“There is no means of avoiding a final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as the final and total catastrophe of the currency involved.” – Ludwig von Mises

The last week has offered an amusing display of the difference between the cheerleading corporate mainstream media, lying Wall Street shills and the critical thinking analysts like Zero Hedge, Mike Shedlock, Jesse, and John Hussman. What passes for journalism at CNBC and the rest of the mainstream print and TV media is beyond laughable. Their America is all about feelings. Are we confident? Are we bullish? Are we optimistic about the future? America has turned into a giant confidence game. The governing elite spend their time spinning stories about recovery and manipulating public opinion so people will feel good and spend money. Facts are inconvenient to their storyline. The truth is for suckers. They know what is best for us and will tell us what to do and when to do it.

The false storyline last week was the dramatic surge in new jobs. This fantastic news was utilized by the six banks that account for 80% of the stock market trading to propel the NASDAQ to an eleven year high and the Dow Jones to a four year high. The compliant corporate press did their part with blaring headlines of good cheer. The entire sham was designed to make Joe the Plumber pull out one of his 15 credit cards and buy a new 72 inch 3D HDTV for this weekend’s Super Bowl. When you watch a CNBC talking head interviewing a Wall Street shyster realize you have the 1% interviewing the .01% about how great things are.

What you most certainly did not hear from the MSM is that the NASDAQ is still down 42% from its 2000 high of 5,048. None of the brain dead twits on CNBC pointed out the S&P 500 is trading at the exact same level it reached on April 8, 1999. Twelve or thirteen years of zero or negative returns are meaningless when a story needs to be sold. On Friday the hyperbole utilized by the media mouthpieces was off the charts, leading to an all-out brawl between the critical thinking blogosphere and the non-thinking “professionals” spouting the government sanctioned propaganda. Accusations flew back and forth about who was misinterpreting the data. I found it hysterical that anyone would debate the accuracy of BLS (Bureau of Lies & Swindles) data.

The drones at this government propaganda agency relentlessly massage the data until they achieve a happy ending. They use a birth/death model to create jobs out of thin air, later adjusting those phantom jobs away in a press release on a Friday night. They create new categories of Americans to pretend they aren’t really unemployed. They use more models to make adjustments for seasonality. Then they make massive one-time adjustments for the Census. Essentially, you can conclude that anything the BLS reports on a monthly basis is a wild ass guess, massaged to present the most optimistic view of the world. The government preferred unemployment rate of 8.3% is a terrible joke and the MSM dutifully spouts this drivel to a zombie-like public. If the governing elite were to report the truth, the public would realize we are in the midst of a 2nd Great Depression.

The unemployment rate during the Great Depression reached 25%. Without the BLS “adjustments” the real unemployment rate in this country is 23%. Cheerleading and packaging the data in a way to mislead the public does not change the facts:

- There are 242 million working age Americans. Only 142 million Americans are working. For the math challenged, such as CNBC analysts, that means 100 million working age Americans (41.5%) are not working. But don’t worry, the BLS says the unemployment rate is only 8.3%. Things are going so swimmingly well in this country the other 33.2% are kicking back enjoying the good life.

- The labor force participation rate and employment to population ratio are at 30 year lows. The number of Americans supposedly not in the labor force is at an all-time record of 87.9 million. A corporate MSM pundit like Steve Liesman would explain this away as the Baby Boomers beginning to retire. Great storyline, but the facts prove that old timers are so desperate for cash they have dramatically increased their participation in the labor market.

- The data being dished out by the government on a daily basis does not pass the smell test. The working age population since 2000 has grown by 30 million people. The number of people working has grown by only 4.7 million. A critical thinker would conclude the unemployment rate should be dramatically higher than the reported 8.3%. But the government falsely reports the labor force has only increased by 11.8 million in the last eleven years. They have the gall to report that 17.9 million Americans just decided to leave the workforce. The economy was booming in 2000. It sucks today. Don’t more people need jobs when times are tougher? The Boomers retiring storyline has already proven to be false. The fact that 46 million (15% of total population) people are on food stamps is a testament to the BLS lie. A look at history proves how badly the current figures reek to high heaven:

- 2000 to 2011 – Not in Labor Force increased by 17.9 million.

- 1990’s – Not in Labor Force increased by 5 million.

- 1980’s – Not in Labor Force increased by 1.7 million.

- The Not in the Labor Force category is utilized to hide how bad the employment situation in this country really is. They conclude that 17 million out of 38 million Americans between the ages of 16 and 24 are not in the labor force. That is complete bullshit. From the time I turned 16, I worked. Everyone I knew worked. I worked through high school and college. It is a lie that 45% of these people don’t want a job. If you dig into their data, you realize the horrific state of employment in this country:

- 74% of 16 to 19 year olds are not employed

- 85% of black 16 to 19 year olds are not employed

- 31% of black 25 to 54 year old men are not employed

- 40% of 20 to 24 year olds are not employed

- 22% of 25 to 29 year old males are not employed

- 22% of 50 to 54 year old males are not employed

- According to the BLS, 11% of men between 25 and 54 are not in the labor force

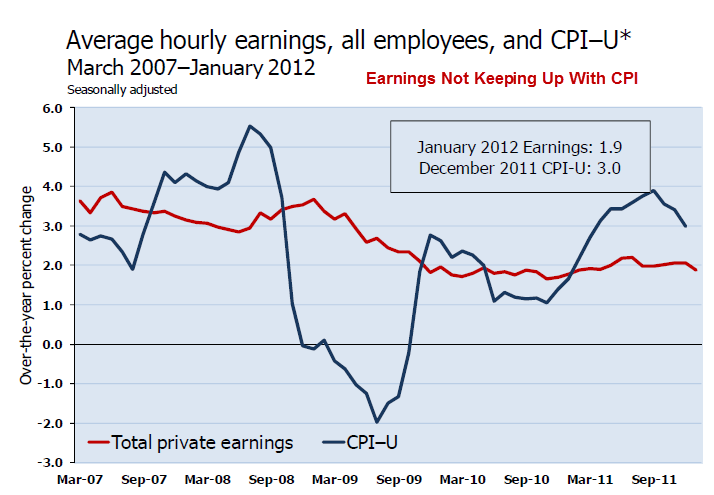

Not only is real unemployment at Depressionary levels, but those that do have jobs are falling further and further behind. Wages have gone up less than 2% in the last year and have been rising at an annual rate below 3% for the last four years. According to our friends at the BLS, inflation has risen 3% in the last year. This is almost as ludicrous as their unemployment rate. Anyone living in the real world, as opposed to the BLS model world, knows that inflation on the things we need to live has been rising in excess of 10%. It is a fact that if you measure CPI exactly as it was measured in 1980, at the outset of our great debt inflation, it exceeds 10% versus the fake 3% reported without question by the MSM to a non-thinking public. A poor schmuck making the median salary of $25,000 who gets a 2% raise thinks he has $500 more to spend when in reality he has lost $2,000 of purchasing power. Federal Reserve created inflation is an insidious hidden tax that destroys the 99%, while enriching the 1%.

