In Part One of this article I laid the groundwork of the Fourth Turning generational theory. I refuted President Obama’s claim that the shadow of crisis has passed. The shadow grows ever larger and will engulf the world in darkness in the coming years. The Crisis will be fueled by the worsening debt, civic decay and global disorder. I will address these issues in this article.

Debt, Civic Decay & Global Disorder

The core elements propelling this Crisis – debt, civic decay, and global disorder – were obvious over a decade before the financial meltdown catalyst sparked this ongoing two decade long Crisis. With the following issues unresolved, the shadow of this crisis has only grown larger and more ominous:

Debt

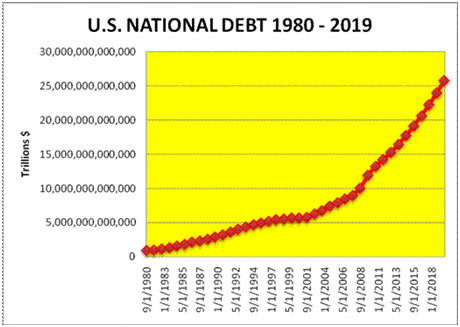

The national debt has risen by $7 trillion (64%) to $18.1 trillion since 2009 and continues to accelerate by $2.3 billion per day, on track to surpass $20 trillion before Obama leaves office and $25 trillion by 2019.

The national debt as a percentage of GDP is currently 103% (it would be 106% if the BEA hadn’t decided to positively “adjust” GDP up by $500 billion last year). It is on course to reach 120% by 2019. Rogoff and Reinhart have documented the fact countries that surpass 90% experience economic turmoil, decline, and ultimately currency collapse and debt default.

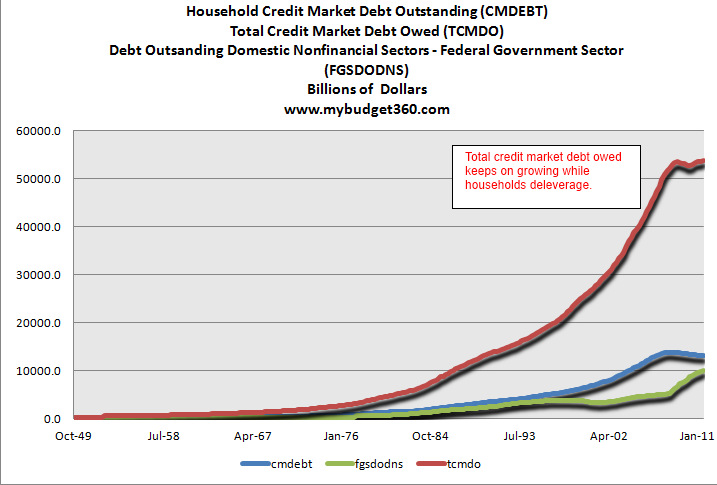

Despite the housing collapse and hundreds of billions in mortgage, credit card, auto, and corporate debt being written off, dumped on the backs of taxpayers and hidden on the Federal Reserve balance sheet, total credit market debt has reached a new high of $58 trillion.

Harvard professor Laurence Kotlikoff has been a lone voice telling the truth about the true level of unfunded promises hidden in the CBO numbers. The unfunded social welfare liabilities in excess of $200 trillion for Social Security, Medicare, Medicaid, and Obamacare are nothing but a massive future tax increase on younger and unborn generations. Kotlikoff explains what would be required to pay these obligations:

“To honor these obligations we could (a) raise all federal taxes, immediately and permanently, by 57%, (b) cut all federal spending, apart from interest on the debt, by 37%, immediately and permanently, or (c) do some combination of (a) and (b).”

The level of taxation and/or Federal Reserve created inflation necessary to honor these politician promises is too large to be considered feasible. Therefore, these promises, made to get corrupt political hacks elected to public office, will be defaulted upon.

Sometimes I wish I could just passively accept what my government monarchs and their mainstream media mouthpieces feed me on a daily basis. Why do I have to question everything I’m told? Life would be much simpler and I could concentrate on more important things like the size of Kim Kardashian’s ass, why the Honey Boo Boo show was canceled, the Victoria Secret Fashion Show, whether I’ll get a better deal on Chinese slave labor produced crap on Black Thanksgiving, Black Friday, or Cyber Monday, fantasy football league standings, the latest NFL player to knockout their woman and get reinstated, Obama’s latest racial healing plan, which Clinton or Bush will be our next figurehead president, or the latest fake rape story from Rolling Stone. The willfully ignorant masses, dumbed down by government education, lured into obesity by corporate toxic packaged sludge disguised as food products, manipulated, controlled and molded by an unseen governing class of rich men, and kept docile through never ending corporate media propaganda, are nothing but pawns to the arrogant sociopathic pricks pulling the wires in this corporate fascist empire of debt.

I’m sure my blood pressure would be lower and my mood better if I just accepted everything I was told by my wise, sagacious, Ivy League educated, obscenely wealthy rulers as the unequivocal truth. Why should I doubt these noble, well intentioned, champions of the common folk? They’ve never misled us before. They would never attempt to use two highly publicized deaths as a lever to keep black people and white people fighting each other and not realizing all races are now living in a militarized police surveillance state supported by the one Party. They would never use their complete control over the financial, political, judicial, and media organisms to convince the masses that voting for one of their hand selected red or blue options will ever actually change anything. They would never engineer the overthrow of a democratically elected government, cover up the shooting down of an airliner, and attempt to blame their crimes on the leader of a nuclear power in their efforts to retain a teetering global empire. They would never overthrow or wage economic warfare on countries that don’t toe the line regarding the continued dominance of the petrodollar in global commerce.

Sadly, I’m cursed with a mind that questions everything and trusts no one in authority or associated with the status quo. It’s the reason I don’t read newspapers or watch mainstream media television entertainment propaganda, disguised as news. It’s the reason I will never vote in a national election again. The lesser of two evils is still evil. I’m skeptical of every piece of data fed to the sheep by the government apparatchiks working for the state. The faux journalists being paid millions by one of the six corporations controlling the media and dependent upon the government, Wall Street bankers, and mega-corporations for their advertising revenues regurgitate whatever they are told by those pulling the purse strings. The mainstream media are nothing but propaganda peddlers for the Deep State and truth telling is prohibited in their world of deception, debt, and denial. Their job is to sustain, enhance, and further enrich the status quo by engineering consent through what they report and what they do not report. The true ruling powers who operate in the shadows behind the scenes are men of power, wealth, status and education who truly believe they are better equipped to consciously manage and manipulate the public mind to achieve their ends. They are disciples of the Edward Bernays School of deception, manipulation and propaganda.

“If we understand the mechanism and motives of the group mind, is it not possible to control and regiment the masses according to our will without their knowing about it? The recent practice of propaganda has proved that it is possible, at least up to a certain point and within certain limits.”–Edward Bernays

The Nazis were pikers compared to the technologically savvy Madison Avenue maggots and Silicon Valley snakes who mold the opinions, tastes, and beliefs of the iGadget addicted, vapid, unintelligent, unquestioning, zombie-like masses who beseech to be led, told what to do and what to believe. A vast swath of the population don’t read books or even know how to read above a grade school level. They couldn’t write a coherent paragraph if their life depended upon it. But they can twitter, text, Instagram, and facebook at the speed of light. Try walking down any street in an American city without some iGadget distracted oblivious moron bumping into you. The addicting nature of today’s technology is being used by the ruling elite to monitor, control, and make you respond the way they choose.

Facebook, corporate media organizations, quasi-government organizations, and the NSA are creating a corporate totalitarian state where the slaves willingly sacrifice their privacy, liberty and freedom for mindless entertainment and distractions. The 21st Century totalitarian state captures your political beliefs, daily activities, habits, interests, spending behaviors, organizational associations, love life, pictures, psychological makeup, and fears from your own postings on the internet. With the right algorithms they can uncannily predict how you will react to different situations and messaging. They can also uncover threats to the status quo. Under the guise of keeping you safe from terrorists they are actually ferreting out subversives and radicals who refuse to conform to their idea of a good citizen slave. We will all be subject to our own Room 101.

Dan Kaplan in his recent article about Facebook as a tool for totalitarianism lays out the extreme threat to our future:

Today’s totalitarian demands a more subtle way to influence cultural and political sentiment. But if you got your hands on an algorithmically filtered newsfeed? One that could control the stories people see every day and influence their emotions across geographic, political and economic lines? You’d be in business.

But then there was the mood-influence study that scandalized us for a couple of weeks this year. Facebook changed the tone of content showing up in people’s feeds to test the impact it could have on their moods. The results, not too surprisingly, suggested that Facebook has the power to manipulate sentiment at scale.

Given how easy it is to scare people about the scary-seeming-but-actually-low-risk Ebola, and how dumb we all get when we are afraid, it is not crazy to think that under the wrong circumstances — like one or two more mass-scale terrorist attacks on major cities — modern democracy gives way to something akin to 1984.

If Big Brother were to seize the reins of power, sure, he’d use the cable news the way it’s being used today. But Facebook’s data maw, targeting power and sentiment-manipulation capabilities would be far more insidious. Whether this is what we become or not comes down to the future we choose to build.

