Guest Post by David Stockman

There is nothing more substantive than Bernanke’s original finger-in-the-air proposition that the Fed needed a 200 basis point cushion in the inflation rate in order to steer the economy clear of the dreaded 0.0% inflation line, the other side of which allegedly amounted to a black hole of deflationary demise.

But here’s the thing. There is not a shred of historical evidence that the US economy needs a 2.00% inflation guardrail to thrive, or any fixed rate of inflation at all.

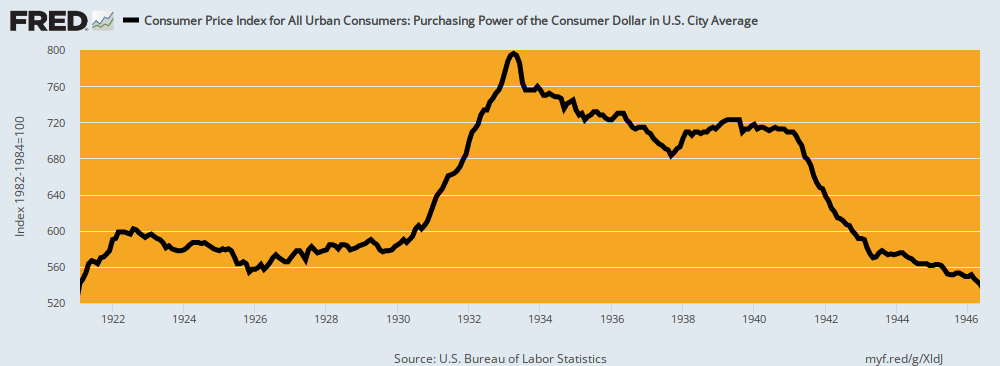

For instance, even during the most difficult period of the 20th century—from 1921 to 1946 when the US economy experienced the Roaring Twenties boom, the Great Depression bust and the WWII rebound—there was abundant net economic growth over the period as a whole, accompanied by zero inflation.

In fact, the US economy nearly tripled in size during that quarter-century period. Real GDP expanded at a robust 3.64% per annum rate, and real GDP per capita rose by 2.55% per annum.

By contrast, between the 2007 pre-crisis peak and 2021, real GDP grew at only half that rate (1.72% per annum), while per capita real GDP increased by just 1.04% per year. That was just two-fifths of the rate of annual gain during 1921-1946.

Needless to say, it didn’t take any 2.00% inflationary guard rails to generate the salutary outcomes cited above for 1921-1946. The CPI index shown below posted at 542 in February 2021 and 541 a quarter century later in May 1946.

Purchasing Power of the Dollar, 1921 to 1946

As it had unfolded, there was zero CPI inflation during the Roaring Twenties; a severe deflation during the Great Depression, which merely reversed the war inflation of 1915-1920; and then a return to the 1921 price level during the booming but regimented economy of WWII.

Still, by the spring of 1946 the dollar’s purchasing power was 100% of what it had been in early 1921. It had not taken any net inflation at all to generate a near tripling of the nation’s economic output.

The implication is straightforward. To wit, the Fed doesn’t need a pro-inflation target of 2.00% per annum. Nor does it need any of its other macroeconomic targets for unemployment, jobs growth, actual versus potential GDP or the rest of the Keynesian policy apparatus. All of those variables are the job of the people interacting on the free market, producing whatever outcomes their collective actions happened to generate.

Indeed, macro-economic outcomes are not properly the business of the state at all. The Fed’s job is far more narrow. As originally conceived by its great architect, then Congressman Carter Glass, its mission was to keep the purchasing power of the dollar as good as the gold to which it was to be linked, and the banking system liquid and stable, as driven by the free market of borrowers and lenders.

As we have explained on other occasions, Congressman Glass called this a “bankers’ bank” and the term could not be more diametrically opposed to the central planners’ bank of Greenspan, Bernanke, Yellen, Powell and Brainard.

As Carter Glass saw it, no academician needed to stick his finger in the air and divine an inflation target. Nor did any modeler need to goal-seek his/her equations until they suggested the optimum U-3 unemployment rate relative to an arbitrary inflation target.

The fact is, the free market operating with sound gold-backed money was never inflationary. In that context, interest rates were also not a policy “tool” of the central bank, but the result of a market-clearing balancing of supply and demand.

