Gail wrote this almost four weeks ago when oil was still $80 per barrel. Today it is $66 per barrel. The unintended consequences of this crash have yet to be realized. Enjoy the lower gasoline prices, because the other consequences may not be so pleasant.

Guest Post by Gail Tverberg

The world is in a dangerous place now. A large share of oil sellers need the revenue from oil sales. They have to continue producing, regardless of how low oil prices go unless they are stopped by bankruptcy, revolution, or something else that gives them a very clear signal to stop. Producers of oil from US shale are in this category, as are most oil exporters, including many of the OPEC countries and Russia.

Some large oil companies, such as Shell and ExxonMobil, decided even before the recent drop in prices that they couldn’t make money by developing available producible resources at then-available prices, likely around $100 barrel. See my post, Beginning of the End? Oil Companies Cut Back on Spending. These large companies are in the process of trying to sell off acreage, if they can find someone to buy it. Their actions will eventually lead to a drop in oil production, but not very quickly–maybe in a couple of years.

So there is a definite time lag in slowing production–even with very low prices. In fact, if US shale production keeps rising, and Libya and Iraq keep work at getting oil production on line, we may even see an increase in world oil production, at a time when world oil production needs to decline.

A Decrease in Oil Prices May Not Fix Oil Demand

At the same time, demand doesn’t pick up quickly as prices drop. We are dealing with a world that has a huge amount of debt. China in particular has been on a debt binge that cannot continue at the same pace. A reduction in China’s debt, or even slower growth in its debt, reduces growth in the demand for oil, and thus its price. The same situation holds for other countries that are now saturated with debt, and trying to come closer to balancing their budgets.

Furthermore, the Federal Reserve’s discontinuation of quantitative easing has cut off a major flow of funds to emerging markets. Because of this change, emerging market demand for oil has dropped. This has happened partly because of the lower investment funds available, and partly because the value of emerging market currencies relative to the dollar has fallen. Again, a decrease in oil price is not likely to fix this problem to a significant extent.

Europe and Japan are having difficulty being competitive in today’s world. A drop in oil prices will help a bit, but their problems will mostly remain because to a significant extent they relate to high wages, taxes, and electricity prices compared to other producers. The reduction in oil prices will not fix these issues, unless it leads to lower wages (ouch). The reduction in oil prices is instead likely to lead to a different problem–deflation–that is hard to deal with. Deflation may indirectly lead to debt defaults and a further drop in oil demand and oil prices.

Thus, oil prices are likely to continue their slide for some time, until real damage is done, perhaps to several economies simultaneously.

The United States’ Role in the Oil Over-Production / Under-Demand Clash

The United States is the country with the single largest increase in oil production in the past year. This growth in oil production seems not to have stopped, in recent weeks.

At the same time, the US’ own consumption of oil has not increased (Figure 2).

The result is a drop in needed imports. A number of oil exporters have been hit by the US drop in imports. Nigeria extracts a very light oil that competes for refinery space with oil from shale formations. Our imports of Nigerian oil have been reduced to zero (Figure 3). (The amounts I am showing on this and several other charts are “net imports.” These reflect transactions in both directions. Often the US imports crude oil and exports oil products, sometimes to the same country. In such a case, we are selling refinery services.)

Our imports of oil from Mexico are way down as well (Figure 4), in part because their oil production has been falling.

It is only in the past few months that US imports from Saudi Arabia have started to be significantly affected (Figure 5).

Saudi Arabia, like other oil exporters, depends on the sale of oil revenue to provide tax revenue for its budget. While it has a reserve fund for rainy days, over the long term it, too, depends on revenue from oil exports. If Saudi Arabia’s exports to the United States decrease, Saudi Arabia needs to find someone else to sell these would-be exports to, or revenues to fund its budget will drop.

Alternatively, it can reduce the price it charges to US refineries, to influence purchasing decisions–something it has just done. Lowering its price to US refineries tends to push the world price for oil down.

Of course, the US also talks about allowing an increasing amount of crude oil exports, as its oil from shale formations rises. This increase would make the surplus of oil on the market worse, and world prices lower, if oil demand does not pick up.

Depending on Saudi Arabia and OPEC

In the West, we have been led to believe that OPEC in general and Saudi Arabia in particular exert great control over oil prices. We have been told that several OPEC countries have spare capacity. Several of the Middle Eastern countries claim that they have very high reserves, and we have been led to believe that they can ramp up their production if they invest more money to do so. We have also been told that these countries will reduce oil production, if needed, to hold up oil prices.