The saddest part of this episode of mass delusion, mass confusion, and mass media collusion is that even though we are moving towards Orwell’s totalitarian vision of society, thus far, technology, triviality and an unending array of distractions have lured the masses into passive preoccupation with egotistical pleasures. We’ve been persuaded to love our servitude while drowning in a sea of irrelevance, diversions, and trifles. We continue to amuse ourselves to death while forging our own chains of debt and yielding to the direction of an all-powerful welfare warfare surveillance state that promises to protect us from phantom threats while actually abolishing our rights, freedoms, and liberties. No coercion necessary. We have been trained to love our servitude.

“A really efficient totalitarian state would be one in which the all-powerful executive of political bosses and their army of managers control a population of slaves who do not have to be coerced, because they love their servitude.” – Aldous Huxley – Brave New World

Arrogance, Desperation, Lies & Truth

“Facts do not cease to exist because they are ignored.” –Aldous Huxley

The level of data massaging by the government and their co-conspirators on Wall Street and in the corporate media is a futile attempt at a happy ending that will never come to fruition. The intensity and relentlessness with which the state and its quasi-state minions attempt to paint a false picture of economic recovery is equal parts arrogance and desperation. The arrogance is a function of successfully pulling off the greatest heist in world history from 2003 through 2008 with no adverse consequences, no criminal charges, no penalties for their crimes, and more power and wealth than they had prior to 2003. The only way to stop sociopaths is to throw them in jail or kill them. In our dystopian paradise of greed, they were rewarded with trillions in rescue packages by their cohorts in crime at the Federal Reserve and in Congress. They’ve paid themselves billions in bonuses for gorging at the Federal Reserve trough of QE and ZIRP. The desperation is borne from the fact that after $7.5 trillion of debt added by the Federal government and $3.5 trillion of debt created by the Federal Reserve since 2009, the Greater Depression for average Americans deepens by the day.

The men pulling the strings behind the scenes are drunk with power and their hubris allows them to believe their own infallibility and blinds them to the dire consequences for our country when their debt Ponzi scheme fails. But, as we grow ever closer to the day of reckoning, they will use every means at their disposal to paint a positive picture, regardless of the facts and reality for the average person. The examples of twisting, distorting and outright lying about the economic reality of our times are endless. These are some of the major false storylines peddled by our benevolent corporate fascist leaders:

The BLS reported 321,000 jobs added in November and the unemployment rate at 5.8%. Jobs are plentiful, based upon these statistics.

A skeptical critical thinking individual might ask a few questions or point out a few inconvenient facts the government purveyors of propaganda might not want us to ponder:

The non-manipulated, non-seasonally adjusted number of jobs in November FELL by 270,000. The BLS added 600,000 jobs as an adjustment to achieve the headline grabbing result.

If the jobs market is so good, why is the labor participation rate at a 30 year low of 62.8%?

Since 2007 the number of working age Americans has risen by 17 million, while the number of employed has risen by less than 1 million, but the unemployment rate is about the same.

Why would almost 14 million working age Americans leave the labor force since 2007 if the economy is booming and jobs plentiful, with 1.2 million leaving in the last 12 months?

Why would payroll tax receipts be flat with last year if millions of new jobs have been created?

If the country has really added 8 million jobs since 2010, how could real median household income FALL by 2.3%?

According to the government reported figures, the economy hasn’t been this strong since 2007. GDP has supposedly grown at greater than 4% over the last two quarters.

Anyone who is sentient knows consumer spending accounts for 68% of GDP. Capital investments that lead to long term prosperity continue to decline as a percentage of GDP from 20% in 2000 to 16% today. We’ve chosen consumption and financialization over savings and investment. This fact leads to some observations:

If GDP has actually grown by 20% since 2008 how does this correlate with a 6.9% decline in real median household income?

GDP has been goosed by a $69 billion increase in government spending, with the majority going to the military industrial complex. ISIS has been a godsend for our GDP and arms dealer profits.

GDP was increased retroactively by $500 billion last year based on a new way the government accounts for intangibles.

The surge in consumer expenditures over the last two quarters has been in the purchase of services. The higher costs for Obamacare are a boon for GDP. Are they a boon for your bank account?

The trade deficit has fallen as exports of petroleum products have temporarily provided a boost to GDP. The collapse in oil prices will reverse that trend rapidly.

According to the quasi-governmental mouthpieces at the Conference Board, consumer confidence is near a 5 year high, reflecting what should be robust spending.

So we are told by the representatives of corporatism that we are confident about the economy and the future. How does that measure up to the facts on the ground:

Black Friday weekend sales collapsed by 11% versus the previous year. As the pundits tried to blame it on on-line sales (10% of total retail sales), Cyber Monday also proved to be a dud.

If the average person is confident about the future and happy with their economic circumstances, why did they just vote to throw out the bums in November?

If consumers are confident, why have real retail sales, excluding subprime debt goosed auto sales, been flat for the last three months and up only 1% in the last year?

If consumers are so confident, why are credit card balances still $138 billion BELOW where they were in 2008? If all these new jobs are being created why is credit card debt lower than it was in mid-2010? Maybe consumers are so desperate they are using credit cards to pay utility and tax bills and not using them for frivolous Chinese crap at big box retailers.

The increased spending at grocery stores and restaurants is driven by food inflation, not foot traffic. Discretionary spending at furniture, electronics, and sporting goods stores is flat.

Department store sales continue to fall. Sears and JC Penney teeter on the verge of bankruptcy. Delia’s is liquidating and Radio Shack isn’t far behind. The major chains have completely stopped building new stores. The great bricks and mortar unwind relentlessly plods forward. In addition, online growth is stalling as states implement sales taxes.

According to the government, the deficit was ONLY $483 billion in 2014.

This is a real doozy. Obama has been touting how he has cut the deficit through his wise management of the budget. This is where government accounting is used by apparatchiks to mislead the public and obscure the truth. A few pertinent facts are always left out by the politicians touting deficit reduction:

Because of the budget impasse in 2013, the Federal government stopped updating the national debt on a daily basis, but we know from when they started counting again, the debt went up by $2.3 billion per day. Therefore, the national debt on October 1, 2013 was approximately $17.038 trillion. On October 1, 2014 the national debt was $17.875. Therefore, the national debt went up by $837 billion in 2014. Just a smidge higher than the reported deficit of $483 billion.

Interest is not paid on reported deficits. It’s paid on the national debt, so the massaged, manipulated and made over deficit is meaningless. The national debt was always slightly higher than reported deficits, but in the last few years the deviation has grown to a Grand Canyon size.

The deficit number has been artificially lowered by nothing other than accounting entry hocus pocus. The Federal Reserve increasing its balance sheet to $4 trillion out of thin air creates approximately $80 billion of phantom interest profits that are paid to the Treasury. Why don’t they increase their balance sheet to $40 trillion and eliminate deficits all together?

The biggest accounting scam is Fannie and Freddie. Just as the Wall Street banks have created fake profits through accounting entries regarding future losses, Fannie and Freddie have gone the extra mile in helping fake deficit reduction. These bloated insolvent government run pigs required a $187 billion taxpayer bailout in 2009. Amazingly, when you allow criminals to value their assets at whatever they choose, phantom profits flow like honey.

These two horribly run institutions of fraud “generated profits” of $129 billion in 2014 which were “paid back” to the Treasury. That is four times more than Apple or Exxon’s profits during a non-existent housing recovery. Why are their stocks trading at just over $2 per share if they are generating vastly more profits than they were in 2007 when their stocks were north of $70 per share? It’s because the profits are fake. Everyone knows it, but the Federal Deficit is reported $129 billion lower because these insolvent entities pretended to pay the taxpayer back. Accounting entries do not reduce deficits. Spending less than you generate in revenues reduces deficits.

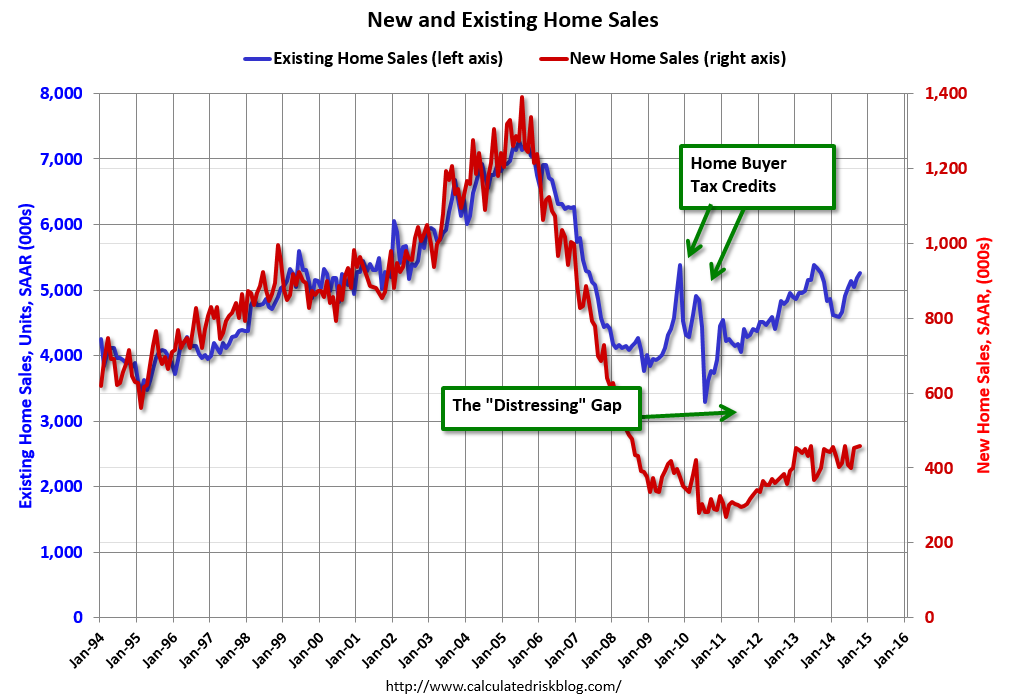

According to the government, we’ve experienced a strong housing recovery since 2010.

