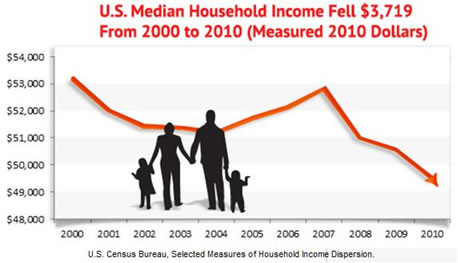

When I read stories like the one below and the information about how much people have saved for their retirement, I’m flabbergasted by the delusional, utterly ridiculous behavior of American consumers. We know for a FACT that 60% of all workers in the country have less than $25,000 of total savings. Many have absolutely nothing saved. Even better, over 25% of all 401k participants have borrowed against their 401k plan as of the end of 2010. This data is for people with jobs. How about the 88 million people who aren’t in the labor market? I wonder how much savings they have. In order to retire at 65 and live above the poverty line, people need to have saved at least a couple hundred thousand dollars. Those who retired in the 1980s and 1990s had equity in their homes, many had defined benefit pensions, and could rely on Social Security and their savings.

Today you have 55 year old people with $25,000 of liquid assets earning .15%, underwater homes, no pension plans, and $15,000 of credit card debt. They cannot afford to retire. They will stay in the labor market until the day they die. This is not good news for the Millenials.

What I find incomprehensible is that Americans ramped up their spending in the 1st quarter of 2012 and their savings rate in back at a four year low of 3.9%. With the data about retirement savings being so pitiful consumers SHOULD BE saving 10% of their disposable income like they did in the early 1980s. Going further into debt in order to enjoy going out to dinner two times per week is about the stupidest thing anyone could do. And our leaders, media and Ivy League trained economists actually encourage this delusional foolish behavior. Can this many Americans be this stupid? What are they thinking? Are they counting on the government to come to their rescue when they are 75 years old, broke, homeless, and begging?

I find myself shaking my head and talking to myself when I see this data and watch the behavior of the majority. We’re surely doomed.

Delaying retirement: 80 is the new 65

NEW YORK (CNNMoney) — A quarter of middle-class Americans are now so pessimistic about their savings that they are planning to delay retirement until they are at least 80 years old — two years longer than the average person is even expected to live.

It sounds depressing, but for many it’s a necessity. On average, Americans have only saved a mere 7% of the retirement nest egg they were hoping to build, according to Wells Fargo’s latest retirement survey that polled 1,500 middle-class Americans.

While respondents (whose ages ranged from 20 to 80) had median savings of only $25,000, their median retirement savings goal was $350,000. And 30% of people in their 60s — right around the traditional retirement age of 65 — that were surveyed had saved less than $25,000 for retirement.

As a result, many people aren’t in a hurry to quit their day jobs.

Three-fourths of middle-class Americans expect to work throughout retirement. And this includes the 25% of Americans who say they will “need to work until at least age 80” before being able to retire comfortably.

The 2012 Retirement Confidence Survey: Job Insecurity, Debt Weigh on Retirement Confidence, Savings

March 2012 EBRI Issue Brief #369 Paperback, 36 pp. PDF, 1,585 kb Employee Benefit Research Institute, 2012

Executive Summary

- Americans’ confidence in their ability to retire comfortably is stagnant at historically low levels. Just 14 percent are very confident they will have enough money to live comfortably in retirement (statistically equivalent to the low of 13 percent measured in 2011 and 2009).

- Employment insecurity looms large: Forty-two percent identify job uncertainty as the most pressing financial issue facing most Americans today.

- Worker confidence about having enough money to pay for medical expenses and long-term care expenses in retirement remains well below their confidence levels for paying basic expenses.

- Many workers report they have virtually no savings and investments. In total, 60 percent of workers report that the total value of their household’s savings and investments, excluding the value of their primary home and any defined benefit plans, is less than $25,000.

