Authored by Lance Roberts via RealInvestmentAdvice.com,

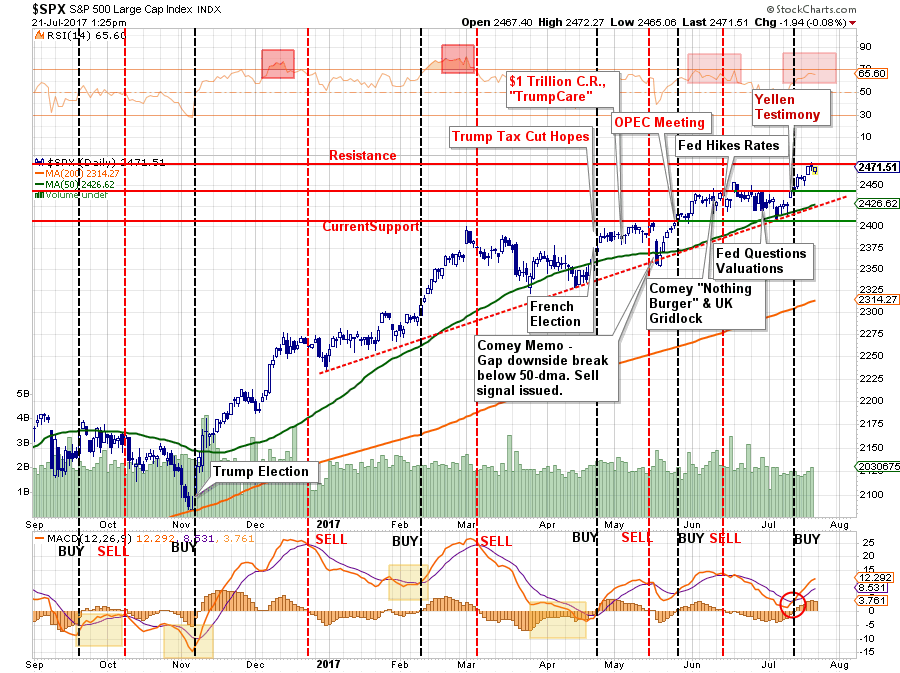

Stocks Rise Following Breakout

In last week’s missive “Bulls Run On Yellen’s Easy Money,” I addressed the breakout and why we increased equity exposure modestly in portfolios.

“However, this changed this past week as Yellen uttered the two magic words: ‘EASY MONEY.’

Okay, it wasn’t exactly two words. It was actually:

‘Because the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance.’

In other words, by saying that interest rates would not have to rise much further, the markets translated that to ‘lower interest rates for longer,’ confirming the Federal Reserve will remain “highly accommodative” to the markets so, therefore, ‘buy stocks.’

And with that, the robots leaped into action pushing markets OUT of the month-and-a-half long trading range of just 1.5%. This push to new highs, as noted above, also triggered a short-term ‘buy signal,’ at the bottom of the chart, which suggests this rally should continue higher over the next week, or so, heading into the month of August.”

“With the break above 2452 on Friday, assuming it will hold above that level into next week, it will provide an opportunity to increase short-term equity allocations in portfolios. However, be mindful, this is VERY short-term in nature and could be quickly reversed – so manage your risk accordingly.”

As stated, this analysis is VERY short-term in nature. Price trends are currently positive which keeps portfolios long-biased for the time being. However, while our portfolios are “bullishly” positioned for the short-term, we remain much more pessimistic about the longer-term return dynamics.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

I want to spend the rest of this weekend’s missive analyzing the ongoing bull thesis that has been pushed out by the media recently.

Analyzing The Bull Thesis

“Exactly a decade ago, it was time for investors to start worrying, even as stocks sat at record highs and the signs of onrushing danger were far from obvious.”