The supposed housing recovery storyline continues to be beaten like a dead horse by the Wall Street media (CNBC) and the shills at the NAR. Anyone with a functioning brain (eliminates CNBC bimbos, hacks, and Ivy League economists) can see there has been no real housing recovery:

The 24% rise in home prices (Case Shiller Index) since the 2012 low has been nothing more than a Wall Street hedge fund/Federal Reserve scheme to elevate prices and make Wall Street bank balance sheets less insolvent. Wall Street banks withholding foreclosures from the market while Wall Street hedge funds (Blackstone) use free money from the Fed to buy up housing and rent it out to former homeowners has enriched the .1% while destroying the dream of home ownership for millions.

The percent of first time home buyers remains near record lows, while speculators, flippers, hedge fund managers, and rich Chinese businessmen make up a record number of purchasers. The fact this is a fake housing recovery is proven by mortgage applications to purchase a home sitting at 1995 levels and 30% below 2009 recession lows. Maybe the fact real median household income is also at 1995 levels, real wages keep declining, and labor force participation is at 1978 levels has something to do with real people not being able to purchase a home.

Even with the artificial hedge fund demand, existing home sales are lower than 2013 and languishing at 1999 levels. They are still 25% below 2005 levels, despite the lowest mortgage rates in history. New home sales are a disaster, with no appreciable increase in two years. Apartment construction has far outpaced single family housing construction. After a five year housing recovery, new home sales languish at levels seen at the bottom of our last six recessions. New home sales are 65% below the 2005 peak and at levels seen in the early 1960’s when there were 130 million less people living in the country.

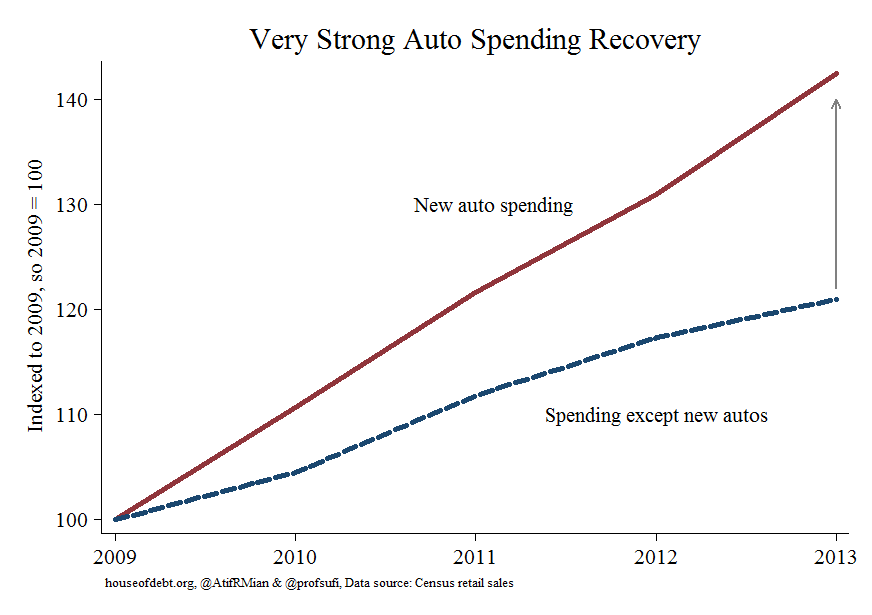

According to the corporate media, the auto market is hitting on all cylinders with annual sales of 16.4 million, the highest since 2006.

Pretending to sell automobiles to people without the means to pay you for the automobile is always a good business idea. Of course, when you have Ally Financial and the rest of the Wall Street banking cabal doling out 7 year 0% loans and subprime auto loans like candy, it’s easy to move inventory. The temporary boost to GDP by issuing more bad debt always works out in the long run. Right?

If the auto business is booming why have GM profits fallen from $9.2 billion in 2011 to $5.4 billion in 2013, and on course to fall to $4 billion in 2014? Record levels of channel stuffing produces sales gains, but no profits. Why is their stock 25% below its 52 week high and lower than it was in 2010 when it was IPO’d after being rescued by Obama?

If the auto business is booming why are Ford’s profits falling by 35% versus last year and lower than they were in 2010? Why is their stock price 16% below its 52 week high and still 20% below its 2010 price?

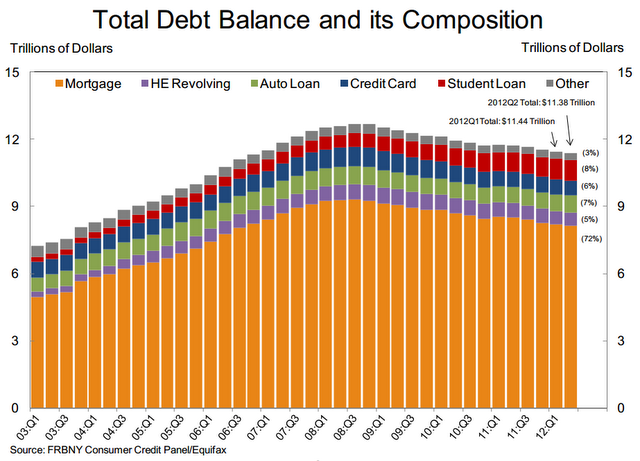

Auto loan debt is at an all-time high of $950 billion, up 33% since 2010 when the Fed, Wall Street, and the political class in the fetid D.C. swamp decided they needed new debt bubbles in auto loans and student loans to jump start our moribund economy.

There are 65 million auto loans outstanding, and the average debt now stands at $17,352. Over 30% of auto “sales” are actually leases. The rest are financed over an average of 65 months. Virtually all new car sales are nothing more than 3 to 7 year rentals. It’s amazing what easy money from the Fed can produce.

Over 31% of all new auto loans this year were to subprime borrowers. They now account for 36.5% of all outstanding auto loans. You become a subprime borrower by defaulting on previous debt obligations. In a shocking development, auto loan delinquencies surged by 13% in the last quarter, with subprime loan delinquencies skyrocketing by 18%. When has issuing billions of debt to subprime borrowers ever caused problems before?

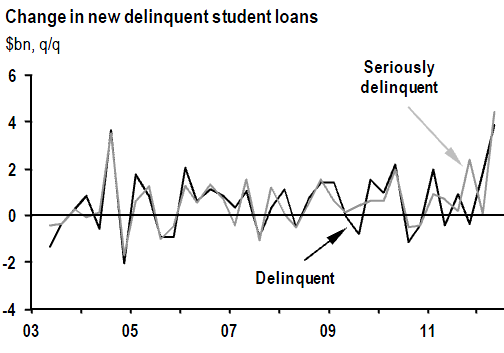

Only a University of Phoenix African Studies major is more of a subprime risk than the millions of ecstatic Escalade drivers cruising around our urban ghetto paradises. The average student loan debt is now $33,000. Until the Obama administration went Keynesian, student loan debt was primarily in the private sector. When Obama entered the White House total student loan debt was $620 billion and delinquencies totaled $50 billion. There are now $1.3 trillion of student loans outstanding, with the Federal government accounting for $830 billion and guaranteeing a large portion of the rest. Delinquencies have skyrocketed to $125 billion, as another taxpayer bailout beckons.

According to the corporate mainstream media pundits, the plunge in oil prices from $100 per barrel to $61 per barrel is unequivocally good for the economy. The shale oil boom has worked its magic and happy times are here again.

Sometimes you have to wonder whether the highly educated spokesmodels on the corporate mainstream media are really as vacuous and clueless as they appear or whether they are just paid to look pretty and mouth the corporate line. They seem incapable of comprehending the unintended consequences of various events. The collapse in oil prices is one of those events.

There is no doubt that lower oil prices will lower the price of gas for the average American. Estimates say they will save $368 per year, which can be spent elsewhere. The highly paid shill economists who declare this will boost spending seem to be math challenged. Retail sales figures include gas stations. What isn’t spent there will be spent in another category, most likely healthcare or groceries as prices in both areas continue to escalate. It’s a zero sum game. No new spending will occur.