Until Debt Do Us Part

“Insanity is doing the same thing, over and over again, but expecting different results.” – Albert Einstein

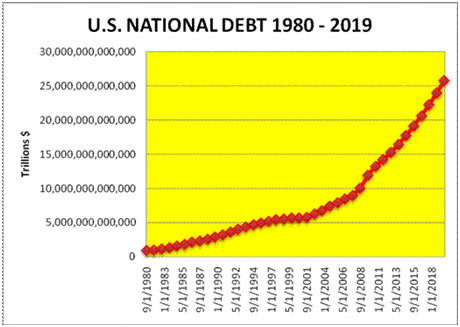

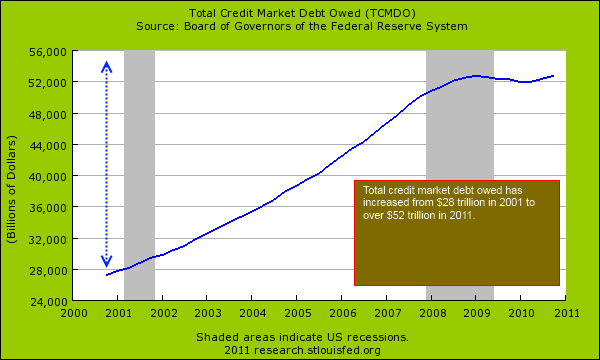

The recovery storyline being touted by the oligarchy of politicians, bankers and media is designed to make consumers feel better. This is a key part of their master plan. Any honest assessment of the financial disaster that struck in 2008 would conclude it was caused by too much debt peddled to too many people incapable of paying it back, too few banks having too much power, the Federal Reserve keeping interest rates too low for too long, and that same Federal Reserve doing too little regulating of the Too Big To Fail Wall Street mega-banks. I wonder what Albert Einstein would think about the “solutions” rolled out to fix our debt problem. Would he find it insane that total credit market debt has actually risen to an all-time high of $53.8 trillion, up $533 billion from the previous 2008 peak? Our leaders have added $6.1 trillion to our National Debt in the last four years, a mere 66% increase. This unprecedented level of borrowing certainly did not benefit the American people, as real GDP has risen by $96 billion, or 0.7%, over the last four years.

Would Einstein find it insane that the governing elite would encourage the 4 biggest banks, that were the main culprits in creating a worldwide financial collapse, to actually get bigger? The largest banks in the U.S. now control 72% of all the deposits in the country versus 68.5% in 2008. The Too Big To Fail are now Too Bigger To Fail. Rather than liquidating the bad debts, breaking up the insolvent banks, selling off the good assets to well run banks, firing the executives, and wiping out the shareholders & bondholders foolish enough to invest in these badly run casinos, the powers that be chose to protect their fellow .01% brethren and throw the 99% under the bus.

Ben Bernanke, in conjunction with Tim Geithner and his masters on Wall Street, implemented a zero interest rate policy designed to enrich the Wall Street banks, force investors into the stock market, and encourage Americans to borrow and spend like it was 2005 again. Rather than accepting that our economy has been warped for decades, with over-consumption utilizing debt as the driving force, and allowing a reset, the Federal Reserve insanely encouraging banks and consumers to do the same thing again. We do know Bernanke has stolen $450 billion of interest income going to savers and senior citizens and handed it to Jamie Dimon, Vikrim Pandit, Lloyd Blankfein and the rest of the Wall Street cabal. The “austerity is bad” storyline is pounded home on a daily basis by the politicians, corporate chieftains, Wall Street billionaires, and MSM pundits. The definition of austere is “practicing great self-denial”. Did you see the mob scenes on Black Friday? Americans are incapable of any self-denial, let alone great self-denial, and the masters of our country will not allow it to happen. One look at our GDP figures confirms the non-austerity occurring in this country. In 2007, prior to the collapse, consumer spending accounted for 69.7% of GDP. Today, consumer spending accounts for 71% of GDP, with investment accounting for 12.7% of GDP. In the good old days of 1979 prior to the epic debt bubble, when the financial industry do not run this country, consumer spending accounted for 62% of GDP and investment accounted for 19% of GDP. What an insane concept. You spend less than you make and save the difference. You then invest that money where you can get a reasonable return (.15% in a money market account is not exactly reasonable).

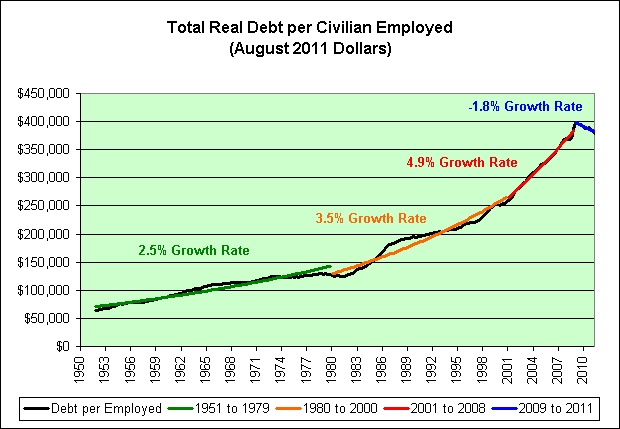

As Ludwig von Mises pointed out, a false boom created by credit expansion will ultimately collapse. We had the chance in 2008 – 2009 to voluntarily abandon the Wall Street induced credit expansion and allow our country to reset. The pain and misery would have been great, especially for the 1% who own most of the stocks, bonds and peddle the debt to the ignorant masses. As you can see in the chart below, the powers that be need debt per employed American to grow at an ever increasing rate to maintain their power and wealth. The miniscule reduction in debt from 2009 to 2011 was unacceptable. The governing powers will not be satisfied until von Mises’ final currency catastrophe is achieved.

Bernanke and his Wall Street puppet masters’ plan is actually quite simple. It’s essentially a confidence game. A confidence game (also known as a con, flim flam, gaffle, grift, hustle, scam, scheme, or swindle) is an attempt to defraud a group by gaining their confidence. The people who commit such tricks are often known as con men, con artists, or grifters. The con man often works with one or more accomplices called shills, who help manipulate the mark into accepting the con man’s plan. In a traditional confidence game, the mark is led to believe that he will be able to win money or some other prize by doing some task. The accomplices may pretend to be random strangers who have benefited from successfully performing the task. Bernanke and the 1% are the con men. They are attempting to defraud the 99% by convincing them their “solutions” will benefit them. The shills acting as accomplices are Wall Street bankers, bought off economists, politicians, journalists, and mainstream media pundits. You are the mark. The game has multiple facets but is based on more freely flowing low interest easy debt. The con man has reduced interest rates to zero at the behest of his puppet masters. The Wall Street accomplices offer enticing financing to the marks for big ticket items like automobiles, furniture and electronics. As the marks go further into debt, the Wall Street shills report record earnings ($26 billion from loan loss reserve accounting entries), consumer spending rises and GDP goes higher. The mainstream media accomplices dutifully report an improving economy. The government accomplices massage the employment and inflation data and declare a jobs recovery with no inflation. The marks are supposed to feel better about the future and spend even more borrowed money. This is what is considered a self-sustaining recovery by the psychopaths running this country.