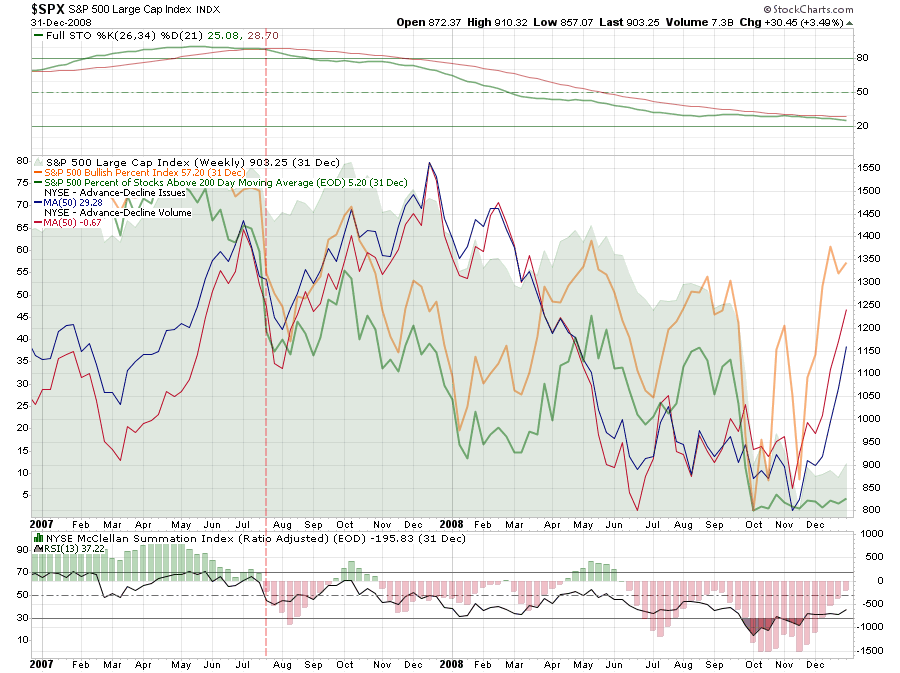

I am not so sure that warning signs weren’t obvious. Starting in mid-2007, the market began to struggle to make gains and initial “sell signals” were given as internal measures began to deteriorate.

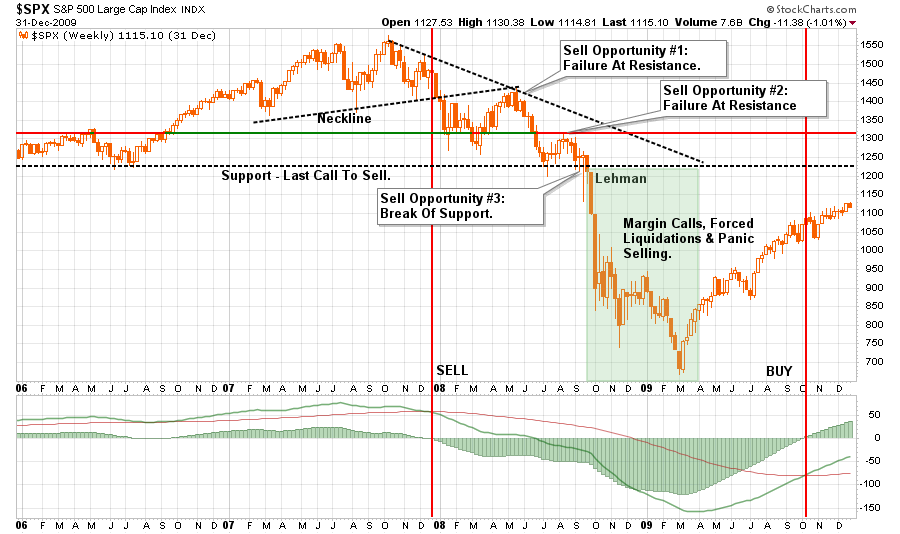

Furthermore, as shown in the chart below, the “financial crisis” was not a sudden event. Had investors been paying attention to the market, rather than listening to the advice of “buying the dips” or Fed Chairmen declaring “subprime is contained” and “it’s a Goldilocks economy,” there were three separate opportunities to step aside BEFORE the Lehman event ever occurred.

Yet, in 2007, much like today, individuals were being told to disregard much of the same evidence that existed then as they are today. Let’s take a look at a few of the arguments being made currently.

