Sometimes I wish I could just passively accept what my government monarchs and their mainstream media mouthpieces feed me on a daily basis. Why do I have to question everything I’m told? Life would be much simpler and I could concentrate on more important things like the size of Kim Kardashian’s ass, why the Honey Boo Boo show was canceled, the Victoria Secret Fashion Show, whether I’ll get a better deal on Chinese slave labor produced crap on Black Thanksgiving, Black Friday, or Cyber Monday, fantasy football league standings, the latest NFL player to knockout their woman and get reinstated, Obama’s latest racial healing plan, which Clinton or Bush will be our next figurehead president, or the latest fake rape story from Rolling Stone. The willfully ignorant masses, dumbed down by government education, lured into obesity by corporate toxic packaged sludge disguised as food products, manipulated, controlled and molded by an unseen governing class of rich men, and kept docile through never ending corporate media propaganda, are nothing but pawns to the arrogant sociopathic pricks pulling the wires in this corporate fascist empire of debt.

I’m sure my blood pressure would be lower and my mood better if I just accepted everything I was told by my wise, sagacious, Ivy League educated, obscenely wealthy rulers as the unequivocal truth. Why should I doubt these noble, well intentioned, champions of the common folk? They’ve never misled us before. They would never attempt to use two highly publicized deaths as a lever to keep black people and white people fighting each other and not realizing all races are now living in a militarized police surveillance state supported by the one Party. They would never use their complete control over the financial, political, judicial, and media organisms to convince the masses that voting for one of their hand selected red or blue options will ever actually change anything. They would never engineer the overthrow of a democratically elected government, cover up the shooting down of an airliner, and attempt to blame their crimes on the leader of a nuclear power in their efforts to retain a teetering global empire. They would never overthrow or wage economic warfare on countries that don’t toe the line regarding the continued dominance of the petrodollar in global commerce.

Sadly, I’m cursed with a mind that questions everything and trusts no one in authority or associated with the status quo. It’s the reason I don’t read newspapers or watch mainstream media television entertainment propaganda, disguised as news. It’s the reason I will never vote in a national election again. The lesser of two evils is still evil. I’m skeptical of every piece of data fed to the sheep by the government apparatchiks working for the state. The faux journalists being paid millions by one of the six corporations controlling the media and dependent upon the government, Wall Street bankers, and mega-corporations for their advertising revenues regurgitate whatever they are told by those pulling the purse strings. The mainstream media are nothing but propaganda peddlers for the Deep State and truth telling is prohibited in their world of deception, debt, and denial. Their job is to sustain, enhance, and further enrich the status quo by engineering consent through what they report and what they do not report. The true ruling powers who operate in the shadows behind the scenes are men of power, wealth, status and education who truly believe they are better equipped to consciously manage and manipulate the public mind to achieve their ends. They are disciples of the Edward Bernays School of deception, manipulation and propaganda.

“If we understand the mechanism and motives of the group mind, is it not possible to control and regiment the masses according to our will without their knowing about it? The recent practice of propaganda has proved that it is possible, at least up to a certain point and within certain limits.” – Edward Bernays

The Nazis were pikers compared to the technologically savvy Madison Avenue maggots and Silicon Valley snakes who mold the opinions, tastes, and beliefs of the iGadget addicted, vapid, unintelligent, unquestioning, zombie-like masses who beseech to be led, told what to do and what to believe. A vast swath of the population don’t read books or even know how to read above a grade school level. They couldn’t write a coherent paragraph if their life depended upon it. But they can twitter, text, Instagram, and facebook at the speed of light. Try walking down any street in an American city without some iGadget distracted oblivious moron bumping into you. The addicting nature of today’s technology is being used by the ruling elite to monitor, control, and make you respond the way they choose.

Facebook, corporate media organizations, quasi-government organizations, and the NSA are creating a corporate totalitarian state where the slaves willingly sacrifice their privacy, liberty and freedom for mindless entertainment and distractions. The 21st Century totalitarian state captures your political beliefs, daily activities, habits, interests, spending behaviors, organizational associations, love life, pictures, psychological makeup, and fears from your own postings on the internet. With the right algorithms they can uncannily predict how you will react to different situations and messaging. They can also uncover threats to the status quo. Under the guise of keeping you safe from terrorists they are actually ferreting out subversives and radicals who refuse to conform to their idea of a good citizen slave. We will all be subject to our own Room 101.

