Guest Post by Jesse Columbo

This article is Part I of a series that explains why U.S. household wealth is experiencing a dangerous bubble, why this bubble is heading for a powerful bust, and how to preserve and grow your wealth when this bubble inevitably bursts.

This series of articles will cover the following key points:

- How inflated household wealth currently is compared to historic levels

- What forces are driving household wealth to such extreme levels

- A look at the underlying components of household wealth and why they are inflated

- A look at the growing bubbles in equities, housing, and bonds

- How the household wealth bubble is driving consumer spending

- How the wealth bubble contributes to our artificial economic recovery

- How the wealth bubble is creating a temporary surge of inequality

- How the wealth bubble will burst

- How to preserve your wealth when the wealth bubble bursts

Part I: U.S. Household Wealth Is In A Bubble

In most people’s minds, any increase in wealth is a good thing. Surely, only a misanthrope would argue otherwise, right? Well, in this article series, I’m going to make the unpopular argument that America’s post-Great Recession household wealth boom is actually a very dangerous phenomenon.

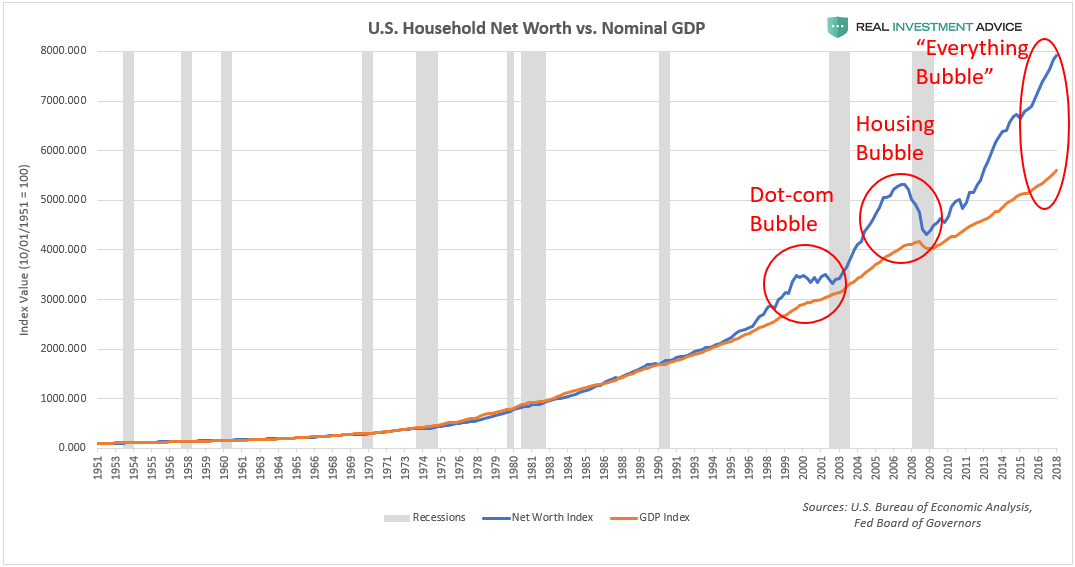

Since the financial crisis in early-2009, household wealth has surged by nearly $46 trillion or 83 percent to a record $100.8 trillion. As the chart below shows, the powerful increase in household wealth (blue line) has far exceeded the growth of the underlying economy, as measured by the GDP (orange line). Household wealth should closely track the economy, as it did during the 20th century until the extreme boom-bust era that started in the mid-to-late 1990s.

When household wealth tracks the growth of the economy, it’s a sign that the wealth increase is likely organic, healthy, and sustainable. When household wealth far outpaces the growth of the underlying economy, however, that is a tell-tale sign that the boom is artificial and unsustainable. The last two times household wealth growth exceeded GDP growth by a large degree was during the late-1990s dot-com bubble and the mid-2000s housing bubble, both of which ended in tears. The gap between household wealth and the economy is far larger today than it was in the last two bubbles, which means that the coming reversion or crash is going to be even more painful, unfortunately.