A very significant part of what we have been led to believe is exaggerated. Saudi Arabia’s oil exports were much higher back in the late 1970s than they are now (Figure 6). When they cut oil production and exports in the 1980s, they likely did have spare capacity.

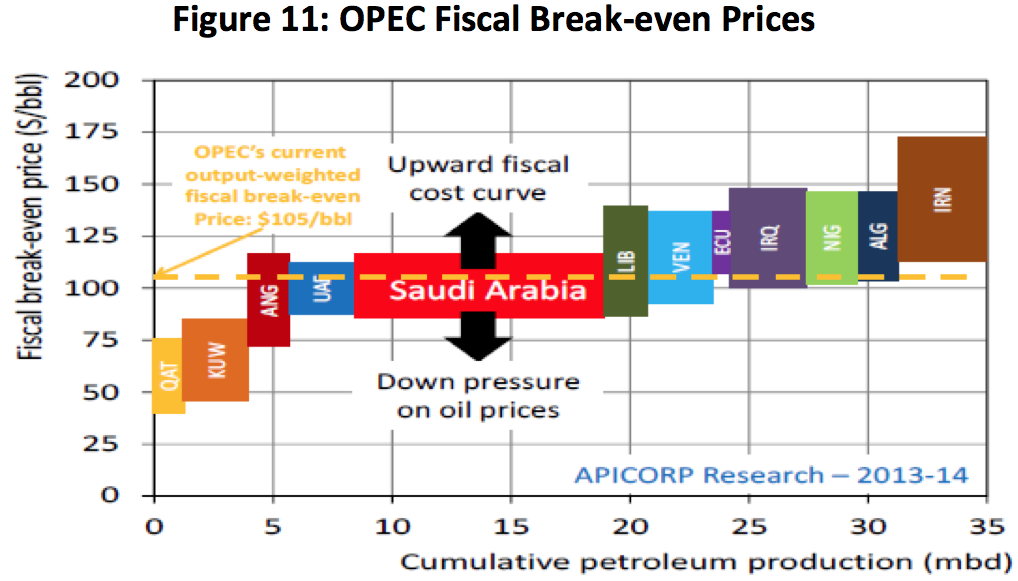

But where we are now, the situation has changed greatly. The population of the Middle Eastern oil producers has risen. So has their own use of the oil they extract. Their budgets have risen, and the countries need increasing revenue from oil taxes to meet their budgets. Some countries, including Venezuela, Nigeria, and Iran, require oil prices well over $100 per barrel to support their budgets (Figure 7).

If oil prices are too low, subsidies for food and oil will need to be cut, as will spending on programs to provide jobs and new infrastructure such as desalination plants. If the cuts are too great, there is the possibility of revolution and rapid decline of oil production. Virtually none of the OPEC countries can get along with oil prices in the $80 per barrel range (Figure 7).

Most of OPEC’s actions in recent years have looked like actions a person would expect if OPEC countries were not all that different from other oil producers–their oil supplies were subject to limits and they tended to act in their own self interest. When oil prices were rising rapidly in the 2007-2008 period, they ramped up production, but not by very much and not very quickly (Figure 8). When oil prices dropped, they dropped their production back to where it had been, before the big ramp up in prices.

Another situation occurred when Libya’s production declined in 2011. Saudi Arabia said it would increase its own supply to offset, but it could only produce extra very heavy crude when light oil was what was needed. In fact, even the increase in heavy oil is somewhat in doubt.

Furthermore, the dynamics of OPEC have been changed considerably in the last few years. Part of the problem relates to fact that both oil prices and the quantity of oil exports have been approximately flat in the period between 2011 and mid-2014. In such a situation, revenue from oil exports tends to be flat. OPEC members have found this to be a problem because their populations continued to grow and their need for water and imported food has continued to rise. These countries need ever-more tax revenue, but oil revenue is not providing it. At a minimum, OPEC countries have a strong “need” to maintain their current level of oil exports.

The other part of changing OPEC dynamics relates to increased oil production volatility. The bombing of Libya and sanctions against Iran have both produced unstable situations. Oil exports from both of these countries are lower than in the past, but can suddenly rise as their problems are “fixed,” adding to downward price pressures.

Another issue is the significant attempt to raise Iraq’s oil production in recent years. If Iraq’s oil production (plus US shale production) is too much to satisfy world demand for oil, should the rest of OPEC be the ones to try to “fix” the problem?