- Twenty-five percent of workers in the 2012 Retirement Confidence Survey say the age at which they expect to retire has changed in the past year. In 1991, 11 percent of workers said they expected to retire after age 65, and by 2012 that has grown to 37 percent.

- Regardless of those retirement age expectations, and consistent with prior RCS findings, half of current retirees surveyed say they left the work force unexpectedly due to health problems, disability, or changes at their employer, such as downsizing or closure.

- Those already in retirement tend to express higher levels of confidence than current workers about several key financial aspects of retirement.

- Retirees report they are significantly more reliant on Social Security as a major source of their retirement income than current workers expect to be.

- Although 56 percent of workers expect to receive benefits from a defined benefit plan in retirement, only 33 percent report that they and/or their spouse currently have such a benefit with a current or previous employer.

- More than half of workers (56 percent) report they and/or their spouse have not tried to calculate how much money they will need to have saved by the time they retire so that they can live comfortably in retirement.

- Only a minority of workers and retirees feel very comfortable using online technologies to perform various tasks related to financial management. Relatively few use mobile devices such as a smart phone or tablet to manage their finances, and just 10 percent say they are comfortable obtaining advice from financial professionals online.

Life expectancy is 78, but 25% of Americans think they’ll need to work until 80 in order to retire comfortably.

This is Delusion with a capital D. Who is going to employ drooling doddering old fools like DaveL when they are 75 years old and racked with incontenance?

I’m also flaccid.

Not really surprising. In this area retire just means from a 9-5 job. Almost everyone I know works until 70 and then relies on family to help support them.

Yeah I know, anecdotal evidence is anecdotal….

Anyway, the evidence supporting my belief that people are idiots continues to pile up.

“What I find incomprehensible is that Americans ramped up their spending in the 1st quarter of 2012 and their savings rate in back at a four year low of 3.9%.”

When you’ve spent most of your life eating filet mignon, it’s hard to stick with hamburg for very long. But, if you(me) spent most of your life eating hamburg, you get to retire and dine on filet mignon. Dumbfuck is as dumbfuck does. And I don’t need to be employed or take Viagra either.

[img [/img]

[/img]

Fuck you all.

I just paid off my $18,000 credit card bill with spare change from my cushions.

We’re all happy for ya Dave. John

bluestem

That’s not nice. The poor guy is flaccid and you’re happy for him?

Admin you must of had a good job or retired before 08. Ive only met a dozen people in my life that have a payed for home.And now its even harder.Would you put serious money in the stock market for your retirement?

If your amazed by all the poor people with no retirement money your out of touch.

ron

You bet your ass I’ve had good jobs. I worked my ass off in school, worked my ass off to get my CPA. Worked my ass off going to school at night after work for 3 and a half years to get my MBA. And I’ve been an excellent hard worker my whole life. I put money in 401k plans since I was 25 years old, maximizing my savings. I drive my cars into the ground. I have never in my life carried a credit card balance because I have never spent more than I made.

Don’t give me sob stories about the poor Boomers. My parents paid off their house. It’s not hard if you just make the payments and don’t borrow against the equity.

I’m amazed at the complete and utter stupidity of millions of morons in this country.

Maybe 4 decades of living on the edge of just getting by has driven the heard totally mad ?

..and we all believed the economy was growing.Little did we know that we were being sucked into a black hole created by debt inflated currency.

[img]http://blog.bmgbullion.com/wp-content/uploads/2.01.12_Real-Average-Weekly-Earnings.jp[/img]

“The utter failure of our government controlled educational system in teaching our children how to think critically or question the validity of government created data has allowed the elite to paper over the fact the average American worker has not had any real income gains in at least four decades. The insidious nature of Federal Reserve created inflation (up 600% since 1970) is incomprehensible to a public that finds math boring and not essential in their lives.”

~ James Quinn

[img [/img]

[/img] [/img]

[/img]

[img

See how fast the tanks and military would rush out when for example 50 000 workers would

unite and demand a 200% wage increase.

The system was fucked up from day 1.

It’s moral coercion backed up by physical force.

Very basic.

