In Part One of this three part article I laid out the groundwork of how the Federal Reserve is responsible for the excessive level of debt in our society and how it has warped the thinking of the American people, while creating a tremendous level of mal-investment. In Part Two I focused on the Federal Reserve/Federal Government scheme to artificially boost the economy through the issuance of subprime debt to create a false auto boom. In this final episode, I’ll address the disastrous student loan debacle and the dreadful global implications of $200 trillion of debt destroying the lives of citizens around the world.

Getting a PhD in Subprime Debt

“When easy money stopped, buyers couldn’t sell. They couldn’t refinance. First sales slowed, then prices started falling and then the housing bubble burst. Housing prices crashed. We know the rest of the story. We are still mired in the consequences. Can someone please explain to me how what is happening in higher education is any different?This bubble is going to burst.” – Mark Cuban

Now we get to the subprimiest of subprime debt – student loans. Student loans are not officially classified as subprime debt, but let’s compare borrowers. A subprime borrower has a FICO score of 660 or below, has defaulted on previous obligations, and has limited ability to meet monthly living expenses. A student loan borrower doesn’t have a credit score because they have no credit, have no job with which to pay back the loan, and have no ability other than the loan proceeds to meet their monthly living expenses. And in today’s job environment, they are more likely to land a waiter job at TGI Fridays than a job in their major. These loans are nothing more than deep subprime loans made to young people who have little chance of every paying them off, with hundreds of billions in losses being borne by the ever shrinking number of working taxpaying Americans.

Student loan debt stood at $660 billion when Obama was sworn into office in 2009. The official reported default rate was 7.9%. Obama and his administration took complete control of the student loan market shortly after his inauguration. They have since handed out a staggering $500 billion of new loans (a 76% increase), and the official reported default rate has soared by 43% to 11.3%. Of course, the true default rate is much higher. The level of mal-investment and utter stupidity is astounding, even for the Federal government. Just some basic unequivocal facts can prove my case.

There were 1.67 million Class of 2014 students who took the SAT. Only 42.6% of those students met the minimum threshold of predicted success in college (a B minus average). That amounts to 711,000 high school seniors intellectually capable of succeeding in college. This level has been consistent for years. So over the last five years only 3.5 million high school seniors should have entered college based on their intellectual ability to succeed. Instead, undergraduate college enrollment stands at 19.5 million. Colleges in the U.S. are admitting approximately 4.5 million more students per year than are capable of earning a degree. This waste of time and money can be laid at the feet of the Federal government. Obama and his minions believe everyone deserves a college degree, even if they aren’t intellectually capable of earning it, because it’s only fair. No teenager left behind, without un-payable debt.

According to National Center for Educational Statistics, colleges and universities will award 1 million associate’s degrees and 1.8 million bachelor’s degrees in 2014-2015. So they are admitting more than 5 million in the front end, with only 2.8 million ever earning a degree. That means almost 50% never graduate, confirming the SAT predictive results. Then there is the fact an associate’s degree and most of the liberal arts degrees awarded qualify the graduate for a fry cook job at Burger King. What is even more fascinating in this episode of absurdity is the fact undergraduate enrollment has fallen by 930,000 in the last two years and stands only 700,000 higher than when Obama took office. A critical thinking person might ask how student loan debt could grow by $500 billion when college enrollment only grew by 700,000. That is $711,000 per additional student in college. Something doesn’t add up.

The Federal government couldn’t possibly have doled out $500 billion to anyone with a pulse as a way to manipulate the national unemployment rate lower, because anyone in school is not considered unemployed. Do you think the $500 billion was spent on tuition and books? Or do you think those “students” used it to for hookers, blow, booze, iGadgets, HDTVs, online poker, weed, fantasy football entry fees, and Linkedin stock? – Whatever it takes to boost GDP. With default rates already at all-time highs and accelerating skyward, with $131 billion of loans already in serious delinquency, you don’t need a PhD from the University of Phoenix (where default rates exceed 30%) like Shaq to realize the American taxpayer is going to get it good and hard once again.

It seems the for-profit diploma mills and community colleges account for a huge percentage of loan defaults. They are nothing but bottom feeders in a feeding frenzy of Federal loans. The five schools in the country with the highest level of defaulters from 2011 through 2014 are as follows:

- University of Phoenix – 45,123

- ITT Technical Institute – 11,260

- Kaplan University – 10,684

- DeVry University – 9,081

- Ivy Tech Community College – 7,237

These institutions of lower learning spend more annually on marketing than Ivy League business schools generate in total revenue. They are nothing more than swindlers, gaming the Federal loan system, and dispensing virtually worthless diplomas, and leaving its students deep in debt. The true consequence of providing easy money to people who shouldn’t be in college has been to drive up tuition rates at all colleges and universities. Without this $500 billion infusion of illusion, demand would drop, the diploma mills would go out of business, and legitimate institutions would have to lower tuition rates to attract students. But that’s not how Obama and his administration roll.

The biggest scam is the reported default rate disseminated by the Fed and regurgitated by the mainstream media. There are over 7 million borrowers in default on a federal or private student loan. Roughly a third of Federal Direct Loan Program borrowers have been forced into choosing alternative repayment plans to lower their payments. The reported 11.3% delinquency rate is based on total student loans outstanding. In reality 50% of the loan balances are held by students still in school, in their grace period, in deference, or in forbearance. They haven’t been required to make a payment yet. Of course the loans in deference or forbearance due to unemployment or economic hardship are essentially an allowable delinquency. The true delinquency rate on loans in the repayment cycle is 23%. This strongly implies that taxpayers will be on the hook for at least $250 billion of losses.

The long term impact on borrowers is also dire. Student loan debt cannot be extinguished in bankruptcy. It will follow them throughout their lives. Defaulting on a federal student loan has serious consequences. Unlike other consumer credit, borrowers in default on a federal student loan might see their tax refund taken and their wages garnished without a court order. The impact on their credit rating will keep them from buying a home. The pure volume of student loan debt is currently restricting household formation, first time home buyers, marriages, and consumer spending. The unintended negative consequences of issuing hundreds of billions in bad debt have far outweighed the ephemeral short term fake benefits. But short-term appearances are all that matter to the ruling class.

As of the fourth quarter of 2014, 11.3% of all borrowers were in default, with an additional 7% of borrowers having defaulted in the past. Another 6% of borrowers were in earlier stages of delinquency, but not yet defaulted; fully 37% of borrowers had at least one missed payment on their credit report. The chart below shows the cohort of student loans since 2005. Each cohort has progressively worse default experience. Roughly one quarter of each of the cohorts has defaulted as of the fourth quarter of 2014. The default rate of the 2009 cohort has surpassed that of the earlier cohorts much more quickly. Based on historical trends, the 2009 cohort will experience close to a 40% default rate. And this is before Obama unleashed the torrent of subprime student loan debt.

Only an Ivy League educated Princeton economist could examine the facts presented and conclude these were brilliant fiscal policy decisions which have boosted economic activity and fended off another Depression. A rational thinking person would conclude these desperate reckless measures will result in far worse outcomes when the debt dominoes begin to fall.