The worldwide supply of oil has only increased marginally over the last few years. The U.S. shale boom has been offset by declines elsewhere (Libya, Iran, Mexico). The reason for the collapse is the same reason for the 2009 collapse – worldwide demand is contracting. Europe is in a depression. Japan is in a depression. Russia’s economy is contracting. China is decelerating rapidly. The U.S. demand is flat. The implications of another global recession after five years of central banks printing trillions of fiat currency are alarming to say the least.

The cost to extract shale oil and transport it to a refinery capable of processing it is high. Honest analysts will tell you that a price of $70 to $80 is required to breakeven. Most companies don’t build breakeven into their plans. Bakken shale oil sells at a discount of about $14 per barrel due to the difficulty of extraction, transport, and processing. It is now selling for $47 per barrel. The number of permits for new rigs fell by 40% in November when oil was still selling for $75 per barrel. Do you think permits for new wells will fall at a price of $61 per barrel? Capital spending by the energy industry accounted for 33% of all capital spending in the last few years. I’m sure some other industry will pick up the slack. Right?

It seems the shale oil boom has resulted in a few jobs being created since the 2010 recession trough. In fact the states where fracking is prevalent have accounted for all the job growth in the nation. I wonder if a shale oil bust will have any employment implications. There are 9.3 million jobs related to the energy industry across the country. The plunge in oil prices created by Saudi Arabia in the 1980s created a depression in Texas which contributed to the S&L crisis. This plunge will reveal who has been swimming naked in the high yield bond market and derivatives market.

These are just a few examples among a multitude of lies. Others include: stocks aren’t overvalued, gold isn’t money, inflation is good for you, and ISIS terrorists are an imminent threat to your way of life. Every feel good story fed to the masses by the oligarchs running this shitshow we call America is no different than the propaganda doled out by other infamous totalitarian regimes throughout history. We believe things because we’ve been conditioned to believe them. The crony capitalist oligarchs are intelligent enough to invent theories to explain how the world should work, but not intelligent enough to interpret their models correctly. When they act on their theories (Keynesianism), their actions appear to be those of a lunatic. Despite all evidence refuting their theories, their arrogance and hubris lead them to destruction. The collective insanity of this world is almost too much for a rational thinking person to grasp. The extremely wealthy men operating in the shadows will use every means at their disposal to retain power, enhance their wealth, and crush dissent.

“Being a card carrying member of the privileged class means never having to say I’m sorry, much less ‘not guilty.’ Power is doing what you want when you want, and consequences are for everyone else. Or perhaps these titans of modern industry and the halls of power are at heart just good natured bumblers, who in a genuine belief destroy lives and crash economies, while pursuing insane ideological assumption put forward by vested interests, all the while stuffing their pockets, and crushing all dissent with the political skills of a Machiavelli and the ruthlessness of Al Capone.” – Jesse

The two party system is nothing but a ruse designed to keep the people believing they have a say in how things are run in this country. Both parties support the military industrial complex. Both parties support the militarization of police forces around the country. Both parties support the mass surveillance of its citizens. Both parties do the bidding of their rich corporate and special interest benefactors. Both parties favor deficit spending for eternity. Both parties believe the government should expand its role in our everyday lives. Both parties do the bidding for and protect the Wall Street interests who really run this country. No more proof is needed than what has occurred over the last five years, as criminal Wall Street bankers were rewarded for their malfeasance with trillions of dollars from taxpayers and their puppets at the Federal Reserve. While we were allowing ourselves to be distracted, amused, entertained, and indebted, the oligarchs were busy conducting a silent coup.

“Let’s be clear about this, the oligarchs are flush with victory, and feel that they are firmly in control, able to subvert and direct any popular movement to the support of their own fascist ends and unslakable will to power.

This is the contempt in which they hold the majority of American people and the political process: the common people are easily led fools, and everyone else who is smart enough to know better has their price. And they would beggar every middle class voter in the US before they will voluntarily give up one dime of their ill-gotten gains.

But my model says that the oligarchs will continue to press their advantages, being flushed with victory, until they provoke a strong reaction that frightens everyone, like a wake-up call, and the tide then turns to genuine reform.” – Simon Johnson

The oligarchs have had a good run. The system cannot be reformed from within. The corruption runs too deep. The system is broken and can’t be fixed. There is no doubt in my mind that a collapse approaches which will make 2008/2009 look like a walk in the park. The anger, blame and retribution will sweep away the existing social order and replace it with something new. It will be up to the people to decide what happens next. We were warned two centuries ago by a wise man. Hopefully, we’ll get a 2nd chance.

“However political parties may now and then answer popular ends, they are likely in the course of time and things, to become potent engines, by which cunning, ambitious, and unprincipled men will be enabled to subvert the power of the people and to usurp for themselves the reins of government, destroying afterwards the very engines which have lifted them to unjust dominion.” – George Washington

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson

Does this chart portray an economic recovery in any way? Wages have been stagnant since the START of the supposed recovery in 2010. Real median household income, even using the highly understated CPI, is on a glide path to oblivion. You just need to observe with your own two eyes the number of Space Available signs in front of office buildings, strip centers and malls across America to realize we have further to fall. Low paying, part-time burger flipping jobs aren’t going to revive this debt saturated economic system. But at least the .1% are enjoying their Federal Reserve created high. Fiat is a powerful drug when administered in large doses to addicts on Wall Street.

The S&P 500 has risen from 666 in March of 2009 to 1,972 today. That is a 196% increase in a little over five years. During this same time, real household income has fallen by 7%. There have been a few million jobs added, while 11 million people have left the labor market. According to Robert Shiller’s CAPE ratio, the stock market valuation has only been higher, three times in history – 1929, 1999, and 2007. He seems flabbergasted by why valuations are so high. Sometimes really smart people can act really dumb.

The Federal Reserve balance sheet was $900 billion before the 2008 financial crisis. Today it stands at $4.4 trillion. The Fed has increased their balance sheet by 220% since the March 2009 market lows. Do you think there is any correlation between the Fed puppets printing $2.4 trillion and handing it to their Wall Street puppeteers, who used their high frequency trading supercomputers and ability to rig the markets so they never lose, and the third stock bubble in the last 13 years? It’s so self evident that only an Ivy League economist or CNBC anchor wouldn’t be able to see it.

Let’s look at the amazing stock market recovery without Federal Reserve heroine pumped into the veins of Wall Street banker addicts. If you divide the S&P 500 Index by the size of the Federal reserve balance sheet, you see the true purpose of QE1, QE2, and QE3. It wasn’t to save Main Street. It was to save Wall Street. Without the Federal Reserve funneling fiat to the .1% banking cabal and creating inflation in energy, food, and other basic necessities for the 99.9%, there is no stock market recovery. The recovery has occurred in Manhattan and the Hamptons. It’s been non-existent for the vast majority of people in this country. The wealth effect and trickle down theory have been disproved in spades. The only thing trickling down on the former middle class from the Fed is warm and yellow.

The entire stock market advance has been created on record low trading volumes and record high levels of monetary manipulation. Even though the Federal Reserve has driven senior citizens further into poverty with 0% interest rates, those with common sense have refused to be lured back into the lion’s den. They have parked record levels of fiat in no interest bank and money market accounts. They are tired of being muppets led to slaughter.

Quantitative easing was supposed to force little old ladies into the stock market and consumers to spend their debased dollars before they lost more value. The spending would revive the dormant economy just as the Keynesian text books promised. It didn’t happen. The peasants haven’t cooperated. Quantitative easing and ZIRP sapped the life from the middle class as their wages have stagnated and their living expenses have skyrocketed. Mission Accomplished by the Fed. Of course, the CNBC bimbos and shills would declare this $10.8 trillion to be money on the sidelines ready to boost the stock market ever higher. I love that storyline. It never grows old.

The MSM, government and Wall Street continue to flog the story about a housing recovery. It’s been nothing but a confidence game based upon the Fed’s easy money and the Wall Street scheme to buy up foreclosed properties with the Fed’s money. The scheme was to artificially boost home prices by restricting home supply through foreclosure manipulation, in order to allow the insolvent Wall Street banks to get out from under their billions in toxic mortgage loans.

Shockingly, the Case Shiller home price index has soared by 25% since 2012 despite first time home buyers being virtually non-existent and mortgage applications plunging to 14 year lows. How could that be? Don’t people need mortgages to buy houses? Isn’t real demand necessary to drive prices higher? Not when Uncle Ben and Madam Yellen are in charge of the printing press. Housing bubble 2.0 has arrived. I wonder if the Federal Reserve balance sheet increase of 50% since 2012 has anything to do with the new housing bubble.

It seems a similar result is obtained when dividing the Case Shiller Index by the size of the Fed’s balance sheet. The real housing market for real people is worse than it was in 2009. The national home price increase has been centered in the usual speculative markets, aided and abetted by the Fed’s easy money, managed by the Wall Street hedge funds, and exacerbated by the late arriving flippers who will be left holding the bag again. The Fed/ Wall Street scheme has priced young people out of the market and has failed to ignite the desired Keynesian impact. Investors/flippers account for 34% of all home sales. Foreigners with no knowledge of value metrics account for 30% of all home sales. The lesson of history is that most people don’t learn the lessons of history. The 2nd housing bubble in seven years is seeking a pin.