Earnings Growth Is Driving The Markets

The bulls currently have the “wind at their backs” as the continued “hope” the Trump administration will foster an age of deregulation, infrastructure spending and tax cuts which will boost corporate earnings in the future. Shortly after the election in 2016, Jack Bouroudjian via CNBC wrote:

“Let’s be clear, this market run up to the 20K level has a much more solid foundation for valuation. We are not looking at a P/E which has been stretched beyond historical norms as was the case in 1999, nor are we looking at a dot com bubble ready to implode. On the contrary, between digestible valuations and the prospects of real pro-growth policies, we have the foundation for a run up in equities over the course of the next few years which could leave 20K in the dust.”

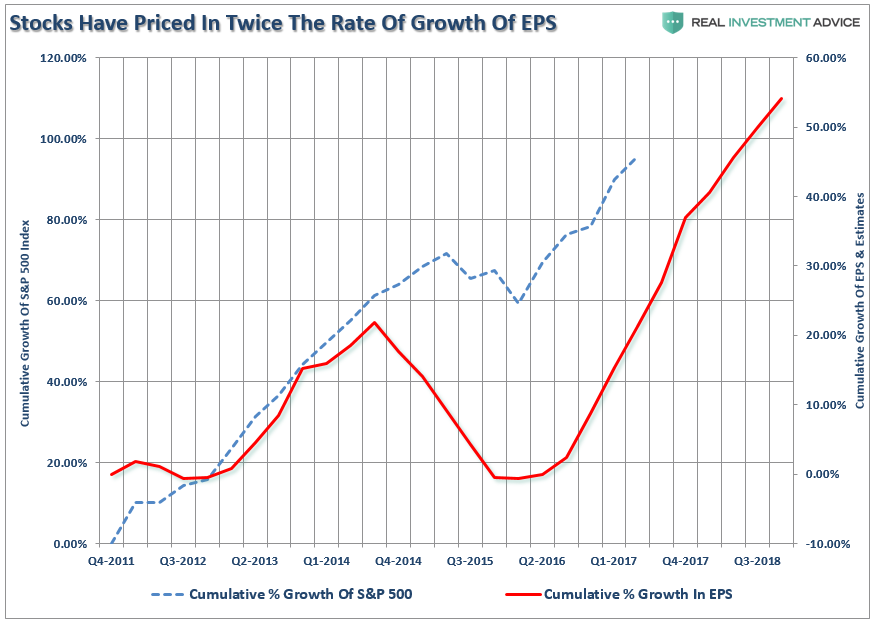

The problem is 9-months later there has been no advancement on that legislative agenda while the markets have surged more than 18% since the election. As I discussed previously, the market has already priced in the expected earnings growth from the “promised” Trump agenda which puts the market in danger of disappointment.

“Given that stocks have surged based on ‘hopes’ of deeper tax cuts, a tax cut only roughly half of previous estimates certainly puts valuations at risk. Once again, the market has already priced in earnings growth through 2018, making disappointment a much higher probability.”