We are in a World of Debt

“After the 2008 financial crisis and the longest and deepest global recession since World War II, it was widely expected that the world’s economies would deleverage. It has not happened. Debt continues to grow. Since 2007, global debt has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points.” – McKinsey

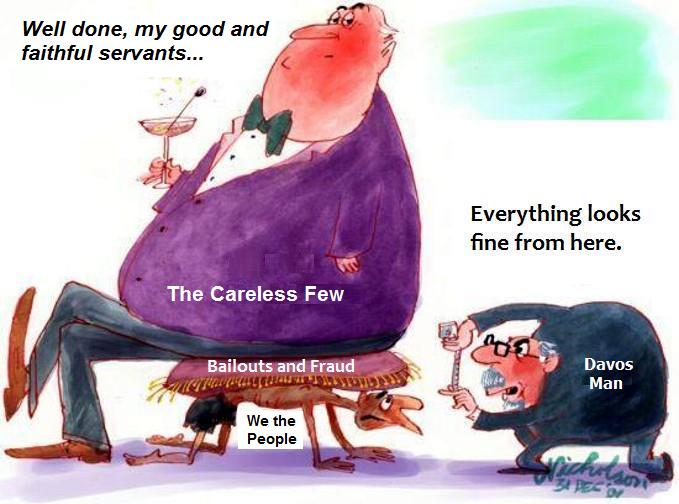

It seems McKinsey is making the mistake of thinking like a logical sentient human being, rather than intellectually dishonest central bankers, criminally psychotic Wall Street CEOs, greedy myopic mega-corporation CEOs, or captured cowardly politicians. In a world run by honest, intelligent, rational people who cared about the long-term sustainability of our economic system, the actions taken after the 2008 debt fueled implosion would have been far different than the actions taken by the psychopathic, greedy, ego maniacal, hubristic moneyed interests over the last six years.

The 2008 worldwide financial crisis was produced due to excessively easy monetary policy, which caused the largest debt driven mal-investment in housing, automobiles, and Chinese produced crap in world history. It was done purposely by a uber-wealthy ruling class who call the shots, rig the game, reap the benefits, and deny responsibility when their machinations create havoc and suffering across the globe for the masses.

The consequences of this debt bacchanalia should have been the orderly liquidation of the Wall Street entities that created the crisis, the writing off of trillions in bad debt, corporate and personal bankruptcies of businesses and people who borrowed recklessly, a sharp steep economic decline to cleanse the excesses, and politicians who immediately began the process of reducing budgets and addressing long term unfunded unpayable liability promises. Instead, the psychotic oligarchs did not want to lose any of their power, wealth or control over the proletariat. They have done the exact opposite of what needed to be done. You must deleverage to solve a crisis caused by excessive debt. The oligarchs have succeeded in further raping and pillaging the working class, but have only delayed the final reckoning and guaranteed a debt apocalypse when their futile schemes fail again. And fail they will.

Arrogant condescending central bankers, narcissistic Wall Street psychopaths, crooked bought off politicians, and narrow-minded government apparatchiks across the developed world have colluded to add $57 trillion of additional debt to the existing Himalayan Mountain of unpayable debt we started with in 2008. We’ve entered the NIRP phase of the currency debasement race for the bottom.

Households throughout the developed world have acted in a relatively rational manner by paying down credit card debt and attempting to live within their means, because their real wages continue to decline and they are receiving no return on their savings. The moneyed interests continue to prey on the desperate and financially ignorant in their last ditch desperate attempt to loot the remaining treasure from the U.S.S. Titanic, hijack the remaining lifeboats, and leave the American people to sink into the frigid murky depths.

Corporate titans have added $18 trillion of debt as they take on debt to buy back their overpriced stock, artificially enhancing earnings per share and boosting their own compensation packages. Investing in their business is passé. We’ve entered a new paradigm where driving your stock price higher is all that matters to the Ivy League MBA executives. The Financial sector has shifted most of their toxic debt onto the Federal Reserve balance sheet and the backs of the American taxpayer.

The governing bodies of Japan, the EU, and the US have accounted for the vast majority of the $25 trillion increase in debt by the government sector. Total world debt as a percentage of World GDP is now approaching 300%. In 2000, the percentage was 185%. This level of debt can’t be sustained at zero interest rates, let alone normalized rates of 5%. Something that can’t be sustained won’t be. It is mathematically impossible for $200 trillion of debt to ever be repaid. It’s just a question of who gets screwed. And if the moneyed interests have their way, it’ll be you.

Everyone loves a boom. The party from 1996 to 2000 was a blast. Remember your moronic brother-in-law boasting about getting rich day trading. The bust was a bummer and your brother-in-law had to get a job at Wendy’s. The highly educated academics at the Fed couldn’t allow the pain or consequences to last. They made it their sole responsibility to create another boom from 2003 to 2008. It was a real doozy. The hangover afterwards was going to be epic.

The party should have been over, but Ben and Janet know better than the rest of us. Ben is a self-proclaimed expert on the Great Depression. Pain isn’t fun. Corrections and adversity must be banned. They have now created the most all-encompassing debt fueled contrived boom in history, with debt, stocks, and real estate all outrageously overvalued. The party has been going on for over five years. The inevitable collapse will be earth shatteringly horrendous. The public will be shocked once again. The anger, disillusionment, and shattering of confidence in the powers that be will be monstrous. This time there will be blood.

“The boom produces impoverishment. But still more disastrous are its moral ravages. It makes people despondent and dispirited. The more optimistic they were under the illusory prosperity of the boom, the greater is their despair and their feeling of frustration. The individual is always ready to ascribe his good luck to his own efficiency and to take it as a well-deserved reward for his talent, application, and probity. But reverses of fortune he always charges to other people, and most of all to the absurdity of social and political institutions. He does not blame the authorities for having fostered the boom. He reviles them for the inevitable collapse. In the opinion of the public, more inflation and more credit expansion are the only remedy against the evils which inflation and credit expansion have brought about”. – Ludwig von Mises

Despite the non-stop propaganda campaign waged by the ruling class through their media mouthpieces about a non-existent economic recovery, the papering over of the gaping funding holes through the issuance of $57 trillion more debt, the waging of wars against terrorists we created to distract the masses, conducting coups against our latest perceived enemies, and the blatant rigging of financial markets to extract the remaining wealth of the nation from the people, the crack-up boom is nearing its endgame. The system is exceptionally fragile. Confidence in leaders is waning. The people are growing weary of the lies and their restlessness will morph into anger when the economic collapse resumes. You can sense things are not right. Trust in the system has turned to suspicion and cynicism. The growing anger in the nation and the world is palpable. Violent protests are a daily event, even if the mainstream media doesn’t report them.

Yellen, Draghi, and Kuroda speak as if they know what they are doing, perform confidently when on stage, but continue to act in desperate manner five years into a supposed economic recovery. The emergency measures they continue to employ and expand upon reveal their angst and inability to implement a monetary solution. Their only tool is the printing press and when confidence in their infallibility dissipates, the system will fail. The stench of fraud, cronyism, corruption, and hypocrisy of the moneyed interests permeates our degraded culture of materialism, greed and criminality. The party was fun while it lasted, but it is reaching its sordid drunken climax in the near future. There is no means of avoiding the final collapse of this Federal Reserve created boom.

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.” – Ludwig von Mises

Ok ,so your saying financial Armageddon is on the horizon . Now we need to know what you think it will be like or look like.You said there will be blood and I agree.I guess what I’m asking is do you think the government will declare martial law ?. Will we lose any rights? Will the banking system completely collapse ? We there be food shortages and riots? How bad do you think it will get ? During the next collapse is there anything the federal reserve can doto prevent a total economic destruction of the currency?