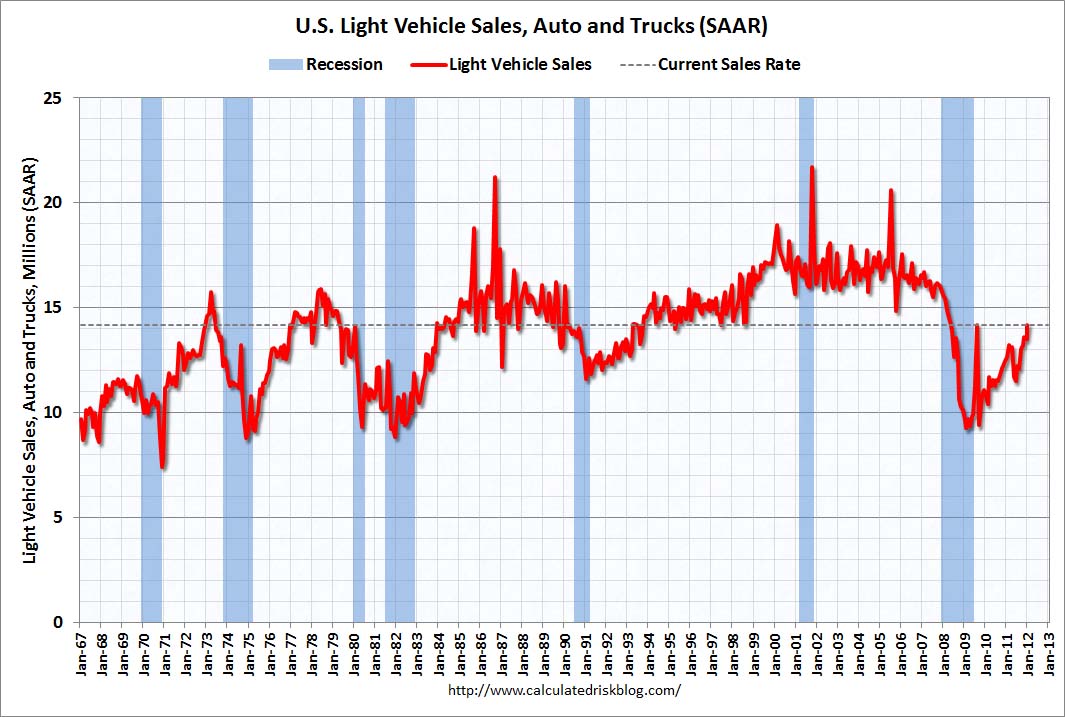

All you have to do is open your daily paper to see the confidence game in full display. Last week the MSM reported another surge in automobile sales. Our beloved American automobile manufacturers are back baby!!! Automobile sales are now pacing above 14 million on an annual basis. This is up from the depths of the recession in 2009 when the annual rate was below 10 million. We’ve breached the Cash For Clunkers level and there is nowhere to go but up. The storyline is that Obama was right to save GM and Chrysler with your tax dollars. They are now making splendid vehicles (except for the exploding Chevy Volts) and employing millions of Americans. This is a true American comeback success story. Clint Eastwood should do a commercial about it.

There is one little problem with this storyline. It’s bullshit. Remember GMAC? You bailed them out when all their subprime auto and mortgage loans went bad in 2009. They have a brand new business plan. Change your name to Ally Bank and start making as many subprime auto loans as possible. You will be happy to know that according to Experian, 45% of all auto loans being made today are to subprime borrowers. What could possibly go wrong? In addition, the average loan term has grown to almost 6 years. Executives at Ally Financial said that subprime car lending had become “very attractive” because profit margins on the loans more than cover the cost of expected losses from borrowers who fail to repay what they owe. I’m sure they have everything completely under control. Gina Proia, a company spokeswoman, said the company places “greater emphasis on the higher end of the nonprime spectrum” and only lends to people who show they can pay. I can’t believe they are restricting their loans to only people who they think can pay. I’m surprised Obama isn’t condemning them for such restrictive loan terms. If you open your paper to the auto section you will see financing offers of $0 down-payment, and 0% interest for 7 years across the board on most models. But why buy, when you can lease a luxury automobile for $300 per month? It is simply amazing how many vehicles you can “sell” when “credit challenged” Americans can rent them for seven years. I wonder if this explains why I see dozens of $40,000 luxury autos parked in front of $25,000 dilapidated hovels during my daily commute through West Philadelphia. It also seems the Big Three are “selling” a few extra vehicles to their dealers in January as pointed out by Zero Hedge. No need to let a few facts get in the way of a feel good story.

- Ford month-end inventory 86-day supply at end of Jan. (492k vehicles) vs 60-day supply (466k) as of Dec. 31

- Chrysler had 83-day supply (349k units) end of Jan. vs 64-day (326k units) as of Dec. 31

- GM month-end inventory 89-day supply (619k units) vs 67-day supply (583k) Dec. 31

The facts prove the issuance of billions in easy credit is creating the illusion of recovery. Non- revolving (auto & student loans) consumer credit outstanding is now at an all-time high of $1.7 trillion. Even with billions in bad debt write-offs since 2009 the amount outstanding has risen by $100 billion. Does this sound like austerity is gripping the nation? The Federal government is dishing out student loans like candy, as hundreds of thousands of students get worthless degrees from for-profit diploma mills like the University of Phoenix and its ilk. By keeping them occupied in school, the government is able to keep them in the Not in the Labor Force category. Not to be outdone, our friends at GE Capital, Wells Fargo and the other too big to fail entities have been doing their part on the revolving credit side of the scam. I’ve recently been seeing an ad by the largest U.S. furniture retailer, Ashley Furniture, offering 0% interest with no payments for 7 years. I don’t know about you, but my kids destroy a couch in less than 7 years. Wells Fargo Credit doesn’t seem too worried. A critical thinker might ask, how can Wells Fargo possibly make money offering these terms? But there is the rub. Ben Bernanke is loaning Wells Fargo money at 0% so they can perpetuate the confidence game. These insane bankers truly believe they can kick start this moribund debt saturated economy by issuing billions more in debt to people incapable of repaying them. Einstein would be amused.

