Guest post by John Mauldin

One difficulty in analyzing our economic future is the sheer number of potential crises. When so much could go wrong (and really right, when the exponential technologies I foresee get here), it’s hard to isolate, let alone navigate, the real dangers. We are tempted to ignore them all. Ignoring them is usually the right response, too. We can “Muddle Through” almost anything.

But muddling through isn’t the same as smooth sailing. It’s difficult, unpleasant, and often keeps you from looking for better opportunities. Then there are times when you can’t even muddle through. Instead, you find yourself emotionally at a dead stop or even going backwards. When surviving the storm is your focus, taking those “blood in the streets” buying opportunities is hard.

Which leads to this week’s letter. Almost every day I read scores of finance and economic newsletters, websites, articles, and books. A few articles on pensions hit my inbox this week and pursuing them led me to today’s topic.

But dear gods, I can remember writing a decade ago that public pension funds were $2 trillion underfunded and getting worse. More than one person told me that couldn’t be right. They were correct: It was actually much worse. (See, I’m an optimist!)

Two years ago I wrote that Disappearing Pensions are The Crisis We Can’t Muddle Through. Nothing since then has changed my mind. In fact, failure at all levels to even begin solving the problem is making it worse. The latest estimates, as we will see, suggest that it has gotten $2 trillion or more worse in just a few years.

Note we are talking here about a specific kind of pension: defined benefit plans, usually those sponsored by state and local governments, labor unions, and a dwindling number of private businesses. Many sponsors haven’t set aside the assets needed to pay the benefits they’ve promised to current and future retirees. They can delay the inevitable for a long time but not forever. And “forever” is just around the corner.

As we will see below, the numbers are large enough to make this a problem for everyone, even those without affected pensions. The problem is “solvable”… but the solutions will be problems in themselves.

Underfunded Future

Let’s begin with the enormity of the pension funding gap. As with the federal budget deficit, the large numbers are hard for our minds to process. They are also inherently uncertain. Let me explain.

A defined benefit pension plan for, say, a city’s police department, knows it owes a certain number of retirees certain monthly benefits for life. Their lifespans are fairly predictable when the pool is large enough. (I think new biotechnologies will change this soon, but that’s another topic.)

From that, it’s simple math to calculate how much money the plan should have right now in order to pay those benefits when they are due. But then the assumptions start. The plan must presume a future rate of return on the invested portfolio, an inflation rate, and in some cases future health care costs (medical benefits are part of many plans).

So, when we say a plan is “fully funded,” it may not be so if the assumptions are wrong. The amount a plan is underfunded could be much larger than the sponsor and auditors say. In theory, it could be smaller, too, but I have never seen that happen. The accounting rules that govern all this allow (some would say encourage) the sponsoring cities, counties, and states to understate their liabilities. This lets them avoid hard decisions like raising taxes, cutting benefits, or reducing other needed services.

Here’s a Wharton School note to place this huge number in context.

Sanitation workers, firefighters, teachers and other state and local government employees have performed their duties in the public sector for decades with the understanding that their often lackluster salaries were propped up by excellent benefits, including an ironclad pension. But Moody’s Investors Service recently estimated that public pensions are underfunded by $4.4 trillion. That amount, which is equivalent to the economy of Germany, accounts for one-fifth of national debt. It’s a significant concern for public employees who were banking on a fully funded retirement to get them through their golden years. The true number could be much higher. Whatever it is, filling it will be painful for somebody. Pensioners will receive lower-than-expected benefits, taxpayers will get higher-than-expected tax bills, or citizens will see government services cut. Or maybe all the above.

Then again, if you make more realistic assumptions on future returns the unfunded liability becomes $6 trillion according to the American Legislative Exchange Council. Total state and local annual revenues are only $3.1 trillion. Total property taxes are roughly $590 billion.

Here’s more grim news from The Heritage Foundation.

Overall, the American Legislative Exchange Council estimates that pension plans have only about a third of the funds on hand—33.7 percent—that they need to pay promised benefits. Some states have significantly lower funding levels, which means they are at risk of running out of funds in the near future.