Damn Admin , every time you write an article like this I always have a godzillaion questions I would like to ask.This information is enough to make anyone worry .

bb

The answer is yes to all of your questions. The Federal Reserve will cause the final collapse. The Federal government is the enemy. They are already preparing to kill you if you don’t follow orders. Prepare for the worst case scenario because that is the one we will be faced with.

I almost forgot. As always you did a good job. Makes me worry about the tribulations coming our way.I just wish we had some answers to the hard questions.How are you ,me and others going to survive.

If the Admin knew the answers to those questions, I think he would rule the world.

A good friend of mine moved to Paris, he took his wife and two boys for a weeks vacation in Greece, he’s only posted some pics on FB but mentioned in his post while the people seemed nice and the food good, they witnessed two violent riots in the streets of Athens. He said it’s still tense in Paris as well.

On a note of student loans, the wife and I joined a 60th birthday party for my daughter in laws dad on Saturday night (big liberal with lots of liberal pro union friends) they sat around moaning about their kids.

Seems quite a few of the liberal offspring have massive student loan debt, and no futures. The fat one next to me said her 23 year old has a “good job” paying $13.00 per hour, so it’s bout time he moved out. Most were complaining their kids have no jobs at all.

To our amusement they all shared the same story, “My kid got a degree in a field where there are no jobs available.” And of course, “Only the democrats care”

I drank my Jamison’s neat, kept my mouth shut and smiled.

Admin says “The answer is yes to all of your questions. The Federal Reserve will cause the final collapse. The Federal government is the enemy. They are already preparing to kill you if you don’t follow orders. Prepare for the worst case scenario because that is the one we will be faced with.”

And that, folks, largely sums up why I am getting out of Dodge. My story TBA eventually. I am trying to formulate what to say and how to say it.

Basically, what Admin says is the driver. I have mentioned two things on many occasions: 1) that I try to obey the law, and 2) I will not fight the majority as they are getting what they want, and thus who am I to try to subvert the democratic process? Those two things in combination with what Admin has said leaves me with, and to, the get out of Dodge decision.

I have paid my dues, and I have generated very substantial revenue for the country, and I have provided jobs for unskilled people paying a reasonable living wage. I have obeyed the laws, and have done the best I can with what the govt has left me with. The ever increasing regs, the increasing taxes, including Obamacare, the ever increasing risk and cost of running a business, the continual animosity towards small business owners, the denigration of those top 10% that pay the bills for the rest – all of these things have worn me down and I have had enough.

I am working on the article describing what I am doing, why, and how it came about. I hesitate, then restart, then stop, then start again. It is a deeply personal thing, and I am of two minds with regards to sharing it. But I suppose I will in the end.

Jim, your writing is highly persuasive and always well researched. However I must admit that I question whether you personally believe- I mean truly believe- what you write. If you were convinced that all this was actually around the corner, I have a hard time believing that you would still choose to live and work in Philadelphia… A place that as you yourself have described, would be ground zero for urban chaos and destruction.

I am forced to conclude that you are not especially concerned for yourself and your family, given your choice to live in a place that would surely be among the most volitile urban areas in the US should a financial crisis occur. Deeds speak louder than words.

Pining 4

You must not read too well, because I don’t live anywhere near Philadelphia. I live 30 miles north of Philadelphia surrounded by farms. Worry about your own fucking family and I’ll worry about mine.

I question whether 90% of the morons who visit this site have any comprehension skills whatsoever.

I am forced to conclude that I don’t give a flying fuck what you think about me.

Is that clear enough for you asshole?

I am glad you and your family are somewhat out of the line of fire. Best of luck to you.

@LLPOH

I appreciate your desire to get out of dodge – and I am envious of your ability to do so with style and substance.

My question is how exactly is this helping anyone else?

And perhaps you’ve felt you’ve done all that is necessary and helping others is a thing of the past – you have done a lot and I appreciate the aggravation. I can’t help but think being a mentor to humanity sucks.

Leadership is not fun. And yet we need leaders.

So now we have the big Libertarian versus Everyone Else debate – are we capable of mentoring [leading] others – and if so is this actually something we have the gonads to do?

Great 3 part series. Crazy things seem to be accelerating even more so in the new year. Just have a sense this cannot go much longer as it is. Be that as it may, I would like to relate a story about my daughter whom I love dearly. Unlike my other offspring, she is really not college material. None the less, living in Ohio where you are basically screwed if you don’t have a job (read: live in parents basement forever), we encouraged her to apply to some of the State universities even after a disasterous ACT score of 19 and then a follow up 18. To my shock, 2 weeks after applying to two respectable State U’s. she received an acceptance letter with the gall to congratulate her on her high school achievements and good work. She is now attending one of them. In Ohio, and I suspect elsewhere, they are just taking in about everyone who applies to keep the coffers going. It got me to thinking about the low standards that I believe can extrapolate across the country as standards drop and a college diploma becomes increasingly suspect. I am not even talking about the for profit diploma mills. In sum, not only is the country screwed with all these student loans which will never be paid , but a far more troubling scenario, of graduating students who really don’t know anything worthwhile and will be unable to turn said diploma into a real career.

When you lend money to a borrower, you defer consumption The money that you could spend on your self is transferred to another. Why would you do this? Out of the goodness of your heart? When have you donated time to your employer, to a charitable organization for free, without compensation? Money is time, your life’s energy. You had to give of your time and life energy to get money. No corporation gives you goods for less than the cost of manufacture. Money has value and when you lend it you should be compensated for that period of non use. Islam and others who abhor interest, not withstanding.

Your production of goods, as represented by money, is your right to demand goods produced by others.

You must produce to partake of the production others. Whenever, you lend money, your lawn mower. shovel or rake to your neighbor, there must be a deferring of consumption or use by you. Either you have use of it or your neighbor has use of it, there is no other choice, “Tertium non datur”.

Ahhh! The magic of printed money!

Historically, printed money, fiat money, money printed out of thin air has always without exception failed. There is a reason for this. It’s fraudulent. It’s based on fraud. (It’s a moral universe out there, kiddies.) If you accept the premise that ‘you must produce goods in order to partake of the goods of others’, which is deeply rooted in barter, the precursor to money, then any contract you engage in must be, by inference, an exchange of goods. I know there are services, but it all boils down to goods in the final analysis.

The ‘Paper Hangers’, usually governments, today all governments and central banks engage in the practice of kiting paper and substituting it as money. Keynes, the useful idiot, provided the rational for paper kiting, called ‘increased demand’, and other toadies, such as, the FED, Krugman, et al, bolstered the deception.

Central banks print money out of ‘thin air’. That money substitute is use to exchange worthless paper for valuable goods. Therein lays the fraud. There is no exchange of valuable goods for valuable goods. (Note: The value of a Federal Reserve Note is only the value that someone is willing to give you for it. In other words, it’s intrinsic value is 0, but maybe you can con someone to give you something for it.)

It is a premise of law that a contract that is engaged in with willful fraud is no contract. It is ‘null and void’. This is my understanding. I’m sure that the readers will correct me if I am mistaken.

There was a court case, I can’t cite it, where a homeowner was being foreclosed upon. His argument was the when the bank loaned him money, they printed it up out of ‘thin air’ and he had received nothing of value from the bank. The court agreed with the homeowner.

Students, who entered in to a contract to borrow money. printed out of ‘thin air’. for their college education, unknowingly entered into a fraudulent contract. Nothing of value was received from the lender or was conveyed to the borrower. It matters not that the college accepted those worthless pieces of paper. The fraud was perpetrated by the sponsors of that worthless script. It was a fraudulent contract. The students should repudiate those contracts, based upon fraud.