If ever you needed proof of the confidence game in its full glory, the chart below from Zero Hedge says it all. Mortgage rates have been falling for the past year, home builders have been reporting soaring confidence about the future, and the National Association of Realtors keeps predicting a surge in home buying any minute now. One small problem. Mortgage applications are in free fall, new home sales are at 1991 levels, and existing home sales are falling. Home prices have peaked and are beginning to roll over. The Wall Street hedgies are all looking to exit stage left. Young people are saddled with over a trillion of government issued student loan debt and millions of older subprime borrowers have been lured into more auto loan debt. Home sales will be stagnant for the next decade.

Quantitative easing will cease come October, unless Yellen and Wall Street can create a new “crisis” to cure with more money printing. By every valuation measure used over the last 100 years, stocks are overvalued by at least 50%. By historical measures, home prices are overvalued by at least 30%. Ten year Treasuries are yielding 2.4%, while true inflation is north of 5%. With real interest rates deep in negative territory, the bond market is even more overvalued than stocks or houses. These simultaneous bubbles have been created by the Federal Reserve in a desperate attempt to keep this debt laden ship afloat. Their solution to a ship listing from too much debt was to load it down with trillions more in debt. The ship is taking on water rapidly.

We had a choice. We could have bitten the bullet in 2008 and accepted the consequences of decades of decadence, frivolity, materialism, delusion and debt accumulation. A steep sharp depression which would have purged the system of debt and punishment of those who created the disaster would have ensued. The masses would have suffered, but the rich and powerful bankers would have suffered the most. Today, the economy would be revived, saving and investing would be generating needed capital for expansion, and banks would be doing what they are supposed to do – lending money to businesses and individuals. Instead, the Wall Street bankers won the battle and continue to pillage and loot the national wealth while impoverishing the masses.

The arrogance, hubris and contempt for morality displayed by the ruling class is breathtaking to behold. They think they are untouchable and impervious to norms followed by the rest of society. They may have won the opening battle, but will lose the war. Discontent among the masses grows by the day. The critical thinking citizens are growing restless and angry. They are beginning to grasp the true enemy. The system has been captured by a few malevolent men. When the stock, bond and housing bubbles all implode simultaneously, all hell will break loose in this country. It will make Ferguson, Missouri look like a walk in the park. I wonder if the occupants of the Eccles building in Washington DC will get out alive.

“It is well enough that people of the nation do not understand our banking and money system, for if they did, I believe there would be a revolution before tomorrow morning.” – Henry Ford

Auto lending is currently 40% higher than the last peak in 2003.

Auto leases are growing at a 20% annual rate.

The average car loan term is now 66 months, the highest in U.S. history.

The average amount financed is at an all-time high of $27,612.

The average monthly payment reached a new all-time high of $474.

The percentage of subprime deadbeats getting car loans has soared to 34% of all loans.

Lenders are doling out loans that are 25% higher than the value of the autos they are “selling”. A new car depreciates 10% the second you drive it off the lot.

Real household income is 7% lower than it was in 2007, while gas, utilities, food, health insurance, and taxes are significantly higher. The entire consumer spending “recovery” has been nothing but another Federal Reserve/US Treasury engineered debt bubble of auto and student loans. The piper will be paid. The bubble will burst. The losses will be epic. Who coulda knowed? I bet you can’t wait to bail out Wall Street and Obama again. You’ll do it for the children.

One of the many oddities of this cycle is that many things that were good during the post-WW2 era have become bad in the era now starting (unrecognizably so, as we remain unaware of our changed circumstances). Like debt. Such as auto loans. Our use of debt gives clues to our future..

Consumer debt in the old world, and the new

During the post-WW2 era increasing debt supercharged economic growth for the young and rapidly-growing West. But after 60 years of this our societies now carry massive debt loads, both public and private — while the numbers of elderly grow (who experience a crash of income upon retirement, plus rising costs to society for their pensions and health care). Carrying our current load might prove difficult; adding to it now is madness.

Plus, there are other factors in play. Fifty years of growing inequality, for still poorly-understood reasons, have hollowed out the middle class — diminishing their ability to carry their existing debt, making them dependent on borrowing to maintain their lifestyle.

Some take another step beyond borrowing. Borrowing to buy cars and homes results in slowly accumulating equity, one of the most common ways middle class households save. Increasingly Americans abandon buying with debt for renting. Rent homes instead of owning. Renting cars (leasing) instead of owning.

Automobile sales point to our new world

Accelerating borrowing was a natural leading indicator of economic recoveries during the post-WW2 era. So economists see the waves of desperate borrowing by consumers since 2000 as a good thing. Hence their excitement about the subprime lending boom that drove the housing bubble. Such as today’s subprime borrowing to buy cars.

The extreme case of this blindness to our changed conditions is glee about the shift to renting cars (aka leasing). It shows vibrant demand for cars! As we see in this excerpt from a report by BofA-Merrill global economist Ethan Harris, 6 August 2014, showing that after mid-2012 leasing grew faster than total spending on vehicles (2012 saw many such transition points for the US economy).

Households go for the low capital option: leasing soars:

Household outlays on leasing are booming at a 20% yoy pace — a clear sign that demand for vehicles is alive and kicking. With average lease payments lower than typical monthly ownership costs and with a down-payment not typically required to enter into a lease, the surge in vehicle leasing is likely a sign that financial restraints are still holding back some would-be buyers. Thus, as the economy improves, bottled-up household demand for vehicles could translate to higher sales.

Yes, in our society demand is “alive and kicking” by subprime households for cars bought with low-rate loans on easy terms — or even just renting (aka leasing). But does it point to an economic recovery — or exhaustion?.

The terms are very easy

Turning back to people at least attempting to buy, there are four dimensions to consumer loans: the creditworthiness of the borrower, the interest rate of the loan, the length of the loan, and the collateral (the loan to value ratio). A report by Experian Automotive, 2 June 2014, describes the first three.

… average automotive loan term reached an all-time high of 66 months … loans with terms 73-84 months grew to 25% of all loans originated during the quarter. …

The average amount financed for a new vehicle loan also reached an all-time high of $27,612 in Q1 2014, up $964 from the previous year. In addition, the average monthly payment for a new vehicle loan reached its highest point on record at $474 in Q1 2014, up from $459 in Q1 2013.

… Market share for nonprime, subprime and deep subprime new vehicle loans in Q1 2014 rose to 34%.

Six- and seven-year-long auto loans! At what point will the borrower have equity in their cars? Especially since these are probably the subprime borrowers that make up 1/3 of auto lending.

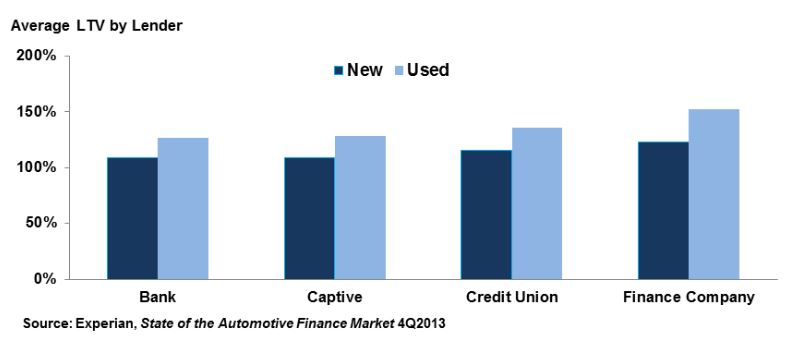

The fourth factor is equally ugly. Lenders are lending more than the value of the collateral (i.e., including closing costs and rolling over the deficit of the buyers’ trade-in). These are averages; half of loans have even higher LTVs. From Semiannual Risk Perspective, Office of the Comptroller of the Currency, Spring 2014:

Why are these numbers important?

The changing nature of auto sales tell us much about ourselves. They show how economists do not see the new era beginning. They imply slower growth in the future, as a household’s longer loans with smaller down payments push out their ability to buy their next car. They tell us something about the recovery.

Auto sales have been a major driver of the recovery. Most economists expect auto sales to continue growing, helping power the long-awaited acceleration from slow ~2% growth to 3% or beyond. So the sustainability of auto sales — and the borrowing and leasing that fuels them — matter.

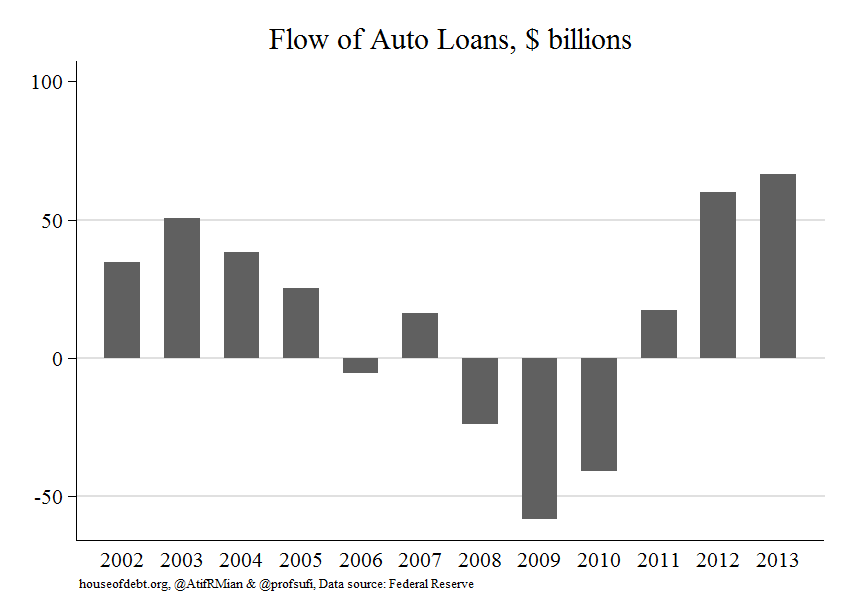

Atif Mian and Amir Sufi show the importance of auto loans to auto sales, and of auto sales to consumer sales. These are from their post “Another Debt-Fueled Spending Spree?“, 31 March 2014. First, lending is rapid:

Second, since the crash, auto sales have grown much faster than overall consumer spending.