As Carter Glass had arranged it, the Fed was not allowed to own government debt, nor did it have an activist arm now known as the FOMC empowered to intervene in the money and capital markets by buying and selling debt securities.

To the contrary, its avenue of operation was the discount window at the 12 regional Federal Reserve banks. The latter were authorized to advance funds to member banks, but only at a penalty spread above the free market interest rate, and also only on the basis of sound, self-liquidating collateral in the form of commercial paper that matured within a matter of months.

Given this mechanism, the dynamics of Fed policy were the opposite of today. Under the Glassian arrangement, the Fed’s balance sheet was the passive consequence of free market activity by commercial bankers and main street borrowers, not a mechanism to proactively steer the level of aggregate commerce and business activity.

Accordingly, the Fed’s value added stemmed not from wild-ass guesses about the inflation rate by PhDs like Lael Brainard, but from the grunt work of green-eyeshade accountants. Their job was to verify that bank loan collateral presented for funding at the discount window represented the obligations of sound borrowers, not speculators and high flyers, who would reliably repay under the terms of the underlying bank loan, thereby ensuring that the Fed’s discount loans would be repaid at term, too.

What this meant was that the Fed’s balance sheet was intended to reflect the ebb-and-flow of decentralized commerce and production on main street, not a centralized judgment by 12 people gathered on the banks of the Potomac about whether inflation and unemployment were too high, too low or just right.

That is to say, under the bankers’ bank arrangement the free market put an automatic check on CPI inflation. That’s because unsound speculative loans could not be easily made in the first place, since they were not eligible for discount at the Fed window.

And if demand for even sound loans got too frisky, interest rates would rise sharply, thereby rationing available savings until more of the latter could be generated or demand for the former was curtailed.

Editor’s Note: The truth is, we’re on the cusp of an economic crisis that could eclipse anything we’ve seen before. And most people won’t be prepared for what’s coming.

That’s exactly why bestselling author Doug Casey and his team just released a free report with all the details on how to survive an economic collapse. Click here to download the PDF now.

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

Inflation wouldn’t exist in a free-market society. There would be competition for currencies, instead of arbitrary cartelized fiat thievery instruments of exchange, as there are now. End the central bank fiat currency monopoly. End the Fed. And decouple the U.S. from the BIS, IMF, World Bank (and frankly, from all of the other international alphabet agencies).

.

MORE: https://www.lewrockwell.com/?s=competing+currencies

.

What To Do While Waiting to End the Fed

https://mises.org/library/what-do-while-waiting-end-fed

MORE: https://mises.org/search-mises?search=competing%20currencies

Yeah, but the FED gets to steal at least 2% of everybody’s money every year.

Thats too sweet a deal to pass up.

Forward Flat Rate Inflation Calculator

Calculates the equivalent value of the U.S. dollar in any year from 1914 to 2023. Calculations are based on the average annual CPI data in the U.S. from 1914 to 2022.

$127.47 in 2023 has the same purchasing power as $100 in 2013. The Fed stole over one quarter of your money in 10 years at 2%

$100 with an average inflation rate of 2% has the same purchasing power as $148.59 after 20 years. The fed has stolen almost half your money in 20 years.

$100 with an average inflation rate of 2% has the same purchasing power as $220.80 after 40 years. That money you put away in your 401K when you started working is gone from inflation, plus some more of the money you earned later in life.

Now look at Bidenflatioin at 8%, which is a lie as it is certainly something in the double digits, ten years from now.

$100 with an average inflation rate of 8% has the same purchasing power as $215.89 after 10 years.

IF there were sound currencies in circulation, gold, silver, nickel, copper,aluminum, platinum, palladium, any or all would work for different denominations, paper redeemable for the aforementioned coin, the Fed and all other central bank racketeers rice bowls would be broken !!!

I’m the guy who started the Boycott American Women blog, and i admit i was quite a woman hater but i went thru a spiritual awakening and now I’m trying to heal women instead of hurt them. Anyway if you wanna ask me questions or do an interview, just DM me on instagram at tantrahealermaster

Just be sure to keep it in yer pants, Corey. Creating a web site dedicated to hate of anything is a big red flag for me.

Good luck on your spiritual journey.