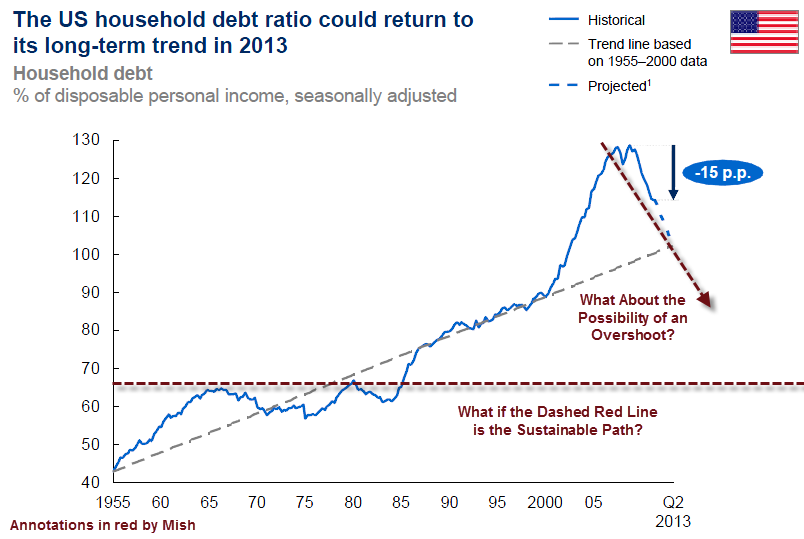

The McKinsey Group put out a report a couple weeks ago analyzing the amount of American household debt and optimistically concluding that it could be back on a sustainable path by 2013. Mike Shedlock pointed out that sustainable is in the eye of the beholder. It seems the bright fellows at McKinsey haven’t grasped the concept of regression to the mean. First of all their analysis is flawed because real disposable personal income is actually declining and Ben Bernanke’s master scam is working and Americans are now adding to their household debt. The little blue line has turned upwards since they gathered their data. Secondly, as Mish so accurately points out, the sustainable level of household debt is really at the levels prior to the debt bubble that began in the early 1980s. That is a debt level of approximately 70% of disposable personal income, as opposed to the current level of 110%.

The implications of household debt levels regressing to their long-term mean would be catastrophic to the 1%. Their kingdom of debt would come crashing down. Their power and wealth would be swept away. This is why it is so vital for them to create the illusion of recovery. Their confidence game is built upon an ever increasing flow of credit expansion. It will not work. There is no avoiding the final collapse of a boom created solely by credit expansion. Those in power will never voluntarily relinquish their grand game of pillaging the wealth of the nation, so economic collapse will be the ultimate result. They will continue to use propaganda, printing presses, and half-truths to further their agenda. But those who examine the facts will come to a logical conclusion that we are being sold a great lie.

“Half the truth is often a great lie.” – Benjamin Franklin

Why do the liars at the BLS have fudge the numbers? A better way to eliminate that nagging unemployment figure is to start a hot war. The bigger, the better.

Iran isn’t making nukes? Don’t worry. They’ll fabricate a hoax through the White House stenographers, otherwise known as the mainstream media. Or better yet, a false flag operation will get the rubes in flyover country hot and bothered about the towelheads under every bed plotting to kill us.

Once this con game is accepted, don’t be surprised if they re-instate a military draft. If you’ll remember, FDR had a similar problem of an imploding economy and millions out of work. Sending 12 million potential coffin-stuffers overseas had a way of putting a dent in the unemployment rate.

Don’t be shocked if Obama pulls the same trick. After all, there’s an election to be won. If countless innocent civilians are slaughtered in the process, it’s a small price to pay.

I doubt that the draft would be reinstated; I think there may be alot of people who aren’t going to stand for that (hopefully). BUT I find it interesting over the past week I’ve seen headlines about the troops coming home from Iraq and winding down Afghanistan. With unemployment so high right now what are they going to do with all those people coming home? Maybe redeploy them to Iran?

Of Two Minds – Charles Hugh Smith

What If We’re Beyond Mere Policy Tweaks? (February 6, 2012)

The nation’s ills cannot be fixed by thousands of pages of regulation or more policy tweaks. Only a profound cultural transformation can address our problems.

The mainstream view uniting the entire political spectrum is that all our financial problems can be fixed by what amounts to top-down, centralized policy tweaks and regulation: for example, tweaking policies to “tax the rich,” limit the size of “too big to fail” financial institutions, regulate credit default swaps, lower the cost of healthcare (a.k.a. sickcare), limit the abuses of student loans to pay for online diploma mills, and on and on and on.

But what if the rot is already beyond the reach of more top-down policy tweaks?

Continued at: http://www.oftwominds.com/blogfeb12/beyond-policy-tweaks02-12.html

Hey, I don’t see the big deal here. Just go with the flow, buy high, sell low…

After going back-to-school shopping with a student loan disbursement, I still felt like I was missing something…

I had the new sterling silver thumb ring, custom fitted… bling!

I had the surplus fatigues, draped over a Che shirt, capped with the cuban cap emblazoned with the Chinese Star… and even got some nice aviators… cheap, under $100…. Stylin!

Still, I had all this loan money so I finally remembered! Lap top! Fucking duh… so I was looking at a deal but I said “this won’t do… I need that 5,000 dollar Alien Ware I saw a classmate with. Cha Ching, bitchez!

THEN I saw 0% for 7 months on a dope lttle chebby. Done. No probs. I can cover the $300 with loan disbursments PLUS the minimum payment on the charge card for those DOPE 15” chromes and the system that says “booooom… boom boom….. boooom”.

What could go wrong, really? People are such negative Nancies sometimes. The way I see it, I’ll enjoy the semester, impress some hottties and when I graduate, I’ll pay it back at my leisure when I’m really making the scrilla.

What could go wrong? Buy high, sell low… that’s how you do it!

Colma giving HZK a run for the sarcasm champ of the day.

[img [/img]

[/img]

Great article Jim!

Where da hell you been, matt?

CORPORATE media doesn’t control what you think. THEY control what you’re allowed to think about. Pull the plug on your electronic toilet and tell all those CORPORATE media whores and their allegedly, reported somewhere, almost maybe, financial analysts, military consultants, security experts, and PhRMA funded white coat psychopaths that have been lying to you since the days of William Randolph Hearst to go stand in line at their local soup kitchen. Tell them to go beg Ted “The Turn Coat” Turner for some buffalo burgers. And if that compromising coward UN butt kisser won’t feed them they can go see that corporate bought, paid for and appointed, teleprompter reading illegal alien bastard imposter-usurper CEO of the bankrupt since FDR US Inc. occupyer of the white house in the district of corporatism and dig up some food from his wife’s communitarian garden.

Surf the net and youll run into lots o people who just love president Obama.

I dont like the dept,we need a more positive person who can put on a more positive act and who relizes the dept is killing the country

I find Mitt romney more optimistic and think his energy ideas cant help but be a step up.

Global Debt Crisis

The greatest private fraud of human history.

Who are the great fraudsters who are becoming the murderers of the human kind? How does the economy “illness” threaten Democracy and the freedom of people?

http://eamb-ydrohoos.blogspot.com/2012/01/global-debt-crisis.html

———————————

By knowing what happened in indebted Greece, where loan sharks created “bubbles” and the current inhuman debt, one can understand the inhuman plan in total …understand where this plan started just to bring all states at the same end …understand how this type of plans are established…

Authored by PANAGIOTIS TRAIANOU

I love this:

“When you watch a CNBC talking head interviewing a Wall Street shyster realize you have the 1% interviewing the .01% about how great things are.”