Auto sales have been one of the few drivers of this recovery. They have been pushed up by easy credit, longer terms, lower credit quality, and sky-high loan-to-value ratios. But these loans lock the buyer out of the market for years to come. Charge-off for lenders will rise, and in response lenders will re-tighten their underwriting standards. And outstanding auto loans, once useful in the prior era, will become malignant. By Editor, Fabius Maximus.

As usual, the corporate MSM is attempting to spin a shitty retail sales report into a report showing consumers are back baby. They desperately want this storyline to convince the sheeple that all is well in our consumer spending dependent economy. The headline on the Rupert Murdoch owned Marketwatch was:

U.S. RETAIL SALES RISE AT A BRISK PACE

I guess their definition of brisk and my definition of brisk are slightly different. The storyline during the winter was the shitty retail sales were due to the cold weather. We were told retail sales would skyrocket come spring. Well let’s examine what has happened from March through May, which the last time I checked constituted Spring. Here is a link to the data I’ll be referencing:

Excluding the debt financed auto sales, retail sales grew by an infinitesimal .07%.

We know for a fact that auto loan length is at a record high of 66 months, auto leases are at an all-time high of 26%, and 34% of all loans are being made to people with bad credit. Does anyone really think these are sales? They constitute 20% of all retail sales in this country.

Retail sales are $18 billion higher this May versus last May. $8.4 billion, or 47% of that increase, is attributable to Government Motors through Ally Financial and the rest of the Wall Street bankers doling out easy money loans to deadbeats.

During this supposed retail recovery from the dreadful winter, total retail sales have grown by a total of $3.6 billion from March through May. That is a miniscule 0.8%. When you back out the auto sales, it is a microscopic 0.5%. On an annualized basis retail sales are growing at below 2%.

With inflation running at 5% or higher, REAL retail sales are declining. This is why retailers are reporting horrible profit results.

Over the last three months retail sales, excluding autos, has risen $1.7 billion. You’ll be thrilled to know that $0.6 billion of that increase is from you paying more at gasoline stations. That is 34% of the increase. Another $0.8 billion was spent at building and materials stores to make repairs on your houses damaged from the winter storms.

Over the last three months sales have declined at electronics & appliance stores, food stores, restaurants and for all the idiots thinking on-line is the reason bricks and mortar is dying – INTERNET SALES DECLINED. I guess sales tax does matter.

Again, the MSM and the Wall Street shyters are wrong. There is no retail recovery. It was not the weather. The only retail being done is through easy long-term auto and home furnishing debt. The loan losses will follow when the next financial crisis arrives. The retail death rattle grows ever louder as Radio Shack announced results that foretell a bankruptcy filing before year end. That will mean 5,000 more SPACE AVAILABLE signs in strip malls and regional malls across America.

The corporate MSM continues to do their part. They reported STRONG growth in consumer credit in September. That is awesome. Strong is such a great word. It make me feel good, because we all know taking on more debt is always a good thing in America. Just one little problem when you actually look at the data.

Non-revolving credit jumped by $14.3 billion to an all-time record of $1.885 trillion. It was at $1.52 trillion in 2007, before the financial crisis. Revolving credit (also known as credit card debt) fell for the 2nd straight month and is now at the same level as the fourth quarter of last year. It is $158 billion below the level of 2007. With no income growth and declining credit card spending, can someone explain how retailers are going to increase sales?

Non-revolving credit is made up of two main pieces – student loan debt and auto loan debt. The STRONG growth in consumer credit was attributed to a $13.8 billion SURGE in student loan debt and a $500 million increase in auto loans. What do these two areas have in common? You guessed it – Obama is spreading the debt around. The Federal government is taking your tax dollars and doling it out to clueless University of Phoenix enrollees getting an online degree in African Studies or Lesbian Literature. His friends at Ally Financial are making sure everyone in West Philly gets their very own Cadillac Escalade. Credit scores be damned.

So this is your STRONG demand story in a nutshell. So it goes.

Consumer credit jumps again in September

WASHINGTON (MarketWatch) – U.S. consumers increased their debt in September by a seasonally adjusted $11.4 billion, the second straight strong gain, the Federal Reserve reported Wednesday. The increase in September was stronger than the roughly $10 billion gain expected by Wall Street economists. The gain in August consumer credit was revised up slightly to $18.3 billion increase from the initial estimate of $18.1 billion. For the third quarter, consumer credit increased at a 4% annual rate. As in the prior month, the increase in September credit came from a jump in non-revolving debt such as auto loans, personal loans and student loans. These loans experienced a $14.3 billion jump in September after a $14.1 billion gain in the prior month. Analysts said that student loans, now captured under the federal government subcomponent, are driving credit higher. Credit-card debt fell by $2.9 billion in the month after a $4.3 billion increase in August.

Have you heard the news? Auto sales are booming. Total sales for the month of August were 1,285,202 vehicles, according to Autodata Corp, the highest monthly sales figure for any August since 2007, when 1.47 million autos were sold in the United States. Year to date auto sales have totaled 9.7 million and are on track to reach 14.5 million. Between 2006 and 2007, auto sales ranged between 16 million and 18 million. They crashed below 10 million in 2009. The Keynesians running our government have pulled out all the stops to restart this engine of consumer spending. First they wasted $3 billion of taxpayer funds on the Cash for Clunkers debacle. Almost 700,000 perfectly good cars were destroyed in order to keep union workers happy. This Keynesian brain fart distorted the used car market for two years, raising prices for cars needed by the working poor. After that miserable failure, they realized the true secret to selling vehicles is to give them away to anyone that can scratch an X on a loan document, with 0% interest for 60 months, financed by Federal government controlled banking interests. Add in some massive channel stuffing and presto!!! – You’ve got an auto sales boom.

General Motors sales are up 3.7% over 2011. Ford Motors sales are up 6% over 2011. The Obama administration continues to tout their saving of the U.S. auto industry with their bailout in 2009 that saved unions and screwed bondholders. If this strong auto recovery is not an illusion, how do you explain the two charts below? General Motors stock is down 42% since 2011. The highly proclaimed success story called Ford Motors has seen their stock collapse by 50% since 2011. This is surely a sign of tremendous success and anticipation of soaring profits for these bastions of American manufacturing dominance.

This is America, land of the delusional and home of the vain. The appearance of success is more important than actual success. The corporate mainstream media dutifully reports the surge in auto sales is surely a sign the economy is recovering and the consumer has finished deleveraging and is ready to spend again. The government propaganda machine proclaims the surging auto sales are due to their wise and forward thinking policies (like the Chevy Volt). Luckily for them, there are millions of gullible Americans who believe the storyline and are easily convinced that driving a $30,000 new car, financed over seven years, makes them a success. The decades of Bernaysian marketing propaganda has worked its magic on the government educated, math challenged citizenry. There are only two things that matter to the non-thinking auto buyer (renter) – the monthly payment and what the next door neighbor and his coworkers will think. Buying a fuel efficient car they can afford, paying it off in three or four years, and driving it for ten years, while saving the monthly car payment, is what a practical, rational thinking person would do. The fact that only 20% of the 9.7 million vehicles sold this year have been small cars and the average sales price of new cars sold is now $31,000 proves Americans are still living in a delusional fantasyland of cheap gas and monthly payments for eternity.

As gas prices surpass $4 per gallon across the country, somehow 4.7 million of the 9.7 million vehicles sold in 2012 have been pickups, vans, crossovers or SUVs. Three of the top eight selling vehicles are pickups. Luxury vehicle sales are booming, with Mercedes, BMW, Porsche, Land Rover and Audi showing double digit percentage sales gains over 2011. We’ve entered a recession, gas prices are approaching all-time highs, job growth is pitiful, and Americans continue to buy luxury gas guzzlers on credit. This will surely end well.

The average payment on a new car in 2012 is $461. For used cars, the average monthly payment is $346. Today, 77% of new car purchases are financed. About half of all used vehicles involve financing. Of those cars financed, 89% are through a loan vs. 11% with a lease. A critical thinking person might wonder how a country with 4 million less employed people than we had in 2007, median household net worth down 35%, and real wages lower than they were in 2007, could be experiencing an auto boom. The answer is a government/corporate/banker/media effort to funnel taxpayer funds to deadbeats across the land in a fruitless attempt to create a facade of recovery. Our governing elite are convinced that more debt peddled to the masses is the path to recovery for an economy that imploded due to excessive debt peddled to the masses in the first place. Essentially, it comes down to who benefits from the peddling of debt. It isn’t the masses, as they become enslaved in the chains of debt and monthly payments in perpetuity. Debt peddling benefits Wall Street bankers, politicians, and mega-corporations selling crap to the masses.

