If you think Obama and his government flunkies have done miracles with Government Motors since they saved this piece of shit union company with your tax dollars while ignoring bankruptcy law, wait until they are in complete control of your rectal exams. Obama loves to tout his saving of this awful company and the thousands of union drone jobs he was able to keep on the Democrat voting rolls. Who wouldn’t want to buy one of their death traps?

Of course, GM keeps reporting strong sales as they stuff their shitty inventory down the throats of dealers, use the government run ALLY Financial to dole out subprime 7 year 0% auto loans to the Free Shit Army Obama voters, and offer huge money losing discounts that guarantee losses for the company. They are using the tried and true method of selling each car at a loss, but promising to make it up on volume.

This is a joke of a company, reflecting a joke of a president.

The old saying “As GM goes, so goes the country” is truer today than it ever was in the 1950s.

GM Flunks Derek Zoolander School For Bailed Out Companies Who Can’t Build Cars Good, Recalls All New Camaros

Submitted by Tyler Durden on 06/13/2014 09:31 -0400

Another week, another massive GM recall, this time the bailed out company, which clearly is unable to build cars on the “first” attempt, announcing moments ago that it is recalling all current generation Chevvy Camaros “because a driver’s knee can bump the key FOB and cause the key to inadvertently move out of the “run” position, with a corresponding reduction or loss of power.” Supposedly, the issue, which may primarily affect drivers sitting close to the steering column (as opposed to?), was discovered by GM during internal testing following the ignition switch recall earlier this year.

“Discovering and acting on this issue quickly is an example of the new norm for product safety at GM,” said Jeff Boyer, vice president of GM Global Safety.

One wonders how many wrongful death lawsuits are piling into the GM inbox as a result of GM “acting quickly” on what are now over 16 million recalls in 2014 alone! According to the release, GM is aware of three crashes that resulted in four minor injuries that it believes may be attributed to this condition. Is death considered a minor injury by the product safety team at GM one wonders?

Separately, GM also announced two safety recalls and one non-compliance recall involving a total of 65,121 cars in the U.S. all three of which were reported to the NHTSA on Wednesday, June 11, 2014. Including Canada, Mexico and exports, the total recall population is 69,839.

Here is the full and updated list of cars recalled by GM in 2014 alone:

And here is what happens to GM when month after month it confirms it has flunked the Derek Zoolander school for bailed out companies who can’t build cars good: GM has now recalled 70% more cares than it sold in all of 2013, and has recalled 83% more cars in the first 6 months of 2014 than it did in the entire 2008-2013 period!

At least all those votes Obama bought when he bailed out GM were certainly put to good use… just not for building quality cars.

Charts always tell me a more truthful story than the written and spoke propaganda doled out by the corporate mainstream media. The bimbos and boobs on CNBC and the rest of what passes for financial journalism in the dying legacy media were ecstatic about the fantastic May auto sales. These mouthpieces for the establishment just regurgitate the lines written for them by their corporate PR departments. They blather about new highs and best sales since 2007. Maybe they could try using their brains and dig a little deeper to examine the underlying foundation of these fantastic sales.

With a cursory investigation they would discover that average loan length reached an all-time high of 66 months and the average amount financed exceeded $27,000. I’ve never spent more than $20,000 on a car, let alone finance $27,000. The percentage of people leasing those “sold” cars also reached an all-time high of 26%. And the cherry on top is the 34% of auto loans going to subprime deadbeats. “Selling” automobiles using easy money and extending loan lengths is the same strategy employed from 2002 through 2008. That worked out so well, I’m sure it will work just as well this time.

These same clueless dolts paraded on TV as financial journalists would do well to try and explain the chart below. When the economy is running on all cylinders the motor vehicle inventory to sales ratio hovers between 2.0 and 2.5. So at this current point in time, with auto sales reaching seven year highs, we have an extreme inventory to sales ratio of 3.0. Therefore, we have 20% to 50% too many automobiles for the current sales level. An inquisitive mind might wonder what happens next? Are GM, Ford and Chrysler going to allow 10 year auto loans and bump up their subprime clientele to 50%? The inventory continues to pile up on dealer lots, even with the extremely loose financing deals being pushed on the delusional American public.

Based upon history, only a fool, a CNBC economics reporter, or a Federal Reserve chairwoman would expect auto sales to accelerate above the current level. Real household incomes are back at 1998 levels, financing terms are at the loosest in history, the economy is contracting, and gas prices are near three year highs. Does that sound like a recipe for accelerating automobile sales? The data I see is telling me we have reached a peak in auto sales. The extremely high inventory levels will lead to major discounting by the auto companies and huge profit declines. These companies will have to cut back on production, further pushing the economy into recession. It’s amazing what you can see when your agenda isn’t to mislead, obfuscate and misinform.

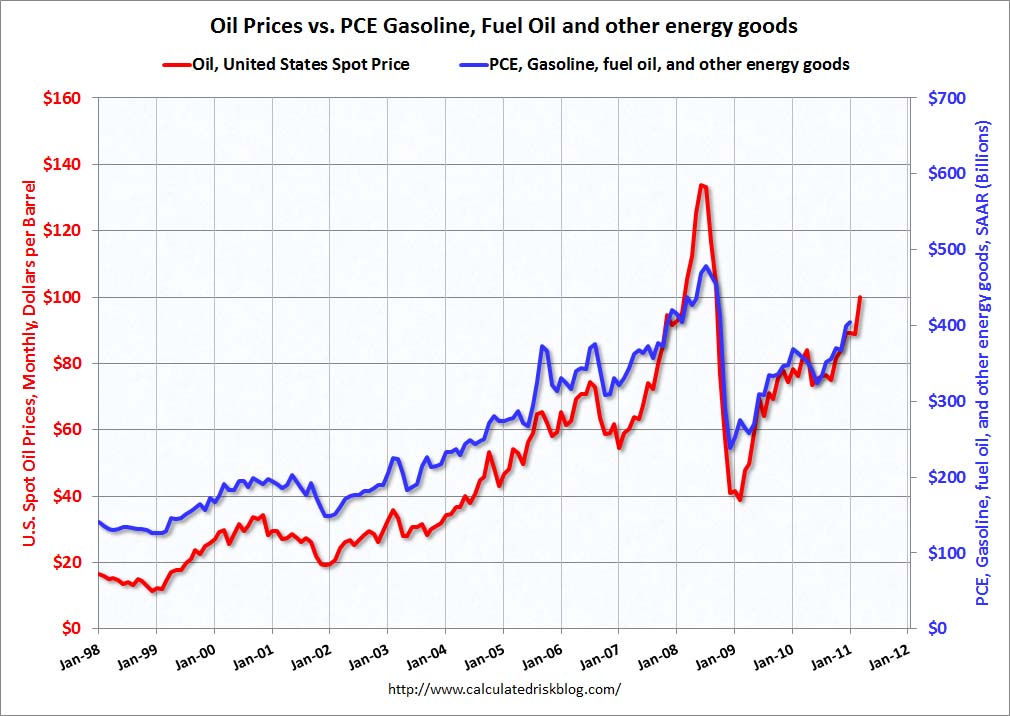

Our beloved leaders and their insistence on democratizing the world at the point of a few hundred tomahawk missiles has had predictable consequences. West Texas crude oil hit $109 a barrel today, the highest level since February 2012 when we were saber rattling over the imminent threat of Iran. Gas prices breached $3.90 per gallon then and again in September of 2012 when West Texas crude hit only $99 per barrel. The price at the station near my house has jumped by 8 cents in the last few days to $3.71 per gallon. The national price of $3.62 is headed higher. If and when the missiles start flying, the sky is the limit depending on what Syria, Russia and Iran do. There already appears to be a disconnect, as WTI has surged by 23% since April, but national gas prices are only up 4%. Some of this is due to demand destruction as the high prices and declining economy have led to a collapse in vehicle miles driven and fuel usage.

Some of the disconnect may be explained by the price of Brent crude. It is pretty much flat versus last year, while WTI has gone up 12%. The West and Midwest are most influenced by the price of WTI, while the East is impacted by Brent. The price of Brent hit $116 today, up 16% since April. That is close to the one year high reached in February, when U.S. gas prices hit their high for the year of $3.70 per gallon. Last year ended up with the highest average price for a gallon of gas in U.S. history and that was with falling prices from September through December. The average price in 2013 is only slightly lower than 2012 and we are about to experience much higher prices from September through December. Throw in a hurricane or two and we’ll really be partying. Prices in Chicago and Los Angeles are already above $3.90 per gallon.

There is nothing like high energy prices to kick the ass of this economy. We are already in recession, as the consumer is up to their eyeballs in debt and getting gouged by higher taxes, healthcare costs, tuition costs, and food costs. These soaring oil prices will make everything more expensive, as our economy is dependent upon shipping shit by truck. One of the storylines peddled by the MSM has been the fantastic auto recovery. Thank God Obama saved GM!!!

Again we have a disconnect. The number of vehicle miles driven continues to decline. Why would auto sales be soaring if people are driving less and young people can’t afford cars? The chart below makes the point. We’ve got record high energy prices and a decade long decline in miles driven, but somehow we have a booming auto industry. It couldn’t possibly be driven by cheap credit doled out to subprime auto buyers? Obama and his minions at Ally Financial, along with Bennie and his Wall Street cohorts wouldn’t be using those free Bennie bucks to create the illusion of an auto recovery? Would they?

Do you think the auto recovery is sustainable with rising interest rates, rising gas prices, falling stock prices, increasing bad debt on auto loans, and a recession? If you do, I have some prime real estate in Damascus I’d like to sell you.