I can see that this won’t work. I think most of us(US) can. I just can’t see what keeps it going or when it will stop. In the meanwhile I buy gold and sit on cash, and I am getting so outraged by the banking system, I am constantly flirting with the idea of converting the majority to gold and digging a hole in the ground to stick it in.

(Why oh why are there no real alternative to the banking systems!! In this day and age, can’t one be devised, can’t an association of users not create their own?)

I have been expecting a crash for more than four years, and I still expect it. But they keep finding more rabbits in the hat, and I still have to figure out how the first one got in there. I know they are conning me, and cheating me out of part of my saving. Yet I still believe the trap can snatch closed faster than you can pull your money out of their ponzi scheme. And alternative investments are few unless you want to sit glued to the investment, in case it needs to terminated quickly to save you principal.

The game is rigged, the honest cry and the evil laugh. I don’t trust anyone any more.

When I got home last night I went through the mail and we had 4 credit card offers from the Too Big To Fail bankers.

The plan is being executed as designed by Ben and the boys.

The TBP comment stream is pretty lame. This article has 176 comments on ZH.

I received emails from Kunstler, Charles Hugh Smith, Jesse and Mish thanking me for sending it to them.

CHS is adding TBP to his recommended blogroll.

Soon, GEO [Wackenhut] and CCA will have created laws where those who dont pay off credit cards end up in jail until you, thru government expenditure, pay off your debt. Unfortunately a 100 dollar debt, minus prison owner profits, will take you about ten years,

Welcome to Laissez Faire!

Admin: What more is there to say?

Do your credit offers beckon you to go on vacation?

Colma

Admin and Avalon using our new credit card and doing our part to produce an economic recovery.

[img [/img]

[/img]

@Colma: I salute you! That was hilarious!! I had to shut the door of my office as I was giggling for about 20 minutes and my staff was getting worried that Dr. HZK was (finally) losing it.

Now, we want to see PICTURES of your big shopping spree. I am particularly interested in the thumb ring…..

What is your degree plan anyway?

How about the irony of me putting an advertisement to buy more shit at the end of an article about the stupidity of buying more shit.

@Admin:

OOOooo. I totally missed that. You sly dog. I thought it was kind of Google insert thingy on the site.

But most advertising goes completely over my head anyways. I have some kind of immunity to it, thanks God, sorry.

But I will make an effort to click on every single of your advertisers every time I visit the site as penance.

HZK

I only get paid when someone buys something. The ad at the top of the site is the only one that pays per click.

Mine says “Because SHE deserves it”, so I’m good with that.

And it’s shiny.

Hope:

Good question… the front office asked the same after over 200 units and a loan bill creeping on a quarter million.

RE: The TBP comment stream is pretty lame. This article has 176 comments on ZH.

95% of the 176 Zero Hedge comments do not even relate to the ILLUSION OF RECOVERY post.

That’s less than 10 valid posts vs close to close to 30 on this site. TBP wins this one by a long shot.

FTL

The Zero Hedgers do have a slight problem staying on topic.

But at least I get a chance to kick David Pierre in the balls.

Great article Jim. You have an uncanny ability to assemble facts and present them to us in a way that really displays the truth.

It is high time that America does stop living an illusion. Enough is enough. I don’t think even the MSM can fool the last bunch of Zombies much longer. This reality snow ball is way too big and way too far down the mountain now not to get noticed even by the left side blind bunch. How long can you contain something and keep it cloaked when it has grown this big? America’s failure plight is like a woman pregnant in her 4th to 5th month. She can only keep it covered and secret for so long. The best thing to happen is for a complete collapse back to the stone age and start from there. The bankers and politicians have screwed the American people, that’s a given. With their printing and corporate manuvers, they are also screwing the entire rest of the develped world. How long can one hive of jackels keep this game going on a scale this big? I believe we can all easily sense a moment coming called Checkmate.

Great stuff. I like how your writing is getting a little more edgy with every piece. So is Kunstler, and the stuff on ZH and DR I usually read. The anger is getting stronger as the MSM parrot’s bullshit is getting thicker by the day. And, sarcasm is a form of anger. And, anger turned inwards is Depression, which is worse than about anything. Let the MSM, Banksters, criminal politicians, lobbyists, Fed.gov.gestapo, entitlement parasites, and corporatocracy make you mad, and sooner or later they cause depression. Seen it on here and elsewhere. So, my advice, just stay as angry as you can, don’t let it turn to depression, keep writing and fighting!

AWD

I walk a fine line between anger and depression on a daily basis.

Let me tell you all about a tale of woe curtesy of Bank of America. (what else, after all?)

Back in December, my broker decided to stop sponsoring my VISA card.. I use the card to purchase everything, pay it off monthly and get a 2% cash back right into my brokerage account. Worked great for years.

Until the broker (Schwab) decides not to sponsor a VISA card and threw me into credit card Hell.

Well, it seems Bank of America wanted to step up to the plate and they grabbed my VISA sponsorship (without anyone letting me know about it), along comes a new card with a new set of rules, regulations, privacy notice shit and in very fine print at the bottom of the fifth page, they advise me of the new cash-back details. 1-1.5% depending on the time of day, the vendor you use, whether or not it’s raining – you know – clear as mud.

Plus, they do not tell you how to get your cash-back money anywhere in the letter.

So I call BOA and get a string of 4 (COUNT THEM ONE< TWO< THREE<FOUR) of the dumbest "Customer Service Executives" I have ever had the misery of talking too. Each one dumber than the one before and NONE of them could off any assistance other than the last one who offered to make a transfer for me. She did and nothing came out the other end (i.e. my brokerage cash account). I was told there were ways to set it up to automatically get the cash-back transferred to an account BUT it had to be an account of Bank of America!

What happens if you don't want it sent to a BOA account (of which I have none)? It seems that then you must call BOA (and speak to a "Customer Service Executive") every time you have the utterly huge amount of $25 in your cash-back mystery account and they will then do the transfer for you. Just like the first one that didn't transfer but left my "cash rewards" web page littered with error messages of "You have a failed transfer! Go to your Transfer Page to correct this! (By God right now) (emphasis mine).

When you go to the Transfer link, you find that every drop of information you provided is exactly what it should be except now, it shows that they've transferred $25 to my brokerage account and a second transfer of $25 "is pending". The total funds in the cash-back account continues to climb and is now $66 + change. They assure you that if a "transfer fails" (TA-TA-TA DUM) the funds will be credited to your cash-back account – I assume so they can try,try again.

So now I'm up to dumbass "Customer Service Executive" #7. This one can't even find the fucking web page where to look up what I'm having trouble with – much less fix it. Again, I asked to be transferred to someone who can answer questions. BUZZ, CLICK ring! ring! ring! ring! and so forth for 4 minutes (I checked it). When TA!-TA! the call was answered, a disembodied voice said, "Welcome to Microsoft Software Support! Due to a heavy call volume (of transferred BOA customers, no doubt) you're wait time will be in excess of 20 minutes."