Figure 9 seems to indicate that US imports from Iraq have increased in recent months. Of course, if we import more from Iraq, we will likely need to cut back on imports elsewhere. This doesn’t create good feelings among OPEC exporters.

Shouldn’t the United States Take Some Responsibility for Fixing the Problem?

One might ask whether the United States should be cutting back in its oil production, in response to low prices. Of course, as indicated above, US oil majors (like Shell, Chevron, and Exxon) are cutting back on investment in new fields, and this is eventually likely to lead to lower production. The question is whether this will be a sufficient change, quickly enough.

It is less likely that shale drillers will intentionally cut back quickly. The shale drillers have taken on leases on huge acreage and are reluctant to step back now. For one thing, part of their costs has already been paid, reducing their costs going forward on acreage already under development. They also have debt that needs to be repaid and many contractual arrangements with respect to drilling rigs, pipelines, and other services. Some may have futures contracts in place that will soften the impact of the oil price drop, at least for a while. Because of all of these factors, there is a tendency to continue business as usual, for as long as possible.

Whether or not shale drillers intentionally plan to cut back on oil production, some of them may be forced to, whether or not they believe that the production is likely to be profitable over the long run. The problem is likely to be falling cash flow because of lower oil prices, if the price drop is not mitigated by futures contracts. Because of this, some companies may be forced to cut back on drilling quite soon. Another alternative might be to ramp up borrowing, but lenders may not be very happy with such an arrangement.

We notice that some companies are already in very cash flow negative situations–in other words, in situations where they need to keep adding more debt. For example, Capital Resources, the largest operator in the Bakken, shows rapidly growing outstanding debt through 6/30/2014, without seeming to take on significant new acreage (Figure 10).

When companies are already in such cash flow negative situation, there may be more problems than otherwise.

If Lower Oil Prices “Hang Around” for Months to Years, What Could this Mean?

We are in uncharted territory, in such a situation.

One of the big issues is potential deflation. The issue seems to be not only lower oil prices, but lower prices for many other commodities, as well. The concern is that wages will drop, as will government receipts. Lower wages already seem to be happening in Spain. Unless governments figure out a way to “fix” the situation, this situation will make debt repayment very difficult. Lower debt will tend to reinforce the low prices of oil and other commodities.

If low prices become the norm for many kinds of commodities, we can expect major cutbacks in production of these commodities. This would be the situation of the 1930s all over again. Ben Bernanke has said he would send helicopters of money to prevent such a situation. The question is whether this can really be arranged, given that the United States (and several other countries) have already been “printing money” since 2008. At some point, it would seem like the arsenals of central banks will get used up.

If there is a cut back in debt and cutback in production of commodities, many goods we have come to expect in the market place will disappear, as will many jobs. There are likely to be breaks in supply chains, leading to more cutbacks in production.

With all of the debt problems, there is a question of how well international trade will hold up. Will would-be explorers trust buyers who have recently defaulted on their debt, and don’t look likely to be able to earn enough to pay for the goods that they currently are ordering?

The discussion has been mostly with respect to oil, but liquefied natural gas (LNG) is likely to be affected by low prices as well. Reuters is reporting that likelihood of US exports of LNG to Asia is down, for a number of reasons, including the discovery that costs would be higher than originally expected and the regulatory process less smooth. Another reason LNG exports are likely to be low is the fact that Asian prices dropped from a high of $20.50/mmBtu in February to a low of $10.60/mmBtu in August. Without sustained high LNG prices, it is hard to support the huge infrastructure investment needed for LNG exports.

Can Oil Prices Bounce Back?

If we could somehow fix the world’s debt problems, a rise in the price of oil would seem to be much more likely than it looks right now. As long as the drop in demand is related to declining debt, and the potential feedbacks seem to be in the direction of deflation and the possibility of making defaults ever more likely, we have a problem. The only direction for oil prices to go would seem to be downward.

I know that we have very creative central banks. But the issue at hand is really diminishing returns. Prior to diminishing returns becoming a problem, it was possible to extract and refine oil cheaply. With cheap oil, it was possible to create an economy with low-priced oil, inexpensive infrastructure built with that low-priced oil, and factories built with low-priced oil. Workers seemed to be very productive in such a setting, in part because low-priced oil allowed increased mechanization of production and allowed cheap transport of goods.

Once diminishing returns set in, oil became increasingly expensive to extract, because we needed to use more resources to obtain oil that was very deep, or in shale formations, or that required desalination plants to support the population. Once we needed to allocate resources for these endeavors, fewer resources were available for more general uses. With fewer resources for general activities, economic growth has become inhibited. This has tended to lead to fewer jobs, especially good-paying jobs. It also makes debt harder to repay. History shows that many economies have collapsed because of diminishing returns.