I find it fascinating that the horrible consumer credit data was released at 3:00 pm by the Federal Reserve and the “journalists” at the Wall Street Journal owned Marketwatch did not feel it warranted a headline on their site. You see the stock market is above 15,000 and they need to convince the sheep that this is great news for them. Therefore, they wouldn’t want any negative news to derail their 15,000 Dow storyline.

The blatant manipulation of our financial markets by Wall Street and their cronies in Washington DC is completely revealed by the data reported today. Revolving credit card debt tells the story. We already know that real wages have been falling since the mid 2000’s. We know there are 2 million less full-time jobs than there were in 2007. We know that payroll tax increases and Obamacare premium increases have sucked the life out of the consumer. Not only is credit card debt lower than it was 6 months ago, but it is lower than it was in May 2005. It isn’t lower because consumers are paying it down. It is lower because they can’t take on any more debt.

So riddle me this. If they aren’t buying Chinese shit with credit cards and their disposable income is declining, how does a country that depends on consumers to generate 71% of its GDP by spending on shit happen to be in an economic recovery?

Government sanctioned fraud, financed by you the taxpayer. Total consumer credit did hit a new all-time high in March. Since 2009, credit card debt has declined by $71 billion. Over this same time frame non-revolving debt has increased by $458 billion. That sure sounds like a disconnect to me. Using your credit card is a personal choice and can be restricted by the credit card issuer through reduced credit lines. Why would consumers be cutting back on credit card debt by 8% and increasing their use of non-revolving credit by 30%?

Easy answer – Obama and his government minions. They have doled out hundreds of billions in student loans to dullards going to the University of Phoenix to keep the unemployment rate on a downward track and they happen to still own 80% of Ally Financial (GMAC, Ditech, Rescap). Obama and his minions have used Ally Financial as their little engine of growth for GM and the rest of the auto industry. While automaker profits continue to fall, Ally Financial is giving auto loans to deadbeat subprime borrowers accounting for 45% of all vehicle sales in the country.

When has subprime lending created problems in the past? Is there a more subprime borrower than a University of Phoenix dropout or a Cadillac Escalade owner in West Philly? The economy is in the shitter. The average person can’t afford a pot to piss in. The government is using your money to create the illusion of recovery. There will be hundreds of billions in loan writeoffs for this government sanctioned fraud. You will foot the bill, so work harder and pay more taxes. It’s your duty to comrade Obama.

March Consumer Credit Increase Driven Entirely (And Then Some) By Student And Car Loans

Submitted by Tyler Durden on 05/07/2013 15:18 -0400

The March consumer credit headline was a disappointment, increasing by just $7.97 billion, on expectations of a $15.6 billion increase, with the February total revised lower to $18.14 billion. So far so bad. It gets worse when one peeks beneath the surface and finds that discretionary consumer credit in the form of credit card and other revolving loans posted its first decline of 2013, dropping by $1.7 billion, the biggest decline since December’s 2.1 billion. So what rose: why debt for purchases of Government Motors and student loans of course, which increased by $9.676 billion in March. In other words: the student bubble keeps getting bigger, more and more GM cars are being bought on subprime credit, while the vast majority of Americans can’t even afford to charge toilet paper purchases as the discretionary deleveraging continues.

In the last year, of the $157 billion in total debt issued, $152.6 billion, or 97.5%, is in the form of non-revolving credit. Consumer credit created? A whopping 2.5% of the total or $4 billion.

Finally, who is the primary source of all this free credit? Why Uncle Sam of course (and all US taxpayers by implication, when the student and second subprime car bubble pops of course).

GM and Ford reported “strong” sales for March, up 6.4% and 5.7% respectively. The current annual rate of auto sales has “surged” to 15.2 million. Last year sales rose to 14.5 million from only 12.7 million in 2011. This sure sounds like a tremendous recovery led by great new models from our “saved” GM and wonderful iconic Ford Motors. The MSM was crowing about the results today, except the details tell a different story. GM’s car sales FELL 3% in March. The surge in sales was due to fleet sales going up 12%. It couldn’t possibly be the Federal government buying vehicles, could it? Cadillac sales surged as subprime loans in West Philly to the FSA reached record levels. There were 1,478 Volts sold in the whole country – so there will be 15.2 million vehicles sold in the country and the Obama Volt will account for less than 20,000 of these sales or .0013 of all car sales. Ford car sales FELL 0.2%. Their increase was also driven by fleet sales and truck sales. How dense is the average American? Gasoline prices are above $4.00 per gallon in many cities and they continue to buy low gas mileage trucks and SUVs.

The auto market is completely dependent upon 7 year 0% financing for good credits and subprime lending for 45% of sales and this is all they can achieve?

If sales have been so awesome for the last two years, why are their stocks and their profits in decline? Inquiring minds want to know.

If auto sales were 12.7 million in 2011 and they are pacing at 15.2 million in 2013, why has GM stock dropped from $38 to $28, a 26% decline? I thought Obama saved GM and they were doing awesome. Vehicle sales are up 20% since 2011 and GM still managed to earn $3 billion less in 2012 than they earned in 2011. This doesn’t even take into account the massive channel stuffing that has artificially boosted their sales figures.

It seems that selling vehicles to your dealers and to deadbeats through Ally Financial doesn’t generate profits. But who needs profits when a storyline will do.

If Ford Motor is doing so well why is their stock at $13 today when it was at $19 in 2011? For the math challenged, that is a 32% drop when auto sales are up 20% since 2011. Is the MSM reporting that Ford sales dropped by $2 billion in 2012 and their net income from operations dropped by $1 billion? Are we really having a strong auto recovery if the two biggest US automakers are making significantly less profit?

The MSM is not in the truth business. They are in the propaganda business. The storyline of auto recovery is false. The reported sales increases are due to channel stuffing and easy money from Bennie. The 45% of sales from subprime loans will bite the taxpayer in the ass when Ally Financial reports billions in losses over the next few years. You own Ally Financial. So it goes.

After digesting the opinions of the shills, shysters and scam artists, I am ready to predict that I have no clue what will happen during 2013. The weekend weather last week was a perfect analogy for attempting to forecast the future. The professional highly educated meteorologists predicted sunny warm weather, just as the PhD Wall Street paid economist mouthpieces assure the multitudes 2013 will be the year when zero interest rates and $1.2 trillion deficits will finally lead to sunny economic skies. Instead, the weekend was overcast and damp. As I was writing this article and watching the miraculous Baltimore Ravens comeback against Denver, I received a two minute warning from my wife. I had to pick up my son and his buddies at the Montgomery Mall. As I pulled the car out of the garage, I backed out into fog that was thicker than pea soup. I’ve driven the roads to the Montgomery Mall hundreds of times, but the fog was so thick I couldn’t see ten feet ahead. I drove hesitantly, wondering what might be just over the horizon or what might dart out from a side street. I see 2013 as a year of maneuvering through thick fog with startling apparitions lurking to surprise us and force a deviation in our normal course. As I proceeded cautiously through the murky mist there were few cars on the roads and the strip centers and fast food joints resembled haunted houses and grave yards. I expected to see Dracula, Frankenstein’s monster, and Wolfman panhandling on the corners.

The fog of uncertainty is engulfing the nation, making consumers hesitant to spend and businesses reluctant to hire or invest. It was like being in a commercial real estate horror film, with SPACE AVAILABLE, NOW LEASING, and STORE CLOSING signs startling me everywhere I turned. The trip took a spooky turn as I passed branches of those zombie banks – Bank of America and Citigroup. They don’t even know they’re already dead. I finally arrived at the Mall passing thousands of empty parking spaces with a few cars huddled close to the zombie starring in Night of the Retailing Dead – Sears. In the miasma, the few visitors appeared to be automaton like consumers programmed to shuffle through the mall and buy things they don’t need with money they don’t have. To say the road ahead for this country in 2013 is foggy would be an epic understatement. Let’s hope it doesn’t have a Nightmare on Elm Street like ending.

Virtually all of the mainstream media, Wall Street banks and paid shill economists are in agreement that 2013 will see improvement in employment, housing, retail spending and, of course the only thing that matters to the ruling class, the stock market. Even among the alternative media, there seems to be a consensus that we will continue to muddle through and the day of reckoning is still a few years off. Those who are predicting improvements are either ignorant of history or are being paid to predict improvement, despite the overwhelming evidence of a worsening economic climate. The mainstream media pundits, fulfilling their assigned task of purveying feel good propaganda, use the 10% stock market gain in 2012 as proof of economic recovery. The facts prove otherwise:

Real GDP, using a dramatically understated inflation rate, has barely grown by 1% in 2012. Using a true measure of inflation, the GDP was -2% during 2012. Even this pitiful growth was generated by 0% interest rate deals for subprime auto loans through Ally Financial (85% owned by you the taxpayer) and 7 year 0% home furnishing financing deals through GE Capital and the other government subsidized Too Big To Control Wall Street banks. The Federal government chipped in by guaranteeing FHA subsidized 3% down payment loans on houses and handing out billions in loans to students so they can find themselves, keep the unemployment rate down, get drunk, and if they graduate – enter debt servitude for decades.