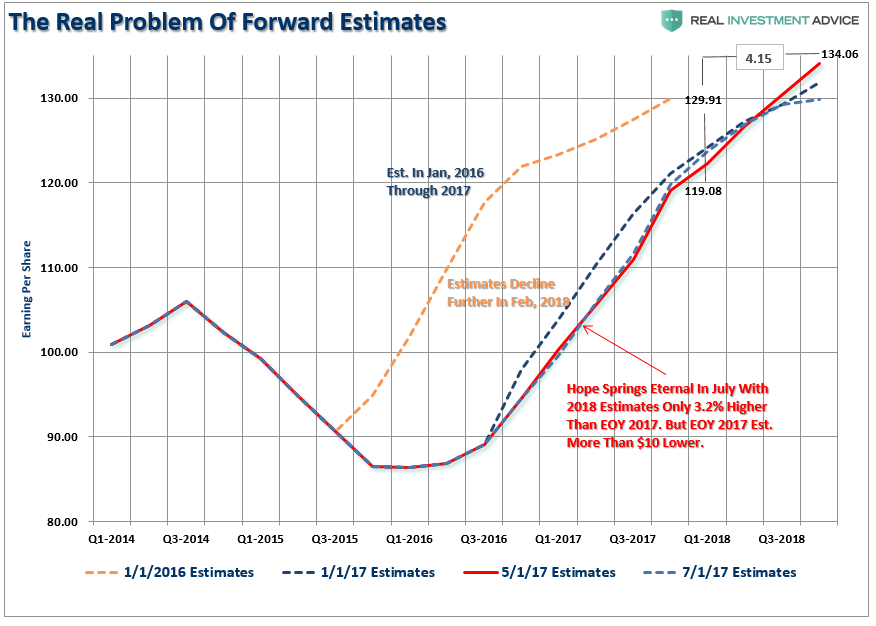

“Considering that forward estimates are generally overstated by 33% on average, the risk is high of disappointment. As shown below, there was a $10 difference between what earnings were expected to be in 2017 at the beginning of 2016 and today. Furthermore, forward earnings have only risen by $4.15/share for the end of 2018. Yet, as shown, above prices have more than priced in that future growth.“

However, as Dr. Lacy Hunt recently discussed, this may not be the case.

“Considering the current public and private debt overhang, tax reductions are not likely to be as successful as the much larger tax cuts were for Presidents Ronald Reagan and George W. Bush. Gross federal debt now stands at 105.5% of GDP, compared with 31.7% and 57.0%, respectively, when the 1981 and 2002 tax laws were implemented. Additionally, tax reductions work slowly, with only 50% of the impact registering within a year and a half after the tax changes are enacted. Thus, while the economy is waiting for increased revenues from faster growth from the tax cuts, surging federal debt is likely to continue to drive U.S. aggregate indebtedness higher, further restraining economic growth.

However, if the household and corporate tax reductions and infrastructure tax credits proposed are not financed by other budget offsets, history suggests they will be met with little or no success. The test case is Japan. In implementing tax cuts and massive infrastructure spending, Japanese government debt exploded from 68.9% of GDP in 1997 to 198.0% in the third quarter of 2016. Over that period nominal GDP in Japan has remained roughly unchanged. Additionally, when Japan began these debt experiments, the global economy was far stronger than it is currently, thus Japan was supported by external conditions to a far greater degree than the U.S. would be in present circumstances.”

With analysts once again hoping for a “hockey stick” recovery in earnings in the months ahead, it is worth noting this has always been the case. Currently, there are few, if any, Wall Street analysts expecting a recession at any point the future. Unfortunately, it is just a function of time until the recession occurs and earnings fall in tandem.

Valuations

Another argument often used to support the “bullish” meme is that valuations aren’t as high as they were in 2000. While that is true, there is a vase fundamental difference between now and then. In 2000, as valuations surged toward 42x CAPE earnings, there were MANY technology companies with negative earnings which skewed the valuation measure. Most of the companies are now gone, or the ones that survived finally begin generating earnings.

While valuations are NOT a good market timing indicator, and are not predictive of the end of a bull market advance, by all historical measures, they are expensive. Most importantly, while high valuations certainly aren’t predictive of bear market onsets, they are HIGHLY predictive of very low returns in the future.