I’m a first stage boomer. My retirement plan was set when I graduated from university: reach 65 with a wholly-owned home and a property that would support small-scale self-sufficient agriculture. I have that property (in South America) and on it is another house now occupied by my son and his fiancee. There is not real dividing line between us on who owns what, whose money is whose: we pool resources. I live an austere life by choice. Like Admin, I have never had credit card debt save for the first semester of boarding school for my son, who began at 13, a year earlier than planned. I have a twelve year old car and plan to keep it till it drops. I am scheduled to collect SocSec this year, but it will be a small sum and I will not depend on it in any case. I have no debt and neither does my son, who works down here and is very well paid. I will “earn my keep” with the kids by providing supplementary education, etc., for grandchildren we all hope will come, and by my farming activities and a small income from writing. Meanwhile, my relatives and friends who had very highly paid work do not enjoy a life nearly as comfortable as mine, and they have worries I do not. It’s all a question of priorities and, I suspect, of mastering the vital art of delayed gratification.

Oscar – Amen

Here is an example of how stupid most people are about money, planning and delayed gratification. I bring my lunch to work 9 out of 10 days. It is usually leftovers from dinner the night before. I meet my buddy every couple weeks and we get a couple slices of pizza and a drink for $7.

The people in my office, most who make less money than me, eat out for lunch every day. They will spend $1,650 or so per year eating lunch. I’ll spend $150 per year. I will save the $1,500 difference and over 20 years that savings will grow to $50,000 if I can make a small return. The story above says that 60% of workers have less than $25,000 of savings. Just by bringing their lunch to work they could have $50,000.

This exact scenario can be played out on a larger scale with cars. I buy a car, pay it off in three years and drive it for 10 or 12 years. I save the car payment for 7 to 9 years while morons lease BMWs and Lexuses for eternity so that people think they are successful. These are the people who are 50 years old with no savings and debt up to their eyeballs.

We’re a nation of materialistic delusional morons.

Why should they save? Intrest paid on the savings is 0.15%. Annual inflation is somewhere between 2% and 12% depending on who you want to quote. So every year that you save it you lose. Buy assets that you can use and then e-bay to fund retirement and you are way ahead. Inflation gets worse every year. Saving is for suckers.

WTF are you going to buy assets with?

If you spend your dollars on lunches and leases you won’t have it to buy gold and silver.

I weep for humanity when I read some of the comments on this site.

The idea of not saving in cash and instead purchasing productive assets is one that makes sense to me once one has the essentials covered. Some cash should be always be kept on hand, I believe; the amount varies with the individual and with circumstances. The nature of my son’s work is such that he is able to save a large portion of his salary. Some of the savings is going into a phased-growth silvopasture plantation on owned-outright land. Some goes into ag machinery to be operated by relatives. Some goes into small-scale projects like a brick-making operation, a machine shop, etc. If I read CT’s comment right, his idea is to buy things that will go up in price at a percentage higher than interest or stock market growth. That might not be so bad an idea, because a soldering machine I bought five years ago now retails for triple what I paid for it!

If I misread CT, then Admin and I will weep together. If prudence does not make a comeback, the future for posterity is one I prefer not to contemplate.

“I will save the $1,500 difference and over 20 years that savings will grow to $50,000 if I can make a small return.”

After working and saving, working and saving, working and saving and after twenty years——- you end up with $50,000. That’s all well and good and quite commendable. The problem is that your $50,000 will only buy about $12,500 worth of stuff.

That is $12,500 more than the idiots who saved nothing can buy.

The $50,000 is from bringing my freaking lunch to work.

Driving cars for 10 or 12 years adds another $200,000 to that figure.

I love to see the comments from people who didn’t live beneath their means and try to rationalize why they are fucked.

It’s actually pathethic.

“I didn’t save because inflation would have eaten away at my savings, so I went out to dinner three nights per week, leased fancy cars, borrowed against the equity in my house, bought 5 HDTVs for every room in my house, and went on nice vacations every year.”