At that point, I very carefully put the telephone back in its' stand, stretched and scared the shit out of my sweetie by screaming a death howl of First Class quality! Then I got a beer, popped a Xanax and started a book I've been wanting to read.

This is being written after booze and pill have taken affect and I must face the future of yet another call to one of thousands of stupid BOA's "Customer Service Executives". I would quit and write a letter but, damn, if they can't figure out their own stupid system how (for sure) can I know anyone there can read. And if I luck out and get a reader, how in Hell will they know who to give the letter too? Probably forward it to a "Customer Service Executive" who will then destroy it through ignorance or idiocy.

And that, friends and fellow TBP Bank of America lovers is where things stand at the moment.

I feel so much better now..

MA

@Admin-is-traitor: Feel free to use the above comment as a post on it’s own if you wish (and delete it as a comment). I will then continue to tell mirthful stories of glee and laughter as I continue to probe BOA (Bank of Assholes) orifices until it falls into post hell in a day or so…

MA

Student loan debt is approaching $1 trillion. People that think there are jobs available for people with a college education are willing to go into life-long student loan debt, many for POS degrees from U. of Phoenix and a hundred other bullshit “universities”. And Sallie Mae is there to collect all the interest on those that do have jobs and can actually pay it back. Oh, and if your not in enough debt already, get yourself a credit card from Sallie Mae…

[img [/img]

[/img]

Muck:

Their system was designed precisely for your wonderful experience…

Admin: ZH= good articles…. comments? Yaaaaawn.

Anger makes good fun, depression makes for great writing….

“depression makes for great writing….”

Or, Admin bailing yet again…

Credit VROOMs: Auto Loans in 30 Seconds

Three years ago, credit was so tight that the owner of a legal firm with a $400,000 salary and a very good credit score of more than 700 couldn’t get financed to buy the car he wanted from Michael Mosser’s dealership.

“The world is upside-down compared to then,” said Mosser, general manager of Chevrolet and Cadillac stores in Ann Arbor, Michigan. “Today, somebody with a 500 credit score, I can get approved and in a Malibu,” which starts at $22,110.

Lenders resisted extending credit to car buyers when the mortgage market collapsed in 2008, helping push General Motors Corp. and Chrysler LLC into bankruptcy and sending U.S. sales to the lowest point in almost three decades. Amid a slow housing market, auto demand is rebounding, spurring lenders from Bank of America Corp. to Capital One Financial Corp. to approve buyers faster and at better rates to compete for a piece of an expanding market.

“Banks have had to look elsewhere for growth opportunities, and auto has been one of the nice spaces over the last couple years,” Curt Beaudouin, a bank analyst for Moody’s Investors Service in New York, said in a phone interview. “The credit experience in terms of losses has been very good in recent times. It’s never gotten out of hand. Right now, it’s basically good for everybody in the industry.”

U.S. light-vehicle sales rose 10 percent to 12.8 million last year. That momentum continued as automakers sold cars and trucks in January at the fastest pace since the U.S. government’s “cash for clunkers” program in August 2009, according to Autodata Corp.

Capital One

Capital One boosted new-vehicle loan originations by 35 percent in the third quarter and 75 percent in each of the first two quarters of 2011 from the year-earlier periods, according to data provider Experian Automotive. That put Capital One ahead of Bank of America in market share for new-vehicle loan volumes and closer to Ally Financial Inc. and Wells Fargo & Co.

Capital One revamped a program for select dealers late last year that gives them perks such as faster approvals and exceptions for customers with borderline credit scores, said Kevin Borgmann, president of the McLean, Virginia-based lender’s auto-finance unit.

The company’s speed is “a big competitive advantage for us,” Borgmann said in a phone interview. Capitol One decides “the majority of applications for any dealer that does business with us within 30 seconds. Dealers find a lot of value in that because they can go out and sell the next car.”

Capital One is among several large banks creating dealer- specific programs to take advantage of a market with growing sales and still-low delinquency rates, said Melinda Zabritski, director of automotive credit for Experian Automotive.

Fast Decisions

“You’ve got pretty fast decisioning going on in the market,” Zabritski said in an interview. “When the market pulled back, the instant decisions really slowed down. You had more manual reviews. That’s one of the things you’re starting to see change is you’re going back to the automatic approvals. For a while, you really were only doing automatic declines.”

Lenders also are protected by a strong wholesale market, Zabritski said. Used-vehicle prices, which are near record highs because of short supplies, may increase 1.8 percent this year, according to Jonathan Banks, an analyst with the National Automobile Dealers Association’s Used Car Guide. Higher prices for used-cars reduce the loss a lender takes in the event of reselling a repossessed vehicle.

Faster decisions on auto-loan applications is “clearly something you would expect as credit becomes looser,” Don Johnson, General Motors Co.’s vice president of U.S. sales, said in an interview. “Consumers are deleveraging, their scores are getting better, so those automated systems logically should be turning more positive with more and more yesses.”

Aggressive Competitors

The ratio of borrowers who fall behind on their auto loans by 60 days or more will remain the same this year as 2011, according to TransUnion LLC. Delinquencies may have fallen to 0.51 percent at the end of last year, from their peak of 0.86 percent during the recession, TransUnion said in a report.

GM Financial, formerly known as AmeriCredit Corp., the subprime lender that GM acquired in 2010, has provided competition for Ally Financial, GM’s former financial arm under the name GMAC Inc. Wells Fargo also is “aggressively going after our dealers’ business,” Johnson told analysts and reporters on a Feb. 1 conference call.

Subprime borrowers are considered to be a higher-than- normal credit risk.

‘Almost Zero’

Ally, the top lender in new-vehicle financing this year, let its market share go to “almost zero” when liquidity dried up in 2008, Chief Executive Officer Michael Carpenter said in an interview.

“There were months in 2009 where our share of retail was zero because we simply couldn’t fund it,” he said. “If you roll the clock forward and get to the middle of 2010, we were back with higher share than we ever had as a captive” lender to GM.

AutoNation Inc., the largest retailer of new vehicles in the U.S., is forecasting U.S. auto sales will rise to about 14 million this year.

Mike Jackson, chief executive officer of the Fort Lauderdale, Florida-based company, said in an interview last month that available financing combined with better selection of cars from Japanese automakers and customers wanting to replace aging vehicles will spur demand.

The average age of U.S. cars and trucks has risen to a record 10.8 years, according to R.L. Polk & Co.

Contrast With Mortgages

“People pay for their cars before they pay for their houses,” Mike Maroone, Autonation’s chief operating officer, said in a phone interview. “They couldn’t afford to lose transportation because it ties right to their ability to work.”

Wells Fargo, JPMorgan Chase & Co. and Bank of America are among the lenders with whom AutoNation works most closely on financing customers with prime and near-prime credit, Maroone said. GM Financial has been among the most aggressive in lending to subprime borrowers, he said.