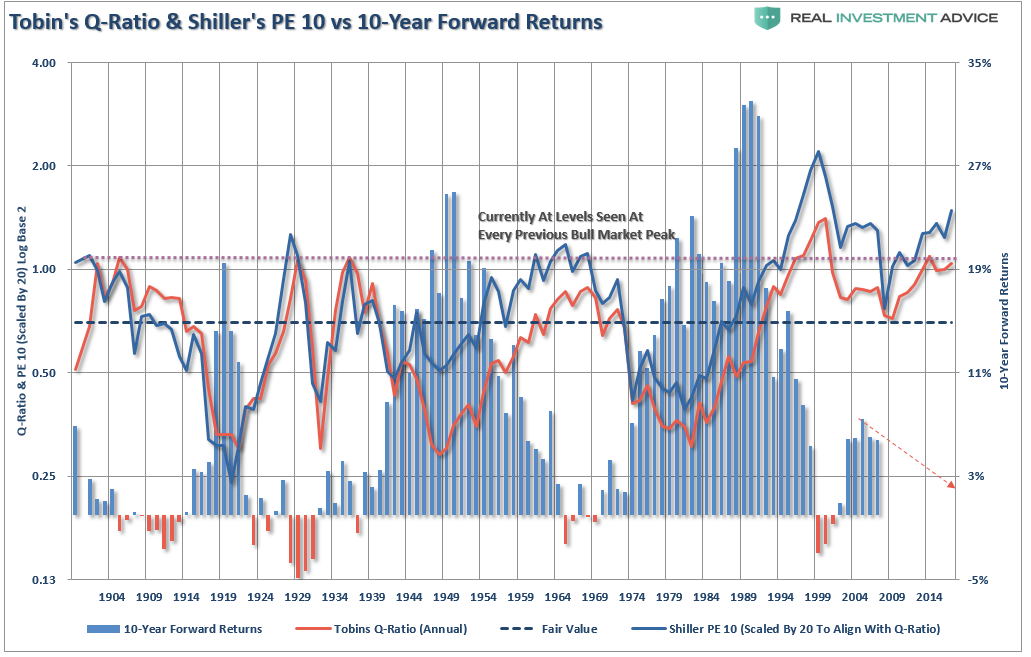

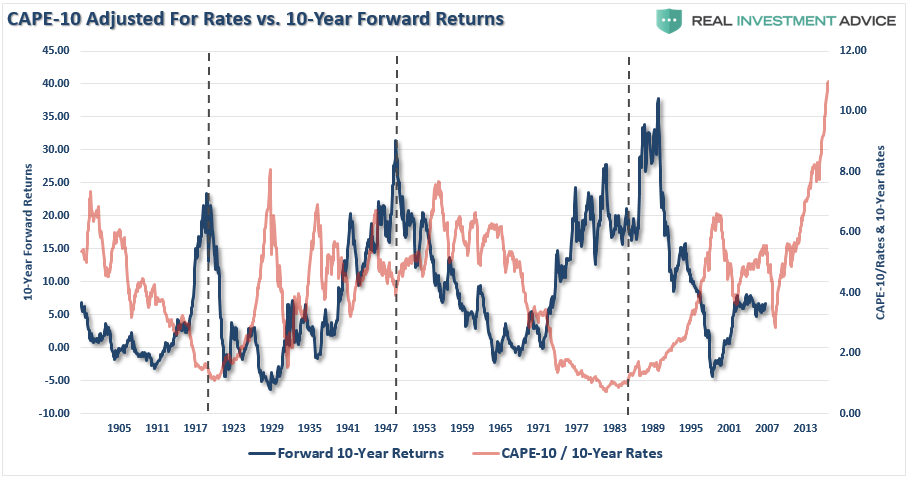

One of the other arguments to justify higher valuations has been that interest rates are so low. Okay, let’s take the smoothed P/E ratio (CAPE-10 above) and compare it to the 10-year average of interest rates going back to 1900.

Importantly, the statement of “lower future returns” is very misunderstood. Based on current valuations the future return of the market over the next decade will be in the neighborhood of 2%. This DOES NOT mean the average return of the market each year will be 2% but rather a volatile series of returns (such as 5%, 6%, 8%, -20%, 15%, 10%, 8%,6%,-20%) which equate to an average of 2%.

Sentiment Is Bullish

Of course, as discussed previously, investor behavior makes forward long-term returns even worse.