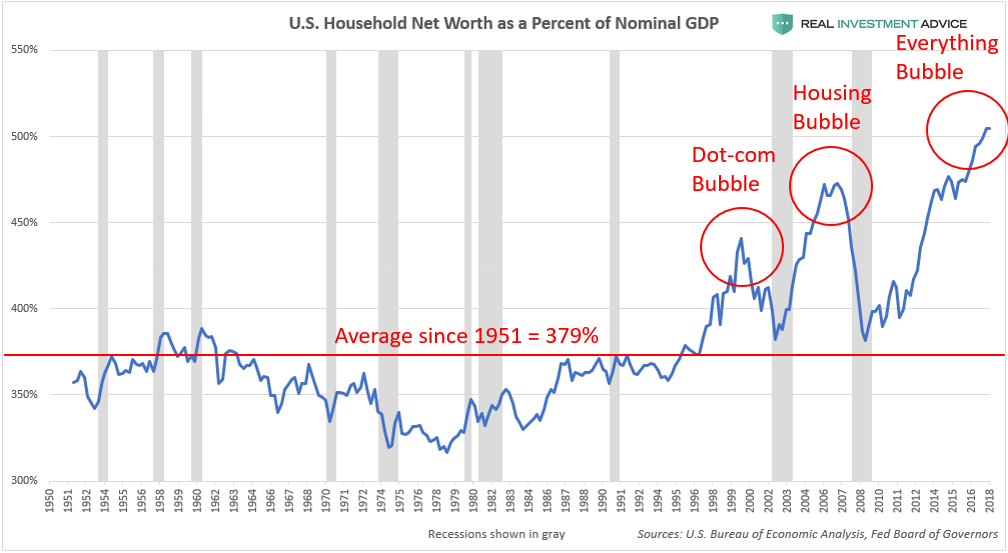

Another way of visualizing the household wealth bubble is to plot it as a percent of GDP, which paints the same picture as the chart above. U.S. household wealth is currently 505 percent of the GDP, which is even more extreme than the housing bubble’s peak at 473 percent, and the dot-com bubble’s peak at 429 percent. Household wealth has averaged 379 percent of the GDP since 1951, so the current 505 percent figure is completely out of line, which means that a violent reversion to the mean (aka, another crash) is inevitable. To make matters even worse, the 379 percent average figure is skewed upward by the anomalous boom-bust period that began in the mid-to-late 1990s. When U.S. household wealth comes crashing down again, there is a very good chance that it will overshoot below its historic average due to how stretched it has become during the current bubble.

What is driving the current U.S. household wealth bubble and why is it happening? The answer lies squarely with the U.S. Federal Reserve and its actions during and after the Global Financial Crisis. During the Crisis, household wealth plunged as stocks, housing prices, and bonds (aside from Treasuries) cratered. These aforementioned assets make up the bulk of household wealth, so bull markets in stocks, housing, and bonds lead to bull markets in household wealth and vice versa. When household wealth plunges as it did in 2008 and 2009, consumers pare back their spending dramatically, which leads to even more economic pain.

In an attempt to pull the economy and financial markets out of their deep-freeze, the Federal Reserve cut interest rates to record low levels and launched emergency monetary stimulus policies known as quantitative easing or QE. QE basically entails creating new money out of thin air (this is done digitally) and using the proceeds to buy mortgage-backed securities and Treasury bonds with the idea that the massive influx of liquidity into the financial system would indirectly find its way into riskier assets such as stocks. Even though the Fed only has two official mandates (maximizing employment and maintaining price stability), boosting asset prices essentially became their unspoken third mandate after the 2008 financial crisis.

As former Fed chairman Ben Bernanke wrote in a 2010 op-ed in which he explained (what he claimed to be) the virtues of the Fed’s new, unconventional monetary policies:

And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.

While the idea of having a central bank like the Federal Reserve boost asset prices to create an economic recovery may seem clever and admirable, it is terribly misguided because asset booms driven by central bank intervention are overwhelmingly likely to be unsustainable bubbles rather than genuine booms. Central bank-driven booms are very similar to sugar highs or highs from hard drugs – a crash is inevitable once the substance wears off. When central banks interfere in markets, they create mass distortions and false signals that trick investors into believing that the boom is legitimate, even though it’s not.