Dan Kaplan in his recent article about Facebook as a tool for totalitarianism lays out the extreme threat to our future:

Today’s totalitarian demands a more subtle way to influence cultural and political sentiment. But if you got your hands on an algorithmically filtered newsfeed? One that could control the stories people see every day and influence their emotions across geographic, political and economic lines? You’d be in business.

But then there was the mood-influence study that scandalized us for a couple of weeks this year. Facebook changed the tone of content showing up in people’s feeds to test the impact it could have on their moods. The results, not too surprisingly, suggested that Facebook has the power to manipulate sentiment at scale.

Given how easy it is to scare people about the scary-seeming-but-actually-low-risk Ebola, and how dumb we all get when we are afraid, it is not crazy to think that under the wrong circumstances — like one or two more mass-scale terrorist attacks on major cities — modern democracy gives way to something akin to 1984.

If Big Brother were to seize the reins of power, sure, he’d use the cable news the way it’s being used today. But Facebook’s data maw, targeting power and sentiment-manipulation capabilities would be far more insidious. Whether this is what we become or not comes down to the future we choose to build.

The saddest part of this episode of mass delusion, mass confusion, and mass media collusion is that even though we are moving towards Orwell’s totalitarian vision of society, thus far, technology, triviality and an unending array of distractions have lured the masses into passive preoccupation with egotistical pleasures. We’ve been persuaded to love our servitude while drowning in a sea of irrelevance, diversions, and trifles. We continue to amuse ourselves to death while forging our own chains of debt and yielding to the direction of an all-powerful welfare warfare surveillance state that promises to protect us from phantom threats while actually abolishing our rights, freedoms, and liberties. No coercion necessary. We have been trained to love our servitude.

“A really efficient totalitarian state would be one in which the all-powerful executive of political bosses and their army of managers control a population of slaves who do not have to be coerced, because they love their servitude.” – Aldous Huxley – Brave New World

Arrogance, Desperation, Lies & Truth

“Facts do not cease to exist because they are ignored.” – Aldous Huxley

The level of data massaging by the government and their co-conspirators on Wall Street and in the corporate media is a futile attempt at a happy ending that will never come to fruition. The intensity and relentlessness with which the state and its quasi-state minions attempt to paint a false picture of economic recovery is equal parts arrogance and desperation. The arrogance is a function of successfully pulling off the greatest heist in world history from 2003 through 2008 with no adverse consequences, no criminal charges, no penalties for their crimes, and more power and wealth than they had prior to 2003. The only way to stop sociopaths is to throw them in jail or kill them. In our dystopian paradise of greed, they were rewarded with trillions in rescue packages by their cohorts in crime at the Federal Reserve and in Congress. They’ve paid themselves billions in bonuses for gorging at the Federal Reserve trough of QE and ZIRP. The desperation is borne from the fact that after $7.5 trillion of debt added by the Federal government and $3.5 trillion of debt created by the Federal Reserve since 2009, the Greater Depression for average Americans deepens by the day.

The men pulling the strings behind the scenes are drunk with power and their hubris allows them to believe their own infallibility and blinds them to the dire consequences for our country when their debt Ponzi scheme fails. But, as we grow ever closer to the day of reckoning, they will use every means at their disposal to paint a positive picture, regardless of the facts and reality for the average person. The examples of twisting, distorting and outright lying about the economic reality of our times are endless. These are some of the major false storylines peddled by our benevolent corporate fascist leaders:

The BLS reported 321,000 jobs added in November and the unemployment rate at 5.8%. Jobs are plentiful, based upon these statistics.

A skeptical critical thinking individual might ask a few questions or point out a few inconvenient facts the government purveyors of propaganda might not want us to ponder:

- The non-manipulated, non-seasonally adjusted number of jobs in November FELL by 270,000. The BLS added 600,000 jobs as an adjustment to achieve the headline grabbing result.

- If the jobs market is so good, why is the labor participation rate at a 30 year low of 62.8%?

- Since 2007 the number of working age Americans has risen by 17 million, while the number of employed has risen by less than 1 million, but the unemployment rate is about the same.

- Why would almost 14 million working age Americans leave the labor force since 2007 if the economy is booming and jobs plentiful, with 1.2 million leaving in the last 12 months?

- Why would payroll tax receipts be flat with last year if millions of new jobs have been created?

- If the country has really added 8 million jobs since 2010, how could real median household income FALL by 2.3%?