Most people assume that of course, oil prices will rise. That is what they learned from supply and demand discussions in Economics 101. I think that what we learned in Econ 101 is wrong because the supply and demand model most economists use ignores important feedback loops. (See my post Why Standard Economic Models Don’t Work–Our Economy is a Network.)

We often hear that if there is not enough oil at a given price, the situation will lead to substitution or to demand destruction. Because of the networked nature of the economy, this demand destruction comes about in a different way than most economists expect–it comes from fewer people having jobs with good wages. With lower wages, it also comes from less debt being available. We end up with a disparity between what consumers can afford to pay for oil, and the amount that it costs to extract the oil. This is the problem we are facing today, and it is a very difficult issue.

We have been hearing for so long that the problem of “peak oil” will be inadequate supply and high prices that we cannot adjust our thinking to the real situation. In fact, the two major problems of oil limits are likely to be shrinking debt and shrinking wages. The reason that oil supply will drop is likely to be because customers cannot afford to pay for it; they don’t have jobs that pay well and they can’t get loans.

In some ways, the oil prices situation reminds me of driving down a road where we have been warned to look carefully toward the left for potential problems. In fact, the potential problem is in precisely in the opposite direction–to the right. The problem gets overlooked for a very long time, because most of us have been looking out the wrong window.

For more on this subject, read my last two posts:

WSJ Gets it Wrong on “Why Peak Oil Predictions Haven’t Come True”

Eight Pieces of Our Oil Price Predicament

Oil so cheap , no one can afford it to pump it…oh,the irony.

Cheap Oil A Boon For The Economy? Think Again

Submitted by Raul Ilargi Meijer via The Automatic Earth,

I thought it might be a nice idea to question a certain someone’s theories using their own words, while at the same time showing everybody what the dangers are from falling oil prices. There are many ‘experts and ‘analysts’ out there claiming that economies will experience a stimulus from the low prices, something I’ve already talked about over the past few days in The Price Of Oil Exposes The True State Of The Economy and OPEC Presents: QE4 and Deflation. And I’ve also already said that I don’t think that is true, and I don’t see this ending well.

Today, our old friend Ambrose Evans-Pritchard starts out euphoric, only to cast doubt on his self-chosen headline. He’d have done better to focus on that doubt, in my opinion. And I have his own words from earlier in the year to support that opinion. Ambrose is bad at opinions, but great at collecting data; his personal views are his achilles heel as a journalist. That’s maybe why he fell into the propaganda trap of picking this headline; after all, if you write for the Daily Telegraph you’re supposed to write positive things about the economy.

Oil Drop Is Big Boon For Global Stock Markets, If It Lasts

Tumbling oil prices are a bonanza for global stock markets, provided the chief cause is a surge in crude supply rather than a collapse in economic demand

Roughly one third of the current oil slump is a shortfall in expected demand, caused by China’s industrial slowdown and Europe’s austerity trap. The other two thirds are the result of a sudden supply glut, which Saudi Arabia and the Gulf states have so far chosen not to offset by cutting output. This episode looks relatively benign. Nick Kounis from ABN Amro says it will add $550 billion of stimulus to world markets. “That is fantastic news for the global economy,” he said. But it comes at a time when stocks are already high if measured by indicators of underlying value. The Schiller 10-year price earnings ratio is at nose-bleed levels above 27.

Tobin’s Q, a gauge based on replacement costs, is stretched to near historic highs. Andrew Lapthorne from SocGen says the MSCI world index of stocks has risen 38% over the last three years but reported profits have risen just 3%. “Valuations, as measured by median price to cash flow ratios, are near historical highs. As US QE has come to an end, depriving the world of $1 trillion printed dollars a year, there are plenty of reasons to be nervous,” he said.

Ambrose’s gauge of share values is dead on, and far more important than he seems to realize. He knows full well there are tons of reasons to doubt his own headline. But he still leaves out many of those reasons in that article today. So let’s move back in time to look at what he wrote this summer, before the drop in oil prices.

Here are a few lines from Ambrose on July 9 2014:

Fossil Industry Is The Subprime Danger Of This Cycle

The epicentre of irrational behaviour across global markets has moved to the fossil fuel complex of oil, gas and coal. This is where investors have been throwing the most good money after bad. [..] oil and gas investment in the US has soared to $200 billion a year. It has reached 20% of total US private fixed investment, the same share as home building.