The Government and banks gain from this deception and the ones who lose are the ones that are left holding these ‘worthless pieces of paper’. It has always been so!

Administrator—The government is like a tiger. When you are starving to death with a tiger, The tiger starves last!

Olga – how is it helping anyone else? You mean anyone but my wife and kids and me? Those are the ones that matter to me, and I am indeed doing right by them, as best I can. The rest will have to do the same.

I have done my bit, and I am tired of being denigrated for it. I am not a milch cow, but I am used as such.

As I have said, people are getting what they want – who am I to argue with them. It wastes my life, and is no good for me personally, or for my family.

The good that I have done for society and for others has largely been in vain. No long-term good will come of it, save for those families that I employed that managed to use what I was able to provide to better themselves.

I have done my bit for society. It is time for someone else to do theirs. The benefits that have accrued to me personally are substantial with respect to financial benefits, but what I have retained is but a fraction of the benefits that have been passed along to government coffers. I have had enough of feeding the beast. Someone else can feed him. It will not be me.

I’m in agreement with your forecast, Jim, however I think the situation is even worse. Did you cover the story about the staged “situation room” photo op supposedly while the bin Laden operation played out? Apparently the only other skirt than Hilary in the room is Audrey Tomason (close counterterrorism adviser to Oblunder) whose master’s thesis (now classified) is about the need to depopulate the world, and ways to do it humanely using nuclear radiation. This happened before Fukushima.

http://cubaindependiente.blogspot.com/2011/05/audrey-tomason-situation-room-mystery.html

http://theunhivedmind.com/wordpress/audrey-tomason-calls-for-humane-depopulation-using-nuclear-radiation/

Could the story unfolding before our eyes be according to such a playbook?

bb says, “During the next collapse is there anything the federal reserve can doto prevent a total economic destruction of the currency?”

bb read Von Mises. A short answer is NO! There is no avoiding a currency collapse based on credit expansion. So, party up, bb, cuz you sure ain’t goinna like the hangover.

Llpoh—I can sympathize with you and I understand where you are coming from.

I headed for the ‘hills’ over 30 years ago. I could see even then what the future was going to be. I just never thought that the unfolding would take so long. My timing sucks! It is a small community, but there are enough to kill you. Many are social parasites, living off the productivity of others. They are entitled, you know., Obama says so. A starving person is a dangerous person.

One need to surround themselves with other productive people for any level of salvation, I think. People with a moral understanding. How nice it would be to be a Quaker, or maybe a Latter Day Saint.

Jim, the value of an education is going to be whether you can produce something of value for others and whether others will have the means to exchange with you.

How many Librarians, Archeologist, Psychologists, ect. do we need? What are going to be the needs of the people during this re-adjustment? Time is valuable, spend it on a skill, something that is marketable.

Jim, don’t tell me She is a psychology major.

Move to Puerto Rico. It has great tax advantages, It is surrounded by water ( you can fish for food), it has a warm climate (you can grow food) and the population is small, and they like Americans.

So. get goin’.

Jim,

Another excellent article.

Student Debt is in effect Child Abuse. If private industry were encouraging these practices and dooming many of these kids to a lifetime of poverty, the perps would be jailed. I suspect some of these students are not even 18 when they commit to the loans. Regardless, we know how dumb they are when they get out of college so how dumb must they be when they are conned into this debt slavery.

Monty

Homer , I have read some of Von Mises in the past.I was just hoping. Last week Greenspan said there was going to be major economic crisis or event.I believe a major collapse is not far away.

Don’t go to Puerto Rico . To much crime .If you go you had better have money to live in gated community with it’s own security.

Be careful about body armor. I bought some about two years ago. It is heavy .Hard to get use to.I ended up selling my armor. Do your research . Very important.

Homer – you ever been to Puerto Rico? Ever lived there?

I have lived there. A bigger shit hole there never was. Crime rate through the roof. Filth and trash everywhere.

Puerto Rico? Damn, Puerto Rico sucks and I kid you not.

Llpoh

I share your disgust for the peril of the small business owner, it is hardly worth my effort going forward. Please write your article as I am truly interested. I have posted in the past that I am hedged every way possible but you may add some insight.

Consumer Credit Moving Higher into 2015.75

Posted on March 2, 2015 by Martin Armstrong

Subprime consumer borrowing — encompassing auto loans, credit card loans and personal loans — climbed to $189 billion in the first 11 months last year, the highest total since 2007, according to a study compiled for The Wall Street Journal by Equifax. This is precisely what I mean about living with the cycle. People will spend when they SEE everyone else spending. This provides the foundation to consumer confidence. This is why the rich are important. If they are driving around in flashy cars and going out to dinner, not only are they spending, they are creating the impression everything is OK and this becomes the contagion that spreads as consumer confidence. If they spend nothing and save, the rest of society will follow. It is an interesting leadership role.

This is right on time. We should see the peak in debt on a private level whereas when the economy turns down, governments will be desperately trying to borrow more and more.

I think is safe to conclude that a college degree is no longer proof of higher education , but merely another symbol of social status used to fill up a blank space on an otherwise insignificant resume’ .

I can file this report from the millennial front lines, a college degree is worthless. Even with a respectable bachelors degree (not leisure studies, but not quite STEM either) and five years of management experience I could not get a call back for any jobs, menial or otherwise. If I had to guess at a metric to getting hired these days it would be:

50% – networking / family connections

40% – meeting a quota

10% – experience / skills

The degree is actually negligible, less than 1%. While it’s true that some jobs list it as a requirement, you still won’t get the time of day if you don’t meet the networking or quota requirements. And if you do, you can probably get a pass on not having a degree.

Hey, don’t worry, be happy.

Collapses occur with regularity in all complex societies, ours is no exception.

Collapses mark the end of social orders, not humanity.

Collapses are, in every single case known throughout history, to be based on three levels; resource depletion, societal degeneration and environmental degredation. Every problem fits within one of those subsets, no society known in recorded history has ever re-emerged post collapse in the same configuration and in each case the human species has survived.

None of the above takes into account an ELE.

We have to learn to accept when and where we are born in the timeline of history and to decide whether we wish to be part of the remainder that makes it through to the other side of the collapse or to live fast, die young and leave a beautiful corpse covered in tattoos and Cheetohs colored fingertips.

Oh, and there are no guarantees either way.

Excellent piece once again Jim, really like the multiple part format you’ve created.

Homer, not a Psychology degree but an equally suspect one — Communications. Good luck!

Well said, HSF, collapses have occurred throughout history and for the fundamental reasons you list. These have remained constant throughout the centuries. What changes with each collapse are the details and the coming collapse with be radically different from any other because of technology. The world has changed so dramatically in the past century–I was going to begin a list of the changes and quickly realized it was futile, even a long one would hardly scratch the surface. Also, never before has mankind been capable of causing an ELE. Would mankind be around if Nero had had ICBM’s? Any answer is of course pure speculation, but it won’t remain so for too much longer. The dominoes are beginning to fall and we can only wait and see which way the house of cards falls.

Great article. Thank you for your time.

Housing Bubble Redux: Subprime Auto Market Begins To Crack

Submitted by Tyler Durden on 03/02/2015 10:36 -0500

As noted last week, the aggregate amount of loans for new and used cars will in short order eclipse the $1 trillion mark, joining total student debt in full-on bubble mode. Better still, early delinquencies on auto loans are now sitting back at their 2008 highs (both for all borrowers and for subprime borrowers, with 9% of the latter now missing a payment within the first 8 months of origination). Despite this, and despite the fact that nearly a third of all auto loans in 2013 were made to subprime borrowers (the same amount we saw in 2006 at the very height of reckless underwriting standards), Experian says everything is fine.