According to the government reported figures, the economy hasn’t been this strong since 2007. GDP has supposedly grown at greater than 4% over the last two quarters.

Anyone who is sentient knows consumer spending accounts for 68% of GDP. Capital investments that lead to long term prosperity continue to decline as a percentage of GDP from 20% in 2000 to 16% today. We’ve chosen consumption and financialization over savings and investment. This fact leads to some observations:

- If GDP has actually grown by 20% since 2008 how does this correlate with a 6.9% decline in real median household income?

- GDP has been goosed by a $69 billion increase in government spending, with the majority going to the military industrial complex. ISIS has been a godsend for our GDP and arms dealer profits.

- GDP was increased retroactively by $500 billion last year based on a new way the government accounts for intangibles.

- The surge in consumer expenditures over the last two quarters has been in the purchase of services. The higher costs for Obamacare are a boon for GDP. Are they a boon for your bank account?

- The trade deficit has fallen as exports of petroleum products have temporarily provided a boost to GDP. The collapse in oil prices will reverse that trend rapidly.

According to the quasi-governmental mouthpieces at the Conference Board, consumer confidence is near a 5 year high, reflecting what should be robust spending.

So we are told by the representatives of corporatism that we are confident about the economy and the future. How does that measure up to the facts on the ground:

- Black Friday weekend sales collapsed by 11% versus the previous year. As the pundits tried to blame it on on-line sales (10% of total retail sales), Cyber Monday also proved to be a dud.

- If the average person is confident about the future and happy with their economic circumstances, why did they just vote to throw out the bums in November?

- If consumers are confident, why have real retail sales, excluding subprime debt goosed auto sales, been flat for the last three months and up only 1% in the last year?

- If consumers are so confident, why are credit card balances still $138 billion BELOW where they were in 2008? If all these new jobs are being created why is credit card debt lower than it was in mid-2010? Maybe consumers are so desperate they are using credit cards to pay utility and tax bills and not using them for frivolous Chinese crap at big box retailers.

- The increased spending at grocery stores and restaurants is driven by food inflation, not foot traffic. Discretionary spending at furniture, electronics, and sporting goods stores is flat.

- Department store sales continue to fall. Sears and JC Penney teeter on the verge of bankruptcy. Delia’s is liquidating and Radio Shack isn’t far behind. The major chains have completely stopped building new stores. The great bricks and mortar unwind relentlessly plods forward. In addition, online growth is stalling as states implement sales taxes.

According to the government, the deficit was ONLY $483 billion in 2014.

This is a real doozy. Obama has been touting how he has cut the deficit through his wise management of the budget. This is where government accounting is used by apparatchiks to mislead the public and obscure the truth. A few pertinent facts are always left out by the politicians touting deficit reduction:

- Because of the budget impasse in 2013, the Federal government stopped updating the national debt on a daily basis, but we know from when they started counting again, the debt went up by $2.3 billion per day. Therefore, the national debt on October 1, 2013 was approximately $17.038 trillion. On October 1, 2014 the national debt was $17.875. Therefore, the national debt went up by $837 billion in 2014. Just a smidge higher than the reported deficit of $483 billion.

- Interest is not paid on reported deficits. It’s paid on the national debt, so the massaged, manipulated and made over deficit is meaningless. The national debt was always slightly higher than reported deficits, but in the last few years the deviation has grown to a Grand Canyon size.

- The deficit number has been artificially lowered by nothing other than accounting entry hocus pocus. The Federal Reserve increasing its balance sheet to $4 trillion out of thin air creates approximately $80 billion of phantom interest profits that are paid to the Treasury. Why don’t they increase their balance sheet to $40 trillion and eliminate deficits all together?

- The biggest accounting scam is Fannie and Freddie. Just as the Wall Street banks have created fake profits through accounting entries regarding future losses, Fannie and Freddie have gone the extra mile in helping fake deficit reduction. These bloated insolvent government run pigs required a $187 billion taxpayer bailout in 2009. Amazingly, when you allow criminals to value their assets at whatever they choose, phantom profits flow like honey.

- These two horribly run institutions of fraud “generated profits” of $129 billion in 2014 which were “paid back” to the Treasury. That is four times more than Apple or Exxon’s profits during a non-existent housing recovery. Why are their stocks trading at just over $2 per share if they are generating vastly more profits than they were in 2007 when their stocks were north of $70 per share? It’s because the profits are fake. Everyone knows it, but the Federal Deficit is reported $129 billion lower because these insolvent entities pretended to pay the taxpayer back. Accounting entries do not reduce deficits. Spending less than you generate in revenues reduces deficits.