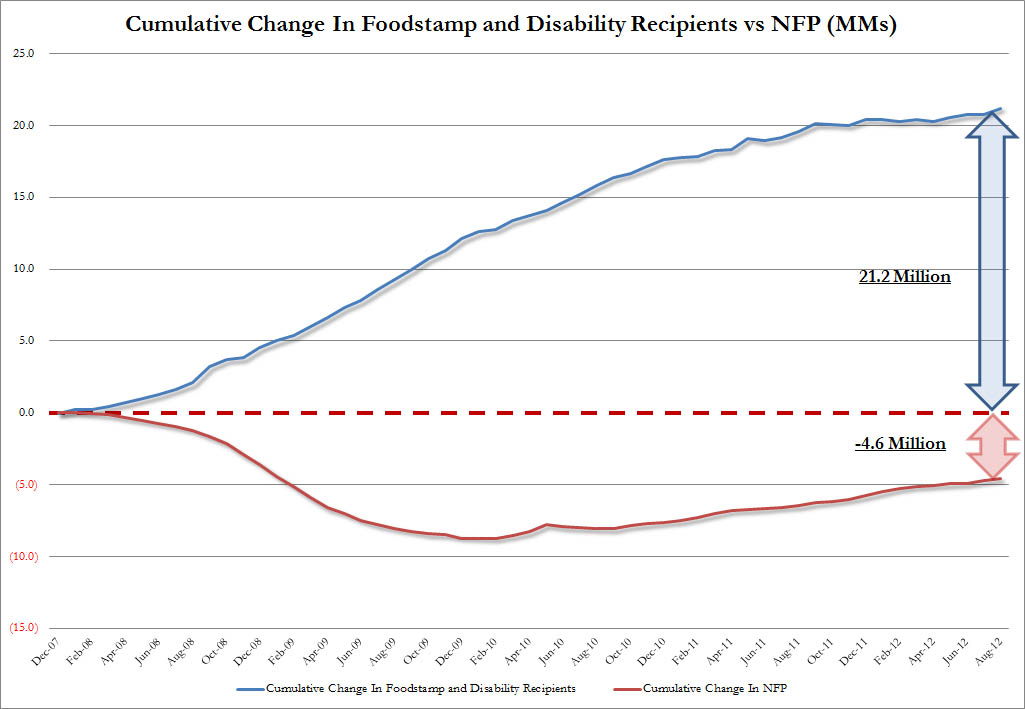

The number of people who have left the workforce since last December (2.2 million) almost matched the number of newly employed (2.4 million), as the labor participation rate has collapsed to a three decade low of 63.6%. The propagandists attempt to peddle this dreadful condition as a function of Baby Boomers retiring. This is obliterated by the fact the 55 to 69 age bracket has added 4 million jobs since Obama became president, while the younger age brackets have lost 3 million jobs. The working age population has grown by 13 million since 2007 and there are 4 million less people employed.

Another 1.5 million Americans were forced onto food stamps during 2012, bringing the total increase to 17 million since Obama assumed office. With 47.5 million depending on assistance to feed them, a full 20% of all households in the U.S. are dependent on this program, costing taxpayers $76 billion, versus $34 billion in 2008. Another 4.8 million have joined the ranks of the disabled since 2009, with a dramatic surge when the 99 week unemployment benefits began to run out. These trends are surely signs of recovery.

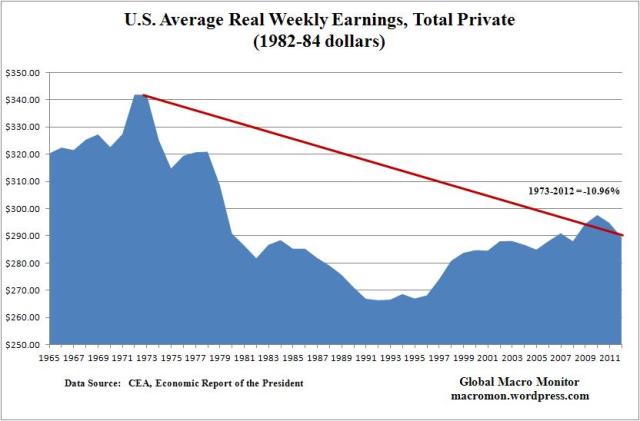

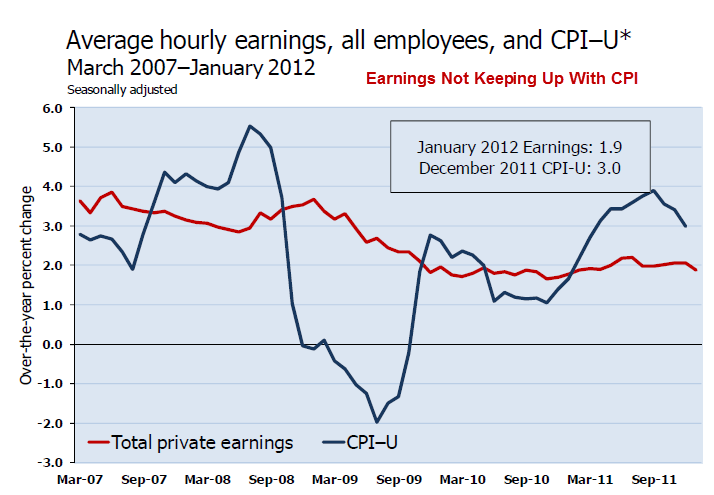

Real average hourly earnings were flat in 2012, and have fallen 1.5% since Obama became president. The average middle class worker is making less than they were forty years ago. Using a true measure of inflation would reveal the true devastation wrought on the middle class. As the things we need (food, energy, shelter, education, healthcare) have grown more expensive and the things we are brainwashed to buy (iGadgets, HDTVs, luxury autos, bling) by the masters of propaganda have been made easily accessible through credit, the middle class has enslaved themselves in chains of debt. The declining average wages since 1973 have forced families to have both spouses work outside the home, with the consequence of more divorces, children raised by strangers, and the proliferation of depressed human beings. The lost real income has been replaced by credit card, auto, mortgage, and student loan debt.

The reason Bernanke, Geithner, Obama, Wall Street, corporate titans, and media pundits focus their attention on the stock market is because they are looking out for their fellow 1%ers. The working middle class, once the backbone of this country, own virtually no stocks. The 88% stock market increase since March 2009 hasn’t benefitted the middle class one iota. The Federal Reserve engineered stock market recovery has benefitted moneyed bankers and wealthy corporate executives, the very people who collapsed the worldwide financial system and received the bailouts when they should have gone to jail.

Those who continue to tout a non-existent economic recovery have focused on the manufactured stock market and housing recovery, extrapolating those trends without understanding how it has been achieved. A master plan implemented through the collusion of the Federal Reserve, Treasury Department, Executive branch, Wall Street cabal, and corporate media conglomerates has created the illusion of recovery. Make no mistake about it, those in power held clandestine meetings and had covert discussions that will never see the light of day in transcripts or recordings. They developed a strategy to save themselves, their fellow cronies, and the corporate interests that run this country. They threw the middle class, senior citizens, and young people under the bus in their sordid determination to retain their power, wealth and control. Their multi-faceted scheme has been rolled out as follows:

Reduce interest rates to 0% so Wall Street banks could borrow for free and reinvest in Treasuries, therefore earning risk free profits so they could rebuild their non-existent capital. The Wall Street banks also used the free money to generate trading profits using their HFT supercomputers, with only the occasional glitch (JP Morgan London Whale $9 billion slipup, Corzine blowing up his firm and stealing $1.2 billion from ranchers & farmers). The ability to borrow at 0% has spurred these financial institutions to make 0% loans to subprime auto buyers and offer 7 year 0% interest deals on behalf of furniture, electronics, and appliance retailers. This Keynesian solution is supposed to spur demand and generate new jobs. The reality is that Bernanke’s ZIRP has transferred $400 billion of annual interest income from savers and senior citizens to the Wall Street bankers, while setting the table for more massive bad debt write-offs when the millions of subprime borrowers default.

The Federal Reserve and the Treasury Department forced the FASB to scrap mark to market accounting, allowing the Wall Street banks to fraudulently value their worthless assets. The Federal Reserve than tripled their balance sheet from $900 billion to $2.95 trillion by purchasing almost $1 trillion of toxic mortgage debt from the Wall Street banks at full face value of the debt. The Fed purchased Treasuries to artificially lower mortgage rates and attempt to spur a housing recovery.

The Wall Street banks have purposely manipulated the foreclosure process and restricted the inventory of foreclosures available to purchase. In conjunction with Fannie Mae and Freddie Mac, large inventories of foreclosed properties have been sold in bulk to connected Wall Street firms at above market prices and positioned as rental properties. The FHA has done their part by guaranteeing 3% down payment mortgages and putting taxpayers on the hook for the billions in losses to come. Fannie and Freddie have already lost $200 billion of taxpayer money since 2008 on behalf of the Wall Street banks. The concerted effort to restrict the supply of homes available for sale resulted in the price of homes sold rising in 2012. Those in power are attempting to resuscitate the millions of heavily indebted underwater home occupiers at the expense of the young and frugal who would buy when home prices dropped to a clearing level. The same people who created the first housing bubble are attempting to re-inflate it as a solution to our economic woes.

Despite the fact that individual investors have pulled billions out of the stock market over the last three years, the stock market has managed to approach all-time highs. This has been the lynchpin of their plan. The sole purpose of every QE initiated by Bernanke has been to elevate the stock market. Academics like Bernanke and Krugman sell the “wealth effect” storyline to the masses as a way to spur consumer spending. The only wealth effect is to shift the wealth of the working middle class to the ruling class who own the stocks and control the markets. As each QE has further enriched the 1%, the inflationary impact on energy, food, and clothing has destroyed the lives of millions in the middle class who own virtually no stocks. The gap between the uber-rich ruling class and the peasants has never been wider.