This has never happened before in US history, even during the Second World War when oil production was a strategic imperative. The International Energy Agency (IEA) says global investment in fossil fuel supply doubled in real terms to $900 billion from 2000 to 2008 as the boom gathered pace. It has since stabilised at a very high plateau, near $950 billion last year. The cumulative blitz on exploration and production over the past six years has been $5.4 trillion [..]

… upstream costs in the oil industry have risen 300% since 2000 but output is up just 14% [..] The damage has been masked so far as big oil companies draw down on their cheap legacy reserves.

… companies are committing $1.1 trillion over the next decade to projects that require prices above $95 to break even. The Canadian tar sands mostly break even at $80-$100. Some of the Arctic and deepwater projects need $120. Several need $150. Petrobras, Statoil, Total, BP, BG, Exxon, Shell, Chevron and Repsol are together gambling $340 billion in these hostile seas.

… the biggest European oil groups (BP, Shell, Total, Statoil and Eni) spent $161 billion on operations and dividends last year, but generated $121 billion in cash flow. They face a $40 billion deficit even though Brent crude prices were buoyant near $100 ..

… the sheer scale of “stranded assets” and potential write-offs in the fossil industry raises eyebrows. IHS Global Insight said the average return on oil and gas exploration in North America has fallen to 8.6%, lower than in 2001 when oil was trading at $27 a barrel.

What happens if oil falls back towards $80 as Libya ends force majeure at its oil hubs and Iran rejoins the world economy?

A large chunk of US investment is going into shale gas ventures that are either underwater or barely breaking even, victims of their own success in creating a supply glut. One chief executive acidly told the TPH Global Shale conference that the only time his shale company ever had cash-flow above zero was the day he sold it – to a gullible foreigner.

… the low-hanging fruit has been picked and the costs are ratcheting up. Three Forks McKenzie in Montana has a break-even price of $91. [..]

“Under a global climate deal consistent with a two degrees centigrade world, we estimate that the fossil fuel industry would stand to lose $28 trillion of gross revenues over the next two decades , compared with business as usual,” said Mr Lewis. The oil industry alone would face stranded assets of $19 trillion, concentrated on deepwater fields, tar sands and shale.

By their actions, the oil companies implicitly dismiss the solemn climate pledges of world leaders as posturing, though shareholders are starting to ask why management is sinking so much their money into projects with such political risk.

Those numbers alone, combined with the knowledge that prices are off close to 40% by now, should be enough to give anyone the jitters, about the oil industry, and therefore about the global economy. Any industry that’s so deeply in debt cannot afford a 40% dip in revenue, not even for a short while. Dominoes must start tumbling in short order.

And of course saying ‘any industry so deeply in debt’ is already a bit misleading, because there is no industry like oil in the world (except maybe steel, and look how that’s doing), and it’s highly doubtful there’s another one with such debt levels. Oil stocks are down somewhat, but it’s hard to see how they could not fall a lot further. And as for the huge amounts invested in energy junk bonds, one can but shudder.

On August 11 2014, Ambrose had some more:

Oil And Gas Company Debt Soars To Danger Levels To Cover Cash Shortfall

The world’s leading oil and gas companies are taking on debt and selling assets on an unprecedented scale to cover a shortfall in cash, calling into question the long-term viability of large parts of the industry. The US Energy Information Administration (EIA) said a review of 127 companies across the globe found that they had increased net debt by $106 billion in the year to March, in order to cover the surging costs of machinery and exploration, while still paying generous dividends at the same time.

They also sold off a net $73 billion of assets. [..] The EIA said revenues from oil and gas sales have reached a plateau since 2011, stagnating at $568 billion over the last year as oil hovers near $100 a barrel. Yet costs have continued to rise relentlessly.

… the shortfall between cash earnings from operations and expenditure – mostly CAPEX and dividends – has widened from $18 billion in 2010 to $110 billion during the past three years. Companies appear to have been borrowing heavily both to keep dividends steady and to buy back their own shares, spending an average of $39 billion on repurchases since 2011.

… “continued declines in cash flow, particularly in the face of rising debt levels, could challenge future exploration and development”. [..] upstream costs of exploring and drilling have been surging, causing companies to raise long-term debt by 9% in 2012, and 11% last year. Upstream costs rose by 12% a year from 2000 to 2012 due to rising rig rates, deeper water depths, and the costs of seismic technology. This was disguised as China burst onto the world scene and powered crude prices to record highs.