Mantra of a Moron

Idiots who made a conscious choice to spend more than they made and now try to rationalize why they haven’t saved a fucking dime.

[img [/img]

[/img]

Delusion of Americans and the size of their houses. As Mencken said, you deserve to get it good and hard.

[img [/img]

[/img]

Im fine with my siuation.I

Pressed wrong button,anyhow your just not in touch with most americans who didnt do as well as you.

Must be great being perfect.

ron

Yeah. I was born with a silver spoon in my mouth in a 900 sq ft row home to a truck driver and a stay at home mom.

I’m tired of the excuses from people who didn’t work hard and didn’t save enough. Bullshit.

Eh, I’m guilty of eating out too much. Not for lunch, but for dinner.

It costs me a lot, but me and my wife are working on changing it. College got us used to a steady diet of insta-food, and we suck at cooking for two.

“Administrator says:

bluestem

That’s not nice. The poor guy is flaccid and you’re happy for him?”

No Jim, he’s just as dumb as you for believing I wrote that.

Ron,

[img [/img]

[/img]

How dare some of you come on here and boast about how you work hard and save for retirement or are now fairly comfortable in retirement from doing so. You are just a bunch of fuckers who say “I’ve got mine and fuck the rest of you”.

That’s the way it works on this site.

So instead of renting a room to save more, I should just keep renting a place of my own?

Instead of driving a beater, I should get a big ol’ pick m’ up on a 7 year no-interest loan?

Instead of letting the roomies cook me splendid feasts, I should sit down to a steak every night?

Consider this: Isn’t NOT saving much more energy intensive than saving?

This is a thread that llpoh would drop some logic on.

Pigs and squirrels.

Admin says

I’m tired of the excuses from people who didn’t work hard and didn’t save enough. Bullshit.

Admin it’s too late the boomers did not save enough and time is up. The more salient question is; what is it going to look like going forward? Who will feed and care for 77 million boomers, what’s the free shit army (50 million strong) going to do when the free shit faucet is turned off, that my friend is the most critical question facing us today. Run a little risk analysis over that, I would be willing to bet they don’t just go back to work all peaceful like, the molotov cocktail will be their instrument of protest. A few hundred youth and a few gallons of gasoline and wreak havoc that’s unstoppable.

Just sayin

sensetti

The future is not bright. I have no solutions. It’s too late. Good luck.

Did I mention that I was a teacher? I taught my students how to spell their names for 30 years. Now I collect a government gold plated pension as a parasite in the intestines of America. I got mine. Fuck those kids. They just interrupted my 6 hour days, 9 months of work, and 30 days off during the school year.

Admin:

Yeah, thats what I was afraid you would say.

Hide

Hide [/img]

[/img]

[img

I just got throttled, Word Press alert appeared on the laptop and stated, Slow down you are posting to fast. That never happened before.

WPES

@ ron, who said, “Admin you must of had a good job or retired before 08. Ive only met a dozen people in my life that have a payed for home.And now its even harder.Would you put serious money in the stock market for your retirement?”

My story mirrors Admin’s. For the last 20 years prior to retirement, my wife and I maxed out everything we legally could set aside in our retirement accounts. We collapsed a 30 year mortgage to 15 years and paid it off in 13, resulting in a big, fat check to us when we sold the house…..enough to build a brand new retirement home with no mortgage. No debt EVER, including the cost to put a son through college.

The federal government could default on Social Security and my pension check, and we’d still have enough to live comfortably off our retirement savings. And yes, we’ve got really serious money in the stock market. Mostly VERY SAFE preferred common stock (think utility companies) that pays 6-7% interest.

It can be done. The watchword is discipline.

Saving for retirement implies a long term belief in the system. That things will be better years from now and you will be able to kick back and live fat and easy. That the value of what ever you have saved will be equal to or greater than the value that it has now. The savings rate is going down because the people can see that the old ways no longer apply. You want to save now, spend it like you got it. Funds are flowing out of stocks and into guns, food and supplies. Farm land is a savings that you can use, eat off of, and then sell when you are too old to work. I would never put money back into stocks or the bank so that they could clean me out like Corzine did to his customers. Saving is for suckers

Savings rate is going down because idiots are whipping their credit cards out to buy iPhones and eat out at Cracker Barrel.