Bond offerings linked to automobile loans and leases, such as GM Financial’s $1 billion sale announced on Jan. 31, are set to dominate the asset-backed debt market for the fourth straight year in 2012, according to Wells Fargo Securities LLC estimates.

Sales of the securities may jump 11 percent to $63 billion this year, accounting for about 55 percent of bonds tied to consumer borrowing, the bank said. About $57 billion of bonds tied to auto debt were sold in 2011, or 54 percent of new deals.

The strength of the auto lending market differs from that of mortgages, where offerings of bonds without government guarantees backed by such loans may total just $5 billion this year, compared with peak originations of about $1.2 trillion in both 2005 and 2006, according to JPMorgan analysts.

No `Blank Check’

Ally, based in Detroit, has told investors it won’t file for an initial public offering until issues tied to faulty home loans are resolved and that it won’t give a “blank check” to its mortgage unit, which has teetered near bankruptcy.

Mosser, the Chevy and Cadillac dealer, said his daughter is struggling to buy a $105,000 condo. While she’s putting 20 percent down and he’s going in on the mortgage with her, it has taken more than 30 days for the bank to approve.

“I could walk out of this dealership in 20 minutes with a brand-new, $80,000 Escalade,” he said. “And you’re going from a car loan, which is somewhat unsecured, to a home, a property, which is secured. It’s kind of crazy.”

And poor decisions make for great stories.

Akanon:

You would cry…. my “Student Loan” story, while fictional, is based on a couple of characters who’ve made an appearance on the stage of life.

Basically, Mises and his genius horde were quite correct about easy money, distortions caused by such….

Keeping with Da Buddah, the disappointment following expectations…. the expectations of many, many Americans, will run deep. No logic will explain, no lessons will console. Only the specter of the “good life” will remain when masses are yet again suckered into the folly of over consumption.

a snip from Feb 7 5 Min. Forecast:

“America has turned into a giant confidence game,” says Jim Quinn, with his own take on the numbers.

Mr. Quinn is an interesting fellow: His passionate blog entries run counter to everything you’d expect from the director of strategic planning at an Ivy League business school.

“This fantastic news,” he writes, “was utilized by the six banks that account for 80% of the stock market trading to propel the Nasdaq to an 11-year high and the Dow Jones to a four-year high. The compliant corporate press did their part with blaring headlines of good cheer.”

“The entire sham was designed to make Joe the Plumber pull out one of his 15 credit cards and buy a new 72-inch 3-D HDTV for this weekend’s Super Bowl.”

“If the governing elite were to report the truth, the public would realize we are in the midst of a second Great Depression.”

The rise of the machines….sheesh

From Barnhardt

http://barnhardt.biz/

1. I tweeted this last night, but just have to post it here because it is . . . terrifying. This animated .gif is from Nanex, via ZeroHedge.com . Each frame in this animation is one trading day. The various colors are the 14 main electronic markets. The red is NASDAQ, the yellow is NYSE, etc. The color key is on the top-right. The x-axis (along the bottom) is the day session, beginning at 9:30am EST on the far left, and proceeding to the close at 4:00pm EST on the right. The y-axis (up and down) is the amount of trade volume of the high-frequency computer trading algorithms. The animation (time) is January 2007 through today. You can see the date scrolling in the very bottom-left of the frame.

First, note the evolution of the HFT trading itself. Next, notice what happens on August 5, 2011 and forward. 8/5/2011 is the day U.S. Treasury paper was downgraded to AA+ by the ratings agencies. [/img]

[/img]

When I say that the markets are a total smoke-and-mirrors farce, do you understand what I am saying now? All of the PEOPLE are gone. The entire edifice is just these computers trading in-and-out with each other all in a matter of microseconds, over and over again. None of it is real. And the futures markets are exactly the same. The people have been either leaving or have been forced out, or raped. Get out, get out, get out, get out, get out.

[img

but other then all that the economy is getting better

mjl

“Of all the contrivances for cheating the laboring classes of mankind, none has been more effective than that which deludes them with paper money.”

— Daniel Webster

Bend over America. Old Blowhard will continue to deliver the good news to you until you figure it out and stand up. Wake up ans smell the strong BS. VOTE THE SWINE OUT OF OUR GOVERNMENT AND END THE FED!!!

Jim

Great work. Are your sons in tune with your blog? Do they read it and know how you feel? (I have 3 sons as well, my oldest going to college next year maybe Penn State). How would you keep them optimistic in the light of such relevant facts? It seems that the normal stages of resentment, anger, depression, apathy could come into play. You’ve done a fantastic job of outlining the very real and unavoidable problem. Now what’s the solution? The goal has always been: go to a good school, get a degree in finance, and work for one of the too big to fails. That would be even more inronic than an ad to sell more shit you don’t need at the bottom of your work, if your sons went to work at JP morgan or goldman sachs!

I agree with all your works, but really feel bad about encouraging my oldest son who is brilliant (missed 1 question on math sat) to go into business/finance. Any suggestions for a fellow father wanting to guide young brilliance to a productive career?

Thanks and keep up the great work.

Neurogain

My oldest son (at Penn State) reads my articles. My other two sons get to hear their father rant at the TV. We talk quite a bit about their futures. It sounds like your son is brilliant. There will always be opportunities for smart hard working people in this world. He should stay as far away from Wall Street as possible. He should just study hard and have a good time in college. No need to worry about things you or he can’t control.

IF I WAS YOU GUYS (AMERICAN) I WOULD WORRY MORE ABOUT YOUR LIBERTY.

SOON THEY WILL EVEN STOP YOU RELEASING ARTICLES SUCH AS THE EXCELLENT ONE ABOVE.

THEY KNOW WHAT’S COMING .THEY KNOW IT’S ALL BULLSHIT.

THEY KNOW THAT BY THE TIME THE 99.9% HAVE FIGURED IT OUT THEY WILL BE COMPLETELY POWERLESS TO DO ANYTHING ABOUT IT.

YOU DON’T EVEN HAVE DEMOCRACY…YOU CAN CHOOSE ANY POLITICAL CANDIDATE EVERY FOR YEARS AS LONG AS THEY’RE ONE OF THE TWO PARTIES WE HAVE PRE-CHOSEN FOR YOU.

IT’S PATHETIC.

SAD THING IS BRITAIN IS GOING THE SAME WAY.

TRUST NO 1:

STOP SHOUTING YOU COCKNEY HOOLIGAN!!!

front page link and excerpt on infowars.com

My other two sons get to hear their father rant at the TV -Admin

Dont have a grandson with a dog collar

So many articles, so many comments, but little to no input as to how to be prepared for the inevitable. Move out of the country, where to? I have 3 single daughters in all in their twenties I could never leave otherwise I would be out of here! I have invested heavily in Silver Eagles and junk Silver, have a large garden, stocked up on 6 months worth of food, purchased a 7500 watt generator that can run on gasoline, LP, or Natural Gas. I now own 2 pistols, a shotgun, 2 rifles and am buying ammo big time because when gas goes up this summer so will ammo….but yet I still feel unprepared. Wish I had more resources to do more. I hope you an others can offer those that want to prepare real advice on what to do….there is so little being written in this regard!