Once a state or local pension plan runs out of money, taxpayers have to fund the pension benefits of retirees as well as the contributions of current employees.

Connecticut, Kentucky, and Illinois have the lowest funding ratios, at 20 percent, 21 percent, and 23 percent respectively.

Already, Illinois spends as much on pensions as it does on welfare and public protection (that is, police and firefighters) combined, and nearly half of its education appropriations go toward teacher pensions. If the state’s pension plans reach insolvency, pensions could become its single biggest cost.

These unfunded liability estimates are high because plan assumptions are too optimistic. Almost all public pension funds assume investment returns somewhere around 7% (and some as high as 8%+). A more conservative and realistic approach would force the state and local governments to fund those pension plans at a much higher level by either raising taxes or reducing services. What local politician will volunteer to do that? Better to find a consultant to tell you what you want to hear. There are plenty of them that will, for a reasonable fee, billed to the taxpayers.

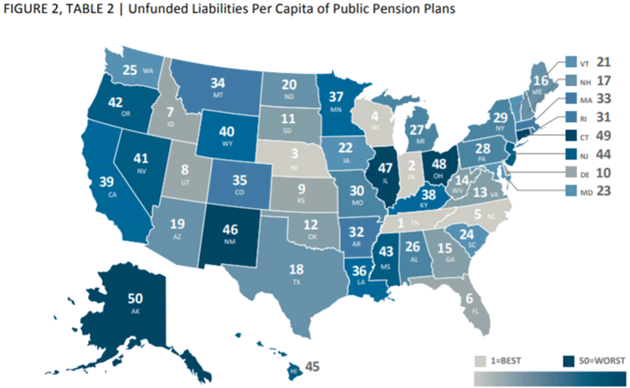

The following graphic shows how your state is ranked on a per capita funding basis. You can see the absolute numbers in the following table.

Source: Valuewalk

A further complication is that the taxpayers who might have to cover these amounts are mobile. They can move to other states with lower tax burdens, leaving behind those who, for whatever reason, can’t leave their states.

And to make it even more interesting, the beneficiaries often no longer live in the states that pay them. Retired public employees from the Northeast might live in Florida now, for instance. They can’t even vote for the people who govern their incomes.

The broader point: As with the federal debt, some portion of this unfunded pension debt is going to get liquidated in some manner. Any way we do it will hurt either the pensioners or taxpayers.

Pension Fund Underfunding Is a Local Problem

Thirty years ago Frisco, Texas, had fewer than 20,000 residents. Today its population is well over 180,000. Corporations from all over America are moving there. Tax revenues are booming. Frisco is the happy exception that simply grew faster than its pension liabilities.

Not so Dallas, whose Police and Fire Pension System was advertised as solvent just a few years ago. Now it is so deep in the hole that the mayor says plugging the gap would take almost a doubling of city taxes. (I bought my Dallas apartment after that news was announced but such an increase would have still made my taxes cost more than my mortgage. Can you say taxpayer revolt? It wasn’t the main reason, but it did factor in to my move.) Texas Monthly recently noted:

For those of us in Texas, with our gloriously high credit ratings and fervent allegiance to low taxes, restrained spending and conservative oversight of a robust Rainy Day Fund, the news that certain big cities around the country were in a heap of trouble might have elicited nothing more than a collective, if somewhat condescending, shrug. Except for one thing: Texas’s four biggest cities were all high on the list [of the worst 15 cities]. Dallas, which came in second, is on the hook for $7.6 billion, about five times the amount of its total operating revenues. Houston was fourth, with a $10 billion shortfall—equal to four times its operating revenues. Austin, at number nine, has $2.7 billion in liabilities, and San Antonio, ranked number twelve, is $2.3 billion short. That seems like very bad news for just about any Texan. Particularly since the vast majority of Texans now live in urban areas. How can a state known for fiscal responsibility have so many cities with empty pockets?

Will Frisco residents want to pay for the Dallas pension funding problems? Is The Woodlands going to want to pay for Houston’s problems? Is Indiana ready to pay for Illinois? Of course not. How much of a crisis will we need in order to recognize we are all in this together? Probably a lot bigger than you imagine.