Meanwhile, Wells Fargo recently noted that although lending standards had indeed gotten back to “normal” (and as a reminder, “normal” now means how things were in 2006) it’s beginning to look like some households “might be overleveraged.” Simultaneously, lenders are again showing a propensity towards origination for the purpose of selling loans rather than holding them; that is, originating loans and then happily passing them on to the Wall Street securitization machine, which explains why despite a collapse in the issuance of ABS backed by home equity loans since the crisis, total ABS issuance in the U.S. hit its highest level since 2008 last year.

These are things that Wells should know something about as they made some $30 billion in auto loans last year and indeed it now appears the bank may be getting concerned about the market it’s helped to build. As the NY Times reports:

Wells Fargo, one of the largest subprime car lenders, is pulling back from [subprime auto lending], a move that is being felt throughout the broader auto industry…

Wells Fargo has imposed a cap for the first time on the amount of loans it will extend to subprime borrowers.

The bank is limiting the dollar volume of its subprime auto originations to 10 percent of its overall auto loan originations, which last year totaled $29.9 billion, bank executives said.

The decision, detailed in interviews with top Wells Fargo executives, along with other large auto lenders, is a sobering moment for the booming market. Other lenders may decide to take their cue from Wells Fargo, one of the nation’s largest lenders.

The Times’ description of industry dynamics could easily be mistaken for a recap of the buildup to the housing bust, as investors chase returns, Wall Street chases fees, banks ease lending standards to increase volumes, and borrowers who are jobless (which must mean they aren’t experienced waiters) throw every semblance of prudence out the window:

Large banks, weathering a slowdown in other types of lending like mortgages, have increased their auto lending. And much as in the housing boom, investors in search of higher returns, like insurance companies and hedge funds, are buying billions of dollars of investments backed by subprime auto loans.

Such growth, though, has given rise to concerns, like those at Wells Fargo, that growing competition is fostering lax lending practices, including longer repayment periods and increased loan balances.

Federal and state authorities, meanwhile, are examining whether dealerships have been inflating borrowers’ income or falsifying employment information on loan applications to ensure that any borrower, even some who are unemployed and have virtually no source of income, can buy a car.

Just how bad has it gotten? This bad:

Last week at the annual conference of the Global Association of Risk Professionals in New York, Darrin Benhart, a senior regulatory official at the Office of the Comptroller of the Currency, which regulates Wells Fargo, noted that lenders had extended repayment periods to 84 months — 40 percent longer than the typical period — and were making loans that were far greater than the value of the car.

This is perhaps the clearest sign yet that we have learned literally nothing from the crisis years. That is, this is precisely the same dynamic and it will end precisely the same way: defaults will rise, investors in assets backed by these loans will suffer outsized losses, and the assets themselves will become completely illiquid. Indeed, the dominoes have already started to fall. Here’s Fitch with the last word:

Weaker seasonal trends led to annualized net losses (ANL) on U.S. subprime auto ABS reaching their highest level since 2009, according to the latest monthly index results from Fitch Ratings.

Subprime auto loan ABS ANL rose 4.5% month-over-month (MOM) to 8.19% last month, the highest level since February 2009 (9.07%). Prime ANL also crept higher in January.

In the subprime sector, 60+ day delinquencies rose to 4.75% in January, a 7.7% move higher and were 24% above the same period in 2014. This is the highest level recorded since October 2009 (4.76%). Meanwhile, ANL rose 4.5% MOM in January hitting a five-year high when 9.07% was recorded in early 2009. Asset performance has slowed over the past two years driven mainly by softer underwriting and collateral credit quality in securitized pools.

Who owns American debt?

[img [/img]

[/img]

A couple of things stand out:

1. China and Japan are by far the largest owners of U.S. Treasury debt. Both benefit from their currency being weakened and ours being strengthened so they can sell us (relatively) cheap goods.

2. WTF is up with Belgium? Belgium is rapidly increasing its holdings of American debt, up 31% in just a year. Did Belgium suddenly develop a taste for the dollar? No, according to Paul Craig Roberts:

“From November 2013 through January 2014 Belgium with a GDP of $480 billion purchased $141.2 billion of US Treasury bonds. Somehow Belgium came up with enough money to allocate during a 3-month period 29 percent of its annual GDP to the purchase of US Treasury bonds.

“Certainly Belgium did not have a budget surplus of $141.2 billion. Was Belgium running a trade surplus during a 3-month period equal to 29 percent of Belgium GDP? No, Belgium’s trade and current accounts are in deficit.

“Did Belgium’s central bank print $141.2 billion worth of euros in order to make the purchase? No, Belgium is a member of the euro system, and its central bank cannot increase the money supply.

“So where did the $141.2 billion come from?

“There is only one source. The money came from the US Federal Reserve, and the purchase was laundered through Belgium in order to hide the fact that actual Federal Reserve bond purchases during November 2013 through January 2014 were $112 billion per month.”

more here — http://www.opednews.com/articles/Who-owns-American-Debt-by-Scott-Baker-Debt-Ceiling_Debt-Ceiling_Debt-GOP-Tax-Cuts_Economy-Built-On-Debt-150302-616.html

A collapse is definitely in our near future, but it’s not possible to know the date, even to within the nearest year. Rome didn’t collapse in a day and neither will we. Our rich masters have a vested interest in maintaining the pillaging for as long as possible. Even the masters can’t be sure what the world will be like after the collapse (AC). They currently live as aristocrats surrounded by serfs. They could end up in a world of hurt AC. Unfortunately, their avarice will not allow them to back off and let the little people have enough table scraps to maintain the status quo.

Homer…The case you speak of is “First Bank Of Montgomery vs Jerome Daly .

He was a flake but I think he was spot on in his argument that the Banks lent him money that was “Printed ” out of thin air .

I believe the “judge” in this case was murdered shortly after the jury found in Jerome’s favor .

Murdered you say? It seems over time that anyone that stands against the bankers meet their end pushing up daisies. Maybe all the bankers that were helped to commit suicide were changing sides.

How can one not think that this is demonic. There is a great battle being waged between “good and evil”.

It’s choosin’ time. Choose wisely, folks.

pavan says—“A collapse is definitely in our near future, but it’s not possible to know the date, even to within the nearest year.”

Pavan predicting the collapse is easy.

Like Mark Twain said about smoking, “Giving up smoking is the easiest thing in the world to do, why, I’ve done it a thousand times myself.”

Predicting the collapse is easiest thing in the world to do, getting it right is the hard part.

Stucky, you says right! Its all in which set of books they let you read,( books having a double meaning,) which determins the way one understand the world and its economies! I see education as an ambiguity and a Degree just a measure of salt sprinkled on the shiz nittle one shovels to make it palatable! Assuming one believed and was not excommunicated for lack of faith. It might as well be a cult religion , some kind of voodoo economics , its magic ! Just believe hard enough an it will happen!! Like the cowardly lion in the Wizard Of Oz, I do believe in spooks! The Powers that be(men behind the curtain) can pull a rabit out of their @$$ at any time ! But the circle cannot be broken and the Cycle is a hard taskmaster! Can you Glean( definition, to gather slowly and laboriously, bit by bit) it Man!