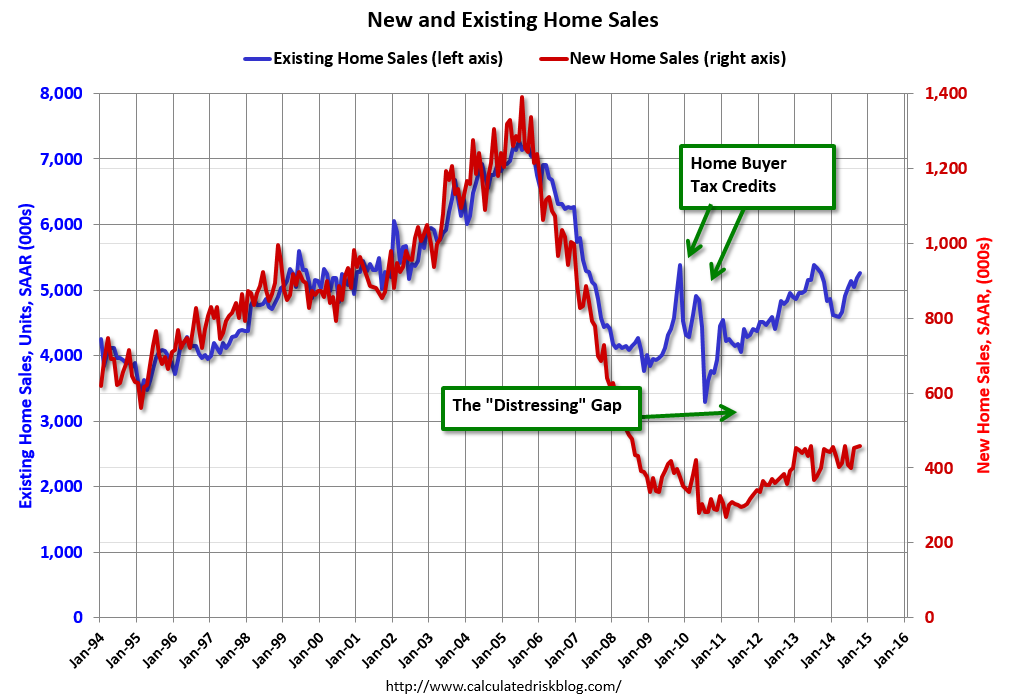

According to the government, we’ve experienced a strong housing recovery since 2010.

The supposed housing recovery storyline continues to be beaten like a dead horse by the Wall Street media (CNBC) and the shills at the NAR. Anyone with a functioning brain (eliminates CNBC bimbos, hacks, and Ivy League economists) can see there has been no real housing recovery:

- The 24% rise in home prices (Case Shiller Index) since the 2012 low has been nothing more than a Wall Street hedge fund/Federal Reserve scheme to elevate prices and make Wall Street bank balance sheets less insolvent. Wall Street banks withholding foreclosures from the market while Wall Street hedge funds (Blackstone) use free money from the Fed to buy up housing and rent it out to former homeowners has enriched the .1% while destroying the dream of home ownership for millions.

- The percent of first time home buyers remains near record lows, while speculators, flippers, hedge fund managers, and rich Chinese businessmen make up a record number of purchasers. The fact this is a fake housing recovery is proven by mortgage applications to purchase a home sitting at 1995 levels and 30% below 2009 recession lows. Maybe the fact real median household income is also at 1995 levels, real wages keep declining, and labor force participation is at 1978 levels has something to do with real people not being able to purchase a home.

- Even with the artificial hedge fund demand, existing home sales are lower than 2013 and languishing at 1999 levels. They are still 25% below 2005 levels, despite the lowest mortgage rates in history. New home sales are a disaster, with no appreciable increase in two years. Apartment construction has far outpaced single family housing construction. After a five year housing recovery, new home sales languish at levels seen at the bottom of our last six recessions. New home sales are 65% below the 2005 peak and at levels seen in the early 1960’s when there were 130 million less people living in the country.

According to the corporate media, the auto market is hitting on all cylinders with annual sales of 16.4 million, the highest since 2006.