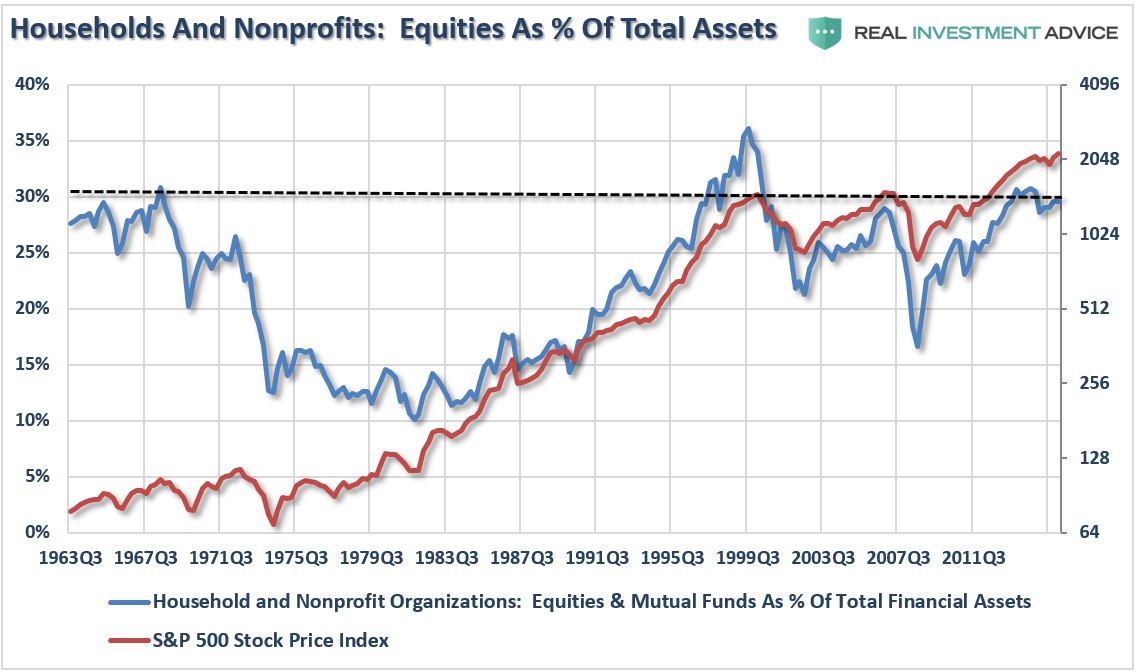

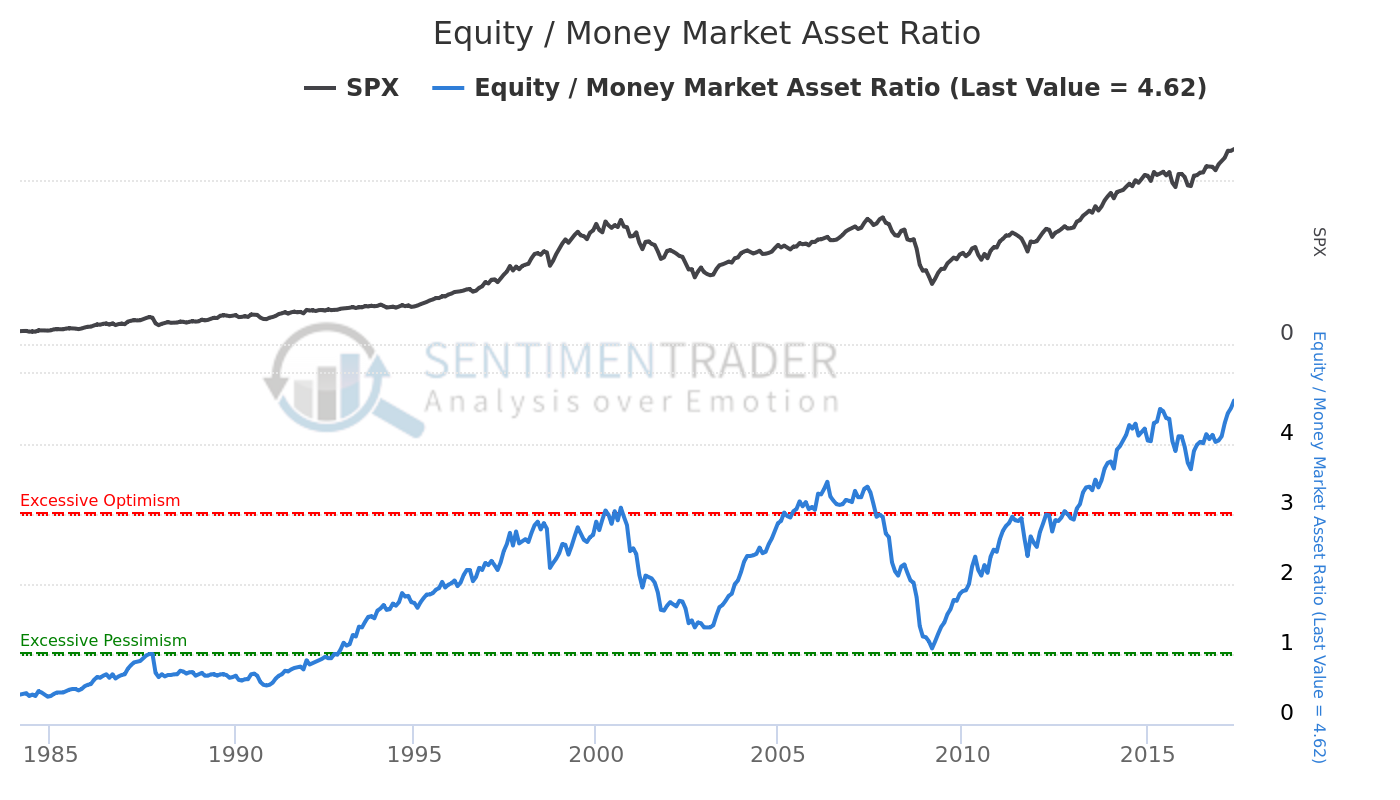

The bulls have continually argued the “retail” investor is going to jump into the markets at any moment which, with all the “cash on the sidelines,” will keep the bull market alive. The chart below suggests they are already in. At 30% of total assets, households are committed to the markets at levels only seen near peaks of markets in 1968, 2000, and 2007. I don’t really need to tell you what happened next.

Furthermore, as I have discussed repeatedly in the past, there is NO “cash on the sidelines” to begin with. To wit:

“Every transaction in the market requires both a buyer and a seller with the only differentiating factor being at what PRICE the transaction occurs. Since this must be the case for there to be equilibrium to the markets there can be no ‘sidelines.’

Furthermore, despite this very salient point, a look at the stock-to-cash ratios also suggest there is very little available buying power for investors current.”