Westcoaster-Obama’s demeanor in fetal position hunched over with little to no confidence will forever be know as “The smallest man in the room”Barry in his jacket was said to have been pulled from golf coarse,speaks volumes.We all know now that he is just a puppet.

@Anonymous: You & I may know he’s a puppet, a figurehead, but the vast majority do not. Personally I’ve talked myself blue in the face trying to open the minds of mostly the tea party folks who swear by, not at, Fox News, and support their claptrap. Meantime while the non-news memes of the day roll off the screen, the real action is behind the scenes, mostly with people we don’t even know the names of.

Stucky

What is up with Belgium is this, Brussels is to the planet as the underground control Imagineers are to Disney World. You know things have accelerated when they openly intervene….not a good sign for Merikans. The wheels are wonking on the bus and they will maintain control until they are ready for the big show to begin.

The Craven Failure of the ‘Technocrats’ at the Fed

I see where Mr. Bernanke thinks that Presidents should be given extraordinary powers to declare ‘financial emergencies’ and ‘not leave it all up to the Fed.’

And who is it that doesn’t want to be audited, doesn’t want anyone looking over their shoulder, wants to be free to exercise their independent judgement, and keeps raising their hands to be given more and more regulatory powers which they fail to exercise faithfully and objectively over their banking cronies.

And then when they blow up the economy with a financial bubble which they created, they want the nation to clean up their mess, presumably by having the President invoke special emergency powers so that their financial engineering prowess is not encumbered by the democratic rule of law as they continue to throw trillions of dollars at the aftermath of the collapse of financial bubbles for which they have been the chief architects.

Jesse

[img [/img]

[/img]

Looking forward to Llpoh article in depth.

Obvious Lessons Obviously Not Learned: Zero Down Payments Are Back!

by Anthony B. Sanders • March 3, 2015

After the financial crisis of 2008 (nicely summarized by this UK Parliament study RP09-34 (2)), the financial system vowed to return to safe underwriting standards such as 20 percent down payments on mortgages. The US financial system returned to high down payments for a while, but …. the itch is back to make zero down payments loans again.

First, of course, you have the FHA which stuck by it’s low down payment guns (3.5 percent).

Second, you have mortgage giants Fannie Mae and Freddie Mac pushing the enveloped with 3 percent down payment loans.

Third, you have this story from Housing Wire, “BBVA Compass launches zero-percent down mortgage program.” (Banco Bilbao Vizcaya Argentaria, a Spanish bank).

In recent months, the Obama administration has taken several steps to expand the credit box and make it easier for borrowers, especially first-time homebuyers, to buy a home. To that end, in October, Fannie Mae and Freddie Mac announced 97% loan-to-value offerings.

For some borrowers, saving up 3% for a down payment is still a hurdle they can’t quite clear. However, a new program from BBVA Compass (BBVA) will allow borrowers to put down even less for a down payment, in fact.

BBVA Compass announced the launch of a new program, called Home Ownership Made Easier or HOME for short, designed to help low- and moderate-income borrowers become homeowners by helping to overcome one of the “most significant barriers” to homeownership, the down payment.

In the HOME program, qualifying borrowers will be eligible to finance 100% of the home’s value. In addition to offering 100% LTV loans, BBVA will also contribute up to $4,500 toward “certain closing costs” associated with obtaining a home loan.

What could go wrong? 100 percent LTV lending with lenders paying $4,500 of closing costs?

Fourth, you have the American Enterprise Institute (AEI) repackaging the 15 year mortgage with a maximum LTV (loan-to-value ratio) of 100 percent that allows for repurposing the 5 percent in down payment funds for a 1.25 percent permanent rate buydown. The 15 year mortgage rate already available is 3.03 percent compared to a 3.85 percent 30 year fixed, so the AEI’s plan is to buy down the rate even further.

I am a big fan of the traditional 15 year mortgage because of it’s lower interest rate. But the 15 year mortgage also requires a larger monthly payment to amortize the mortgage over 15 years. This will raise the mortgage payment considerably and borrower’s may not be able to meet the debt-to-income (DTI) requirement, even at the lower interest rate AFTER the buydown. AND it is a 100 percent LTV mortgage!

AND this is hardly a mortgage product for low income households. We already have a product for low-income households — it’s called RENTING.

So there you go, sports fans. The financial system is returning to 100 percent (or thereabouts) LTV lending.

Admin – I have submitted my Getting out of Dodge story, but no sure I submitted it right. Please have a look for it if you have not seen it it yet. Thanks.

2015-03-04 11:44 by Karl Denninger

The Tower Shudders

The cracks in the dam have begun to show, and water is spurting from them. Meanwhile, the ivory tower, gold-encrusted with the many millions of taxdebtor dollars (many forcibly extracted from impressionable young people via knowingly-false starry-eyed claims peddled to same) is beginning to sway as the foundation has been undermined — and will soon come crashing down.

SWEET BRIAR — In an announcement that stunned students Tuesday, Sweet Briar College said it will close at the end of this academic year because of “insurmountable financial challenges” blamed on the dwindling number of women interested in single-sex education and the pressures on small, liberal arts schools.

The “insurmountable financial challenge” is charging young adults upward of $100,000 for four year degrees all-in when a liberal-arts education is, in most places, a recipe for a sub-$50,000 a year salary.

This, in a nation where tax burdens on such people in the “middle class” reaches 25-30% of one’s base pay and is guaranteed to rise due to deficit spending and entitlement decisions that cannot possibly be paid on existing cash flow is utterly insane.

It was once the case that you could get a liberal arts degree for about $3,000 a year including books with no other mandatory costs. That is, roughly $100/credit hour. You could live off-campus as you decided but if you wanted to live on campus block-constructed dorms of modest expense were available, making the $5,000/year full-in college education, absent discretionary spending, quite possible.

This, in turn, could be worked for during summer vacation and a part-time, mostly weekend-hour job during the school year, making the proposition one of an entirely sunk cost. Thus, if you only earned $40-50,000 a year after getting your degree you were still ok.

That is no longer possible and it is the intentional acts of the higher-education “industry” that have made it so, along with the idiotic bleating and advocacy for more loans on looser terms that have driven costs to the moon.

Undergraduate tuition is $34,935, and room and board costs $12,160. In 2013-14, 99 percent of undergraduates were awarded aid (a mix of grants/scholarships, loans and work-study) that averaged $18,914.

The full 4-year cost here is $200,000! Even with “financial aid” the cost is still over $100,000 for four years, and what’s worse is that in all probability half or more of that “aid” is loans, which means the graduate comes out of this school having sunk more than $100,000 into their so-called “education” while carrying back $50,000 more in debt!

This is utterly insane and indefensible. It was indefensible a decade ago and it is today.

Any school peddling such a system of so-called “education” is selling something has negative real value ex-costs, and they know it.

If you’re a parent and assist, recommend or even sit silently while your kid applies to and goes to such a place you are either an idiot or worse, you are actively conspiring in destroying your now-grown child’s economic future.

In short, you, along with the faculty and staff of any such institution, are monsters.

Way back when, my undergrad tuition was $185 per quarter (state school), with room and board another $330 per quarter. Worked 3 different jobs, fraternity waiter, campus food service, and grocery store, and graduated plus dollars. MBA scored via tuition reimbursement..cost of books only. (University of Chicago). All sounds like a great foundation, but life choices and economic conditions left a void with reality. Need a mulligan.