The master plan has succeeded in delaying the worst of the Crisis, further enriching the oligarchs, further impoverishing the middle class, fanning the flames of revolution across the globe, provoking foreign adversaries, inciting anger among the populace and darkening the mood of the country. Those predicting a return to the peaceful autumn like days of the late 90s reveal their ignorance of history. Winter is here and there are many dark days ahead before Spring is discernible. The linear thinking crowd who hang their hats on never ending progress spurred by technological innovation and a limitless supply of cheap resources are denying reality. Delusion and hope for a better tomorrow is not a strategy. We have entered the 5th year of this ongoing Crisis. Fourth Turnings do not fizzle out; they build to a societal earth shattering crescendo (American Revolution, Civil War, Great Depression/WWII). Economic, financial, social and global conditions do not progress during a twenty year Crisis period, driven by the generational configuration that arises once every 80 years. An epic struggle between good and evil, rich and poor, government and governed, young and old, nation and nation, awaits us over the next fifteen years. No matter what happens in 2013, it will be driven by the core elements of this Crisis – Debt, Civic Decay, and Global Disorder.

“In retrospect, the spark might seem as ominous as a financial crash, as ordinary as a national election, or as trivial as a Tea Party. The catalyst will unfold according to a basic Crisis dynamic that underlies all of these scenarios: An initial spark will trigger a chain reaction of unyielding responses and further emergencies. The core elements of these scenarios (debt, civic decay, global disorder) will matter more than the details, which the catalyst will juxtapose and connect in some unknowable way. If foreign societies are also entering a Fourth Turning, this could accelerate the chain reaction. At home and abroad, these events will reflect the tearing of the civic fabric at points of extreme vulnerability – problem areas where America will have neglected, denied, or delayed needed action.” – The Fourth Turning – Strauss & Howe -1996

Until Debt Do Us Part

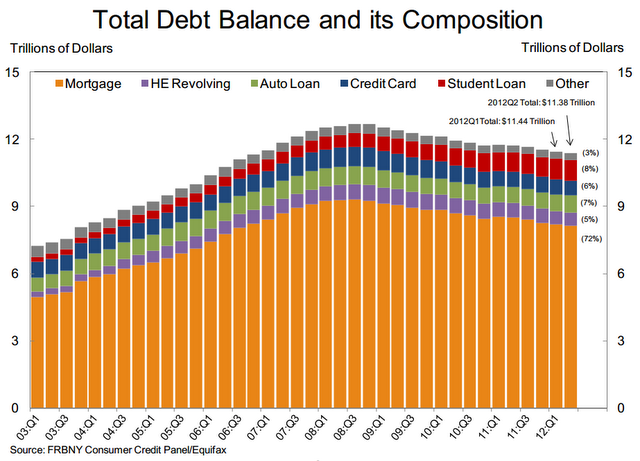

The storyline of austerity and deleveraging perpetuated through the mainstream media mouthpieces is unequivocally false, as consumer debt has reached an all-time high of $2.77 trillion, driven by a surge in subprime auto loans and subprime student loans. The reason for the surge in these loans, while credit card debt lingers 15% below the 2008 peak, is because the Federal Government is doling out these loans with your tax dollars. Ally Financial (aka GMAC, aka Ditech) is under the complete control of the Federal Government and doesn’t care about future losses. The taxpayers won’t notice another $1 billion in losses. There are Cadillac Escalades, Silverados and RAM pickups to peddle to morons without money.

Could there be a more subprime borrower than a 20 year old majoring in African literature or a 40 year old former construction worker enrolled at the University of Phoenix with 500,000 other schmoes? The Federal government assumed control over the student loan market in 2009 and has proceeded to blow a new bubble. They have driven tuition higher and enabled millions of barely functioning morons to enter college, where they will not only fail, but also be burdened by un-payable levels of non-dischargeable debt. Now the government solution is to pass those bad debts onto you the taxpayer while encouraging even more debt for students. Here is an assessment of the new “Pay as you Earn” program from your owners:

“(BusinessWeek) We have one example of someone who might look similar to an MBA student. He starts out with a starting salary of $90,000 and by the end of 20 years is making $243,360. Under the old IBR program, he’ll have paid $409,445 by year 25 and be forgiven $23,892 of his loan balance. Under the new IBR repayment plan he’ll pay less than half of that, or $202,299, and be forgiven $208,259 by year 20. The old IBR plan was punitive if you borrowed a lot of money, made you pay more over time and trapped you, so there were serious consequences to doing that. It was a downside and a pretty big risk, which is why you didn’t see people borrowing without regard to how much it will cost. The new plan essentially eliminates any downside or risk for that type of behavior, and cuts payments in half and then some.”

The enslavement of our children in student loan debt and handing them the bill for $200 trillion of unfunded entitlement liabilities will be the spark that ignites the worst part of this Crisis.

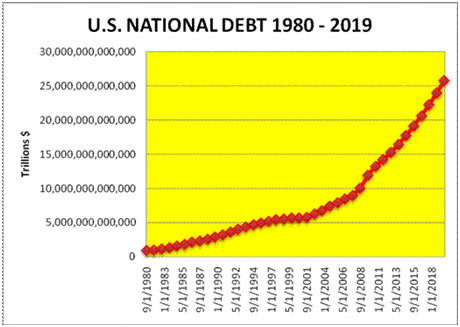

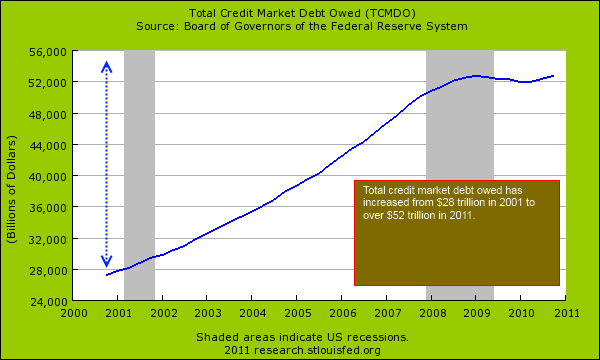

Those in power realized very quickly that without continued credit growth, their entire corrupt, repugnant, fiat currency based debt system would implode and they would lose all of their fraudulently acquired wealth. That is why total credit market debt is at an all-time high of $56 trillion, and 350% of GDP. The National Debt of $16.5 trillion is now 103% of GDP, well beyond the Rogoff & Reinhart level of 90% that always leads to economic crisis and turmoil.

As Wall Street bankers acted like lemmings leading up to the 2008 financial collapse the famous July 2007 quote from Charles Prince, CEO of Citigroup, summed it up nicely:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing,”

Now central bankers across the globe are dancing an Irish Jig. Every major central banker in the world is lemmingly following Bernanke’s lead and printing money at hyper-speed. The Europeans have surpassed the Japanese in their quest to become the first casualty in the coming debt collapse. Bernanke, in his quest to not be outdone, has committed to taking his balance sheet to 25% of GDP within the next year. Japan has vowed not to be outdone. The currency debasement race is gathering steam. The devastation, anger, resentment and ultimately war caused by these bankers will engulf the world when it reaches its apocalyptic ending.

Will the grain of sand that collapses the pile be a debt ceiling crisis as postulated by Strauss & Howe?

“An impasse over the federal budget reaches a stalemate. The president and Congress both refuse to back down, triggering a near-total government shutdown. The president declares emergency powers. Congress rescinds his authority. Dollar and bond prices plummet. The president threatens to stop Social Security checks. Congress refuses to raise the debt ceiling. Default looms. Wall Street panics.” – The Fourth Turning – Strauss & Howe – 1996

I don’t think so. The Democrats and Republicans are playing their parts in this theater of the absurd. Neither party has any desire to cut spending, reduce our debt, or secure the future of unborn generations. In 2013, I see the following things happening related to our debt crisis:

The debt ceiling will be raised as the toothless Republican Party vows to cut spending next time. The political hacks will create a 3,000 page document of triggers and create a committee to study the issue, with actual measures that slow the growth of annual spending by .000005% starting in 2017.

The National Debt will increase by $1.25 trillion and debt to GDP will reach 106% by the end of the fiscal year.

The Federal Reserve balance sheet will reach $4 trillion by the end of the year.

Consumer debt will reach $2.9 trillion as the Feds accelerate student loans and Ally Financial, along with the other Too Big To Control Wall Street banks, keep pumping out subprime auto loans. By mid-year reported losses on student loans will soar and auto loan delinquencies will show an upturn. This will force a slowdown in consumer debt issuance, exacerbating the recession that started in 2012.

The Bakken oil miracle will prove to be nothing more than Wall Street shysters selling a storyline. Daily output will stall at 750,000 barrels per day and the dreams of imminent energy independence will be annihilated by reality, again. The price of oil will average $105 per barrel, as global tensions restrict supply.

The home price increases generated through inventory manipulation in 2012 will peter out as 2013 progresses. The market has been flooded by investors. There is very little real demand for new homes. Young households with heavy student loan debt and low paying jobs will continue to rent, since the oligarchs refused to let prices fall to a level that would spur real demand. Mortgage delinquencies will rise as job growth remains stagnant, leading to an increase in foreclosures. Rent prices will flatten as apartment construction and investors flood the market with supply.

The disconnect between the stock market and the housing and employment markets will be rectified when the MSM can no longer deny the recession that began in 2012 and will deepen in the first part of 2013. While housing prices languish 30% below their peak levels of 2006, the stock market has prematurely ejaculated back to pre-crisis levels. Declining corporate profits, stagnant consumer spending, and increasing debt defaults will finally result in a 20% decline in the stock market, with a chance for losses greater than 30% if Japan or the EU begin to crumble.

