Guest Post by Doctor Housing Bubble

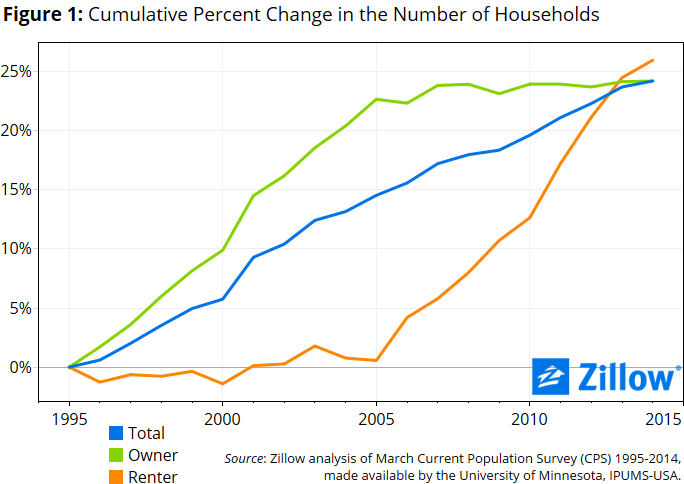

What a difference a decade can make. Over the last two decades the number of U.S. households has grown by 25 percent. But the growth has come in two distinctive waves. Between 1995 and 2005 nearly all of this growth came in the form of new homeowners. However, the subsequent decade saw something very different. Most of household growth between 2005 and 2015 has come in the form of renter households. It should come as no surprise that new home buying still remains weak. With this new trend unfolding, it shouldn’t come as a shock that multi-unit permits are surging as builders place their bets on rental Armageddon. While a few people can’t wait to dive into mega debt for a crap shack, others are simply renting either out of necessity or by choice. In fact, renting over the last decade has been the choice many have made (out of necessity or free will) contrary to the crap shack enthusiasts trying to talk up their poorly built piece of junk as some kind of diamond in the rough. Builders with deep pockets are betting on a continuation of the rental trend. It should also be no surprise that this decade saw a major surge of the “single family home” as rental unit.

Two decades with two different stories

We have witnessed continued household growth in the U.S. Household formation has increased by 25 percent over the last 20 years. However, each half of the last 20 years has seen growth come from two very distinct categories.

The homeownership boom followed by the renter boom:

The chart above is as clear as day. You have the last hurrah leading to peak homeownership followed by a massive shift to renting as millions upon millions of Americans lost their homes to foreclosure. You need to remember what this has done to consumer psychology. Never in our lifetime have we witnessed a countrywide housing bubble. Housing before this recent crash never suffered one year of negative price growth. Not one. So this put a major dent into the untouchable perception of housing as a sure bet. It also didn’t help that over 7 million Americans actually lost their home to foreclosure. We now have a nice group of revisionists talking about these people “strategically walking away” but in reality, this was a small subset. The majority lost their home because when the economy contracted, cut wages and lost jobs couldn’t cover the mortgage payment. Research has shown that people will prioritize debt payments in crisis and housing gets pushed up to the top of importance. So losing a home is a big deal and certainly most people lost it for this obvious reason. But you have to live somewhere. Where did these people go?

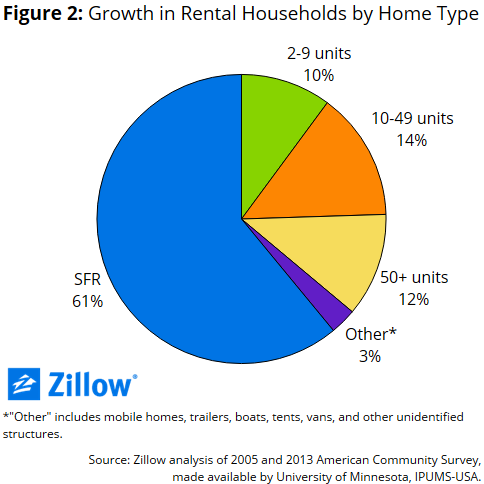

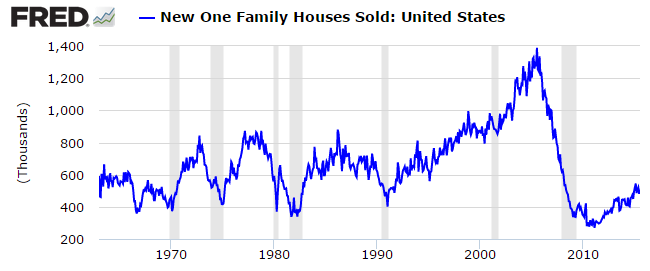

A large part of the single family home inventory got sucked up in the investor orgy to convert them into rentals. This took an already low supply of homes and made it lower. And builders simply did not build new homes in large quantities because new home sales continue to be pathetic:

Why not build new homes if supply is so low? The answer is clear and that is new potential households have weaker wages and new homes cost more. Why would builders construct an expensive product when the demand based on household income is for rentals? It is also the case that younger households watching mom and dad stressing their minds our to make the mortgage payment has left an indelible memory on their mind. Homeownership isn’t all that it is cracked up to be. Millennials certainly don’t have the taste for home buying like the Taco Tuesday baby boomer generation.

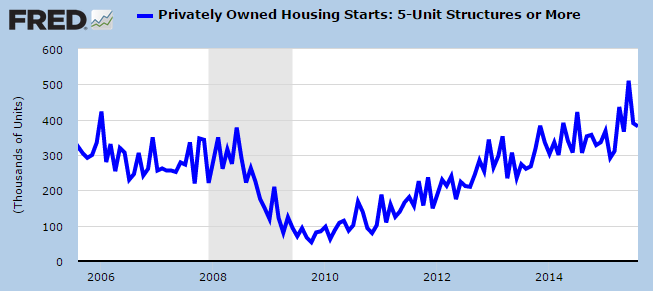

Which leads us to the bet home builders are making. Permits are surging for multi-unit housing (aka most likely rental housing):

You notice how the market didn’t react to the Fed? The Fed’s action merely speaks volumes in that they still don’t trust this “recovery” and household formation is telling us an even clearer picture. For all those that worship the Fed as their new religion your preacher just said “we can’t raise rates because the economy is still weak.” For the last year or so home prices rising has come at the hands of speculation and stock market run-off. The stock market had a tiny hiccup and we are already seeing the impact on housing. People simply can’t afford to buy even with the Fed holding rates near zero.

In my fairly prosperous community, two giant high-density apartment complexes are being built. They both will hold thousands of people and I understand one is low income housing. They are completely out of character with local ambience and I guess prove that we still have plenty of water around here.

The water comment because I live in So. California.

Since Neegrows don’t bathe, they can get by with less water.

The houses cost so much its insane. No wonder people rent. Everything has gone up in price except how much people make.

Many Americans no longer have the kind of jobs and stability that homeownership requires. The math doesn’t work. Assuming a modest $250,000 property with 20% down you need $50,000 in capital. In a zirped world that is not easy to accumulate. You need job stability, which is hard to get these days especially in two income households. If you have to sell it will cost you about 8% of the sale price or $20,000 in commissions and moving and presentation costs at a minimum. This would require property price appreciation of 2% for almost 4 years to get your capital out of the home without a loss assuming no inflation. That may or may not happen depending on where your home is and the interest rate environment at the time of sale.

The reality is the areas most likely to enjoy price appreciation are also the areas where $250,000 homes do not exist. Homeownership is best suited for property in the $500,000 and up range. The property ladder is broken in that you can’t sell your bungalow and move up into a more substantial home in the same city because there aren’t any buyers for the first rung on the ladder anymore. They rent because they don’t qualify to buy. You have to be willing and able to rent that starter home and still have the capital to move up to the more substantial home to climb the property ladder in the same metro area these days.

Gayle said:

“They both will hold thousands of people and I understand one is low income housing. They are completely out of character with local ambience”

Towns and cities all over the country receive federal funds (carrots) for various programs. The Federal govt, under the Obamunist regime, have used Census data to identify overly white, Christian, affluent neighborhoods and threatened to stop those funds (stick) if they do not diversify these areas by building tax payer subsized housing, usually low rise ghetto apartments. In my city they have changed zoning laws to make this happen. About three miles from my house they changed a former industrial/business zone that was filled with decades old, mostly family run businesses to multi family residential apartments. These businesses were going concerns still doing well and paying taxes.

My advice is to either refuse to participate in the Census or self identify as black or some other minority. If it’s ok for Elizabeth Warren and Rachel Dolezal and countless others to self identify as something they are not, it’s damn sure ok for me to! Besides, it’s entertaining as hell to fuck with the census goons they send around to find out why you haven’t replied. Just don’t talk about anything that pertains to the census form like family, roommates, etc. because if you mention wife, husband or similar they write that down and reply for you.