This college scam, first to offer “loans” to sub-subprime “students” and now for free is just the same recycled jobs for young people programs instituted by most other socialist economies when the actual productive jobs disappeared. Look to Russia where there are masters degree economists selling trinkets at a corner store. Jobs programs like all other federal programs, non-productive busywork leading nowhere.

Collapse can either appear slowly as decay or rapidly as a crash. Just because it isn’t currently a climacteric doesn’t indicate there isn’t collapse ongoing. Adjusting to the process of collapse is a personal decision when one decides that life would be better with the adjustment. For some, limiting the amount of predation on one’s personal lifestyle is, in itself, satisfying.

Admin, suddenly in my area more empty retail popping up. What are you seeing? This area is relatively well off. Spooky.

IT WAS WRITTEN IN THE BIBLE ALONG TIME AGO AMERICA IS BABYLON THE GREAT AND THE SYSTEM WILL CRASH IN ONE HOUR!!!HERE IS 99 REASONS !!!DOES THIS SOUND LIKE AMERICA?1. Babylon would be an END TIME GREAT NATION (Rev 17,18; Isa 13:6).

2. Babylon would have a huge seaport city within its borders (Rev 18:17).

3. The Great City Babylon is the home of a world government attempt (Rev 17:18).

4. The Great City Babylon would be the economic nerve center of the world (Rev 18:3).

5. Babylon would be the center of a one world Luciferian religious movement (Jer 51:44).

6. Babylon would be the center for the move to a global economic order (Rev 13:16).

BABYLON THE NATION

1. Babylon would be the youngest and greatest of the end time nations (Jer 50:12).

2. Babylon would the QUEEN AMONG THE NATIONS (Isa 47:5,7; Rev 18:7).

3. Babylon would be the most powerful nation in the world (Isa 47, Jer 50, 51, Rev 18).

4. Babylon would be the HAMMER OF THE WHOLE EARTH (Jer 50:23; Rev 18:23).

5. Babylon is called a lady, and has the symbol of the Lady (Isa 47:7-9).

6. Babylon would be the praise of the WHOLE EARTH (Jer 51:41).

7. Babylon is center of world trade (Jer 51:44; Rev 17:18; 18:19).

8. Babylon would grow to be the richest nation in the world (Rev 18:3, 7, 19, 23).

9. All nations that traded with Babylon would grow rich (Rev 18:3).

10. The merchants of Babylon were the GREAT MEN OF THE EARTH (Rev 18:23).

11. Babylon is a huge nation, with lands, cities, and great wealth (implied throughout).

12. Babylon is nation “peeled”, or timbered, a land of open fields (Isa 18:2).

13. Babylon is land quartered by mighty rivers (Isa 18:2).

14. Babylon is a land that is measured out, and populated throughout (Isa 18:2).

15. Babylon destroys her own land, with pollution and waste (Isa 14:20, 18:2, 7).

16. Babylon is a land rich in mineral wealth (Jer 51:13).

17. Babylon is a the leading agricultural nation of the world (Jer 50, 51; Rev 18).

18. Babylon is the leading exporting nation in the world (Jer 51:13; Rev 18).

19. Babylon is the leading importing nation of the entire world.(Jer 50, 51; Rev 18).

20. Babylon is a nation filled with warehouses and granaries (Jer 50:26).

21. Babylon is the leading INDUSTRIAL NATION OF THE WORLD (Isa 13, 47, Jer 50, 51; Rev 18).

22. Babylon is noted for her horses (Jer 50:37).

23. Babylon is noted for her cattle, sheep and other livestock (Jer 50:26, 27; Rev 18:13).

24. Babylon is noted for her fine flour and mill operations (Rev 18:13).

25. Babylon is a nation of farmers and harvests huge crops (Jer 50:16, 26, 27).

26. Babylon is a huge exporter of MUSIC (Rev 18:22).

27. Babylon’s musicians are known around the world (Rev 18:22)

28. Babylon has a huge aviation program (Isa 14:13-14; Jer 51:53; Hab 1:6-10).

29. Babylon’s skies are filled with the whisper of aircraft wings (Isa 18:1; Jer 51:53).

30. Babylon has a huge space industry, has “mounted up to the heavens” (Jer 51:53).

31. Babylon fortifies her skies with a huge military aviation program (Jer 51:53).

32. Babylon is portrayed as a leading in high tech weapons and abilities (Jer 51:53; Hab 1:6-10; implied throughout).

33. Babylon is a nation filled with warm water seaports (Rev 18:17-19).

34. Babylon is a coastal nation and sits upon MANY WATERS (Jer 51:13).

35. Babylon trades with all who have ships in the sea year round (Rev 18:17-18).

36. Babylon is nation filled with a “mingled” people (Jer 50:37).

37. Babylon is a SINGULAR NATION founded upon OUT OF MANY, ONE (Isa 13, 47, Jer 50, 51, Hab 1).

38. Babylon is a REPUBLIC or a DEMOCRACY, it is ruled by many counsels (Isa 47:13).

39. Babylon’s governmental system breaks down (Isa 47:13).

40. Babylon is bogged down with deliberations and cannot govern properly (Isa 47:13).

41. Babylon’s leaders use astrology, seers and mystics for guidance (Isa 47:13; Rev 18:2).

42. Babylon labored in the occult from her very inception (Isa 47:12).

43. Babylon falls to the occult just before her end by nuclear fire (Rev 18:2)

44. Babylon was born as a CHRISTIAN NATION (Jer 50:12).

45. Babylon turns upon its heritage and destroys it all in the end (Jer 50:11).

46. Babylon’s Christian leaders lead their flock astray in prophecy and salvation (Jer 50:6; implied Rev 18:2).

47. Babylon’s Christian leaders are “strangers” in the Lord Houses of Worship (Jer 51:51).

48. The people of Babylon are deep into astrology and spiritism (Isa 47:12; Rev 18:2).

49. Babylon becomes the home of all antichrist religions in the world (Rev 18:2).

50. Babylon is a nation of religious confusion (Isa 47:12-13).

51. Babylon turns upon its own people and imprisons and slays them by millions (Jer 50:7,33; 51:35; 39; Dan 7:25; Rev 13:7; 17:6; 18:24).

52. Babylon sets of detention centers for Jews and Christians and rounds them up for extermination (Jer 50:7, 33; 51:35, 49; Rev 17:6; 18:24).

53. Babylon has a mother nation that remains in existence from her birth to death (Jer 50: 12).

54. The mother of Babylon has the symbol of the LION (Dan7:4; Eze 38:13; Jer 51:38; Psalms 17:12).

55. The mother of Babylon will rule over her daughter her entire life (Dan 7:4; Jer 50:12).

56. The mother of Babylon will be a state of major decline as the end nears (Jer 50:12).

57. Babylon is considered to be a lion’s whelp (Eze 38:13; Jer 51:38).

58. Babylon will have the symbol of the EAGLE and builds her nest in the stars (Dan 7:4 EAGLE WINGS; Isa 14:13-14; Jer 51:53).

59. Babylon turns totally antichrist and is the leading antichrist power at the end (Rev 18:2; Isa 14:4-6).

60. THE KING OF BABYLON is called LUCIFER, the ANTICHRIST (Isa 14:4-6).

61. The King of Babylon will rule from THE GREAT CITY BABYLON (Isa 14:4-6; Rev 17: 18).

62. A world government entity will rise up to rule the world from BABYLON THE CITY (Isa 14; Hab 2, Rev 13, 17, 18).

63. This world entity will be a diverse entity, different than all other ruling bodies of the world (Dan 7:7, 23).

64. This entity will be a TREATY POWER ENTITY (Dan 7:7, 23 DIVERSE).

65. This entity will rise up and use the military power of Babylon the nation to RULE THE WORLD (Isa 14:4-6; Hab 1 & 2, Rev 13, 17).