The only way to get ahead in life is to spend less than you make and save the difference.

Only people who haven’t saved a fucking dime in their lives says saving is for suckers. It is nothing but idiots rationalizing their utter stupidity.

I gotta go with admin on this. In 1999 I bought an old 1986 4Runner for $1500. During the next 12+ years I paid myself $600 each month which is roughly what a car payment would have been. I’m still driving that 26 year old car today. I’ve used the $$$ saved to pay down debt, put a roof on my house and buy things that will ease my transition from this fucked up economy to whatever comes next. Live below your means and you will be amazed at how well things work out for you. Live large and you end up like most Americans……slaves to debt, spending your income to “make payments” and financing the rest with credit cards and equity loans. Reap what you sow idiots.

I_S

@ CavTanker, who said, “Saving is for suckers.”

I disagree. Your line of thinking is precisely the reason why government benefits programs have gotten out of control and created so much debt…………….supporting millions of irresponsible, lazy people who won’t get off their fat ass and try to do for themselves.

Another story. My golfing buddies are nearly all millionaire Silents and hard working, self-made success stories. And every single one of them is a pinch-penny. No one puts on airs or drives a flashy car. One guy owns 6 homes and is constantly looking for lost golf balls which he sells on eBay. Another guy sold his computer business for $5 million and drives a beat up, 20 yr old Dodge truck with a floor stick shift. For our golf matches, everyone kicks in $2.86 (don’t ask why $2.86). The winning team gets 5 bucks each player, 4 bucks each to second place, and 3 bucks each to third place (wow, a big 14 cent profit to third place). We are obviously not high-rollers, and everyone just loves it that way. We’re there to relax and have FUN, and we do.

Admin: exactly what interest rate are you expecting to turn an investment of $1500.00 annually for 20yrs into 50K? Also, where would you get said interest rate in 2012?

ragman

I didn’t say interest rate. I said return. I’ve been putting money into the American Century Global Gold fund every month since 2004. Annual return has been in excess of 15% for the last 8 years. A mear 5% return would get you to $50,000.

I’m 17 years from retirement and I’ve put away plenty.

People who lived for today always have a rationalization for why they didn’t save. I laugh at their bullshit excuses.

SPEND LESS THAN YOU MAKE.

Admin, you seem to be getting quite worked up, I think you should spend some of your savings on St. John’s Wort before you have a heart attack.

SSS, That sounds like a good time, but it misses my point. I agree with you completely, when you bring up you friends who worked hard, saved and are now enjoying it. Good for them, I hope you all have fun. You were able to save and prosper during a time when the system worked.

My point isn’t to sit on my butt and milk the system. I am working full time, going to class, and running a farm based business. What I am trying to say, is that I am 20+ years from retirement; the traditional systems of savings i.e. stocks, bonds, cash, etc. at this time do not appear to be a good store of wealth. If you are looking ahead, spending money on assets is a much safer store of wealth than Savings.

CavTanker

Show me someone who says savings is for suckers and I’ll show you an idiot with a big fat credit card balance and a big fat car loan or three year lease, a 401k balance of $5,000 with $3,000 loan against the balance.

Did I hit any nerves?

CavTanker

What “ASSETS” you talkin about that you are going to sell on Ebay and fund your glorious retirement? Inquiring minds want to know your secret to success.

everyone kicks in $2.86 (don’t ask why $2.86) -SSS

Now I am curious. Im not asking. Perhaps thats the average price of a viagra pill.

Retiring to other countries is something I keep hearing more and more of. Is this worth investigating? Or is it just another scheme?

Saving is for suckers -CT

I suppose you are saying that because of inflation, the Fed shoots for about 4% a year, what you make is worth less and less. Thats true. However credit card rates run about 20%.