Global output of conventional oil peaked in 2005 despite huge investment. [..] the productivity of new capital spending has fallen by a factor of five since 2000. “The vast majority of public oil and gas companies require oil prices of over $100 to achieve positive free cash flow under current capex and dividend programmes. Nearly half of the industry needs more than $120,” ..

Analysts are split over the giant Petrobras project off the coast of Brazil, described by Citigroup as the “single-most important source of new low-cost world oil supply.” The ultra-deepwater fields lie below layers of salt, making seismic imaging very hard. They will operate at extreme pressure at up to three thousand meters, 50% deeper than BP’s disaster in the Gulf of Mexico.

Petrobras is committed to spending $102 billion on development by 2018. It already has $112 billion of debt. The company said its break-even cost on pre-salt drilling so far is $41 to $57 a barrel. Critics say some of the fields may in reality prove to be nearer $130. Petrobras’s share price has fallen by two-thirds since 2010.

… global investment in fossil fuel supply rose from $400 billion to $900 billion during the boom from 2000 and 2008, doubling in real terms. It has since levelled off, reaching $950 billion last year. [..] Not a single large oil project has come on stream at a break-even cost below $80 a barrel for almost three years.

… companies are committing $1.1 trillion over the next decade to projects requiring prices above $95 to make money. Some of the Arctic and deepwater projects have a break-even cost near $120 . The IEA says companies have booked assets that can never be burned if there is a deal limit to C02 levels to 450 (PPM), a serious political risk for the industry. Estimates vary but Mr Lewis said this could reach $19 trillion for the oil nexus, and $28 trillion for all forms of fossil fuel.

For now the major oil companies are mostly pressing ahead with their plans. ExxonMobil began drilling in Russia’s Arctic ‘High North’ last week with its partner Rosneft, even though Rosneft is on the US sanctions list. “Exxon must be doing a lot of soul-searching as they get drawn deeper into this,” said one oil veteran with intimate experience of Russia. “We don’t think they ever make any money in the Arctic. It is just too expensive and too difficult.”

Plummeting oil prices not only mirror the state of the – real – economy, they will also drag the state of that economy down further. Much further. If only for no other reason than that today’s oil industry swims in debt, not reserves. Investment policies, both within the industry and on the outside where people buy oil company stocks and – junk – bonds, have been based on lies, false presumptions, hubris and oil prices over $100.

The oil industry is no longer what it once was, it’s not even a normal industry anymore. Oil companies sell assets and borrow heavily, then buy back their own stock and pay out big dividends. What kind of business model is that? Well, not the kind that can survive a 40% cut in revenue for long. The industry’s debt levels were, in Ambrose’s words, at a ‘danger level’ when oil was still at $110.

Is Big Oil still a going concern? You tell me. I don’t want to tell the whole story bite-sized on a platter, there’s more value in providing the numbers, this time from Ambrose but there are many other sources, and have you make up your own mind, do the math etc.

Ambrose’s exact numbers can and will be contested three ways to Sunday, but his numbers are not that far off, and if anything, he may still be sugarcoating. WTI closed at $66.15 on Friday, Brent is at $70.15. Given the above data, where would you think the industry is headed? What will happen to the trillions in debt the industry was already drowning in when oil was still above $100?

And how will this be a boon to the economy even if, as Ambrose puts it, the ”oil drop lasts”? Do you have any idea how much your pension fund is invested in oil? Your money market fund? Your government? I would almost say you don’t want to know.

There can be very little doubt that oil prices will at some point rise again from whatever bottom they will reach. Even if nobody knows what that bottom will be. At the same time, there can also be very little doubt that when that happens, the energy industry’s ‘financial landscape’ will look very different from today. And so will the – real – economy.

Cheap oil a boon for the economy? You might want to give that some thought.

The Imploding Energy Sector Is Responsible For A Third Of S&P 500 Capex

Submitted by Tyler Durden on 11/30/2014 17:28 -0500

We have previously discussed the implications that tumbling crude oil prices will have not only on some of the most levered companies with exposure to Brent prices, namely the vast majority of the US energy space with outstanding junk bonds which, as we explained before, should WTI drop to $60, it would “Trigger A Broader HY Market Default Cycle” (based on a Deutsche Bank analysis) leading to pain across the entire credit market (and in the process impairing the stock-buyback machinery which companies aggressively use to artificially boost their stock price), as well as on oil-exporting nations, whose economies are assured to grind to a halt leading to broad social unrest or worse, and lastly, on global asset liquidity, which is set to contract even more now that for the first time in over a decade, the net flow of Petrodollars will be an outflow (as explained in How The Petrodollar Quietly Died, And Nobody Noticed).