AWV its my thunk that peaceful protest, actions, to point out the corruption, is a way to nullify the historical wave of class war. Peaceful revolution.

I dont want anyones Mcmansion. I dont want Dimons IOUs. I dont want Drones.

I want to be left alone. I dont want political and pundit spin. I dont want war, I have nothing to gain from it. I dont need high tech jets. I dont need spyware on my computer. I dont need a government that passes moral laws while ignoring moral laws. I dont want many of the things that tax dollars pay for, today.

So what do you suggest we do, anyone? Personally to get out of the immediate loan crisis and dependance on China, install a federal VAT tax of 4.99% on all imported goods. In Sweden where I now live this is 25%! A lot but ´no national or extremely small, 1%, debt. I think that what US shall do. And then there is noo global law that all debts shall be paid. In the a historical past these were ignored, (often followd by wars of course) but they were written off after the American revolution for example. Britain could not do anything, just look on. Maybe we shall have the Chinese do the same, just look on….!? France has always been debt ridden for the last 300 years, and always got out of it somehow!

Humor, of sorts, as received from a reader. Obviously this was inspired by the famous Abbott and Costello baseball sketch Who’s on first? Never mind that it is funny. It explains perfectly how the unemployment rate has been dropping.

COSTELLO: I want to talk about the unemployment rate in America .

ABBOTT: Good Subject. Terrible Times. It’s 9%.

COSTELLO: That many people are out of work?

ABBOTT: No, that’s 16%.

COSTELLO: You just said 9%.

ABBOTT: 9% Unemployed.

COSTELLO: Right 9% out of work.

ABBOTT: No, that’s 16%.

COSTELLO: Okay, so it’s 16% unemployed.

ABBOTT: No, that’s 9%…

COSTELLO: WAIT A MINUTE. Is it 9% or 16%?

ABBOTT: 9% are unemployed. 16% are out of work.

COSTELLO: IF you are out of work you are unemployed.

ABBOTT: No, you can’t count the “Out of Work” as the unemployed. You have to look for work to be unemployed.

COSTELLO: BUT THEY ARE OUT OF WORK!!!

ABBOTT: No, you miss my point.

COSTELLO: What point?

ABBOTT: Someone who doesn’t look for work, can’t be counted with those who look for work. It wouldn’t be fair.

COSTELLO: To who?

ABBOTT: The unemployed.

COSTELLO: But they are ALL out of work.

ABBOTT: No, the unemployed are actively looking for work… Those who are out of work stopped looking. They gave up. And, if you give up, you are no longer in the ranks of the unemployed.

COSTELLO: So if you’re off the unemployment roles, that would count as less unemployment?

ABBOTT: Unemployment would go down. Absolutely!

COSTELLO: The unemployment just goes down because you don’t look for work?

ABBOTT: Absolutely it goes down. That’s how you get to 9%. Otherwise, it would be 16%. You don’t want to read about 16% unemployment do ya?

COSTELLO: That would be frightening.

ABBOTT: Absolutely.

COSTELLO: Wait, I got a question for you. That means they’re two ways to bring down the unemployment number?

ABBOTT: Two ways is correct.

COSTELLO: Unemployment can go down if someone gets a job?

ABBOTT: Correct.

COSTELLO: And unemployment can also go down if you stop looking for a job?

ABBOTT: Bingo.

COSTELLO: So there are two ways to bring unemployment down, and the easier of the two is to just stop looking for work.

ABBOTT: Now you’re thinking like an economist.

COSTELLO: I don’t even know what the hell I just said

End Neoeconomics – Embrace Geoeconomics

“Don’t forget to bookmark and share”

Simple introduction

http://www.henrygeorge.org/isms.htm

Origins of our “crisis”

http://www.amazon.com/Corruption-Economics-Georgist-Paradigm/dp/0856831603?tag=duckduckgo-d-20A

Professor Mason Gaffney speaks “The Corruption of Economics”

http://www.wealthandwant.com/docs/Gaffney_Intro_TCOE.html

His suggested Policy Fixes.

http://www.amazon.com/After-Crash-Designing-Depression-free-Economic/dp/1444333070/ref=sr_1_1?s=books&ie=UTF8&qid=1328707968&sr=1-1

http://libertyrevival.wordpress.com/2011/01/09/ending-poverty-and-political-turmoil/

Professor Michael Hudson

http://www.cooperativeindividualism.org/hudson-michael_theory-of-rent-needs-theory-of-history.html

Usufrunct Explained

http://en.wikipedia.org/wiki/Usufruct

– On the Monetary System –

American Monetary institute

http://www.monetary.org/

Critique

http://libertyrevival.wordpress.com/?s=monetary

http://useconomy.about.com/od/monetarypolicy/p/gold_history.htm

Silvio Gesells Natural Money

http://www.mindcontagion.org/worgl/worgl2.html

https://secure.wikimedia.org/wikipedia/en/wiki/Demurrage_%28currency%29#

Professor Ingo Bishoff – comparing and contrasting Georgist and Libertarian thought

http://www.thedailybell.com/503/Ingo-Bischoff-Henry-George.html

Critiques by CHM

Beyond policy tweaks?

http://www.oftwominds.com/blogfeb12/beyond-policy-tweaks02-12.html

The Paradoxes at the Heart of the “Progressive” Project

http://www.oftwominds.com/blogmar11/faux-progressive3-11.html

The Paradoxes at the Heart of the “Conservative” Project

http://www.oftwominds.com/blogmar11/faux-conservative3-11.html

Back to our simple model

http://www.henrygeorge.org/isms.htm

AWV Re advice on what to do, or rather food for thought in that regard

Two sources

TheTexasRing.com Article on Preparing a plan

allencurrie.ca Free read of a novel written as Orwell wrote ‘1984’ when he observed a trend in the ’40s and said if this trend continues the world will look like this in 1984. Then set his protagonist down in this world and watched. His forecast was chillingly near reality today. Haven’t seen a negative comment on the novel yet.

A lot of these articles start to look the same. You would have to be about brain dead to beleave the reports about the economy.Giant propaganda for the government,it should about be sickening just before the elections.

You never dissappoint Admin, nicely done.

Couple things to add.

The BLS figures the cost of employer paid health insurance in that “hourly” wage number. In 2002, my employee (and my own) health insurance ran about $200 a month. $200 a month X 12 = $2400. $2400 divided by the normal “full time” employment hours (2080 annually, unless you have a government job) means that in 2002 we should subtract a little less than a buck an hour from the “wages” figure to find a more accurate WAGE number.

Today, employee insurance (including the new 1.5% damn tax on it) is over $560 a month. $560 x 12 = $6720 a year, or $3.24 an hour.

Tell me again how much better off we are?

If this is a recovery, then the next “downturn” looks to be a real bitch.

Fiat on.