Pretending to sell automobiles to people without the means to pay you for the automobile is always a good business idea. Of course, when you have Ally Financial and the rest of the Wall Street banking cabal doling out 7 year 0% loans and subprime auto loans like candy, it’s easy to move inventory. The temporary boost to GDP by issuing more bad debt always works out in the long run. Right?

- If the auto business is booming why have GM profits fallen from $9.2 billion in 2011 to $5.4 billion in 2013, and on course to fall to $4 billion in 2014? Record levels of channel stuffing produces sales gains, but no profits. Why is their stock 25% below its 52 week high and lower than it was in 2010 when it was IPO’d after being rescued by Obama?

- If the auto business is booming why are Ford’s profits falling by 35% versus last year and lower than they were in 2010? Why is their stock price 16% below its 52 week high and still 20% below its 2010 price?

- Auto loan debt is at an all-time high of $950 billion, up 33% since 2010 when the Fed, Wall Street, and the political class in the fetid D.C. swamp decided they needed new debt bubbles in auto loans and student loans to jump start our moribund economy.

- There are 65 million auto loans outstanding, and the average debt now stands at $17,352. Over 30% of auto “sales” are actually leases. The rest are financed over an average of 65 months. Virtually all new car sales are nothing more than 3 to 7 year rentals. It’s amazing what easy money from the Fed can produce.

- Over 31% of all new auto loans this year were to subprime borrowers. They now account for 36.5% of all outstanding auto loans. You become a subprime borrower by defaulting on previous debt obligations. In a shocking development, auto loan delinquencies surged by 13% in the last quarter, with subprime loan delinquencies skyrocketing by 18%. When has issuing billions of debt to subprime borrowers ever caused problems before?

- Only a University of Phoenix African Studies major is more of a subprime risk than the millions of ecstatic Escalade drivers cruising around our urban ghetto paradises. The average student loan debt is now $33,000. Until the Obama administration went Keynesian, student loan debt was primarily in the private sector. When Obama entered the White House total student loan debt was $620 billion and delinquencies totaled $50 billion. There are now $1.3 trillion of student loans outstanding, with the Federal government accounting for $830 billion and guaranteeing a large portion of the rest. Delinquencies have skyrocketed to $125 billion, as another taxpayer bailout beckons.

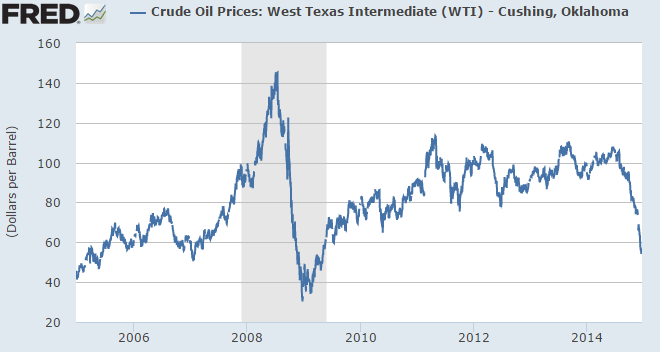

According to the corporate mainstream media pundits, the plunge in oil prices from $100 per barrel to $61 per barrel is unequivocally good for the economy. The shale oil boom has worked its magic and happy times are here again.

Sometimes you have to wonder whether the highly educated spokesmodels on the corporate mainstream media are really as vacuous and clueless as they appear or whether they are just paid to look pretty and mouth the corporate line. They seem incapable of comprehending the unintended consequences of various events. The collapse in oil prices is one of those events.

- There is no doubt that lower oil prices will lower the price of gas for the average American. Estimates say they will save $368 per year, which can be spent elsewhere. The highly paid shill economists who declare this will boost spending seem to be math challenged. Retail sales figures include gas stations. What isn’t spent there will be spent in another category, most likely healthcare or groceries as prices in both areas continue to escalate. It’s a zero sum game. No new spending will occur.

- The worldwide supply of oil has only increased marginally over the last few years. The U.S. shale boom has been offset by declines elsewhere (Libya, Iran, Mexico). The reason for the collapse is the same reason for the 2009 collapse – worldwide demand is contracting. Europe is in a depression. Japan is in a depression. Russia’s economy is contracting. China is decelerating rapidly. The U.S. demand is flat. The implications of another global recession after five years of central banks printing trillions of fiat currency are alarming to say the least.