There is no cash on the sidelines.

Furthermore, the dearth of “bears” is a significant problem. With virtually everyone on the “buy” side of the market, there will be few people to eventually “sell to.” The hidden danger is with much of the daily trading volume run by computerized trading, a surge in selling could exacerbate price declines as computers “run wild” looking for vacant buyers.

This thought dovetails into the “hyperextension” of the market currently. Since price is a reflection of investor sentiment, it is not surprising the recent surge in confidence is reflected by a symbiotic surge in asset prices.

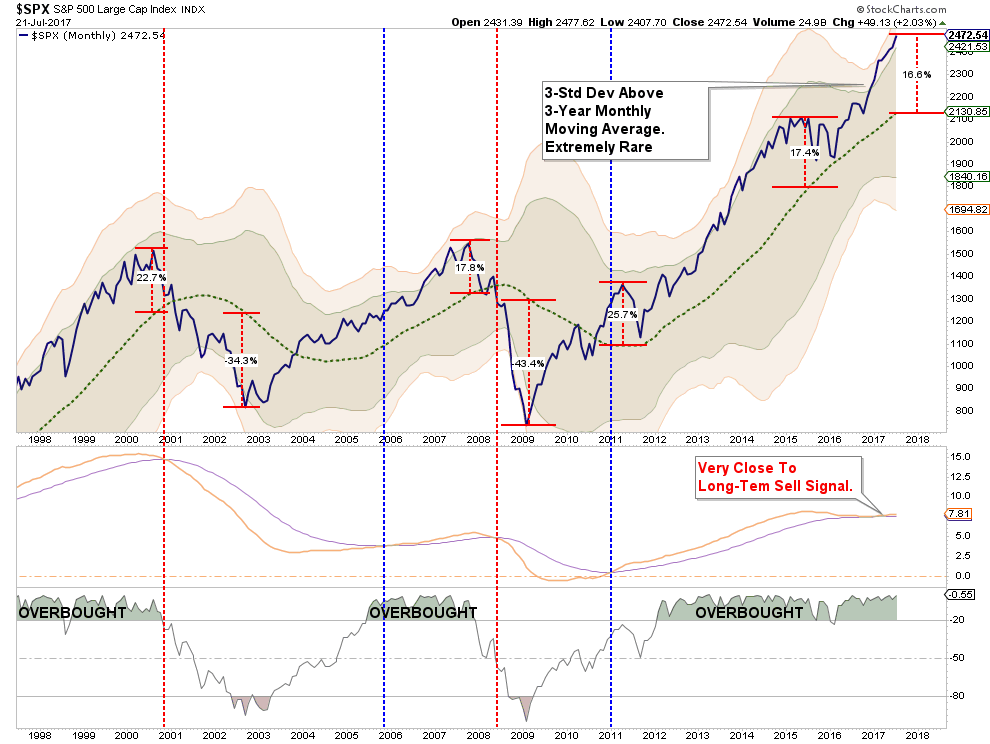

The chart below shows the deviation above the 3-year moving average. Importantly, at the peak of the previous two bull markets, the deviation never pushed into the 3-standard deviation range as it is currently. This suggests there is VERY little room left to the upside before some corrective action occurs.