Japan is still a bug in search of a windshield. With a debt to GDP ratio of 230%, a population dying off, energy dependence escalating, trade surplus decreasing, an already failed Prime Minister vowing to increase inflation, and rising tensions with China, Japan is a primary candidate to be the first domino to fall in the game of debt chicken. A 2% increase in interest rates would destroy the Japanese economic system.

The EU has temporarily delayed the endgame for their failed experiment. Economic conditions in Greece, Spain and Italy worsen by the day with unemployment reaching dangerous revolutionary levels. Pretending countries will pay each other with newly created debt will not solve a debt crisis. They don’t have a liquidity problem. They have a solvency problem. The only people who have been saved by the actions taken so far are bankers and politicians. I believe the crisis will reignite, with interest rates spiking in Spain, Italy and France. The Germans will get fed up with the rest of Europe and the EU will begin to disintegrate.

Civic Decay Accelerates

“History offers no guarantees. If America plunges into an era of depression or violence which by then has not lifted, we will likely look back on the 1990s as the decade when we valued all the wrong things and made all the wrong choices.”– Strauss & Howe – The Fourth Turning

The liberal minded Op-Ed writers that decry the incivility of dialogue today once again show their ignorance for or contempt for American history. They call for compromise and coming together. They should see Spielberg’s Lincoln to understand the uncompromising nature of Fourth Turnings and how conflicts are resolved. They should watch documentary film of Dresden, Hiroshima, and Guadalcanal during World War II. Compromise and civility do not compute during a Fourth Turning. It is compromise that has brought us to this point. Avoiding tough decisions and delaying action occur during the Unraveling. We’ve known the entitlement issues confronting our nation for over a decade and chose to do nothing. The time for delay and inaction is long gone. The pressing issues of the day will be resolved through collapse, confrontation and bloodshed. It’s the way it has always been done and the way it shall be. The current conflict over banning guns is just a symptom of a bigger disease. Government, at the behest of the owners, has been steadily assuming more power and control over the everyday lives of citizens who just want to be left to live their lives. Government has used propaganda, fear and misinformation to convince large swaths of the populace to voluntarily sacrifice their freedom and liberty for the promise of safety and security. Warrantless surveillance, imprisonment without charges, molestation by TSA agents, military exercises in cities, drones in our skies, cameras watching our every move, overseas torture, undeclared wars, cyber-attacks on sovereign countries, and now the threat of disarmament of the people have all contributed to the darkening skies above. A harsh winter lies ahead.

Civic decay is being driven by two main thrusts. Lack of jobs and destruction of middle class wealth by the oligarchs is resulting in the anger and dismay overwhelming the country. The chart below reveals the truth about our economy and the fraudulent nature of BLS reported data, skewed to paint a false picture. The 25 to 54 year old age bracket captures Americans in their peak earnings years. In 2007 this age bracket had 83% of its members in the labor force and 100.5 million of them employed. Today, according to the BLS, only 81.4% are in the labor force and there are 6.3 million less employed. The BLS has the gall to report that since 2009, even though the number of employed people in this age bracket has declined by 1 million, the number of unemployed people has dropped by 1.5 million people. To report this drivel is beyond laughable. The horrific labor market situation is confirmed by the fact that despite a 3.6 million person increase in this age demographic since 2000, there are 7.8 million more people not employed.

The reduced earnings and savings of the people in this demographic is having profound and long-lasting impact on our society. Household formation, retirement savings, tax revenues, and self-worth are all negatively impacted. The mood of desperation and anger is materializing in this age bracket. The resentment of these people when they see the well-heeled Wall Street set reaping stock market gains and bonuses while they make do on food stamps, extended unemployment and the charity of friends and family is palpable. More than 100% of the employment gains since 2010 have gone to those over the age of 55, further embittering the 25 to 54 workers. There is boiling anger beneath the thin veneer of civility between Millenials, GenXers, and Boomers. The chasm between the ultra-rich and the masses widens by the day and is leading to a seething animosity. The country has lost 2.4 million construction jobs and 2 million manufacturing jobs since 2007, but we’ve added 250,000 fry cook jobs and 440,000 University of Phoenix jobs stimulated by $500 billion in student loans. The complete transformation of a producing society to a consumption society has been accomplished.

When the average person sees Wall Street bankers not only walk away unscathed from the crisis they aided, abetted and created through their fraudulent inducements and documentation, but be further enriched at taxpayer expense, their hatred and disgust with high financers like Corzine, Dimon and Blankfein burns white hot. The mainstream media propaganda machine tries to convince the average Joe that stock market highs and record corporate profits are beneficial to him, even though the gains and profits have been spurred by zero interest rates, fraudulent accounting and outsourcing their jobs to third world slave labor factories. A critical thinking human being (this rules out 95% of the adult population) might question how corporate profits could surpass pre-collapse levels when the economy has remained stagnant.

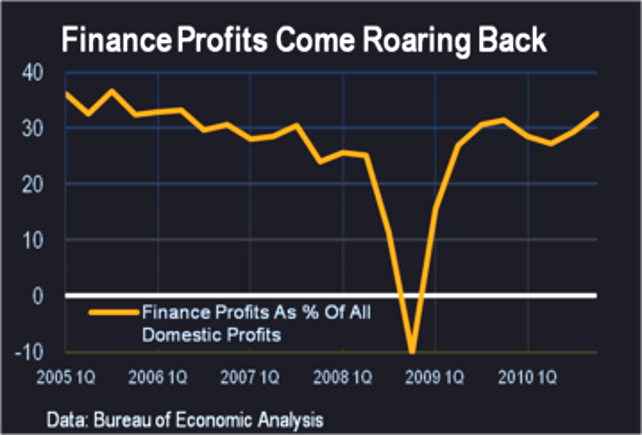

Shockingly, the entire profit surge was driven by Wall Street. Accounting entries relieving billions of loan loss reserves, earning hundreds of millions in risk free interest courtesy of Bernanke, and falsely valuing your loan portfolio can do wonders for profits. We’ve added 6.9 million finance jobs in the last 20 years as this industry has sucked the lifeblood out of our nation. A country that allows bankers to syphon off 35% of all the profits in the country without producing any benefits to society is destined to fail, with the dire consequences that follow.

My civic decay expectations for 2013 are as follows:

Progressive’s attempt to distract the masses from our worsening economic situation with their assault on the 2nd Amendment will fail. Congress will pass no new restrictions on gun ownership and 2013 will see the highest level of gun sales in history.

The deepening recession, higher taxes on small businesses and middle class, along with Obamacare mandates will lead to rising unemployment and rising anger with the failed economic policies of the last four years. Protests and rallies will begin to burgeon.

The number of people on food stamps will reach 50 million and the number of people on SSDI will reach 11 million. Jamie Dimon, Lloyd Blankfein, and Jeff Immelt will compensate themselves to the tune of $100 million. CNBC will proclaim an economic recovery based on these facts.

The drought will continue in 2013 resulting in higher food prices, ethanol prices, and shipping costs, as transporting goods on the Mississippi River will become further restricted. The misery index for the average American family will reach new highs.

There will be assassination attempts on political and business leaders as retribution for their actions during and after the financial crisis.

The revelation of more fraud in the financial sector will result in an outcry from the public for justice. Prosecutions will be pursued by State’s attorney generals, as Holder has been captured by Wall Street.

The deepening pension crisis in the states will lead to more state worker layoffs and more confrontation between governors attempting to balance budgets and government worker unions. There will be more municipal bankruptcies.

The gun issue will further enflame talk of state secession. The red state/blue state divide will grow ever wider. The MSM will aggravate the divisions with vitriolic propaganda.

The government will accelerate their surveillance efforts and renew their attempt to monitor, control, and censor the internet. This will result in increased cyber-attacks on government and corporate computer networks in retaliation.

Global Disorder Spreads

“Eventually, all of America’s lesser problems will combine into one giant problem. The very survival of the society will feel at stake, as leaders lead and people follow. The emergent society may be something better, a nation that sustains its Framers’ visions with a robust new pride. Or it may be something unspeakably worse. The Fourth Turning will be a time of glory or ruin.” – Strauss & Howe – The Fourth Turning

The entire world resembles a powder-keg in a room full of monkeys with matches. As economic conditions worsen around the world the poor, destitute and unemployed increasingly have begun to revolt against their banker masters. Money printing, reporting fraudulent economic data and pretending to make debt payments with newly issued debt does not employ anyone or put food in the mouths of the people. With worldwide unemployment surpassing 200 million, food and energy prices surging, peasants in the Far East treated like slave laborers, politicians stealing from the people to enrich their banker owners, and young people losing hope for a better tomorrow, the likelihood of strikes, protests, armed revolution, and war is high.

The world is about to find out the downside to globalization, as turmoil in Europe or Asia will swiftly impact those in the rest of the world that are interconnected through trade and financial instruments. The trillions of derivatives that link financial institutions across the world will ignite like a string of firecrackers once a spark reaches the fuse. Treaties and alliances between countries will immediately enlarge localized military conflicts into world-wide confrontations. Dwindling supplies of cheap oil and potable water, a changing climate (whether cyclical or human activity based) that is creating droughts, floods and super-storms on a more frequent basis, and religious zealotry set the stage for resource wars and religious wars around the globe and particularly in the Middle East. Fourth Turnings always intensify and ultimately lead to total war, with no compromise and clear winners and losers. The proxy wars that have been waged for the last 60 years will look like kindergarten snack time when the culmination of this Fourth Turning war results in death on a scale that would be considered incomprehensible today. And it will happen within the next fifteen years. The climactic war is still a few years off, but here is what I think will happen in 2013:

With new leadership in Japan and China, neither will want to lose face, so early in their new terms. Neither side will back down in their ongoing conflict over islands in the East China Sea. China will shoot down a Japanese aircraft and trade between the countries will halt, leading to further downturns in both of their economies.

