professional financial assistance.

What you can’t ignore today is the number of vacant storefronts in these strip malls and the overwhelming number of SPACE AVAILABLE, FOR LEASE, and FOR RENT signs that proliferate in front of these dying testaments to an unsustainable economic system based upon debt fueled consumer spending and infinite growth assumptions. The booming sign manufacturer is surely based in China. The officially reported national vacancy rates of 11% are already at record highs, but anyone with two eyes knows these self-reported numbers are a fraud. Vacancy rates based on my observations are closer to 30%. This is part of the extend and pretend strategy that has been implemented by Ben Bernanke, Tim Geithner, the FASB, and the Wall Street banking cabal. The fraud and false storyline of a commercial real estate recovery is evident to anyone willing to think critically. The incriminating data is provided by the Federal Reserve in their Quarterly Delinquency Report.

The last commercial real estate crisis occurred in 1991. Mall vacancy rates were at levels consistent with today.

The current reported office vacancy rates of 17.5% are only slightly below the 19% levels of 1991.

As reported by the Federal Reserve, delinquency rates on commercial real estate loans in 1991 were 12%, leading to major losses among the banks that made those imprudent loans. Amazingly, after the greatest financial collapse in history, delinquency rates on commercial loans supposedly peaked at 8.8% in the 2nd quarter of 2010 and have now miraculously plummeted to pre-collapse levels of 4.9%. This is while residential loan delinquencies have resumed their upward trajectory, the number of employed Americans has fallen by 414,000 in the last two months, 9 million Americans have left the labor force since 2008, and vacancy rates are at or near all-time highs. This doesn’t pass the smell test. The Federal Reserve, owned and controlled by the Wall Street, instructed these banks to extend all commercial real estate loans, pretend they will be paid, and value them on their books at 100% of the original loan amount. Real estate developers pretend they are collecting rent from non-existent tenants, Wall Street banks pretend they are being paid by the developers, and their highly compensated public accounting firm pretends the loans aren’t really delinquent. Again, the purpose of this scam is to shield the Wall Street bankers from accepting the losses from their reckless behavior. Ben rewards them with risk free income on their deposits, propped up by mark to fantasy accounting, while they reward themselves with billions in bonuses for a job well done. The master plan requires an eventual real recovery that isn’t going to happen. Press releases and fake data do not change the reality on the ground.

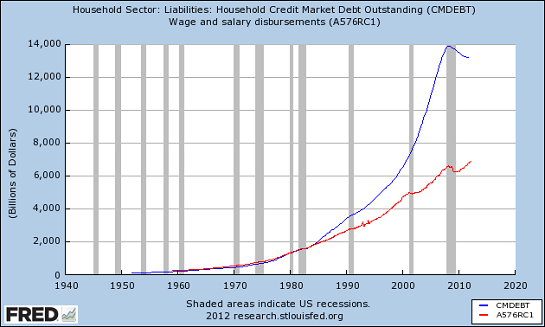

I have two strip malls within three miles of my house that opened in 1990. When I moved to the area in 1995, they were 100% occupied and a vital part of the community. The closest center has since lost its Genuardi grocery store, Sears Hardware, Blockbuster, Donatos, Sears Optical, Hollywood Tans, hair salon, pizza pub and a local book store. It is essentially a ghost mall, with two banks, a couple chain restaurants and empty parking spaces. The other strip mall lost its grocery store anchor and sporting goods store. This has happened in an outwardly prosperous community. The reality is the apparent prosperity is a sham. The entire tottering edifice of housing, autos, and retail has been sustained by ever increasing levels of debt for the last thirty years and the American consumer has hit the wall. From 1950 through the early 1980s, when the working middle class saw their standard of living rise, personal consumption expenditures accounted for between 60% and 65% of GDP. Over the last thirty years consumption has relentlessly grown as a percentage of GDP to its current level of 71%, higher than before the 2008 collapse.