Make the Children Pay

While arguments progress at the national level, state and local leaders must simultaneously pay their pension benefits, provide public services, and keep taxes to a level that doesn’t sweep them out of office or drive top taxpayers away. Not to mention keep the markets happy enough to sell future bond offerings, until such time as the Fed steps in as buyer-of-last resort. A tall order.

Given those choices, the usual answer seems to be “cut services and hope no one notices.” It is happening nationwide but California is in the vanguard, thanks to its massive pension debt. This is from a recent Brookings Institution note.

Pension and health-benefit costs are bending education finances in California to their will. The sheer magnitude of the rising costs is staggering. Large numbers of school board officials who participated in our survey indicate that the rising costs are meaningfully affecting educational services. For example, many report making cost-saving changes to district budgets that include deferred maintenance, larger class sizes, and fewer enrichment opportunities for students in response to rising pension and health benefit costs.

So in effect, today’s students are paying to keep benefits flowing to retired teachers and administrators.

Meanwhile, the Berkeley city council is taking criticism for prioritizing pension payments ahead of public works projects. Voters approved bond issues supposedly dedicated to infrastructure but the city is apparently not doing the work.

Nor is it just California. In a recent study, Bank of America analysts found an inverse relationship between infrastructure investment and pension fund contributions. Each additional $1 billion in plan contributions subtracts about $2.5 billion from state and local government investment.

We have multiple parties fighting over pieces of the same pie, all hoping that Uncle Sam will step in and save them. Uncle Sam may well do it, too, but it won’t remove the pain. It will just redistribute the burden, perhaps more widely, but the aggregate amount won’t change.

In my view, this leads to some kind of Japan-like deflationary recession. If we’re lucky, it will be mild and long. It won’t be fun but the alternatives would be worse.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

DC will bail everyone out. Well, everyone but the private, middle class sector, that is.

In 2005 or 2006 (I would have to look at old records in storage), I was union steward for a technical writing contractor for the USAF. I basically inherited the union steward position by taking the job. At the time, I didn’t quite “get” what the union connection meant. So, for an increase in pay as an “editor” to a full-blown “tech writer” I became a union steward and, because I am who I am… I read the Fair Labor Standards Act and enough of the regulatory theory behind it to decide I could embrace the idea that Corporations were evil and it was only the Union which allowed workers to get paid for their labor. (Notice the new “meaning” of the word “Union”?)

I sat on the negotiating team for the Collective Bargaining Agreement and during a week-long arms’ length negotiation with Boeing partnered with a little minority owned company I won’t name because I won’t give them any press because they were frauds, I learned an awful lot about the IAM National Pension Fund and how these things work.

I tried to insert a plank into the CBA allowing the worker to direct that retirement money themselves… so, if 3 percent was sent by the Company on behalf of the Employee* and was told that while that might indeed be something the employees wanted, it did not benefit the Union in any way. Besides, I was told… the IAM Pension fund is GUARANTEED.

Know why? Donkey Balls, let me tell you why. There is this thing called the PassThrough in the LAWS covering Collective Bargaining Agreements. If the Benefit to the Employee was negotiated at “arms length” between the Company, the Union with a Federal representative present then the government guarantee was already there. The Federal government would back the IAM Pension plan even though it wasn’t actually in the contract. That, my friend, is the beauty of the passthrough. The IAM National Union is too big to fail.

I got suspended a couple months later, but that’s another story. I do not draw from the IAM Pension fund since I was not vested. My husband does and he got a letter a week or so ago indicating pension benefits may be reduced at some point and no one is allowed to retire early any longer.

We laughed and laughed.

(The federal agent came in to meet the Union at 7 a.m. I briefed him on the Company when he met us all later that morning. It was, indeed, a big farce. At 10, we “met” him again when he arrived at the CBA negotiations.)

*the legalese is flat out bullshit at these things. Union fat fucks across the table from Corporate fat fucks with little old me sitting pretty taking notes and offering the Union the gender equality chip. I’d been a member of the dog and pony show before… I was handpicked to brief a class of graduating Generals. Did you know they have classes for newly starred Generals? Well, for graduation one year, the brand new Generals got to see an AWACS plane on static display and I briefed them on how the radar worked.