Worker protests over slave labor conditions in Chinese factories will increase as food price increases hit home on peasants that spend 70% of their pay for food. The new regime will crackdown with brutal measures, but the protests will grow increasingly violent. The economic data showing growth will be discredited by what is happening on the ground. China will come in for a real hard landing. Maybe they can hide the billions of bad debt in some of their vacant cities.

Violence and turmoil in Greece will spread to Spain during the early part of the year, with protests and anger spreading to Italy and France later in the year. The EU public relations campaign, built on sandcastles of debt in the sky and false promises of corrupt politicians, will falter by mid-year. Interest rates will begin to spike and the endgame will commence. Greece will depart the EU, with Spain not far behind. The unraveling of debt will plunge all of Europe into depression.

Iran will grow increasingly desperate as hyperinflation caused by U.S. economic sanctions provokes the leadership to lash out at its neighbors and unleash cyber-attacks on Saudi Arabian oil facilities and U.S. corporations. Israel will use the rising tensions as the impetus to finally attack Iranian nuclear facilities. The U.S. will support the attack and Iran will launch missiles at Saudi Arabia and Israel in retaliation. The price of oil will spike above $125 per barrel, further deepening the worldwide recession.

Syrian President Assad will be ousted and executed by rebels. Syria will fall under the control of Islamic rebels, who will not be friendly to the United States or Israel. Russia will stir up discontent in retaliation for the ouster of their ally.

Egypt and Libya will increasingly become Islamic states and will further descend into civil war.

The further depletion of the Cantarell oil field will destroy the Mexican economy as it becomes a net energy importer. The drug violence will increase and more illegal immigrants will pour into the U.S. The U.S. will station military troops along the border.

Cyber-attacks by China and Iran on government and corporate computer networks will grow increasingly frequent. One or more of these attacks will threaten nuclear power plants, our electrical grid, or the Pentagon.

So now I’m on the record for 2013 and I can be scorned and ridiculed for being such a pessimist when December rolls around and our Ponzi scheme economy hasn’t collapsed. There is no disputing the facts. The economic situation is deteriorating for the average American, the mood of the country is darkening, and the world is awash in debt and turmoil. Every country is attempting to print their way to renewed prosperity. No one wins a race to the bottom. The oligarchs have chosen a path of currency debasement, propping up insolvent banks, propaganda and impoverishing the masses as their preferred course. They attempt to keep the masses distracted with political theater, gun control vitriol, reality TV and iGadgets. What can be said about a society where 10% of the population follows Justin Bieber and Lady Gaga on Twitter and where 50% think the National Debt is a monument in Washington D.C. The country is controlled by evil sycophants, intellectually dishonest toadies and blood sucking leeches. Their lies and deception have held sway for the last four years, but they have only delayed the final collapse of a boom brought about by credit expansion. They will not reverse course and believe their intellectual superiority will allow them to retain their control after the collapse.

“Washington has become our Versailles. We are ruled, entertained, and informed by courtiers — and the media has evolved into a class of courtiers. The Democrats, like the Republicans, are mostly courtiers. Our pundits and experts, at least those with prominent public platforms, are courtiers. We are captivated by the hollow stagecraft of political theater as we are ruthlessly stripped of power. It is smoke and mirrors, tricks and con games, and the purpose behind its deception.”– Chris Hedges

Every day more people are realizing the con-job being perpetuated by the owners of this country. Will the tipping point be reached in 2013? I don’t know. But the era of decisiveness and confrontation has arrived. The people will learn there are consequences to our actions and inaction. The existing social order will be swept away. Are you prepared?

“The era of procrastination, of half-measures, of soothing and baffling expedients, of delays, is coming to a close. In its place we are entering a period of consequences…” – Winston Churchill

Where life had no value, death, sometimes, had its price. That is why the bounty killers appeared. – For a Few Dollars More

“Tell me, isn’t a sheriff supposed to be courageous, loyal and, above all, honest?” –Man with No Name – For a Few Dollars More

Whenever I get an idea for an article I plan to keep it short and sweet. But it never seems to work out that way. Once I start typing, the articles tend to grow exponentially. It happened again with my attempt to make sense of how the United States of America managed to screw our finances up so badly, that an epic collapse is within view to people with their eyes open to facts and the truth. You don’t end up in the predicament we find ourselves in today due to a couple minor mistakes over a short time frame. It took thousands of horrible choices, colossal doses of delusion, a heaping of stupidity, and a mountain of denial over decades to put us on the brink of economic collapse. An unholy amalgamation of demographics, fiat currency, debt, taxes, power and greed have led us to this point. Next we experience collapse, revolution and ultimately, retribution.

Since I’ve identified four major rationales for our impending doom, I’ve decided to write a four part series that can be read in small doses, rather than one enormous article. I don’t want anyone to miss tonight’s episode of Dancing With the Stars, get distracted from the Royal Wedding preparations, or skip the best reality TV show ever – Ben Bernanke’s press conference, while reading an 8,000 word article about the end of America. The four part series will have a Clint Eastwood theme. For a Few Dollars Morewill address the Baby Boomer impact on America’s decline. A Fistful of Dollarswill examine how the creation of the Federal Reserve and the income tax in 1913 set us on a path to ruin. Outlaw Josey Waleswill scrutinize the looting of America by a small group of powerful, connected, super rich men lurking in the shadows, but pulling the strings on our puppet politicians. Lastly, Unforgiven will detail the impending collapse of our economic system and the retribution that will be handed out to the guilty.

Over the last few weeks there seems to be consensus among many financial bloggers, whose credibility is far more trustworthy than the corporate mainstream media, that the country is teetering on the verge of economic collapse due to the complete capture of the government, financial, regulatory, and media by a small group of oligarchs. They have also been described as the super rich, plutarchs, ruling elite, and scum sucking leeches. The bloggers that I have the utmost respect for, including Jesse, Charles Hugh Smith, Mike Shedlock, Yves Smithand Gonzalo Lirahave all come to the logical conclusion the horrific economic situation of the country is a direct result of the greed, corruption, fraud, and plundering by a powerful connected group of rich financiers operating without fear of being brought to justice by the authorities.

While pondering the ruminations of these dedicated truth tellers, I was reminded of the Clint Eastwood Spaghetti Western For a Few Dollars More. The quotes above are representative of living in the USA today. There are supposed to be courageous, loyal and honest sheriffs that protect the citizens from crime, corruption and evil doers. But, just as we saw in the Old West of Clint Eastwood movies, the sheriffs are always corrupt and bought off by the evil cattle barons. In a world where life has no value and you can’t rely on law enforcement to protect your interests, the citizens eventually will need to turn to bounty hunters to take care of the bad guys. The bounty hunters of truth reside on the internet. They reside at Zero Hedge, Jesse’s Café Americain, Of Two Minds, Mish, Chris Martenson, and dozens of other anarchist websites. When you can’t trust your government, your bankers, your church, your media, or mega-corporate CEOs, you need to seek the truth where it can be found. The insightful bloggers who courageously print the truth on a daily basis have unanimously concluded that a small band of powerful elite have accumulated undue influence and control over this country, having brought it to the verge of economic collapse. How did this happen? Who is responsible? Why were they permitted to gain this power?

Boomers Come of Age

“If those in charge of our society – politicians, corporate executives, and owners of press and television – can dominate our ideas, they will be secure in their power. They will not need soldiers patrolling the streets. We will control ourselves.” – Howard Zinn

Whenever I direct any blame for our economic woes towards the Baby Boom generation they react as expected. They blame the GI Generation for creating the welfare state. They declare that Generation X and the Millenials are just as greedy and self centered as the Boomers. Boomers are great at blaming, ridiculing and acting pompously, while taking no responsibility for their actions and more importantly their inaction. This generation cannot avoid their responsibility for the state of affairs. They like to take credit for their stand against the Vietnam War and their protests against the man during the 1960s. They don’t like to take credit for turning into materialistic, greedy, selfish, short-term focused bastards. When a generation of 76 million people decides to go in a particular direction, the country will go in that direction. While blaming FDR and the GIs who stormed the beaches of Normandy for creating the unfunded Social Security and Medicare liabilities, the Boomers have been voting since the mid-1960s and have been in control of corporate America and the levers of government since the early 1980s.

The U.S. Congress is dominated by Baby Boomers today and has been dominated by this generation since the 1990s. The Senate has 60 Boomers out of 100, while the House of Representatives has 254 Boomers out of 435 members. Boomers occupied the White House from 1992 through 2008. They have had the political power and control of the agenda for two decades and have failed miserably. Rather than do what was best for the country for the long-term, they took the expedient, easy, vote getting route. Promise more than you could ever deliver and let future generations worry about the consequences. Not one true noble statesman has arisen from this generation of myopic, self centered “Me Generation” political hacks. Even as the country nears the precipice, they continue to address the great issues of the day with talking points supplied by other Baby Boomer PR maggots from Park Avenue. These weasels care not for the country, but worry only about poll numbers and the next election cycle. An apathetic public, dominated by the Baby Boom generation, has the attention span of a gnat. As long as they can make the lease payment on their Escalade, use one of their 15 credit cards at the Mall, be entertained by 600 cable TV stations, play with the latest iSomething, live in their McMansion for two years without making a mortgage payment and consume massive quantities of fast food, then any thoughts of future generations or civic duty are unnecessary. Live for today has been the rallying cry for the Boomer generation. Pot was their drug during the 1960s. Debt has been their drug since 1980.