The storyline being sold to the vegetative dupes (watching Honey Boo Boo) that occupy space in this delusional paradise we call America, by the corporate media, is that consumers have deleveraged and are ready to resume their “normal” pattern of spending money they don’t have on stuff they don’t need. Of course, the facts always seem to get in the way of a good yarn. Consumers have never deleveraged. Consumer credit outstanding is at an all-time high of $2.58 trillion. The decline from $2.55 trillion in 2008 to $2.4 trillion in 2010 was NOT deleveraging. It was the Wall Street Too Big To Fail banks taking a big dump on the American taxpayers. They passed their bad debts to you through TARP, the Federal Reserve buying their toxic “assets”, and ZIRP.

Revolving credit (credit card) debt peaked at just above $1 trillion in 2008 and “declined” to $850 billion during 2010. The media storyline is that you buckled down and paid off your credit cards, therefore depressing consumer spending and creating a recession. Sounds convincing except for the fact that it’s a load of bullshit. The Federal Reserve’s own data proves it to be false. Your friendly Wall Street banks have written off $213 billion of credit card debt since 2008 and passed the bill to the few remaining taxpayers in this country. For the math challenged, this means that consumers have actually INCREASED their credit card debt by $68 billion since 2008. The bad news for our Chinese crap peddling mega-retailers is that the significantly poorer average middle class American household is using their credit cards to pay their property tax bills, IRS bills, and utility bills in order to survive.

Credit Card Charge-off in Dollars 2005 – 2011 — Not Seasonally Adjusted:

Year

Dollar Amount

2011

$46,017,459,671

2010

$75,090,106,350

2009

$83,179,901,000

2008

$53,506,353,600

2007

$38,149,440,000

2006

$32,111,934,400

2005

$40,634,994,400

Year & Quarter

Dollar Amount

2012Q1

$8,772,385,443

The category of debt that barely budged in the 2009 collapse was non-revolving credit. It stayed in the $1.5 trillion range in 2009 and has since surged to over $1.7 trillion in 2012. What could possibly have made this debt skyrocket by $200 billion when the GDP has only grown by 12% over the same time frame? You guessed it – your corporate fascist friends in Washington DC and on Wall Street. Non-revolving debt consists of auto loan debt of $663 billion and student loan debt of approximately $1 trillion. Student loan debt has shot up by $300 billion since 2008. This student loan debt is being distributed, like candy by a pedophile, from the Federal government in an effort to artificially hold down the unemployment rate.

Approximately $500 billion of the student loan debt is held directly by the Federal government, up from $100 billion in 2008. The Feds guarantee the majority of the remaining student loan debt. Can you think of a more subprime borrower than a 40 year old former construction worker getting a liberal arts degree from the University of Phoenix, sitting at his computer in his underwear scratching his balls, and paying with a $10,000 Federal student loan from you? This fraudulent attempt to obscure the true employment situation will end in tears for the borrowers and the American taxpayer. It’s tough to make a loan payment without a job. The student loan bailout is just over the horizon and will cost you at least $300 billion. Delinquencies are already off the charts.

When has offering low interest debt in ample portions to people without jobs, income or assets ever backfired before? The bankers and politicians that control this country seem to be a one-trick pony. They will never admit that debt is the problem and reducing it the solution. The real solution would make them poorer, so their solution is to pour gasoline on the fire with more debt at lower interest rates to more people. The addict will keep injecting more poison into their system until sudden death. The bankers and politicians know we are a car-centric society and appeal to our vanity and poor math skills to keep the game going.

During the first quarter of this year, total U.S. car loans totaled $52.5 billion. That’s 49% higher than the same period in 2009. Also during the first quarter, the average amount financed on new vehicles rose by $589, to $25,995, and for used cars by $411, to $17,050. Furthermore, buyers are stretching out payments for longer terms: The average length of new- and used-vehicle loans jumped a full month during the first three months of this year, to 64 and 59 months, respectively. The surge in auto sales is being completely driven by doling out more loans for a longer time frame to deadbeat borrowers. Subprime auto loans now make up 45% of all car loans and the vast majority of all used car loans. They have even created a category called Deep Subprime. Borrowers classified as “deep subprime” (i.e. those with Vantage scores below 600) account for 10.7% of auto loans. You can also classify them as loans that will never be repaid.

Two thirds of all car sales are for used cars, so the fact that 37% of all new cars are being sold to subprime borrowers is exacerbated by the ridiculous lending practices for used cars. The fine folks at Zero Hedge have provided the outrageous data and a chart that proves beyond a shadow of a doubt what awaits the American taxpayer – another bailout. Zero Hedge has already revealed the GM fake recovery by detailing their channel stuffing over the last two years. Now they’ve dug up more dirt on why car sales are surging. What could possibly go wrong providing loans for more than the value of the asset to people with a history of not paying their debts?

Subprime borrowers received 56.46% of loans on used cars in the quarter, up from 52.70% a year earlier.

The average loan-to-value on new cars was 109.55%

The average used car loan-to-value ratio rose to 126.62%

77% of Subprime Auto Loans are for a period greater than five years

It’s amazing how many cars you can sell when you aren’t worried about getting paid. This is the beauty of a fiat currency, a printing press, and a taxpayer available to pick up the tab after the drunken party gets out of hand. The chart below provides the details of our superhighway to disaster. The percentage of used car loans to prime borrowers is now at an all-time low, while the percentage of loans to subprime borrowers is near all-time highs reached just prior to the 2008 crash. When lenders cared about being paid back in the early 2000’s, they rarely made loans longer than five years. Today, more than 77% of all subprime used car loans are longer than five years and average FICO scores are now well below 600. Just to clarify – if your FICO score is below 600 – YOU ARE A DEADBEAT.

When you start to connect the dots, things that didn’t seem to make sense begin to crystallize. This is all part of the master plan concocted by Bernanke, Geithner, Obama and the Wall Street Shysters. The auto section of my local paper now makes sense. Offers of 7 year financing at 0% interest and monthly lease offers of $150 to $200 for brand new cars now are understandable. The newer model BMWs, Cadillac Escalades, Volvos, and Jaguars I see parked in front of the low income luxury gated townhome community in West Philadelphia now makes sense. A pizza delivery guy driving a new Lexus is now explainable.

The master plan is fairly simple. The Federal Reserve lends money to the Wall Street banks for 0% interest. These banks then turn around and provide credit card debt at 13% interest, new & used car loans to prime borrowers at 5% interest, and new & used car loans to subprime borrowers at 16%. When you can borrow for free, you can take a chance that a significant number of your borrowers will default. Essentially, Ben Bernanke is screwing the prudent savers and senior citizens by paying them 0.15% on their savings in order to subsidize the bankers that destroyed the country so they can make auto loans to the same people who took out the zero percent down interest only no doc mortgage loans in 2005. In addition, Wall Street knows the Bernanke Put is still in place. If and when these subprime loans explode in their faces again, Bennie, Timmy and Obamaney will come to the rescue with your tax dollars. Its heads you lose, tails you lose, again.

The chart below is like a who’s who of TARP recipients. The top 20 auto lenders control half the market. And look at the leader of the pack. Our friends at Ally Bank are the market share leader. You remember Ally Bank – they conveniently changed their name from GMAC (also known as Ditech – biggest subprime mortgage lender) after losing billions and being bailed out by you. They still owe you $11 billion and are 85% owned by the U.S. Treasury. No conflict of interest there. You have the biggest auto lender on earth controlled by the Obama administration. Do you think they have an incentive to make as many loans as humanly possible to help Obama create the illusion of an auto recovery? The only downside is for the American taxpayer when we have to eat billions more in Ally/GMAC losses. This insolvent excuse for a lending institution has been extremely aggressive in the subprime auto lending market and has forced the other wannabes – Wells Fargo, JP Morgan, Capital One and Bank of America – to lower their lending standards. Does this scenario ring a bell?

We’ve become a subprime auto nation, addicted to easy debt, living lives of hope, delusion and minimum monthly payments. Storylines about economic recovery, fraudulent government statistics showing lower unemployment, feel good propaganda from the corporate mainstream media, and a return to easy money debt fueled spending does not constitute a real recovery. Until the bad debt is purged from the system and saving takes precedence over spending, the country will stagger and ultimately fall under the weight of its immense debt. We are lost in a blizzard of lies. This subprime fueled engine of recovery will propel the country into the same canyon of reality we entered in 2008. The crack up boom approaches.