Most of them didn’t give a shit… they were academy grads and never held a torque wrench nor would they know what to do with a multimeter, so I just gave them the canned brief and the next group of five or so new Generals came along to hear my spiel and see the radar stuff, most of which was in the belly of the plane. Only one guy took me up on crawling down there to see the big klystrons and all the high voltage lines, power supplies and other very interesting things down there, some of which I understood.

At one point, this unique General asked me flat out what the operating frequencies of the radar were and what kind of power output the antenna was capable of. That threw me for a loop, let me tell you. (Hint that dialogue is coming.)

(Feeling.) I stared at him blankly (thought and feeling together) and said “Sir, I just can’t tell you that.” Feeling/Thought/Action/Speech

[Even dialogue requires action/reaction. The general’s reaction is REQUIRED to give perspective.]

His eyes narrowed (his feeling) and I sensed his irritation (my thought). He leaned against the cabinet containing the STALO (Stable Local Oscillator) where the whole frequency business starts in a radar chain of events. (A very meaningful ACTION with a bit of information in it)

“What kind of a radar tech are you if you don’t even know the frequencies and power?”

My stomach clenched at the disdain I heard in the General’s voice. I was a Staff Sergeant by then, no longer a quivering airman but anyone with a star on his shoulder is intimidating to any enlisted soldier or airman and I was no different. I kept my expression respectful as I explained to him that I indeed KNEW the frequencies and power output of the very special radar system Westinghouse engineers designed and built, but it was highly classified data and as far as I knew, he, the General, had no need to know.

I got a letter of commendation out of that.

(Sometimes, dropping into narrative to stretch out the anticipation helps emphasize the conflict. Conflict is what moves people, not resolution.)

[Feeling/Thought/Action/Speech… they do not all have to be there but when they are, it makes it work.]

I do not teach classes on writing any longer, nor I do not edit nor do I revise any longer. However, if you pay attention, you might learn something.

M G- I got the same letter from the IAM national pension fund. They’ve just gone negative (89%) and voluntarily placed the fund in some kind of endangered status that allows them to curtail certain options and basically lower their obligations.

I’m also covered in another IAM pension fund: Automotive Industries. It’s been unsound for years and sinking fast. Recent attempts to take remedial action were pitched to the Treasury Dept. as required, where they were promptly snuffed out.

Treasury essentially said: When the fund goes dry petition Congress for a bailout.

Supposedly only 4 funds out of approximately 100 were allowed to make the necessary adjustments which included benefit reductions.

We will just need to reduce costs.

My employer just sent out the annual pension statement. I am probably one of 7 people that actually read it. They merged an acquired company’s pension fund into the general pension fund. Pre merger, the acquired pension fund was 200%+ funded without the assumed returns. In the latest, the company fund is 71% funded.

Looks to me like they just gutted the acquired fund. But, if you don’t read the mailings you never know.

The crooked E did the same to GE Power, poor bastards ended up with no pension.

The supreme court ruled about 30 years ago that action was legal. Gulf Oil retirees sued Chevron and lost

Just another day in a Broke Dick Nation.

A decade after the recession, 40% of U.S. families still struggling

https://www.cbsnews.com/news/a-decade-after-the-recession-40-of-us-families-still-struggling/

Do these struggling families have newer cars, houses they could never afford, I-phones, cable TV, work more than 40 hours? There is no mention in that article.

I have read enough studies and seen enough 1st hand to believe that many of those struggling families put themselves in that position.

The failure to save for retirement is a cultural/ethical/moral issue. 40% of US households can’t pony up $400 for an emergency. Sounds like the US population in general is immature and unable to fend for themselves. Any wonder many want someone else, big Daddy government, to take care of them. Boy are they in for a surprise when they find out that only the most corrupt rise to the top of big gov. One has to be a fool to trust/rely on the most corrupt among us for their future. Let me add stupid to cultural/ethical/moral bankruptcy.

Billy, this is about working stiffs who counted on a pension.

you’re correct mistico,but go back to your old name–

“beaners who try to get above their raisin irritate me.”panglossie