And while much has been said about the “benefits” the US economy is poised to reap as a result of the plunge in gas prices, which has been compared to a major tax cut (whatever happened to the core Keynesian tenet that “deflation” is the worst thing that can possibly happen) on the US consumer, almost nothing has been said about the adverse impact on US GDP as a result of tumbling fixed investment spending and CapEx.

The reason, clearly, is that the collapse in new investment will more than offset the boost from incremental household spending.

Here are the facts, per Deutsche Bank:

US private investment spending is usually ~15% of US GDP or $2.8trn now. This investment consists of $1.6trn spent annually on equipment and software, $700bn on non-residential construction and a bit over $500bn on residential. Equipment and software is 35% technology and communications, 25-30% is industrial equipment for energy, utilities and agriculture, 15% is transportation equipment, with remaining 20-25% related to other industries or intangibles. Non-residential construction is 20% oil and gas producing structures and 30% is energy related in total. We estimate global investment spending is 20% of S&P EPS or 12% from US. The Energy sector is responsible for a third of S&P 500 capex. 35% of S&P EPS from investment and commodity spend, 15-20% US

In short, while nobody knows just how many tens of billions in US economic “growth”, i.e., GDP, will be eliminated now that energy companies are not only not investing in growth spending or even maintenance, being forced to shut down unprofitable drilling operations and entering spending hibernation territory, the guaranteed outcome is that US GDP is set to slide as the CapEx cliff resulting from Brent prices dropping below the $75/bbl red line under which shale is broadly no longer profitable will offset any GDP benefit unleashed from the “supposed” increase in consumer spending (supposed because according to the latest NRF numbers, Thanksgiving spending was not only well below last year (with the average consumer spending $380.95 over Thanksgiving compared to $407.02 a year ago) but below even our worst case forecasts. So just where are all those external benefits to US retailers as a result of crashing gas prices?

Rhetorical questions aside, the real question is just how much will said GDP slide ultimately be? Sadly, this too will be one question the BEA will never answer, as instead the upcoming GDP plunge will be blamed once again on inclement weather as opposed to actually analyzing what is truly happening as America’s transformation to an oil-producing (and maybe exporting) powerhouse, is so rudely interrupted.

The only good news: the resulting surge in America’s trade deficit as the US is forced to import more crude in the coming months, will provide just the catalyst for the Fed to return to the game and resume monetizing the US budget deficit, which is poised to commence rising once again.

Scotiabank: – Based upon an analysis of more than 50 oil plays across Canada and the United States, we estimate that ‘mid-cycle breakeven costs’ in the North Dakota Bakken (1.05 mb/d) are roughly US$69 per barrel and in the Permian Basin in Texas (1.63 mb/d) about US$68. While some producers have hedged forward at higher prices, if WTI oil remains around US$70 for more than six months, it appears likely that drilling activity will slow in more marginal areas of these plays as 2015 unfolds. Funding for independent oil producers will also tighten. However, the ‘liquids-rich’ Eagle Ford (1.45 mb/d) will be little impacted, with breakeven costs averaging only US$50.

Bwahahahahahaha!

The countries getting screwed by this are ever so deserving of said screwing:

Venezuela _ bwahahaha! Fuckers deserve what they get..

Saudis – Bwahahaha!

Iran – Snort! Bwahaha!

This has made my day. So much for a unified OPEC. Fuck them and their motherfucking cartel.

Let them eat cake.

Oil futures extend their sell-off, as Nymex crude loses grip on $65

By Michael Kitchen

Published: Nov 30, 2014 6:50 p.m. ET

LOS ANGELES (MarketWatch) — U.S. crude-oil futures spiraled further down in electronic trade late Sunday, with the most-active January 2015 contract CLF5, -2.54% breaking below the $65-a-barrel handle to hit $64.90 as East Asian markets opened. The drop represented a 2% fall from the New York Mercantile Exchange settlement Friday, when the contract had plunged 10% after the Organization of the Petroleum Exporting Countries failed to agree to an output cut. A Dow Jones Newswires technical analysis put the next main support at $64.24, the “reaction low” of May 20, 2010. A breach below that level would set up possible downside at the psychological boundary of $60.00, the news agency said. Meanwhile, Nymex crude’s London-traded rival benchmark, Brent crude LCOF5, -2.34% lost 1.9% to $68.85 a barrel in electronic trade, extending its 3.4% retreat Friday.