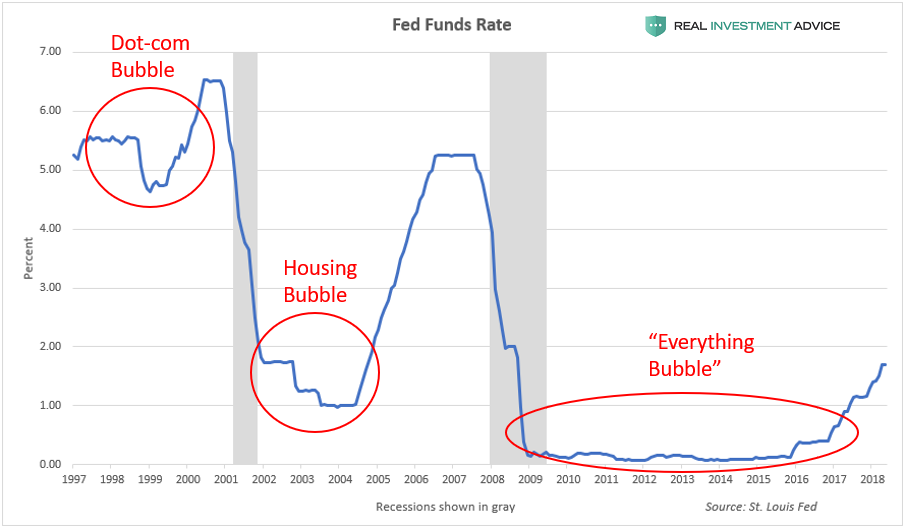

The chart below shows the Fed Funds Rate, which is the interest rate that the Fed raises and lowers in order to steer the economy. When the Fed holds rates at very low levels (which keeps borrowing costs in the economy low), dangerous bubbles form in asset prices and the overall economy. When the Fed ultimately raises rates, the bubble pops, which results in stock bear markets and recessions. The dot-com and housing bubbles formed during periods of low interest rates and popped when interest rates were raised.

What is terrifying is the fact that interest rates have remained at record low levels for a record length of time since the financial crisis, which means that the current market distortion and coming crisis will be even more extreme than the last two. Remember how extreme the current household wealth bubble looked in the two charts shown earlier in this piece? Well, that is certainly no coincidence: it is a direct result of the extremely loose monetary conditions over the last decade.

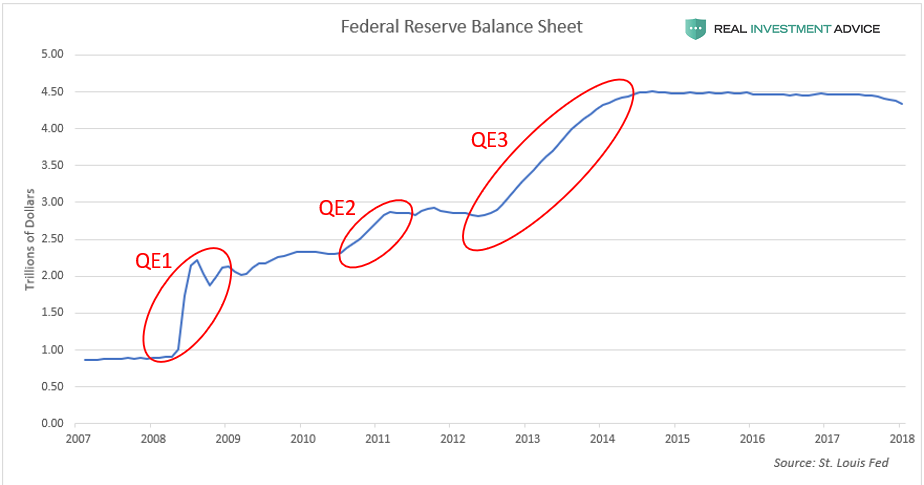

This next chart shows the Federal Reserve’s balance sheet, which shows the assets purchased by the central bank during its QE programs. Each QE program led to an increase in the Fed’s balance sheet and corresponding surge in asset prices. The three QE programs caused the Fed’s balance sheet to expand by over $3.5 trillion to a peak of approximately $4.5 trillion. Since late-2017, the Fed has been attempting to shrink its balance sheet (this is known as quantitative tightening or QT), which has roiled the financial markets.

Summary – Part I

To summarize, we are currently experiencing an explosion of wealth on a scale that has never been seen before. Unfortunately, it’s not the good kind of wealth explosion, but the bad kind – the kind that precedes wealth implosions that lead to deep economic recessions and depressions. While most people are cheering this boom on and are delighted by the return to prosperous times, they have absolutely no clue what is driving it or the fact that it will prove to be fleeting and ephemeral.

Please stay tuned for Part II, where I will discuss the underlying components of U.S. household wealth (stocks, bonds, etc.) and provide even more evidence that they are experiencing speculative bubbles in their own right.