66. Babylon is a huge producer and exporter of automobiles (Jer 50:37; Rev 18:13).

67. Babylon is a nation of CRAFTSMEN, experts in their trade (Jer 50, 51, Rev 18:22).

68. Babylon is noted for her jewelry of gold and silver (Rev 18:22).

69. Babylon is a huge importer and exporter of spices (Rev 18:13).

70. Babylon is a huge exporter of fine marble products (Rev 18:22).

71. Babylon is noted for her iron and steel production (Rev 18:12).

72. Babylon has huge corporations that have bases around the world (Rev 18:23, implied throughout)

73. Babylon is a nation of higher education and learning (Isa 47:10, implied throughout).

74. Babylon is a nation with a GREAT VOICE in world affairs (Jer 51:55)

75. Babylon is a VIRGIN NATION, untouched by major war (Isa 47:1).

76. Babylon has a vast military machine (Jer 50:36; 51:30; Hab 1 & 2, Rev 13:4).

77. Babylon will be instrumental in the setting up of Israel in the Middle East, and is the home of God’s people (Jer 50:47; 51:45).

78. Babylon will have a major enemy to her north (Jer 50:3, 9, 41).

79. Babylon’s enemy will lie on the opposite side of the world, over the poles (Isa 13:5)

80. The enemy of Babylon will be a FEDERAL OF NATIONS (Jer 50:9).

81. The enemy of Babylon will be largely Moslem in make-up (Jer 50:17; Rev 17:16; Psalms 83:5-12).

82. The enemy of Babylon will have nuclear missiles capable of reaching Babylon (Jer 50:9, 14,; Rev 18:8, 18).

83. The enemy of Babylon will be noted for her cruelty (Isa 13, 14, Jer 50, 51, Rev 17, 18).

84. The enemy of Babylon will also have a huge aviation military machine (Jer 50:9, 14, Rev 18:8, 18 implied throughout).

85. The enemy of Babylon will come into Babylon unnoticed (Isa 47:11, Jer 50:24; 51:2, 14).

86. Babylon will be filled with her enemies brought in under the guise of peace (Dan 11:21).

87. Babylon will have all of her borders cut off, and there will be no way of

escape (Jer 50:28; 51:32).

88. Babylon will be destroyed by nuclear fire (Implied throughout)

89. Babylon is land vast land with huge cities, towns and villages throughout (Implied throughout).

90. Babylon will have been a huge missionary nation for Jesus Christ (Jer 50:11; 51:7).

91. Babylon would be a home to multitudes of Jews who leave (Jer 50:4-6, 8; 51:6, 45)

92. The people of Babylon would not know their true identity (Jer 50:6, implied throughout).

93. The people of Babylon would think they are God’s elect and eternal (Isa 47:7-8, Rev 18:7).

94. The people of Babylon would enjoy the highest standard of living in the world (Rev 18:7).

95. The people of Babylon would grow mad upon their idols (Jer 50:2, 38; Hab 2:18).

96. The people of Babylon would go into deep sins of all kinds (Rev 18:5).

97. The nation Babylon dwells carelessly before the Lord (Isa 47:8).

98. Babylon becomes proud, haughty, and does not consider her end (Isa 47:7-8).

99. Babylon deals in the occult, in sorceries and drugs (Isa 47:9, 12; Rev 18:23)

These are but a few of the many parameters listed to help us identify this last great nation that the Lord calls BABYLON THE GREAT. America does now, or is in the process of fulfilling each and every one of them. No other nation upon the face of the earth can fulfill these parameters. AMERICA IS BABYLON THE GREAT. There would likewise be a series of SIGNS that would would begin to emerge that would give BIRTH TO, and WATCH THE RISE OF, as well as THE FALL OF AMERICA-BABYLON.

HERE IS HOW THE STOCKMARKET CRASHES!!!READ IT!! 1After these things I saw another angel coming down from heaven, having great authority, and the earth was illumined with his glory. 2And he cried out with a mighty voice, saying, “Fallen, fallen is Babylon the great! She has become a dwelling place of demons and a prison of every unclean spirit, and a prison of every unclean and hateful bird. 3“For all the nations have drunk of the wine of the passion of her immorality, and the kings of the earth have committed acts of immorality with her, and the merchants of the earth have become rich by the wealth of her sensuality.”

4I heard another voice from heaven, saying, “Come out of her, my people, so that you will not participate in her sins and receive of her plagues; 5for her sins have piled up as high as heaven, and God has remembered her iniquities. 6“Pay her back even as she has paid, and give back to her double according to her deeds; in the cup which she has mixed, mix twice as much for her. 7“To the degree that she glorified herself and lived sensuously, to the same degree give her torment and mourning; for she says in her heart, ‘I SIT as A QUEEN AND I AM NOT A WIDOW, and will never see mourning.’ 8“For this reason in one day her plagues will come, pestilence and mourning and famine, and she will be burned up with fire; for the Lord God who judges her is strong.

Lament for Babylon

9“And the kings of the earth, who committed acts of immorality and lived sensuously with her, will weep and lament over her when they see the smoke of her burning, 10standing at a distance because of the fear of her torment, saying, ‘Woe, woe, the great city, Babylon, the strong city! For in one hour your judgment has come.’

11“And the merchants of the earth weep and mourn over her, because no one buys their cargoes any more— 12cargoes of gold and silver and precious stones and pearls and fine linen and purple and silk and scarlet, and every kind of citron wood and every article of ivory and every article made from very costly wood and bronze and iron and marble, 13and cinnamon and spice and incense and perfume and frankincense and wine and olive oil and fine flour and wheat and cattle and sheep, and cargoes of horses and chariots and slaves and human lives. 14“The fruit you long for has gone from you, and all things that were luxurious and splendid have passed away from you and men will no longer find them. 15“The merchants of these things, who became rich from her, will stand at a distance because of the fear of her torment, weeping and mourning, 16saying, ‘Woe, woe, the great city, she who was clothed in fine linen and purple and scarlet, and adorned with gold and precious stones and pearls; 17for in one hour such great wealth has been laid waste!’ And every shipmaster and every passenger and sailor, and as many as make their living by the sea, stood at a distance, 18and were crying out as they saw the smoke of her burning, saying, ‘What city is like the great city?’ 19“And they threw dust on their heads and were crying out, weeping and mourning, saying, ‘Woe, woe, the great city, in which all who had ships at sea became rich by her wealth, for in one hour she has been laid waste!’ 20“Rejoice over her, O heaven, and you saints and apostles and prophets, because God has pronounced judgment for you against her.”

21Then a strong angel took up a stone like a great millstone and threw it into the sea, saying, “So will Babylon, the great city, be thrown down with violence, and will not be found any longer. 22“And the sound of harpists and musicians and flute-players and trumpeters will not be heard in you any longer; and no craftsman of any craft will be found in you any longer; and the sound of a mill will not be heard in you any longer; 23and the light of a lamp will not shine in you any longer; and the voice of the bridegroom and bride will not be heard in you any longer; for your merchants were the great men of the earth, because all the nations were deceived by your sorcery. 24“And in her was found the blood of prophets and of saints and of all who have been slain on the earth.”