- The cost to extract shale oil and transport it to a refinery capable of processing it is high. Honest analysts will tell you that a price of $70 to $80 is required to breakeven. Most companies don’t build breakeven into their plans. Bakken shale oil sells at a discount of about $14 per barrel due to the difficulty of extraction, transport, and processing. It is now selling for $47 per barrel. The number of permits for new rigs fell by 40% in November when oil was still selling for $75 per barrel. Do you think permits for new wells will fall at a price of $61 per barrel? Capital spending by the energy industry accounted for 33% of all capital spending in the last few years. I’m sure some other industry will pick up the slack. Right?

- It seems the shale oil boom has resulted in a few jobs being created since the 2010 recession trough. In fact the states where fracking is prevalent have accounted for all the job growth in the nation. I wonder if a shale oil bust will have any employment implications. There are 9.3 million jobs related to the energy industry across the country. The plunge in oil prices created by Saudi Arabia in the 1980s created a depression in Texas which contributed to the S&L crisis. This plunge will reveal who has been swimming naked in the high yield bond market and derivatives market.

These are just a few examples among a multitude of lies. Others include: stocks aren’t overvalued, gold isn’t money, inflation is good for you, and ISIS terrorists are an imminent threat to your way of life. Every feel good story fed to the masses by the oligarchs running this shitshow we call America is no different than the propaganda doled out by other infamous totalitarian regimes throughout history. We believe things because we’ve been conditioned to believe them. The crony capitalist oligarchs are intelligent enough to invent theories to explain how the world should work, but not intelligent enough to interpret their models correctly. When they act on their theories (Keynesianism), their actions appear to be those of a lunatic. Despite all evidence refuting their theories, their arrogance and hubris lead them to destruction. The collective insanity of this world is almost too much for a rational thinking person to grasp. The extremely wealthy men operating in the shadows will use every means at their disposal to retain power, enhance their wealth, and crush dissent.

“Being a card carrying member of the privileged class means never having to say I’m sorry, much less ‘not guilty.’ Power is doing what you want when you want, and consequences are for everyone else. Or perhaps these titans of modern industry and the halls of power are at heart just good natured bumblers, who in a genuine belief destroy lives and crash economies, while pursuing insane ideological assumption put forward by vested interests, all the while stuffing their pockets, and crushing all dissent with the political skills of a Machiavelli and the ruthlessness of Al Capone.” – Jesse

The two party system is nothing but a ruse designed to keep the people believing they have a say in how things are run in this country. Both parties support the military industrial complex. Both parties support the militarization of police forces around the country. Both parties support the mass surveillance of its citizens. Both parties do the bidding of their rich corporate and special interest benefactors. Both parties favor deficit spending for eternity. Both parties believe the government should expand its role in our everyday lives. Both parties do the bidding for and protect the Wall Street interests who really run this country. No more proof is needed than what has occurred over the last five years, as criminal Wall Street bankers were rewarded for their malfeasance with trillions of dollars from taxpayers and their puppets at the Federal Reserve. While we were allowing ourselves to be distracted, amused, entertained, and indebted, the oligarchs were busy conducting a silent coup.

“Let’s be clear about this, the oligarchs are flush with victory, and feel that they are firmly in control, able to subvert and direct any popular movement to the support of their own fascist ends and unslakable will to power.

This is the contempt in which they hold the majority of American people and the political process: the common people are easily led fools, and everyone else who is smart enough to know better has their price. And they would beggar every middle class voter in the US before they will voluntarily give up one dime of their ill-gotten gains.

But my model says that the oligarchs will continue to press their advantages, being flushed with victory, until they provoke a strong reaction that frightens everyone, like a wake-up call, and the tide then turns to genuine reform.” – Simon Johnson

The oligarchs have had a good run. The system cannot be reformed from within. The corruption runs too deep. The system is broken and can’t be fixed. There is no doubt in my mind that a collapse approaches which will make 2008/2009 look like a walk in the park. The anger, blame and retribution will sweep away the existing social order and replace it with something new. It will be up to the people to decide what happens next. We were warned two centuries ago by a wise man. Hopefully, we’ll get a 2nd chance.

“However political parties may now and then answer popular ends, they are likely in the course of time and things, to become potent engines, by which cunning, ambitious, and unprincipled men will be enabled to subvert the power of the people and to usurp for themselves the reins of government, destroying afterwards the very engines which have lifted them to unjust dominion.” – George Washington