If you are like most investors, the U.S. household wealth bubble means that your own investments, wealth, and retirement fund are extremely inflated and exposed to grave risk of another crash. Most investment firms have absolutely no clue that another storm is coming, let alone how to navigate it. Clarity Financial LLC, my employer, is a registered investment advisor firm that specializes in preserving and growing investor wealth in precarious times like these.

Please click here to contact us so that we can help protect your hard-earned wealth.

The author wrote,

“When central banks interfere in markets, they create mass distortions and false signals that trick investors into believing that the boom is legitimate, even though it’s not.”

It’s a CONfidence game!

The CON is always directed at the digital herd to move the heard one way or another when IT is time to cash IN and OUT.

Excellent break down of the historic theft and the Greatest Economic Depression of ALL TIME!

In other words it’s time to Cash out while you still can.

Having had to recover in 1984 with the beginning collapse of the third largest steel corporation in the world and losing that 11 years accumulated towards 30 year retirement I have watched what has gone on in realeastate , stocks and bonds and have come to the conclusion that the tried and true investment strategies of get in Watch wait sell take your small profit pay your tax and move on . As for the equity build up of value in housing will only effect you in your assessment regarding property tax or if you are using your equity as an ATM card . If you are doing the later prepare for a rough ride into a wall or out in the street at the worst !

As for bail outs for those living beyond their means TFB

ASSUME THE POSITION PREPARE TO ACCEPT THE PUNISHMENT !

Boat Guy, said

“As for bail outs for those living beyond their means TFB

ASSUME THE POSITION PREPARE TO ACCEPT THE PUNISHMENT !”

Really??

I wish that’s what we would have said to the “Too Big To Fail” banks and corporations that got BAILED out in 2008-2009!

Instead more debt was added to each U.S. citizens burden of the government debt so that many of these transnational corporations and banks could buy up their competition, then for past 8 years with the Fed’s Q.E. 0% interbank lending fueled the ALL TIME highs in equities….

Get the fuck outta here with your virtue signaling holier than thou bullshit.

Holier than who or what , l just learned the lesson 40 years ago the economic game in America was rigged and sliding into a debt rigged system of crony capitalism controlled by the elite circle jerk of Wall Street (the banks) to K-Street to Capitol Street . I was told TFB when the federal assurance of vestige in a retirement plan was an unsecured debt discharged on bankruptcy . Then the group mentioned gave average a real plan 401k that we control so let’s dissect it you put up 100% of the funds take 100% of the risk accept 100% of any losses and fees incurred and in the end recieve 30% of any gains while competing against the Circle Jerk manipulating the stock market thru flash trading and buy back stock moves with currency developed out of thin air devaluing every dime you ever saved with manuiplayed intrest rates as the manipulators engineer bubbles convincing people to use the inflated equity value of their homes like an ATM card . My wife and I witnessed this going on and called it right out that this was crazy for average people to engauge in . Yes there is bull shit about but not from me !

It keeps going until the rest of the world feels it is prepared to let us Venezuela.

Nice article but Inthink the author should have provided the link below as well as his legal obligation of affiliate disclosure. Since this article was also an advertisement….here is their form adv2 from the SEC

https://www.adviserinfo.sec.gov/IAPD/content/ViewForm/crd_iapd_stream_pdf.aspx?ORG_PK=150661

This is how you look up advisory firms. What I found was the following: no guarantee to accuracy…

The firm is an advisory firm with 7 total employees.

5 of which are in advisory roles.

3 hold insurance licenses (Connie Mack is related to firm owner and may be the person the advisors refer for insurance product sales or planning as needed I assume).

Approx 850 accounts for $346m in assets

They manage assets of nearly $300 million mostly at Fidelity and TD Ameriprise.

They have approx 350 clients and approx 40 considered high net worth

The high net worth clients make up approx 40% of their total assets.

They have approx 5 institutional clients (non human, corporate etc)

Seems they don’t do wrap accounts but the form says they hold wraps at Fidelity of $244m (I am still confused)

They primarily use Exchange Traded Funds vs mutual funds (good thing in my opinion,)

No legal or compliance disclosures (a great thing).

They are based in Texas and operate in approx 4 other States

They are goals based vs risk based which everyone should understand more about! (Age has nothing to do with risk is a good starting point!)

Continue your own due diligence from here. I look forward to his second part article.