I dont see how its wise to borrow which is worse than saving. Then again I think perhaps your being facetious.

Retiring to other countries is something I keep hearing more and more of. Is this worth investigating? -TPC

Costa Rica is one of the top places.

Yeah, thats what I hear as well. I wasn’t sure if it was just a pipe-dream or there was actually some merit behind it.

Another place I hear a lot about is New Zealand, but that just may be the professionals I am around. As far as I can tell there aren’t a lot of MDs and PhD’s in NZ so that may be why a number have been relocating down under lately.

Costa Ricans like Americans [for now =] and they have a good health care system which costs much less than here.

the CCSS provides affordable medical service to any foreign resident or visitor. Foreigners living in Costa Rica can join the CCSS by paying a small monthly fee–based on income–or they can buy health insurance from the state monopoly Instituto de Seguro Nacional (INS), valid with over 200 affiliated doctors, hospitals, labs, and pharmacies in the private sector. In 2010, the government made it mandatory for residency applicants to become members of La Caja

http://internationalliving.com/countries/costa-rica/health-care/

I remember being called stupid when friends tried to talk me onto going to the beach when I stayed to work on the roof of a rental.

I was called stupid because I wasn’t buying stock in the 90s, instead I was paying double and triple payments on my properties.

I’ve been called stupid for working so many hours all the time.

Financial advisors used to say it was stupid to pay off your house, I paid off my house.

Now I’m told that I’m really LUCKY to be able to retire and do anything I want to do

ASIG

You should have lived it up and then sold crap on Ebay to fund your retirement. How foolish of you to not spend more than you made. Aren’t you an American?

That is a decidedly depressing article. One comment really stuck out for me, “slower lifestyle.” Man that would be nice. As soon as my student loans are gone I may embrace that.

My friends are shocked that I haven’t bought a new car or a McMansion yet with “all that money” I make.

I don’t think they understand that all of my money is owned by someone else, that every cent I spend on myself puts me further away from my goal of zero debt.

Everyone is going to be surprised when my evil scheme is completed, and I get to live my life as I see fit! Running the numbers, its pretty surprising how much of my income becomes my own once that happens.

TPC

You are way ahead of the game. Don’t let anyone tell you what to do. If you always live beneath your means, you’ll never get in trouble.

Booty witch.

Be careful what you wish for:

http://t2.gstatic.com/images?q=tbn:ANd9GcSFpu5jmYP-7ltvrvyEzie5yWyHqEEaTdKzMQqyPzDFw8rNV2fKkXE1YFc

CavTanker

When you say “Saving is for suckers,” you’re sure to light someone’s fuze on this site because it’s not true. While you are correct that the financial world has been turned upside down in the past few years, there are still some tried and true guidelines which will serve you well. Such as:

1. Despite inflation, always have some cash reserves. Always. The peace of mind is worth it. Even if you can afford only a few hundred bucks for that unexpected car repair, it’s better than taking an ASSET you really love to the pawn shop for some quick cash.

2. There are still some very conservative investments with a steady, decent return (6-8%) which you don’t have to watch and aren’t getting slammed by high-speed computer trading. I mentioned one. Utility preferred stocks. Admin mentioned another, his American Century Global Gold fund (more risky, but he’s younger than I and can afford greater risk).

3. Take a look at some indexed investments focused at stocks and bonds. Some are extremely conservative, some very risky, and lots in between. See next comment if you don’t have the time.

4. We have an outstanding financial advisor for whom my wife worked for 17 years. The mutual trust between us is rock solid. We’re very lucky in that respect, but there are still many, many straight arrows in the financial advice world. Ask around.

Kill Bill

The $2.86 we kick in for our golf matches was to enable the golf shop to charge us an even $20 for the cart fee and the 2 bucks we pay for the bet. With the stupid county and state taxes on the cart rental (Jesus, is there anything that isn’t taxed in this country?), the pro shop added 86 cents to keep their accounting simpler.

Why can the IRS audit the people, but the people can’t audit the government?