Crude Carnage Goes Contagious As Brevan Howard Liquidates Underperforming Commodity Fund

Submitted by Tyler Durden on 11/30/2014 19:08 -0500

The entire commodity complex is seeing major contagion-like price declines in early trading. WTI Crude is back below $65 for the first time since May 2010 – now down 16% since the initial leaks of OPEC’s decision last Wednesday. Gold and Silver are getting whacked and copper has plunged below 300 – back at its lowest since June 2010. The news over the weekend that Brevan Howard is liquidating its $630 million commodity hedge fund following recent poor performance is also likely not helping as what looked like late-Friday margin call liquidations are extending notably this evening.

As The Wall Street Journal reports,

Brevan Howard Asset Management LLP plans to close its commodity hedge fund following recent poor performance, according to two people familiar with the matter.

The fund, managed by Stephane Nicolas, has $630 million in assets. It lost 4.2% last year and is down 4.3% this year to the end of October, according to performance data reviewed by The Wall Street Journal.

It is not clear what Mr. Nicolas’s role might be following the commodity fund’s closure, a person familiar with the matter said. Attempts to reach Mr. Nicolas were unsuccessful.

Brevan Howard is among Europe’s largest hedge fund managers with about $37 billion in assets.

Someday, Gail will be able to venture an opinion on a topic she knows little about without folks remembering her ridiculous peak oil call in 2008 call when helping to run the oil drum.

And if, while waiting for folks to forget her demonstrated ignorance of the market specifically and oil production in general, she LEARNS something to correct those errors, some of us will have an interest in her opinion.

But she demonstrates none of that required learning yet in her current postings, and continues to make the same mistakes she has in the past.

Johnny appears to be a pompous ass know it all.

Just my opinion.

I’m sure he has something worthwhile to offer other than telling us how others are wrong.

I’m already tired of his blatherings.

It’s too bad Johnny’s bullshit about Gale is false. Liquid oil production peaked in 2008. Facts are so inconvenient to pompous assholes who think they can bloviate without being proven wrong.

Admin sure knows how to increase commentators around here. His welcomes are always positive and encouraging.

John – anyone who puts his/her balls on the line by making forecasts will miss the mark very often indeed. Hell, I am still waiting for Admin’s forecast that OWS would be a defining moment in US history to come true. But here is the thing – do I remind him of it? Hell no. Not my style. The fact that he was a total dumbshit on that doesn’t mean I should remind him of it forever, now does it? And besides, he is right on many, many things. Please see his comments re retailers for some outstanding prognostications.

Just because a previous forecast/prediction did not come true does not mean that what is currently being said is not valid. What evidence do you have that her opinions are now currently invalid? You have pointed to no errors whatsoever.

You are indeed, as Admin has so rightly stated, a pompous ass.

Llpoh

OWS will rise again. Book it Dano.

John, like the Joker said, never rub another man’s rhubarb. Never rub admin’s the wrong way, you’ll get nutted in a heartbeat.

WTF?

“Nigeria extracts a very light oil that competes for refinery space with oil from shale formations.”

That fracked oil is pretty heavy. Refinery’s need to be more or less set up to deal with heavy oil to deal with what is coming out of the bakken.

What light oil that is getting produced, is trying very hard to get out as no refinery in the USA is set up to deal with it.

I wonder about long lasting effects from all of this. Oil should shoot up soon i imagine.

I wonder to what numbers. There sure is a lot of shit going on. I guess none of it will overload the system.

Well, it looks like oil prices are a symptom of demand rather then over supply.

If so, those businesses or countries that have a comparative advantage in oil production will survive. My guess is this isn’t some grand conspiracy to drive the weaker oil producers out of business but rather the way the cookie crumbles when a global recession ensues. (Stupid banks and financiers if they couldn’t understand this at the time of the loans)

As has been pointed out , if the said global economy has grown by 20 % since 2009 and oil production only rose 3% in that time , the question needs to be asked is how much of that global growth has been ginned up and phony.

My guess is that those things on the lower rungs of Maslows hierarchy of needs that require real energy have not grown that much. But while, the things government measures as economic activity that don’t require real energy have.

In other words, the government has been measuring things that aren’t really economic activity.

My guess is that the principle thing that the government has been measuring for quit sometime as economic activity and is not, is Health Care services.

IHealthcare services are really inflation not economic growth .

The country needs more Koch Brothers building factories and less home health aides if it wants a higher standard of living.