The drug (debt) dealer for the Baby Boom generation has been the Wall Street mega-banks, coincidentally, run by Boomers. The entire corrupt financial industry is being run by Boomers. The CEOs, CFOs, and the thousands of Harvard MBA VPs that created the fraudulent derivative scheme to bilk billions from clueless municipalities, pension funds and American taxpayers are all Boomers. It is no coincidence that the great debt delusion began in the early 1980’s. Jim Kunstler captured the essence of Boomer transformation:

“The Baby Boomers came back from the land, clipped their pony tails, discovered venture capital, real estate investment trusts, securitization of “consumer” debt, and the Hamptons. Greed was good.”

The Boomer CEO hall of scam has been built on the brilliance and financial acumen of Lloyd (god’s work) Blankfein, Charlie (keep dancing) Prince, Jamie (friend of Obama) Dimon, and the king of the Boomers, Hank (the system is sound) Paulson. These mainstays of crony capitalism led the Boomer charge of greed, greed and more greed. The Baby Boomer generation has been the proverbial pig in a python working its way through the decades as presented below. By 1985, Boomers had entered the work force in full force with the entire generation between the ages of 25 and 42. It will be a great day when the python craps this pig of a generation out the other end.

It is not a coincidence the National Debt growth has far outstripped GDP growth since 1980. Boomers had been spoiled their whole lives and felt they deserved the goodies today while passing the bill to future generations. They voted for politicians who promised them more benefits, more programs, more subsidies, more tax breaks, more military adventures, and more pleasure. And this was “paid for” with more debt. Thirty five years of government debt declining as a percentage of GDP was reversed over the next thirty years starting in 1980, pushing it past the 90% tipping point in the last year. The country is over-indebted to the tune of $9 trillion on a current basis and $100 trillion on a long term accrual basis.

There is no better picture of Boomer decadence and myopia than an historical view of the national savings rate. The parents of the Boomers understood the meaning of sacrifice and investing in the future of the country. During World War II they bought US War Bonds to support the cause. From 1950 through 1985, the savings rate consistently ranged between 7% and 12%. Americans had this odd notion that if you saved more than you spent, you actually got ahead in life. Excess savings were used to invest in new plants and equipment that were used to produce goods and employ more Americans. By 1985, the Boomers considered these notions as quaint and old fashioned. The savings rate methodically declined until it went negative in 2006, just prior to the worldwide financial conflagration. Our inspirational Boomer president George (Mission Accomplished) Bush while waging two wars of choice, asked for the ultimate sacrifice from the Boomers. He solemnly urged them to buy a GM SUV with $0 down and 0% interest for 7 years, so we could defeat the terrorists. The Boomers who ran GMAC were more than happy to make loans to people with no income so they could “purchase” a $40,000 ostentatious gas guzzling hog. They were doing their patriotic duty for the good of the nation. It brings a tear to my eye just thinking about it.

The Boomers not only heeded George’s call, but they did him proud by buying 8,000 sq ft McMansions with $0 down and negative amortization ARMs. Luckily, the executives at the mortgage origination sweatshops were Boomers. They found no good reason to verify income or assets before loaning someone $600,000, because they knew their fellow Boomers at the rating agencies would rate the bundles of these toxic shit loans as AAA so the Boomers on Wall Street could sell them to greater fools. GMAC’s exemplary subprime mortgage arm – Ditech, did a bang up job getting migrant Mexican workers into $450,000 homes in California’s inland empire. As the tsunami of bad debt swept toward shore, delusional Boomers across the land borrowed $500 billion against the inflated value of their McMansions and installed granite counter tops, stainless steel appliances, home theatres, elegant patios, Olympic sized pools, and with the excess home equity, leased a BMW or two. The first devastating tsunami wave hit in 2008 and wiped out billions in faux Boomer wealth. Instead of learning a brutal lesson and reverting back to saving and frugality, the “never say sacrifice” Boomers ventured out to where the waves had subsided looking for more trinkets and treasures.

The next tsunami wave is on its way. The delusional Boomers will be surprised again.

The Boomer persona has been formed over the last five decades and the country will deal with the consequences for decades to come. The clean cut Beaver Cleaver children of the 1950s turned into the pot smoking Dobie Gillis of the 1960’s, then into the slimy Gordon Gekkos of the 1980s and ultimately into the eternal wealth seeking Gollums of today.

This Boomer debt orgy over the last thirty years would have made Caligula blush. Of course, none of this could have happened without the Creature from Jekyll Island. I will address this aspect of our fate in Fistful of Dollars– Part Two.

Now for the righteous indignation from the Boomers that think I have unfairly lumped them all together as one. Their reactions are predictable. Even though they have had the means, the power and the time to reverse the course of USS Titanic, they plowed full steam ahead into the abyss. The GI Generation is dead. Generation X doesn’t hold the reins of power. The Boomer generation needs to look in the mirror to recognize who is to blame. I’m sure there are a few good Boomers out there somewhere, but as a generation they have failed this country and our unborn generations miserably.

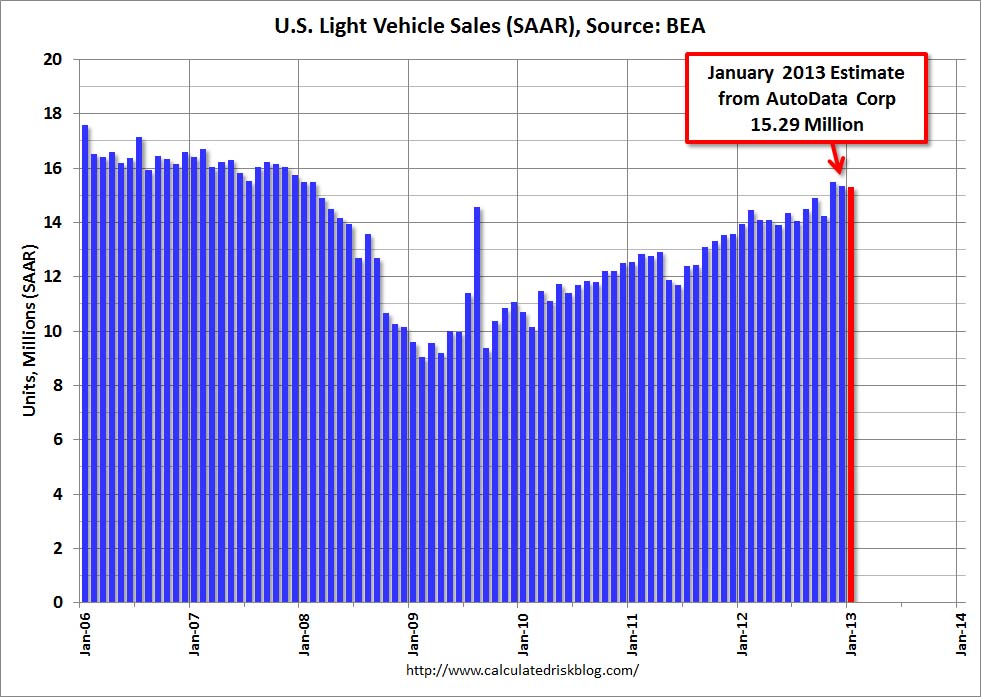

Have you heard the news? Auto sales are booming. Total sales for the month of August were 1,285,202 vehicles, according to Autodata Corp, the highest monthly sales figure for any August since 2007, when 1.47 million autos were sold in the United States. Year to date auto sales have totaled 9.7 million and are on track to reach 14.5 million. Between 2006 and 2007, auto sales ranged between 16 million and 18 million. They crashed below 10 million in 2009. The Keynesians running our government have pulled out all the stops to restart this engine of consumer spending. First they wasted $3 billion of taxpayer funds on the Cash for Clunkers debacle. Almost 700,000 perfectly good cars were destroyed in order to keep union workers happy. This Keynesian brain fart distorted the used car market for two years, raising prices for cars needed by the working poor. After that miserable failure, they realized the true secret to selling vehicles is to give them away to anyone that can scratch an X on a loan document, with 0% interest for 60 months, financed by Federal government controlled banking interests. Add in some massive channel stuffing and presto!!! – You’ve got an auto sales boom.

General Motors sales are up 3.7% over 2011. Ford Motors sales are up 6% over 2011. The Obama administration continues to tout their saving of the U.S. auto industry with their bailout in 2009 that saved unions and screwed bondholders. If this strong auto recovery is not an illusion, how do you explain the two charts below? General Motors stock is down 42% since 2011. The highly proclaimed success story called Ford Motors has seen their stock collapse by 50% since 2011. This is surely a sign of tremendous success and anticipation of soaring profits for these bastions of American manufacturing dominance.

This is America, land of the delusional and home of the vain. The appearance of success is more important than actual success. The corporate mainstream media dutifully reports the surge in auto sales is surely a sign the economy is recovering and the consumer has finished deleveraging and is ready to spend again. The government propaganda machine proclaims the surging auto sales are due to their wise and forward thinking policies (like the Chevy Volt). Luckily for them, there are millions of gullible Americans who believe the storyline and are easily convinced that driving a $30,000 new car, financed over seven years, makes them a success. The decades of Bernaysian marketing propaganda has worked its magic on the government educated, math challenged citizenry. There are only two things that matter to the non-thinking auto buyer (renter) – the monthly payment and what the next door neighbor and his coworkers will think. Buying a fuel efficient car they can afford, paying it off in three or four years, and driving it for ten years, while saving the monthly car payment, is what a practical, rational thinking person would do. The fact that only 20% of the 9.7 million vehicles sold this year have been small cars and the average sales price of new cars sold is now $31,000 proves Americans are still living in a delusional fantasyland of cheap gas and monthly payments for eternity.