“Thousands upon thousands are yearly brought into a state of real poverty by their great anxiety not to be thought of as poor.” – Robert Mallett

I hear the term de-leveraging relentlessly from the mainstream media. The storyline that the American consumer has been denying themselves and paying down debt is completely 100% false. The proliferation of this Big Lie has been spread by Wall Street and their mouthpieces in the corporate media. The purpose is to convince the ignorant masses they have deprived themselves long enough and deserve to start spending again. The propaganda being spouted by those who depend on Americans to go further into debt is relentless. The “fantastic” automaker recovery is being driven by 0% financing for seven years peddled to subprime (aka deadbeats) borrowers for mammoth SUVs and pickup trucks that get 15 mpg as gas prices surge past $4.00 a gallon. What could possibly go wrong in that scenario? Furniture merchants are offering no interest, no payment deals for four years on their product lines. Of course, the interest rate from your friends at GE Capital reverts retroactively to 29.99% at the end of four years after the average dolt forgot to save enough to pay off the balance. I’m again receiving two to three credit card offers per day in the mail. According to the Wall Street vampire squids that continue to suck the life blood from what’s left of the American economy, this is a return to normalcy.

The definition of normal is: “The usual, average, or typical state or condition”. The fallacy is calling what we’ve had for the last three decades of illusion – Normal. Nothing could be further from the truth. We’ve experienced abnormal psychotic behavior by the citizens of this country, aided and abetted by Wall Street and their sugar daddies at the Federal Reserve. You would have to be mad to believe the debt financed spending frenzy of the last few decades was not abnormal.

The Age of Illusion

“Illusions commend themselves to us because they save us pain and allow us to enjoy pleasure instead. We must therefore accept it without complaint when they sometimes collide with a bit of reality against which they are dashed to pieces.” –Sigmund Freud

In my last article Extend & Pretend Coming to an End, I addressed the commercial real estate debacle coming down the pike. I briefly touched upon the idiocy of retailers who have based their business and expansion plans upon the unsustainable dynamic of an ever expanding level of consumer debt doled out by Wall Street banks. One only has to examine the facts to understand the fallacy of a return to normalcy. We haven’t come close to experiencing normalcy. When retail sales, consumer spending and consumer debt return to a sustainable level of normalcy, the carcasses of thousands of retailers will litter the highways and malls of America. It will be a sight to see. The chart below details the two decade surge in retail sales, with the first ever decline in 2008. Retail sales grew from $2 trillion in 1992 to $4.5 trillion in 2007. The Wall Street created crisis in 2008/2009 resulted in a decline to $4.1 trillion in 2009, but the resilient and still delusional American consumer, with the support of their credit card drug pushers on Wall Street, set a new record in 2011 of $4.7 trillion.

A two decade increase in retail sales of 135% might seem reasonable and normal if wages and household income had grown at an equal or greater rate. But total wages only grew by 125% over this same time frame. Interestingly, the median household income only grew from $30,600 to $49,500, a 62% increase over twenty years. It seems the majority of the benefits accrued to the top 20%, with their aggregate share of the national income exceeding 50% today, versus 47% in 1992 and 43% in the early 1970s. The top 5% are taking home in excess of 21% of the national income versus less than 19% in 1992 and 16% in the early 1970s. It appears the financialization of America, after Nixon closed the gold window and allowed unlimited money printing by the Federal Reserve, has benefitted the few, at the expense of the many. The bottom 80% of households has seen their share of the national income steadily decrease since the early 1970s. There are 119 million households in the United States and 95 million of these households have seen their wages and income stagnate. One might wonder how the 80% were able to fuel a two decade surge in retail sales with such pathetic wage growth.

Your friendly Wall Street banker stepped into the breach and did their part to aid a vast swath of Americans to enslave themselves in debt. As the chart above reveals, the slave owners on Wall Street have been the chief beneficiary of the decades long debt deluge. It seems that charging 18% interest on hundreds of billions in credit card debt can be extremely profitable for the shyster charging the interest. Decades of mailing millions of credit card offers, inundating financially ignorant Americans with propaganda media messages convincing them they needed a bigger house, fancier car, or latest technological gadget and creating complex derivatives that permitted banks to market debt to people guaranteed not to pay them back but not care since they sold the packages of these toxic AAA rated loans to pension funds and little old ladies, has done wonders for earnings per share, stock option awards, executive salaries and bonus pools. It hasn’t done wonders for the net worth of the average American who has been entrapped in the chains of debt, forged link by link over decades of purposeful deception and willful delusion.

The 135% increase in retail sales over two decades may have been slightly enhanced by the 213% increase in consumer credit outstanding. Consumer revolving credit rose from $800 billion to the current level of $2.5 trillion over the last two decades. Those 15 credit cards in our possession were so easy to use that we financed our trips to Dollywood, Sandals, and Euro-Disney, in addition to financing our 72 inch 3D HDTVs, granite countertops, stainless steel appliances, decks, pools, recliners with a built in fridges, home theatre rooms, Coach pocketbooks, Jimmy Cho shoes, Rolex watches, yachts, bigger and better boobs, and of course our smokes and beer. Much has been made about the great de-leveraging by the American consumer. There’s just one inconvenient fact – it hasn’t happened – yet.

Total consumer credit outstanding peaked at $2.58 trillion in July 2008. Today it stands at $2.50 trillion. Revolving credit card debt peaked at $972 billion in September 2008 and subsequently declined to $790 billion by April 2011. It now stands at $801 billion, as living well beyond our means has resumed its appeal. Meanwhile, non-revolving credit for automobiles, boats, student loans, and mobile homes peaked at $1.61 trillion in July 2008 and “crashed” all the way down to $1.58 trillion in May 2010. Once Bennie fired up the printing presses, the government car companies decided to make subprime auto loans again and the Federal government started doling out student loans like a pez dispenser, all was well in the non-revolving consumer loan world. The debt outstanding has soared to $1.7 trillion, a full $90 billion above the pre-crash peak. So, after three and a half years of “austerity” and supposed deleveraging, consumer debt outstanding has fallen by 3%.

The Big Lie of austerity and consumer deleveraging is unquestioned by the talking heads in the mainstream media. They are incapable or unwilling to examine the actual data which substantiates the fact that Americans have NOT deleveraged and have NOT taken austerity to heart. The most basic facts fly in the face of consumers even having the wherewithal to pay down their debt. Median household income has declined from $50,300 in 2008 to $49,400 today. There are 5 million less people employed today than employed in 2008. Total wages in the country have only grown from $6.6 trillion in 2008 to $6.8 trillion today. This increase was concentrated among the .01%, who do not carry credit card debt. They profit from credit card debt. Real disposable personal income has fallen by 5% since the peak in 2008 as Bernanke’s Wall Street bailout zero interest rate policy has caused prices for everything except our houses to surge. The people carrying most of the credit card debt are the least able to pay it off. These are the same people who have swelled the food stamp rolls from 28 million in 2008 to 46.5 million today.

A CNBC bubble headed arrogant bimbo might sarcastically ask, “If the American consumer isn’t deleveraging, than how did revolving credit card debt drop by $182 billion over three years?” Rather than do the minimal research needed to find the answer, they would rather parrot the company/government line. The chart below, compiled from Federal Reserve data, provides the answer. The Wall Street banks have written off $193.3 billion of bad debt since 2008. Now for some basic math, that will probably be over the head of most Wall Street analysts and CNBC parrots. If you start with $972 billion of credit card debt and you write-off $200 billion (assuming another $7 billion in the 4th Quarter of 2011) and your ending balance is $801 billion, how much debt did the American consumer pay down? It’s a trick question. The American consumer ADDED $29 billion of credit card debt since 2008 to go along with the $90 billion of auto and student loan debt ADDED onto their aching backs. So much for the deleveraging storyline. It’s comforting to convince ourselves we’ve changed, but we haven’t. And the powers that be need you to keep believing, so they can continue to keep you enslaved and under their thumbs.

Consumer Credit Card Debt and Charge-off Data (in Billions):

Outstanding Revolving Consumer Debt

Outstanding Credit Card Debt

Quarterly Credit Card Charge-Off Rate

Quarterly Credit Card Charge-Off in Dollars

Q3 2011

$793.4

$777.5

5.63%

$10.9

Q2 2011

$787.4

$771.7

5.58%

$10.8

Q1 2011

$779.6

$764.0

6.96%

$13.3

2010

$826.7

$810.2

$75.1

Q4 2010

$825.7

$810.2

7.70%

$15.6

Q3 2010

$806.9

$790.8

8.55%

$16.9

Q2 2010

$817.4

$801.1

10.97%

$22.0

Q1 2010

$828.5

$811.9

10.16%

$20.6

2009

$894.0

$876.1

$83.2

Q4 2009

$894.0

$876.1

10.12%

$22.2

Q3 2009

$893.5

$875.6

10.1%

$22.1

Q2 2009

$905.2

$887.1

9.77%

$21.6

Q1 2009

$923.3

$904.8

7.62%

$17.2

Q4 2008

$989.1

$969.3

(Source: CardHub.com, Federal Reserve)

Loving Our Servitude

“There will be, in the next generation or so, a pharmacological method of making people love their servitude, and producing dictatorship without tears, so to speak, producing a kind of painless concentration camp for entire societies, so that people will in fact have their liberties taken away from them, but will rather enjoy it, because they will be distracted from any desire to rebel by propaganda or brainwashing, or brainwashing enhanced by pharmacological methods. And this seems to be the final revolution.”Aldous Huxley