The problem, as always, is sharp deviations from the long-term moving average always “reverts to the mean” at some point. The only questions are “when” and “by how much?”

Managing Past The Noise

There are obviously many more arguments for both camps depending on your personal bias. But there is the rub. YOUR personal bias may be leading you astray as “cognitive biases” impair investor returns over time.

“Confirmation bias, also called my side bias, is the tendency to search for, interpret, and remember information in a way that confirms one’s preconceptions or working hypotheses. It is a systematic error of inductive reasoning.”

Therefore, it is important to consider both sides of the current debate in order to make logical, rather than emotional, decisions about current portfolio allocations and risk management.

Currently, the “bulls” are still well in control of the markets which means keeping portfolios tilted towards equity exposure. However, as David Rosenberg recently penned, the markets may be set up for disappointment. To wit:

“So we have a sluggish U.S. economy on our hands with growth revisions to the downside. We have a situation where some investors see the softness enduring long enough that Fed funds futures are now pricing in less than 50-50 odds that Yellen et al make another rate move by year-end. Yet the Fed is signaling that it will begin to shrink the balance sheet by the fourth quarter, with no economic liftoff.

The political backdrop is rife with gridlock — unbelievably, there is still hope among investors that tax reform is coming by 2018. At the same time, evidence is mounting that the Dems have a serious shot of taking the House next year. We have a White House that, with the help of inside leaks and the media, continues to find itself embroiled in controversies. And health care reform, which was always pledged to be the first item to be done, is looking more and more like a pipe dream. When hasn’t governing been complicated? It took the Gipper five years and endless bottles of scotch with Tip to get tax reform legislated in 1986!

We have heightened geopolitical risks from North Korea and China has instructed the U.S. that it will not be pressured to invoke sanctions against its unstable satellite.

We have a central bank chief who looks to be a lame duck…a recent WSJ survey found that economists only peg her odds of staying on past February 2018 at 20.8%. Just more uncertainty to deal with.”

Currently, there is much “hope” things will “change” for the better. The problem facing President Trump, is an aging economic cycle, $20+ trillion in debt, an almost $700 billion deficit, unemployment below 5%, jobless claims at historical lows, and a tightening of monetary policy and 80% of households heavily leveraged with little free cash flow. Combined, these issues alone will likely offset most of the positive effects of tax cuts and deregulations.

Furthermore, while “bearish” concerns are often dismissed when markets are rising, it does not mean they aren’t valid. Unfortunately, by the time the “herd” is alerted to a shift in overall sentiment, the stampede for the exits will already be well underway.

Importantly, when discussing the “bull/bear” case it is worth remembering that the financial markets only make “record new highs” roughly 5% of the time. In other words, most investors spend a bulk of their time making up lost ground.

The process of “getting back to even” is not an investment strategy that will work over the long term. This is why there are basic investment rules all great investors follow:

- Sell positions that simply are not working. If they are not working in a strongly rising market, they will hurt you more when the market falls. Investment Rule: Cut losers short.

- Trim winning positions back to original portfolio weightings. This allows you to harvest profits but remain invested in positions that are working. Investment Rule: Let winners run.

- Retain cash raised from sales for opportunities to purchase investments later at a better price. Investment Rule: Sell High, Buy Low

These rules are hard to follow because:

- The bulk of financial advice only tells you to “buy”

- The vast majority of analysts ratings are “buy”

- And Wall Street needs you to “buy” so they have someone to sell their products to.

With everyone telling you to “buy” it is easy to understand why individuals have a such a difficult and poor track record of managing their money.

Trying to predict the markets is quite pointless. The risk for investors is “willful blindness” that builds when complacency reaches extremes. It is worth remembering that the bullish mantra we hear today is much the same as it was in both 1999 and 2007.

Again, I don’t need to remind you what happened next.