As gas prices surpass $4 per gallon across the country, somehow 4.7 million of the 9.7 million vehicles sold in 2012 have been pickups, vans, crossovers or SUVs. Three of the top eight selling vehicles are pickups. Luxury vehicle sales are booming, with Mercedes, BMW, Porsche, Land Rover and Audi showing double digit percentage sales gains over 2011. We’ve entered a recession, gas prices are approaching all-time highs, job growth is pitiful, and Americans continue to buy luxury gas guzzlers on credit. This will surely end well.

The average payment on a new car in 2012 is $461. For used cars, the average monthly payment is $346. Today, 77% of new car purchases are financed. About half of all used vehicles involve financing. Of those cars financed, 89% are through a loan vs. 11% with a lease. A critical thinking person might wonder how a country with 4 million less employed people than we had in 2007, median household net worth down 35%, and real wages lower than they were in 2007, could be experiencing an auto boom. The answer is a government/corporate/banker/media effort to funnel taxpayer funds to deadbeats across the land in a fruitless attempt to create a facade of recovery. Our governing elite are convinced that more debt peddled to the masses is the path to recovery for an economy that imploded due to excessive debt peddled to the masses in the first place. Essentially, it comes down to who benefits from the peddling of debt. It isn’t the masses, as they become enslaved in the chains of debt and monthly payments in perpetuity. Debt peddling benefits Wall Street bankers, politicians, and mega-corporations selling crap to the masses.

The storyline being sold to the vegetative dupes (watching Honey Boo Boo) that occupy space in this delusional paradise we call America, by the corporate media, is that consumers have deleveraged and are ready to resume their “normal” pattern of spending money they don’t have on stuff they don’t need. Of course, the facts always seem to get in the way of a good yarn. Consumers have never deleveraged. Consumer credit outstanding is at an all-time high of $2.58 trillion. The decline from $2.55 trillion in 2008 to $2.4 trillion in 2010 was NOT deleveraging. It was the Wall Street Too Big To Fail banks taking a big dump on the American taxpayers. They passed their bad debts to you through TARP, the Federal Reserve buying their toxic “assets”, and ZIRP.

Revolving credit (credit card) debt peaked at just above $1 trillion in 2008 and “declined” to $850 billion during 2010. The media storyline is that you buckled down and paid off your credit cards, therefore depressing consumer spending and creating a recession. Sounds convincing except for the fact that it’s a load of bullshit. The Federal Reserve’s own data proves it to be false. Your friendly Wall Street banks have written off $213 billion of credit card debt since 2008 and passed the bill to the few remaining taxpayers in this country. For the math challenged, this means that consumers have actually INCREASED their credit card debt by $68 billion since 2008. The bad news for our Chinese crap peddling mega-retailers is that the significantly poorer average middle class American household is using their credit cards to pay their property tax bills, IRS bills, and utility bills in order to survive.

Credit Card Charge-off in Dollars 2005 – 2011 — Not Seasonally Adjusted:

Year

Dollar Amount

2011

$46,017,459,671

2010

$75,090,106,350

2009

$83,179,901,000

2008

$53,506,353,600

2007

$38,149,440,000

2006

$32,111,934,400

2005

$40,634,994,400

Year & Quarter

Dollar Amount

2012Q1

$8,772,385,443

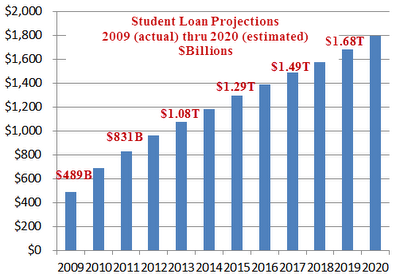

The category of debt that barely budged in the 2009 collapse was non-revolving credit. It stayed in the $1.5 trillion range in 2009 and has since surged to over $1.7 trillion in 2012. What could possibly have made this debt skyrocket by $200 billion when the GDP has only grown by 12% over the same time frame? You guessed it – your corporate fascist friends in Washington DC and on Wall Street. Non-revolving debt consists of auto loan debt of $663 billion and student loan debt of approximately $1 trillion. Student loan debt has shot up by $300 billion since 2008. This student loan debt is being distributed, like candy by a pedophile, from the Federal government in an effort to artificially hold down the unemployment rate.

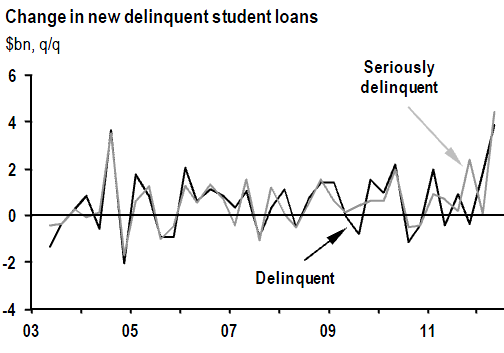

Approximately $500 billion of the student loan debt is held directly by the Federal government, up from $100 billion in 2008. The Feds guarantee the majority of the remaining student loan debt. Can you think of a more subprime borrower than a 40 year old former construction worker getting a liberal arts degree from the University of Phoenix, sitting at his computer in his underwear scratching his balls, and paying with a $10,000 Federal student loan from you? This fraudulent attempt to obscure the true employment situation will end in tears for the borrowers and the American taxpayer. It’s tough to make a loan payment without a job. The student loan bailout is just over the horizon and will cost you at least $300 billion. Delinquencies are already off the charts.

When has offering low interest debt in ample portions to people without jobs, income or assets ever backfired before? The bankers and politicians that control this country seem to be a one-trick pony. They will never admit that debt is the problem and reducing it the solution. The real solution would make them poorer, so their solution is to pour gasoline on the fire with more debt at lower interest rates to more people. The addict will keep injecting more poison into their system until sudden death. The bankers and politicians know we are a car-centric society and appeal to our vanity and poor math skills to keep the game going.

During the first quarter of this year, total U.S. car loans totaled $52.5 billion. That’s 49% higher than the same period in 2009. Also during the first quarter, the average amount financed on new vehicles rose by $589, to $25,995, and for used cars by $411, to $17,050. Furthermore, buyers are stretching out payments for longer terms: The average length of new- and used-vehicle loans jumped a full month during the first three months of this year, to 64 and 59 months, respectively. The surge in auto sales is being completely driven by doling out more loans for a longer time frame to deadbeat borrowers. Subprime auto loans now make up 45% of all car loans and the vast majority of all used car loans. They have even created a category called Deep Subprime. Borrowers classified as “deep subprime” (i.e. those with Vantage scores below 600) account for 10.7% of auto loans. You can also classify them as loans that will never be repaid.

Two thirds of all car sales are for used cars, so the fact that 37% of all new cars are being sold to subprime borrowers is exacerbated by the ridiculous lending practices for used cars. The fine folks at Zero Hedge have provided the outrageous data and a chart that proves beyond a shadow of a doubt what awaits the American taxpayer – another bailout. Zero Hedge has already revealed the GM fake recovery by detailing their channel stuffing over the last two years. Now they’ve dug up more dirt on why car sales are surging. What could possibly go wrong providing loans for more than the value of the asset to people with a history of not paying their debts?

Subprime borrowers received 56.46% of loans on used cars in the quarter, up from 52.70% a year earlier.

The average loan-to-value on new cars was 109.55%

The average used car loan-to-value ratio rose to 126.62%

77% of Subprime Auto Loans are for a period greater than five years

It’s amazing how many cars you can sell when you aren’t worried about getting paid. This is the beauty of a fiat currency, a printing press, and a taxpayer available to pick up the tab after the drunken party gets out of hand. The chart below provides the details of our superhighway to disaster. The percentage of used car loans to prime borrowers is now at an all-time low, while the percentage of loans to subprime borrowers is near all-time highs reached just prior to the 2008 crash. When lenders cared about being paid back in the early 2000’s, they rarely made loans longer than five years. Today, more than 77% of all subprime used car loans are longer than five years and average FICO scores are now well below 600. Just to clarify – if your FICO score is below 600 – YOU ARE A DEADBEAT.

When you start to connect the dots, things that didn’t seem to make sense begin to crystallize. This is all part of the master plan concocted by Bernanke, Geithner, Obama and the Wall Street Shysters. The auto section of my local paper now makes sense. Offers of 7 year financing at 0% interest and monthly lease offers of $150 to $200 for brand new cars now are understandable. The newer model BMWs, Cadillac Escalades, Volvos, and Jaguars I see parked in front of the low income luxury gated townhome community in West Philadelphia now makes sense. A pizza delivery guy driving a new Lexus is now explainable.

The master plan is fairly simple. The Federal Reserve lends money to the Wall Street banks for 0% interest. These banks then turn around and provide credit card debt at 13% interest, new & used car loans to prime borrowers at 5% interest, and new & used car loans to subprime borrowers at 16%. When you can borrow for free, you can take a chance that a significant number of your borrowers will default. Essentially, Ben Bernanke is screwing the prudent savers and senior citizens by paying them 0.15% on their savings in order to subsidize the bankers that destroyed the country so they can make auto loans to the same people who took out the zero percent down interest only no doc mortgage loans in 2005. In addition, Wall Street knows the Bernanke Put is still in place. If and when these subprime loans explode in their faces again, Bennie, Timmy and Obamaney will come to the rescue with your tax dollars. Its heads you lose, tails you lose, again.